Nickel Mining Market Report Scope & Overview:

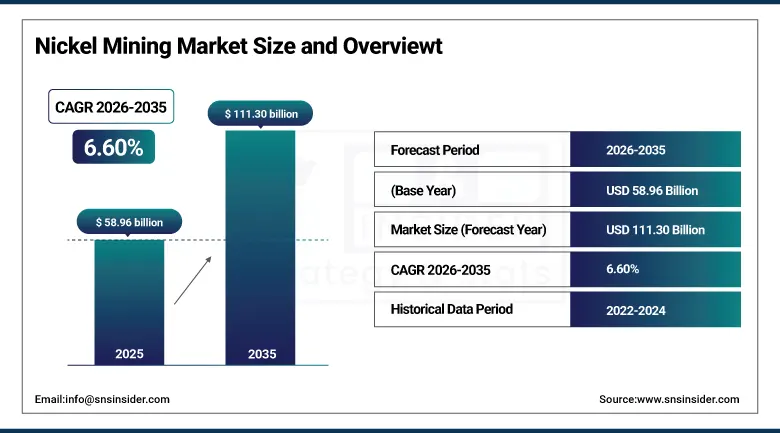

The Nickel Mining Market was valued at USD 58.96 Billion in 2025 and is expected to reach USD 111.30 Billion by 2035, growing at a CAGR of 6.60% from 2026–2035.

The global nickel mining market is growing at an exceptional pace driven by its critical roles across two simultaneously expanding demand categories. Nickel is the world's most important corrosion-resistant alloying metal for stainless steel whose production consumes over two-thirds of global nickel output. Simultaneously, nickel's electrochemical properties make it an irreplaceable cathode material in lithium-nickel-manganese-cobalt oxide and lithium-nickel-cobalt-aluminium oxide battery chemistries whose energy density and cycle life advantages sustain their specification in premium EV applications.

In June 2023, Glencore, Stellantis, and Volkswagen's battery unit PowerCo reached an agreement to back a USD 1.00 billion deal through the special purpose acquisition company ACG Acquisition Company to acquire two nickel mines in Brazil. The investment reflects the commercial urgency of securing battery-grade nickel supply as EV manufacturers recognise that sulphide ore nickel access represents a strategic raw material constraint whose resolution requires upstream mining investment rather than passive spot market procurement.

Key Market Size and Forecast

-

Market Size in 2026E: USD 62.85 Billion

-

Market Size by 2035: USD 111.30 Billion

-

CAGR: 6.60% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information on Nickel Mining Market - Request Free Sample Report

Key Market Trends

-

EV battery nickel demand is creating above-average above-market growth for high-purity Class I nickel whose sulphide ore source and hydrometallurgical refining create battery-grade specifications that laterite/NPI alternatives cannot achieve.

-

Indonesia's nickel pig iron industry expansion is increasing global nickel production volume at lower cost, creating competitive pressure on Class I nickel pricing while serving the stainless-steel market's commodity grade demand.

-

High-pressure acid leach technology development for laterite ore processing is creating new battery-grade nickel supply pathways from laterite deposits that previously could only produce lower-purity Class II nickel for the stainless-steel market.

-

Nickel supply chain geopolitical concerns are motivating EV manufacturers and battery producers to secure long-term supply agreements with Indonesian, Canadian, and Australian miners whose supply diversity reduces dependence on any single producing country.

-

Recycling of nickel from spent EV batteries is creating a secondary nickel recovery industry whose commercial scale will compound with the growing EV fleet's end-of-life battery volume over the forecast period.

