E-commerce of Agricultural Products Market Report Scope & Overview:

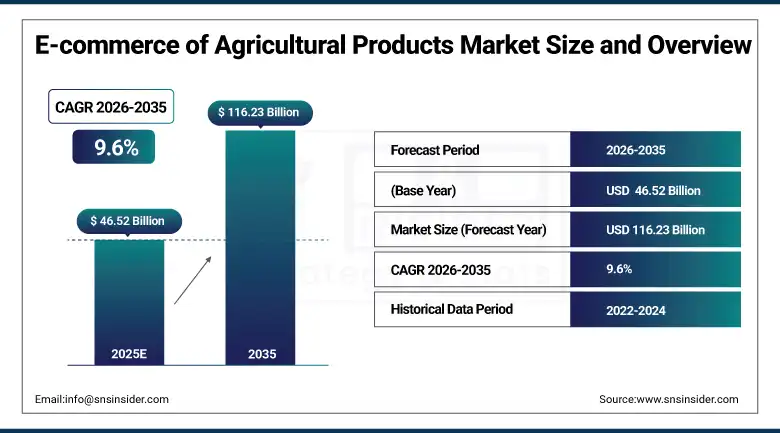

The E-commerce of Agricultural Products Market was valued at USD 46.52 billion in 2025 and is expected to reach USD 116.23 billion by 2035, growing at a CAGR 9.6% of from 2026-2035.

The E-commerce of Agricultural Products Market encompasses digital platforms facilitating the online purchase and sale of farm goods, inputs, and associated services. Several factors are fueling its expansion. Farmers are increasingly using smartphones and gaining internet access. Simultaneously, there's a growing appetite for fresh, traceable agricultural products. Digital payment systems are also improving, and supply chains need to be more efficient. The market is benefiting from technology integration, smoother logistics, and a shift toward direct transactions between farmers and consumers, as well as between businesses.

Around 41.5% of farmers and 56.2% of businesses adopted e-commerce platforms, driving digital agricultural transactions and supply chain efficiency.

E-commerce of Agricultural Products Market Size and Forecast:

-

Market Size in 2025: USD 46.52 Billion

-

Market Size by 2035: USD 116.23 Billion

-

CAGR: 9.6% of from 2026-2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information On E-commerce of Agricultural Products Market - Request Free Sample Report

Trends in the E-commerce of Agricultural Products Market

-

Digital Adoption Among Farmers – Increasing smartphone and internet use for procurement, sales, and market insights.

-

Direct-to-Consumer Models – Growth of farm-to-consumer platforms for fresh produce and perishable goods.

-

Integration of Technology – Use of digital payments, traceability, and supply chain management tools.

-

Marketplace-Based Platforms – Dominance of B2B and hybrid marketplace models connecting multiple stakeholders.

-

Value-Added Services – Expansion of financing, analytics, and logistics solutions to support farmers and retailers.

U.S. E-commerce of Agricultural Products Market Insights:

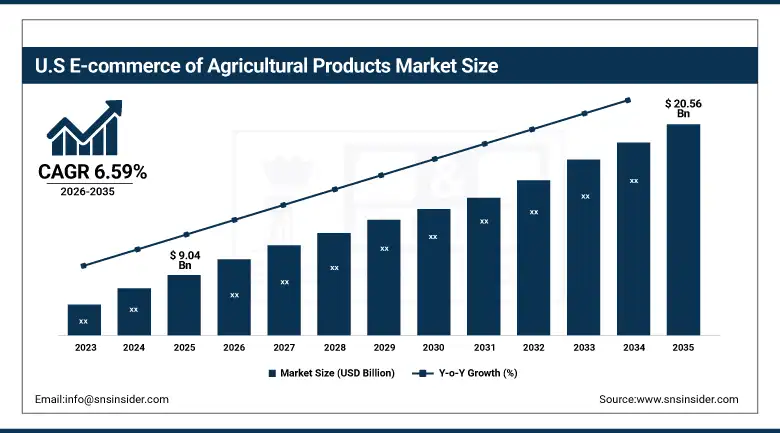

The U.S. E-commerce of Agricultural Products Market is projected to grow from USD 9.04 Billion in 2025 to USD 20.56 Billion by 2035, at a CAGR of 6.59%. Growth is driven by increasing digital adoption among farmers, rising demand for fresh produce, advanced agri-logistics, e-commerce platforms expansion, and integration of payment, traceability, and supply chain technologies.

