Diesel Exhaust Fluid Market Size & Overview:

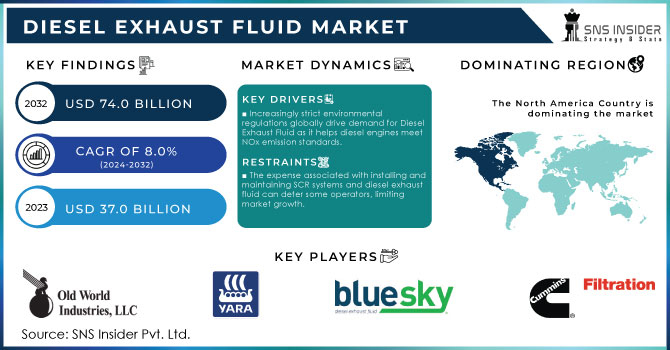

The Diesel Exhaust Fluid Market Size was valued at USD 39.96 billion in 2024, and is expected to reach USD 74.0 billion by 2032, and grow at a CAGR of 8.0% over the forecast period 2025-2032.

The Diesel Exhaust Fluid market has also faced large shifts due to requirements and technological changes. Large vats of diesel exhaust fluid in the form of a very pure liquid solution, mainly composed of deionized water and urea, play a pivotal role in reducing NOx emissions from diesel engines to stringent environmental standards. With major drivers for vehicular emissions reduction, diesel exhaust fluid experienced increased demand, mainly driven by the increasing penetration of SCR systems in the latest diesel engines. This has created a dynamic market landscape, driven by regulatory pressures and technological innovations.

Get More Information on Diesel Exhaust Fluid Market - Request Sample Report

Key Diesel Exhaust Fluid Market Trends:

-

Rising adoption of diesel vehicles and stringent emission norms are driving demand for DEF across commercial and industrial sectors.

-

Increasing use of Selective Catalytic Reduction (SCR) technology in diesel engines is accelerating DEF consumption globally.

-

Expansion of DEF distribution infrastructure, including fuel stations and bulk storage solutions, is improving accessibility for end-users.

-

Growing focus on reducing nitrogen oxide (NOₓ) emissions is boosting regulatory compliance-driven DEF adoption.

-

Technological innovations such as automated DEF dispensing systems and digital monitoring solutions are enhancing operational efficiency.

-

Supply chain challenges, including urea shortages and transportation bottlenecks, are influencing regional market dynamics.

Recent developments have served to bring about rapid progress within the diesel exhaust fluid sector. In May 2024, Rislone announced a new diesel exhaust fluid treatment that boosts the performance and longevity of systems with diesel exhaust fluid. This product spurs research in improving efficiency with diesel exhaust fluid solutions while addressing an ever-growing interest in the automotive industry. Rislone optimizes treatment to address the most prevalent diesel engine operators' challenges, including the degradation of diesel exhaust fluid over time and the challenges related to maintaining the efficiency of the SCR system.

Renewable diesel is increasingly becoming a factor in the diesel exhaust fluid market. In February 2024, an analysis discussed how diesel exhaust fluid and renewable diesel are reshaping the industry. This emerging renewable diesel market originates from bio-based feedstocks, which are considered a serious alternative to traditional diesel: being less carbon-intensive and having better compatibility with the existing engines. Thus, the shift towards renewable diesel has changed the established patterns of diesel exhaust fluid consumption.

Diesel Exhaust Fluid Market Drivers:

-

Increasingly strict environmental regulations globally drive demand for Diesel Exhaust Fluid as it helps diesel engines meet NOx emission standards.