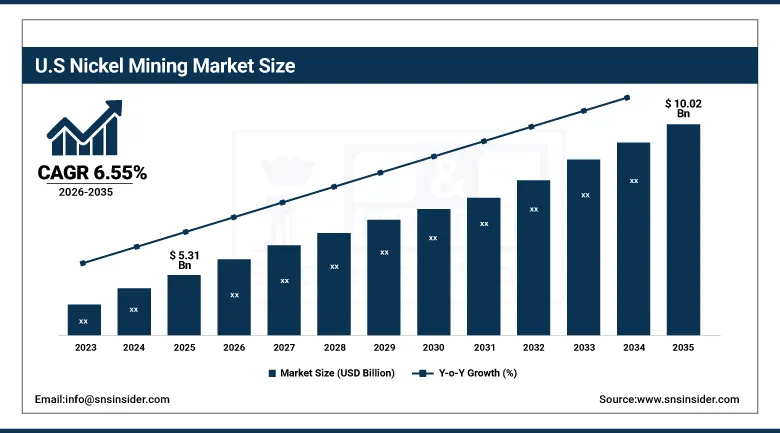

U.S. Nickel Mining Market Outlook

The U.S. Nickel Mining Market, including domestic consumption, was valued at approximately USD 5.31 Billion in 2025 and is expected to reach approximately USD 10.02 Billion by 2035, growing at a CAGR of approximately 6.55%.

The U.S. has minimal domestic nickel mining but is a significant nickel consuming market through stainless steel production, superalloy manufacturing for aerospace and defence, and the rapidly growing EV battery sector. Talon Metals' Tamarack Nickel Project in Minnesota and Lundin Mining's operations represent the most significant potential U.S. domestic nickel mine development whose regulatory approval and financing are progressing. The DOE's critical minerals programme and the IRA's domestic content requirements for EV battery minerals are creating commercial incentives for U.S. nickel supply development that did not previously exist at commercially compelling levels.

Talon Metals and Tesla signed a nickel supply agreement in 2023 for delivery of up to 75,000 metric tonnes of nickel from Talon's Minnesota Tamarack project, representing one of the largest domestic U.S. nickel supply commitments ever made. The agreement reflects Tesla's strategic procurement approach of securing multiple domestic and international nickel supply relationships to ensure the battery-grade nickel access required for its expanding North American vehicle manufacturing programme.

Nickel Mining Market Segment Analysis

-

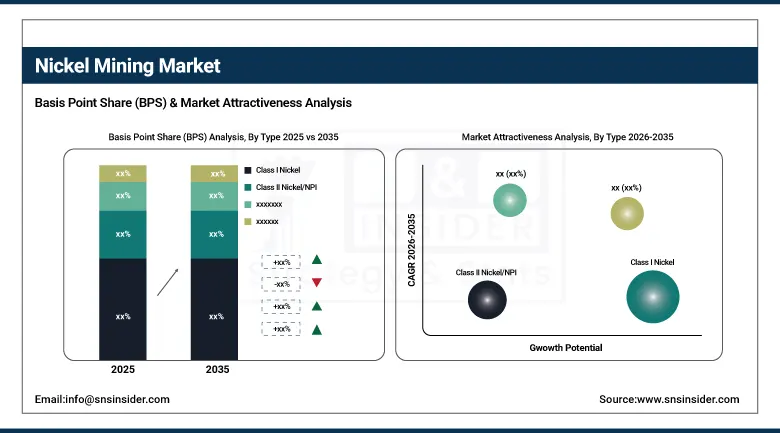

By Type, the Class I Nickel segment dominated the Nickel Mining Market with approximately 60% share in 2025, while the Class II Nickel/NPI segment is growing rapidly.

-

By Mining Method, the Open-Pit/Surface Mining segment dominated the Nickel Mining Market with approximately 65% share in 2025, , while the Underground Mining segment is the fastest growing.

-

By Application, the Stainless-Steel segment dominated the Nickel Mining Market with approximately 68% share in 2025, while the EV Batteries segment is the fastest growing with a CAGR of approximately 15.8%.

-

By End User, the Steel & Alloy Industry segment dominated the Nickel Mining Market with approximately 55% share in 2025, while the Battery Manufacturers segment is the fastest growing.