E-commerce of Agricultural Products Market Growth Drivers:

-

Digital Connectivity and Smartphone Adoption

The increasing penetration of smartphone and internet among farmers and agri-businesses is primarily driving the demand for E-commerce of Agricultural Products Market. Farmers who used to do this same way were as low as 41.5%, and today over that percentage of farmers are currently finding inputs and selling produce from digital platforms as well as getting market information from them. The lightweight nature of mobile internet allows for real-time prices, online payments and very efficient supply chain management and greatly reduces the need for intermediaries. The digital movement creates more control for small and medium-scale farmers, along with increased transparency in transactions and accelerated adoption of B2B and B2C agri-e commerce solutions.

E-commerce of Agricultural Products Market Restraints:

-

Fragmented Agricultural Supply Chains

Challenges in E-commerce of Agricultural Products Market Segment Fragmented Agricultural Supply Chains Most smallholder farmers are unaffiliated with any organized distribution network and lack high-tech infrastructure, storage facilities, or reliable logistics. This can lead to an increase in operational complexity, longer lead times and higher costs, particularly for temperature-sensitive products. Roughly a third of wholesalers and distributors say they lack efficiency with digital product sourcing and transportation. This fragmentation in the supply chain constrains scalability for e-commerce platforms, impedes quality consistency, and creates bottlenecks in seamless integration across producers, platforms and end consumers.

E-commerce of Agricultural Products Market Opportunities:

-

Expansion of B2B and B2C Agricultural E-commerce Models

B2B direct-to-retailer platforms, as well as B2C farm-to-consumer platforms, are experiencing high growth, which is expected to expand the E-commerce of Agricultural Products Market opportunities. Such models allow farmers to sell produce directly to businesses and/or end consumers, and as a result, cut out middlemen and earn higher margins. They improve freshness, traceability, delivery, and shopping experience between producers and retailers, and consumer end users. These platforms encourage the use of e-commerce solutions, improve supply chain transparency, and help achieve overall operational efficiency in the agricultural sector by supporting digital marketplaces.

E-commerce of Agricultural Products Market Segment:

-

By Product Type: In 2025, Agricultural inputs dominated with 35% share; Fresh fruits & vegetables fastest growing segment during 2026-2035

-

By Platform Type: In 2025, B2B platforms dominated with 56% share; B2C platforms fastest growing segment during 2026-2035

-

By End User: In 2025, Farmers dominated with 42% share; Retailers fastest growing segment during 2026-2035

-

By Business Model: In 2025, Marketplace-based model dominated with 63% share; Hybrid model fastest growing segment during 2026-2035

E-commerce of Agricultural Products Market Segment Analysis:

By Platform Type: B2B Platforms Dominate as B2C Platforms Emerge as Fastest-Growing

Both farmers, distributors and retailers are involved in large-scale transactions, usually exchanging small order items with large amounts of goods, which drives B2B platforms like nuts and provides them with various functions such as supply chain efficiency, bulk order management and integration of a wide variety of pay channels into one single digital payment.

The largest growth segment is expected to be B2C platforms, due to farmers directly selling agricultural products to individual consumers, supported by mobile apps or e-wallet and increasing adoption of digital payments in rural and urban areas.

By Product Type: Agricultural Inputs Dominate as Fresh Fruits & Vegetables Emerge as Fastest-Growing

The product type segment is led by agricultural inputs (seeds, fertilizers, pesticides) and delivered high revenues in repeating purchases and large B2B transaction volumes as they are preferred the most among farmer communities for uniform crop yield and quality.