The demand for Diesel Exhaust Fluid has increased as a result of the stringent environmental regulations implemented globally, imposing lower NOx emissions from diesel engines. Very strict regulatory standards have been set by the regulatory bodies of different regions to curb the environmental impact of diesel-powered vehicles and machinery and combat air pollution. For instance, the Euro 6 standards of the European Union and the U.S. The Tier 4 regulations of the EPA impose intense cuts in NOx emissions, mandating the automotive and industrial sectors to develop more advanced forms of emission control technologies. Diesel exhaust fluid plays a key role in this by facilitating the efficient conversion of NOx emissions from SCR systems to harmless nitrogen and water. One such example is that of trucks, wherein large truck manufacturers have made considerable investments in SCR technology as well as in the use of diesel exhaust fluid to comply with new emission standards. Similarly, construction and agricultural machines have deployed diesel exhaust fluid to meet the stringently high Tier 4 standards, highlighting how regulatory pressure has had them adopt such large scales of use of diesel exhaust fluid across the industry. Following the greatest focus on low levels of air pollutants, the effectiveness of diesel exhaust fluid increased and is currently known to make steady improvements within the fluid quality and system performance to enable compliance and efficiency in operations.

-

Innovations in Selective Catalytic Reduction (SCR) technology enhance diesel exhaust fluid efficiency and performance, boosting its market adoption.

Innovations in SCR technology enhanced the efficiency and performance of Diesel Exhaust Fluid, thereby widely gaining its usage in many sectors. NOx emissions of diesel engines have been particularly reduced through the use of diesel exhaust fluid in SCR systems, which, in turn, have been continually improved to become more effective and reliable. Other examples include advanced catalyst formulations and improvements in SCR system designs that have led to a more efficient process of NOx conversion. The engines now can reach emission levels that are well below those of their predecessors and at the same time achieve previous performance levels. Examples of innovations integrated into the SCR technologies include advanced sensors and control systems that improve the dosing of diesel exhaust fluid and work to achieve an overall better performance of the system with reduced consumption of diesel exhaust fluid, thereby reducing running costs. With advancements in SCR technology, compact and lightweight systems could now be used for much wider applications, from heavy-duty trucks to small machinery. The demand for advanced SCR systems from the automotive industry increases because manufacturers have stringent emission regulations and want to improve their fuel efficiency. The use of advanced SCR systems in construction and agriculture has helped meet environmental standards and optimize the performance of diesel-based equipment. Such technological advancements fuel higher usage of diesel exhaust fluid while generally making diesel engine operations more environmentally friendly and sustainable, indicating rising adoption of diesel exhaust fluid among diesel users spurred by technological innovations in SCR systems.

Diesel Exhaust Fluid Market Restraints:

-

The expense associated with installing and maintaining SCR systems and diesel exhaust fluid can deter some operators, limiting market growth.

Installation and maintenance expenses for SCR systems and diesel exhaust fluid are likely to be very costly and may remain a significant deterrent for operators, hindering the growth prospects for the diesel exhaust fluid market. The SCR systems, which are deemed essential for optimal applications of diesel exhaust fluid, involve high initial costs for installation and integration with diesel engines. Moreover, maintenance costs and the necessity of repeated replenishment of diesel exhaust fluid increase the burdens of the total cost. Once again, this is particularly true in industries that are subject to operating budgets highly restricted or regulated. These include transportation and construction. This discourages some operators from adopting diesel exhaust fluid technology, especially in areas with less severe emissions restrictions or in smaller operators who may find the additional costs problematic. In this regard, the financial considerations against SCR systems and the use of diesel exhaust fluid deter the wider market penetration required for further growth in the diesel exhaust fluid sector.

Diesel Exhaust Fluid Market Opportunities:

-

The rise of renewable diesel fuels presents an opportunity to integrate diesel exhaust fluid more effectively, potentially expanding market reach.