By Type, Class I dominates, Class II grows rapidly

Class I nickel retained the dominant type position with approximately 60% of the nickel mining market in 2025. Its commercial primacy reflects the broad application compatibility of high-purity refined nickel across electroplating, specialty alloy, battery cathode material, and chemical applications that Class II nickel's lower purity cannot serve. The global electroplating industry's requirement for electrolytic nickel at 99.9% purity, the superalloy industry's nickel specification for aerospace turbine components, and the battery cathode material sector's requirement for battery-grade nickel sulphate whose production requires Class I nickel feedstock collectively sustain Class I's premium commercial position.

Class II nickel and nickel pig iron are growing rapidly because Indonesia's extraordinary expansion of NPI production capacity has created the world's most commercially competitive nickel supply for the stainless-steel market whose commodity grade requirements NPI satisfies at prices substantially below Class I alternatives. Each new NPI smelter commissioned in Indonesia creates commodity-grade nickel supply that captures stainless steel market share from conventional nickel producers, driving the commercial displacement of higher-cost Class I producers from commodity applications while Class I concentrates in premium battery and specialty markets.

By Application, stainless steel dominates, EV batteries grow fastest

Stainless steel retained the dominant application position with approximately 68% of the nickel mining market in 2025. This dominance reflects the extraordinary commercial scale of the global stainless-steel industry whose annual production exceeds 50 million tonnes, each tonne of austenitic grade stainless containing approximately 8-12% nickel whose stoichiometric requirement creates non-discretionary nickel procurement. The Nickel Institute's documentation that over two-thirds of global nickel consumption occurs in stainless steel production demonstrates the commercial dependency whose scale sustains nickel mining investment independent of any single new application's emergence. Infrastructure construction, consumer goods, food processing equipment, and medical devices' universal stainless-steel specification creates procurement whose volume sustains consistent market demand.

EV batteries are the fastest-growing application at approximately 15.8% CAGR because NMC 811 and NCA battery chemistries' adoption in premium electric vehicles creates per-vehicle nickel consumption of approximately 30-40 kg in a large battery pack, creating nickel demand that scales proportionally with EV production volume. IEA projections of 41% increase in global electric car sales and the progressive EV mandates across Europe, China, and the U.S. collectively create a commercially certain demand growth trajectory whose magnitude will progressively elevate battery applications from 7-10% of current nickel demand toward a structurally significant share by 2035.

By Mining Method, open-pit dominates, underground grows fastest

Open-pit and surface mining retained the dominant mining method position with approximately 65% of the nickel mining market in 2025. Laterite nickel deposits in Indonesia, the Philippines, New Caledonia, and Brazil are amenable to surface mining whose lower capital intensity and higher daily production throughput create the most commercially competitive nickel extraction economics for commodity-grade production. Indonesia's red laterite deposits, processed through rotary kiln electric furnace technology to produce nickel pig iron, represent the most commercially significant surface mining programme in the global nickel market whose cost leadership has defined nickel pricing since 2015.

Underground mining is the fastest-growing method because the high-grade sulphide ore deposits that produce battery-grade nickel are predominantly located in geological environments that require underground access. Canadian deposits at Sudbury and Thompson, Australian deposits in the Kambalda region, and Russian deposits in Norilsk all require underground extraction whose higher operating cost is justified by the premium pricing that battery-grade Class I nickel commands over commodity-grade NPI. Each new sulphide ore underground mine development adds battery-grade nickel supply capacity whose commercial value is above-market relative to laterite alternatives.

By End User, steel industry dominates, battery manufacturers grow fastest

The steel and alloy industry retained the dominant end user position with approximately 55% of the nickel mining market in 2025. Stainless steel producers globally, anchored by Chinese stainless-steel producers whose combined output exceeds 60% of global stainless production, create the most commercially concentrated nickel demand base. Each major stainless steel plant's annual nickel procurement typically ranges from 50,000 to 200,000 tonnes depending on capacity and product mix, creating institutional-scale supply relationships whose commercial value sustains dedicated nickel mining project economics. The steel industry's continuous production process creates non-seasonal, consistent procurement whose reliability is commercially preferred by nickel mining operators.