Fresh fruits & vegetables are expanding the most quickly compared to the other segments, as consumer appetite for farm-to-consumer delivery increases, cold-chain logistics improve, and consumers increasingly seek fresh, traceable, and quality produce items.

By End User: Farmers Dominate as Retailers Emerge as Fastest-Growing

The end-user segment is dominated by farmers as they are among the first adopters of e-commerce platforms and use e-commerce-based platforms to buy inputs and sell their produce directly or through B2B channels.

The fastest growing segment in the fresh produce supply chain are retailers who are using e-commerce platforms to source fresh produce more effectively and cut back on intermediaries as consumer demand for convenient, fresh and traceable produce is expected to grow rapidly.

By Business Model: Marketplace-Based Model Dominates as Hybrid Model Emerges as Fastest-Growing

Marketplace-based models are the largest in the business model segment for their ability to scale quickly, operate asset-light, and with their high stakeholder connectivity.

The strongest growth category, hybrid models combine marketplace and inventory-led approaches, allowing increased control over product quality, fulfillment speed and consumer experience and providing farmers and businesses with greater digital reach.

E-commerce of Agricultural Products Market - Regional Analysis

Asia-Pacific E-commerce of Agricultural Products Market Insights:

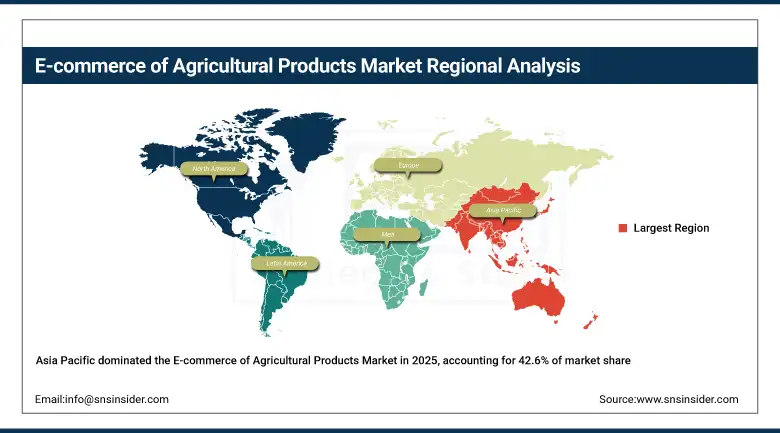

Asia-Pacific accounted for the largest and the fastest-growing E-commerce of Agricultural Products Market, with a share of 42.6% in 2025. The market is expected to grow at a CAGR of 11.1% from 2026 to 2035 supported by a strong agricultural base, benefits of digitization rapidly catering to farmers with a larger penetration of smartphones, internet, increased B2B and B2C platform expansions, growing adoption of digital agriculture among farmers supported by state and center allotted schemes, ever-increasing consumer-preferred demand for quality farm produce with traceability, increasing investments in cold-chain logistics, and growing awareness for F2C models across urban and semi-urban locations.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America E-commerce of Agricultural Products Market Insights:

Due to modern digital infrastructure, easy penetration of e-commerce platforms among farmers, and logistics networks, North America is a key market for agricultural products e-commerce. This lets the growth backed by an improving supply chain synchronization with supply chain tracking, electronic payment systems, and farm operations management. Other factors propelling the growth of this region include solid B2B and B2C platform standing, increasing need for fresh and premium agricultural commodities and progressive technological developments in precision agriculture and agri-tech innovations.

Europe E-commerce of Agricultural Products Market Insights:

Technologically advanced farming practices with high level of quality consciousness coupled with a wider adoption of digital platforms, makes Europe here a key market for e-ecommerce of agricultural products. The growing demand for sustainable, traceable, and fresh produce, a strong B2B and B2C platform presence, and government initiatives driving farm-to-table and digital agriculture solutions further drive growth. We also see benefits in the market from new supply chain management techniques, logistics optimization and the integration of analytics and digital payment systems across agricultural transactions.