The advent of renewable diesel fuels provides the opportunity to more readily integrate diesel exhaust fluid into a more vast market. Renewable diesel products are a cleaner alternative to traditional diesel and are produced from bio-based feedstocks, meaning their carbon emissions are lower than their traditional counterparts. Therefore, environmental objectives promoted by diesel exhaust fluid perfectly form part of this trend. A rise in renewable diesel development creates a complementary relationship with diesel exhaust fluid and enhances the overall rationale behind the strategy of improving emissions reduction. For example, adding diesel exhaust fluid to heavy-duty vehicles and equipment that use renewable diesel would further reduce NOx levels, combining the advantages of good air quality with the additional benefit of regulatory compliance. In this manner, the promotion of the use of diesel exhaust fluid with renewable fuels expands the market for application, opening new niches and markets that deploy both technologies side by side. Consequently, the rise in the consumption of renewable diesel thus presents an emerging market opportunity for the integration of diesel exhaust fluid across sectors and contributes to broader objectives of environmental and sustainability goals.

Diesel Exhaust Fluid Market Challenges:

-

Supply chain disruptions and variability in diesel exhaust fluid production can impact availability and pricing, posing challenges for consistent market supply.

Supply chain disruptions and variability in diesel exhaust fluid production create trouble in consistent supply chain availability in the market. Fluctuations in availability and transportation delays of raw materials also influence inconsistent production and can lead to shortages of diesel exhaust fluid by affecting those industries that depend on it for their business to comply with the need of emission regulations. For example, disruption in the supply chain of urea that is used in the production of diesel exhaust fluid can be a critical production bottleneck that pushes the cost in the hands of the end-users. This instability leads to then-probabilistic diesel exhaust fluid shortages as well as the resultant price rises which have come to discourage the operators from maintaining adequate levels of diesel exhaust fluid or even investing in SCR technology. This unpredictability can thus go against the market stability and growth of diesel exhaust fluid in some respects, ultimately affecting businesses' ability to maintain good control over their operational costs as well as adhere to the proper emission standards in place.

Diesel Exhaust Fluid Market Segmentation Analysis:

By Component, SCR Catalysts Lead Diesel Exhaust Fluid Market by Component in 2024

In 2024, the SCR Catalysts segment dominated the Diesel Exhaust Fluid market accounting for a market share of about 40%. SCR Catalysts are crucial components of Selective Catalytic Reduction systems, without them, the effective reduction of nitrogen oxide (NOx) emission from diesel engines would not be possible. A higher market share reveals more significance in the emissions process, as SCR systems rely on catalysts of this type to convert harmful NOx into harmless nitrogen and water. For example, the wide acceptance of SCR technology in heavy-duty trucks and industrial machinery indicates dependence on high-performance SCR Catalysts because those are mostly applied for strictly stringent emission regulations. It underlines the integral nature of SCR Catalysts to improve the efficiency of the diesel exhaust fluid system and enables diesel-powered applications to meet respective regulations.

By Vehicle Type, Heavy Commercial Vehicles Dominate Diesel Exhaust Fluid Usage in 2024

In 2024, the Heavy Commercial Vehicles (HCVs) segment dominated and accounted for approximately 50% of the market share in the diesel exhaust fluid market. HCVs, which include trucks and buses, are a major diesel exhaust fluid consumer because of the higher emissions from their diesel engines and the strict emission standards to which they are subjected. These are vehicles that, based on the level of their technology, are supposed to be equipped with the most advanced Selective Catalytic Reduction systems that are capable of even higher levels of nitrogen oxide reduction, mainly dependent on diesel exhaust fluid. The more stringent the emission standards increase, the higher the usage of diesel exhaust fluid in, for example, logistics and transportation companies that increasingly rely on HCVs. The HCV segment's dominance depicts its critical role in the diesel exhaust fluid market and impacts the overall demand for diesel exhaust fluid solutions in the transportation sector.