Battery manufacturers are the fastest-growing end user at approximately 18.2% CAGR because the global EV battery supply chain's expansion is creating procurement growth whose percentage rate of increase substantially exceeds any other nickel end use category. CATL, LG Energy Solution, Panasonic, and Samsung SDI are each expanding nickel cathode material procurement proportionally with their battery cell manufacturing capacity additions. Each gigawatt-hour of new battery cell manufacturing capacity commissioned creates approximately 500-1,000 tonnes of annual nickel cathode material procurement, creating demand that compounds with the extraordinary pace of global battery manufacturing investment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

62.5% |

|

Europe |

Russia |

44.8% |

|

Asia Pacific |

Indonesia |

48.6% |

|

Middle East & Africa |

South Africa |

44.2% |

|

Latin America |

Brazil |

52.4% |

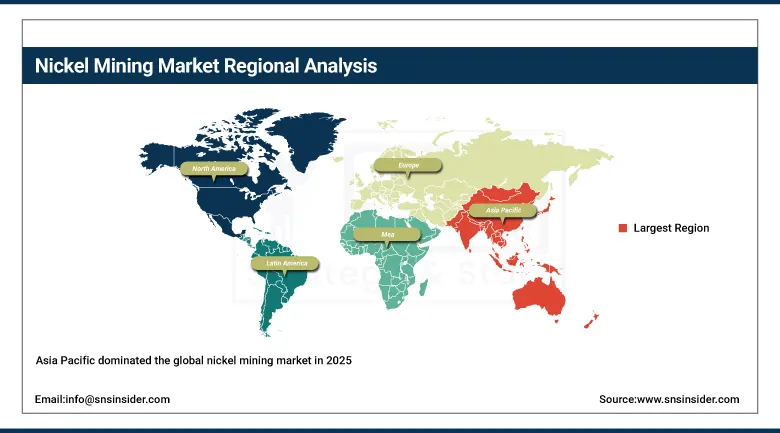

Asia Pacific Nickel Mining Market Insights

Asia Pacific dominated the global nickel mining market in 2025 as the world's largest nickel producing and consuming region. Indonesia accounts for approximately 48.6% of Asia Pacific revenues as the world's largest nickel producer whose NPI industry has transformed global nickel supply since 2015. The Philippines, New Caledonia, and Australia represent significant secondary Asia Pacific producing markets. China's stainless-steel industry creates the largest single national nickel demand concentration globally whose import procurement from Indonesian NPI producers sustains the Asia Pacific market's dual production and consumption dominance.

India and South Korea are commercially significant secondary markets whose stainless steel and EV battery production are creating growing nickel consumption demand. South Korea's POSCO and LG Energy Solution’s combined nickel procurement for stainless steel and EV battery applications represent the region's most commercially sophisticated dual-end-use nickel customer relationships.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Nickel Mining Market Insights

North America is the fastest-growing regional nickel mining market driven by EV battery supply chain investment, IRA domestic content requirements, and the strategic importance of securing critical mineral supply from allied trading partners. Canada accounts for the majority of North American production through Vale's Sudbury operations, Norilsk Nickel's Canadian assets, and the development pipeline of new sulphide ore projects. The U.S. accounts for approximately 62.5% of North American revenues through its dominant nickel consumption from stainless steel, superalloy, and growing battery manufacturing sectors.

Canada's nickel mining infrastructure, anchored by the historic Sudbury basin's sulphide deposits, provides the most commercially significant Class I nickel supply in the Americas. Talon Metals's Tamarack Minnesota project and First Quantum Minerals' U.S. exploration programmes reflect the growing commercial interest in developing domestic American sulphide nickel mining to serve the rapidly growing domestic EV battery manufacturing supply chain.