Latin America E-commerce of Agricultural Products Market Insights:

E-commerce in agribusiness is steadily growing in Latin America, fueled by expanding internet access, the adoption of digital platforms by small and medium-scale farmers and the growth of logistics networks in the region. The B2B and B2C ones allows for direct selling to retail and consumers, facilitating efficiency, transparency, and access to fresh produce.

Middle East & Africa E-commerce of Agricultural Products Market Insights:

The Middle East & Africa market is slowly evolving as agriculture digitization, government support for e-marketplace, and demand for fresh and quality produce is driving it. B2B and B2C platforms, streamlined logistics and supply chain solutions will all contribute to making this market more efficient, and help bridge the gap between farmers and their consumers.

E-commerce of Agricultural Products Market Competitive Landscape:

Alibaba Group, which was founded in Hangzhou, China, is one of the world's leaders in offering a digital platform for e-commerce of agricultural products linking farmers, wholesalers, and consumers. Alibaba has used its Rural Taobao platform in these B2B and B2C plays to reach semi-urban (and rural) areas with supply chain improvement as well as agricultural inputs, fresh produce, and logistics solutions.

-

In March 2025: Alibaba expanded its Rural Taobao network, enhancing cold-chain logistics and digital payment integration to support farm-to-consumer and direct-to-retailer operations.

Seattle-based Amazon (Amazon Fresh & Amazon Business – Agriculture) is one of the prominent companies operating within the agricultural E-commerce sector, providing electronic platforms for both B2C and B2B transactions. Amazon reinforces its physical supply chain, speed of delivery, and cloud within its infrastructure to enable the procurement and resale of fresh produce and commercial level agricultural inputs to businesses and consumers.

-

In April 2025: Amazon strengthened its Amazon Fresh and Amazon Business agriculture offerings by expanding regional distribution centers and implementing advanced inventory and traceability systems.

E-commerce of Agricultural Products Market Key Players:

-

JD.com

-

Walmart

-

Flipkart

-

Ninjacart

-

AgroStar

-

DeHaat

-

Udaan

-

Tridge

-

Farmers Business Network

-

Corteva Agriscience

-

BASF Digital Farming Solutions

-

Bayer CropScience

-

Rivigo Agri Marketplace

-

ProducePay

-

Agrofy

-

Zalando Fresh

-

Olam Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 46.52 Billion |

| Market Size by 2035 | USD 116.23 Billion |

| CAGR | CAGR of 9.6% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type: (Fresh fruits & vegetables, grains & cereals, dairy, meat & poultry, agricultural inputs) • By Platform Type: (B2B, B2C, C2C) • By End User : (Farmers, distributors, processors, retailers, consumers) • By Business Model: (Marketplace-based, inventory-led, hybrid models) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Alibaba Group (Alibaba Rural Taobao), Amazon (Amazon Fresh & Amazon Business – Agriculture), JD.com (JD Agriculture), Walmart (Walmart Marketplace & Agri Supply Chain), Flipkart (Flipkart Farmer Connect), BigBasket, Ninjacart, AgroStar, DeHaat, Udaan, Tridge, Farmers Business Network (FBN), Corteva Agriscience (digital agri-input platforms), BASF Digital Farming Solutions, Bayer CropScience (FieldView & digital marketplaces), Rivigo Agri Marketplace, ProducePay, Agrofy, Zalando Fresh (EU fresh agri e-commerce platforms), Olam Group (digital agri-trading platforms) |

Frequently Asked Questions

Asia-Pacific dominated the E-commerce of Agricultural Products Market in 2025.

The “Agricultural Inputs” segment dominated during the projected period.

The key drivers of the E-commerce of Agricultural Products Market include rising internet penetration, smartphone adoption, digital payment infrastructure, demand for fresh produce, supply chain efficiency, and government agri-tech initiatives.

The market was valued at USD 46.52 Billion in 2025 and is projected to reach USD 116.23 Billion by 2035.

The E-commerce of Agricultural Products Market is expected to grow at a CAGR of 9.6% during 2026–2035.

Get in Touch