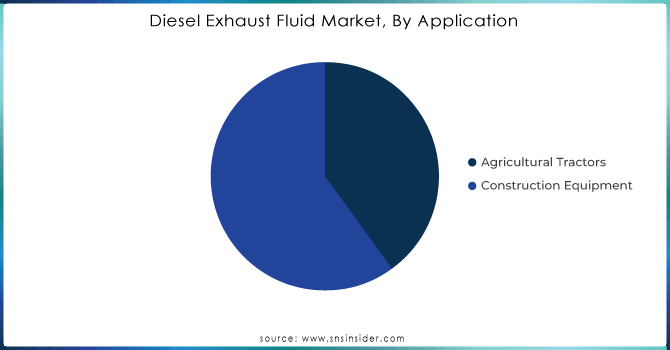

By Application, Construction Equipment Drives Diesel Exhaust Fluid Demand in 2024

In 2024, the Construction Equipment segment dominated the Diesel Exhaust Fluid market, with an estimated market share of approximately 60%. Construction equipment, such as excavators, bulldozers, and loaders, often operates under demanding conditions and is subject to stringent emission regulations. These machines typically use diesel exhaust fluid in their Selective Catalytic Reduction (SCR) systems to manage NOx emissions effectively. For example, large-scale construction projects and infrastructure developments require heavy machinery that adheres to environmental standards, driving higher diesel exhaust fluid consumption in this sector. The dominance of the Construction Equipment segment reflects the critical role of diesel exhaust fluid in meeting regulatory requirements and maintaining the performance of diesel-powered construction machinery.

Get Customized Report as per Your Business Requirement - Request For Customized Report

By Supply Mode, Bulk Supply Segment Leads Diesel Exhaust Fluid Market in 2024

In 2024, the bulk market segment dominated the Diesel Exhaust Fluid market with a market share of around 55%. Bulk diesel exhaust fluid is in great demand among large users such as fleets, construction companies, and agricultural operations primarily because of its cost-effectiveness and convenience. For instance, large logistics companies and construction firms generally consume large amounts of diesel exhaust fluid for heavy-duty vehicles and machinery. Hence, bulk supply is more efficient than cans and bottles which, in return, is a cost-efficient practice for large consumers of large volumes that also saves handling costs and simplifies refueling processes for them.

By Distribution Channel, OEM Segment Commands Diesel Exhaust Fluid Market Revenue in 2024

The OEM segment dominated the Diesel Exhaust Fluid market accounting for a revenue share of at least 65%. OEMs refer to automobile and equipment makers who promote the application mainly through their new diesel engines, wherein they build systems that utilize diesel exhaust fluid. For instance, large truck manufacturers and construction equipment manufacturers install diesel exhaust fluid in their standard components in their SCR systems to ensure the attainment of regulatory emission standards. Therefore, the infusion will entail that the customers receive it through new equipment sales to further increase market penetration. The OEM segment is perceived as a dominant one, meaning that conformity with emission standards at the outset largely accounts for the OEM share of the diesel exhaust fluid market.

Diesel Exhaust Fluid Market Regional Analysis

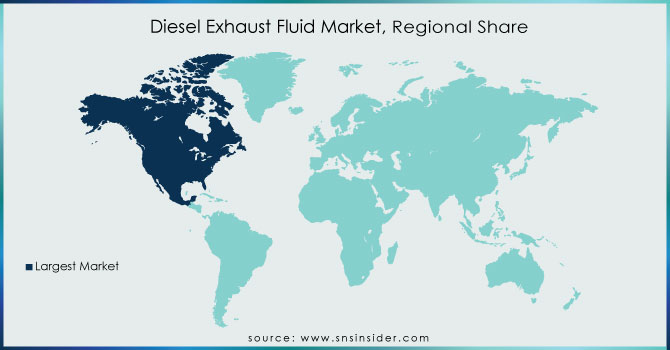

North America Dominates Diesel Exhaust Fluid Market in 2024

North America is the leading region in the Diesel Exhaust Fluid Market, holding an estimated 42% market share in 2024. This dominance is driven by stringent emission regulations, high adoption of heavy-duty diesel vehicles, and widespread implementation of Selective Catalytic Reduction (SCR) systems. Strong government enforcement of EPA standards compels logistics, transportation, and construction companies to use DEF consistently. Additionally, well-established bulk supply networks and refueling infrastructure ensure easy access, reinforcing the region’s market leadership.