Europe Nickel Mining Market Insights

Europe is a significant nickel market where Russia accounts for approximately 44.8% of European production through Norilsk Nickel's extraordinary sulphide ore operations whose Class I nickel output served European stainless steel and battery markets before 2022 geopolitical disruption. Geopolitical risk has accelerated European procurement diversification toward Canadian, Australian, and Indonesian alternatives, creating commercial opportunity for non-Russian nickel producers to capture European market share. Finland's Terrafame and the UK's Pensana represent European nickel processing investment responding to this supply chain realignment.

Germany and France are the largest European nickel consuming markets through their stainless-steel manufacturing, automotive industry's battery material procurement, and aerospace superalloy production. The EU's Critical Raw Materials Act’s nickel designation creates regulatory motivation for European supply chain diversification and domestic processing investment that sustained procurement realignment from Russian sources.

MEA & Latin America Nickel Mining Market Insights

South Africa leads MEA nickel revenues at approximately 44.2% through its laterite nickel deposits and the established mining infrastructure whose platinum group metal operations generate nickel as a co-product whose commercial value sustains mining economics. Brazil leads Latin American revenues at approximately 52.4% through Vale's Onca Puma and Voisey's Bay operations and the Glencore-Stellantis-PowerCo acquisition target mines. Brazil's sulphide and laterite nickel resources create supply potential for both stainless steel commodity grade and battery-grade Class I nickel.

Zimbabwe and the Democratic Republic of Congo represent significant emerging MEA nickel producing markets whose geological prospectivity for sulphide nickel deposits is attracting exploration investment from battery supply chain-focused mining companies seeking non-Russian Class I nickel sources.

Market Dynamics

Growth Drivers: EV battery demand creating above-average nickel procurement and stainless-steel infrastructure demand sustaining base

EV battery demand is the nickel mining market's most commercially transformative growth driver. The progressive adoption of NMC 811 chemistry for its superior energy density creates per-cell nickel requirements whose aggregate compound with global EV production volume growth. IEA forecasts of EV market penetration reaching 30-40% of new vehicle sales by 2030 create a commercially certain demand trajectory whose magnitude will double or triple current battery sector nickel consumption by the end of the forecast period. Each major automotive OEM's EV commitment creates proportional battery-grade nickel supply chain investment.

Global infrastructure investment sustaining stainless steel demand creates the foundational commercial base that sustains nickel mining investment through EV demand cycle development. Construction, food processing equipment, medical devices, and consumer goods' stainless-steel specification creates non-discretionary procurement whose consistency across economic cycles provides commercial stability for nickel mining operators whose capital investment requires multi-decade return horizons that commodity demand variability can undermine without the stainless-steel base load's commercial anchor.

Restraints: Nickel price volatility from Indonesian NPI supply surplus and ESG compliance cost in tropical mining environments

Indonesian NPI production's extraordinary cost competitiveness has created structural price pressure on the global nickel market that limits revenue growth relative to production volume growth. The LME nickel price decline from above USD 30,000 per tonne in 2022 to below USD 15,000 in 2024 reflects the commercial impact of Indonesian supply expansion whose volume growth exceeded demand growth expectations. This price environment compresses mining margins for higher-cost sulphide producers whose Class I nickel premium over NPI pricing remains insufficient to compensate fully for their above-average production costs.

ESG compliance cost is increasingly significant for tropical laterite mining operations in Indonesia, the Philippines, and New Caledonia where large-scale surface mining creates deforestation, soil erosion, and watershed contamination whose remediation requirements are creating increasing regulatory and reputational compliance investment. European and North American EV manufacturers whose supply chain due diligence requirements are progressively extending to nickel mining operations are creating ESG performance expectations that Indonesian producers must meet to maintain market access.

Opportunities: Battery-grade Class I nickel supply development and nickel recycling circular economy

Battery-grade Class I nickel supply development represents the most commercially premium growth opportunity for nickel mining companies whose sulphide ore assets create the production capability that laterite ore alternatives cannot match without HPAL technology investment. Each new sulphide ore mine or HPAL laterite project that achieves battery-grade nickel production creates a supply relationship with EV battery manufacturers whose long-term offtake agreements provide revenue certainty that sustains project financing. Talon Metals' Tesla supply agreement and Glencore's battery material partnerships demonstrate the commercial model.