-

United States Leads North America’s Diesel Exhaust Fluid Market

The United States dominates the regional market due to its vast fleet of heavy-duty trucks, buses, and industrial machinery subject to strict emission regulations. Large-scale adoption of SCR technology, government incentives for cleaner diesel solutions, and a developed infrastructure for bulk DEF distribution boost market growth. High demand from logistics, construction, and transportation sectors ensures continuous DEF usage, making the U.S. the focal point for North America’s diesel exhaust fluid consumption.

Asia Pacific is the Fastest-Growing Region in Diesel Exhaust Fluid Market in 2024

Asia Pacific is the fastest-growing region in the Diesel Exhaust Fluid Market, with an estimated CAGR of 10.5%. Rapid industrialization, expanding construction and logistics sectors, and growing heavy-duty diesel vehicle adoption drive increased DEF demand. Government emission standards and incentives for cleaner diesel technologies further accelerate the market.

-

China Leads Diesel Exhaust Fluid Market Growth in Asia Pacific

China dominates the Asia Pacific market due to rapid industrial and infrastructure development, increasing numbers of commercial diesel vehicles, and strict NOx emission regulations. Extensive adoption of SCR systems in logistics, long-haul transportation, and construction equipment contributes to high DEF consumption. Government policies promoting environmental compliance and technological upgrades in diesel engines strengthen the market. China’s large-scale industrial base, combined with growing infrastructure projects and commercial fleets, positions it as the largest and fastest-growing contributor to the region’s diesel exhaust fluid market.

Europe Diesel Exhaust Fluid Market Insights in 2024

Europe holds a significant share of the Diesel Exhaust Fluid Market, driven by strict EU emission regulations and widespread SCR implementation. Driving Factor: Enforcement of Euro VI emission norms compels diesel operators to use DEF.

-

Germany Dominates Europe’s Diesel Exhaust Fluid Market

Germany leads the European market because of its advanced logistics, transportation, and industrial machinery sectors, all operating under stringent Euro VI standards. DEF integration in SCR systems is mandatory for compliance, creating a high market demand. Extensive DEF distribution networks, along with large commercial and construction vehicle fleets, reinforce Germany’s dominant position, ensuring it remains Europe’s top diesel exhaust fluid market contributor.

Middle East & Africa and Latin America Diesel Exhaust Fluid Market Insights

In 2024, the Diesel Exhaust Fluid Market in the Middle East, Africa, and Latin America is emerging steadily. In Latin America, Brazil leads due to growing heavy-duty vehicle fleets and tightening emission standards in urban areas. In the Middle East, particularly Gulf countries, modernization of commercial fleets and industrial emission regulations are driving DEF adoption. Though smaller than other regions, expanding infrastructure, government incentives, and increasing awareness about emissions control are supporting market growth in these regions.

Competitive Landscape of the Diesel Exhaust Fluid Market:

AdBlue

AdBlue is a globally recognized leader in diesel exhaust fluid (DEF), specializing in high-quality urea-based solutions for heavy-duty vehicles and industrial machinery. With decades of experience, the company develops, manufactures, and supplies DEF that meets stringent emission standards, ensuring optimal performance of Selective Catalytic Reduction (SCR) systems. AdBlue’s direct partnerships with OEMs and distributors allow efficient distribution to fleets, construction equipment, and transportation sectors worldwide. Its role in the DEF market is crucial, as it enables diesel engines to comply with environmental regulations while maintaining engine efficiency and reducing nitrogen oxide emissions.

-

In 2024, AdBlue launched a premium DEF line with enhanced purity and extended storage stability, catering to high-demand commercial and industrial applications.

Blue Sky Diesel Exhaust Fluid

Blue Sky Diesel Exhaust Fluid is a U.S.-based provider of premium DEF solutions, serving heavy-duty trucks, buses, and construction machinery. The company focuses on producing high-quality, environmentally compliant diesel exhaust fluids that optimize SCR system performance. Blue Sky operates through a wide distribution network, ensuring reliable supply to fleet operators and OEM partners. Its role in the DEF market is vital, as it supports emission reduction initiatives and helps transportation and industrial sectors meet regulatory requirements efficiently.

-

In 2024, Blue Sky introduced bulk DEF delivery services for large fleets, improving cost efficiency and operational convenience.

CF Industries Holdings, Inc.

CF Industries Holdings, Inc. is a global manufacturer of nitrogen-based products, including diesel exhaust fluid (DEF), serving agricultural, transportation, and industrial sectors. The company’s DEF products are engineered to meet international emission standards, enhancing SCR system efficiency in heavy-duty engines. With extensive production facilities and distribution networks, CF Industries ensures consistent supply for large-scale industrial and fleet applications. Its role in the DEF market is central, as it provides both standard and premium DEF solutions to maintain engine performance and regulatory compliance.

-

In 2024, CF Industries expanded its DEF production capacity, targeting rising demand from logistics, agriculture, and construction industries.

Cummins Filtration

Cummins Filtration, a subsidiary of Cummins Inc., specializes in diesel exhaust fluid (DEF) solutions under its Fleetguard brand. The company produces high-quality DEF that supports SCR systems in trucks, buses, and off-road equipment, ensuring compliance with NOx emission regulations. Cummins Filtration leverages its global presence, OEM partnerships, and technical expertise to provide reliable and performance-optimized DEF for industrial, transportation, and commercial applications. Its role in the DEF market is significant, as it helps customers maintain engine efficiency while adhering to environmental standards.

-

In 2024, Cummins Filtration launched advanced Fleetguard DFS DEF products with improved purity and optimized NOx reduction for heavy-duty engines.

Diesel Exhaust Fluid Market Key Players:

-

AdBlue

-

Blue Sky Diesel Exhaust Fluid

-

CF Industries Holdings, Inc.

-

Cummins Filtration

-

Diesel Exhaust Fluid (DEF)

-

Dyno Nobel

-

KOST USA, Inc.

-

Old World Industries, LLC

-

STOCKMEIER Group

-

The Potash Corporation of Saskatchewan

-

Yara International ASA

-

BASF SE

-

Chevron

-

ENI S.p.A.

-

Fluid Energy Group Ltd.

-

Groupe Renault

-

GS Caltex

-

JX Nippon Oil & Energy

-

LyondellBasell Industries

-

TotalEnergies

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | US$ 39.96 Billion |

| Market Size by 2032 | US$ 74.0 Billion |

| CAGR | CAGR of 8.0% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (SCR Catalysts, DEF Tanks, DEF Injectors, DEF Supply Modules, DEF Sensors, NOx Sensors) •By Vehicle Type (Passenger Cars, LCVs, HCVs) •By Application (Agricultural Tractors, Construction Equipment) •By Supply Mode (Cans & Bottles, IBCs, Bulk, Pumps) •By Distribution Channel (OEM, Aftermarket) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Old World Industries, LLC, Yara International ASA, Blue Sky Diesel Exhaust Fluid, Cummins Filtration, KOST USA, Inc., STOCKMEIER Group, The Potash Corporation of Saskatchewan, CF Industries Holdings, Inc., Dyno Nobel and other key players |

Frequently Asked Questions

The Diesel Exhaust Fluid Market Size was valued at USD 39.96 billion in 2024, and is expected to reach USD 74.0 Billion by 2032

Supply chain disruptions and variability in diesel exhaust fluid production can impact availability and pricing, posing challenges for consistent market supply

The Diesel Exhaust Fluid Market is expected to grow at a CAGR of 6.5%.

Manufacturers, Consultant, aftermarket players, association, Research institute, private and universities libraries, suppliers and distributors of the product.

Key stakeholders considered in the study:

Raw material vendors

distributors/traders/wholesalers/suppliers

regulatory authorities, including government agencies and ngo

commercial research & development (r&d) institutions

importers and exporters

government organizations, research organizations, and consulting firms

trade/industrial associations

end-use industries are the stake holder of this report

Get in Touch