Nickel recycling from spent EV batteries represents a structurally growing commercial opportunity whose scale will compound with the accumulating EV fleet's end-of-life battery volume through the 2030s and 2040s. Battery recyclers including Li-Cycle, Redwood Materials, and BASF's battery recycling programme are developing hydrometallurgical recovery processes whose nickel recovery efficiency creates commercial-grade battery material from spent cells, progressively creating a secondary nickel supply whose volume reduces primary mining demand per unit of battery production.

Recent Developments:

-

2023: Glencore, Stellantis, and Volkswagen's battery unit PowerCo reached a USD 1.00 billion agreement in June 2023 through ACG Acquisition Company to acquire two nickel mines in Brazil, securing battery-grade sulphide nickel supply for European EV battery manufacturing programmes.

-

2023: Talon Metals and Tesla signed a nickel supply agreement in 2023 for up to 75,000 metric tonnes of nickel concentrate from Talon's Minnesota Tamarack project, representing one of the largest domestic U.S. nickel supply commitments to an EV manufacturer and reflecting the IRA's domestic content incentive impact on battery mineral supply chain investment.

-

2024: Vale completed the separation of its base metals business into a standalone entity Vale Base Metals in 2024, attracting investment from Saudi Arabian mining company Ma'aden and creating a commercially focused nickel and copper mining company whose independent capital structure enables faster investment decision-making for critical mineral supply development.

Key Market Players

-

Norilsk Nickel (Nornickel)

-

Vale S.A.

-

BHP Billiton

-

Glencore plc

-

Jinchuan Group

-

Sherritt International

-

Sumitomo Metal Mining

-

First Quantum Minerals

-

South32

-

Anglo American

-

Wyloo Metals

-

Talon Metals

-

IGO Limited

-

Eramet Group

-

Horizonte Minerals

-

Lundin Mining

-

Panoramic Resources

-

PT Aneka Tambang (Antam)

-

DMCI Mining

-

Nickel Asia Corporation

Nickel Mining Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 58.96 Billion |

| Market Size by 2035 | USD 111.30 Billion |

| CAGR | CAGR of 6.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Class I Nickel, Class II Nickel/NPI) • by Mining Method (Open-Pit/Surface Mining, Underground Mining) • by Application (Stainless Steel, EV Batteries, Electroplating, Superalloys, Others) • by End User (Steel & Alloy Industry, Battery Manufacturers, Chemical Industry, Aerospace & Defence, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Norilsk Nickel (Nornickel), Vale S.A., BHP Billiton, Glencore plc, Jinchuan Group, Sherritt International, Sumitomo Metal Mining, First Quantum Minerals, South32, Anglo American, Wyloo Metals, Talon Metals, IGO Limited, Eramet Group, Horizonte Minerals, Lundin Mining, Panoramic Resources, PT Aneka Tambang (Antam), DMCI Mining, Nickel Asia Corporation |

Frequently Asked Questions

The Nickel Mining Market is expected to grow at a CAGR of 6.60% from 2026 to 2035.

The Nickel Mining Market was valued at USD 58.96 Billion in 2025.

Rising EV battery demand creating above-average nickel procurement growth as NMC and NCA battery chemistry adoption scales with global electric vehicle production, and stainless steel infrastructure demand sustaining the commercial base whose consistency underpins long-duration nickel mining capital investment.

Stainless Steel dominated the Nickel Mining Market with approximately 68% share in 2025, while EV Batteries is the fastest growing with a CAGR of approximately 15.8%.

Asia Pacific dominated the Nickel Mining Market in 2025 as the world's largest producing and consuming region, with Indonesia accounting for approximately 48.6% of Asia Pacific revenues as the world's largest nickel producer.

Get in Touch