Echocardiography Market Size & Trends

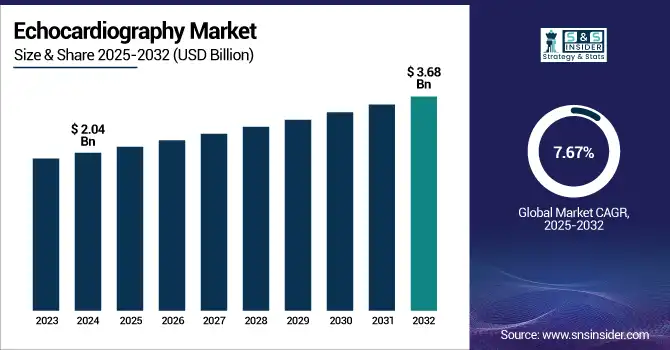

The Echocardiography Market was estimated at US$ 2.04 billion in 2024 and is expected to reach US$ 3.68 billion by 2032, growing at a CAGR of 7.67% over the forecast period of 2025-2032.

The echocardiography market is anticipated to grow at a strong rate driven by the growing prevalence of cardiovascular diseases, advancements in imaging technologies incorporating artificial intelligence (AI), and rising demand for non-invasive diagnostic tools. Ultrasound systems—be it hand-held or AI-assisted—simply aim for improving diagnostics, especially at the point of care, through accessibility and accuracy. While early diagnosis and efficient workflow are more important to healthcare providers, echocardiography is playing a central role in the future of cardiac care. Also key enablers are the supportive reimbursement policies and increasing applications for their use in hospitals, diagnostic centers, and ambulatory surgical centers.

To Get more information on Echocardiography Market - Request Free Sample Report

The U.S. echocardiography market size was valued at USD 0.52 billion in 2024 and is expected to reach USD 0.92 billion by 2032, growing at a CAGR of 7.41% over the forecast period of 2025-2032. The high prevalence of cardiovascular diseases, high-end healthcare infrastructure, and the presence of leading market players in the U.S. are expected to drive the growth of the North America echocardiography market. This leading position is bolstered in the region by favorable reimbursement policies and sustained R&D investments.

Echocardiography Market Dynamics

Drivers

-

Rising Prevalence of Cardiovascular Diseases is Accelerating the Market Growth

Cardiovascular diseases (CVDs), including coronary artery disease, heart failure, and valvular heart diseases, have ranked as the number one cause of death across the world. Lifestyle changes, ageing population, obesity, and diabetes have led to the escalating incidence of these diseases. With the increasing prevalence of heart-related diseases, there is a growing need for effective diagnostic instruments that can enable better early diagnosis and management. The growth of the market can be attributed to the high demand for echocardiography as it is a non-invasive imaging technique and is effective for the objective assessment of heart function, detection of abnormalities, and determination of the management of heart diseases.

For instance, as per WHO, Cardiovascular diseases (CVDs) are the number one globally for mortality, responsible for 17.9 million deaths each year, accounting for 32% of all deaths globally. Eighty-five percent of these deaths were due to heart attack and stroke.

-

Technological Advancements are Propelling the Market to Grow

Ongoing advancements in echocardiography technology have greatly improved echocardiographic capabilities and applications. The addition of artificial intelligence (AI) to automate imaging analysis improves the accuracy of diagnoses and reduces the time to interpret the images. 3D and 4D imaging allows more complex structures and dynamic interactions of the heart to be viewed more than any time previously, enabling novel and improved views of complex anatomy and pathophysiology, allowing better diagnostic capabilities for clinicians. Portable and hand-held echocardiography devices also became available, facilitating point-of-care diagnostics for emergency and outpatient settings, and other built-up settings. Introduction of such technological advancements broadens the scope of echocardiography, thereby driving the market growth.

Restraint

-

Limited Reimbursement Policies in Emerging Markets are Restraining the Market from Growing

In many low- and middle-income countries (LMICs), reimbursement policies for echocardiographic procedures are either limited or not well-established. This can also imply that insurance or government health programs may not pay for all costs associated with echocardiography tests. And that has led to higher out-of-pocket costs in many cases for patients, thereby dampening demand for these diagnostic services. Also, the limited reimbursement and/or uncertainty for the reimbursement of advanced echocardiography equipment can deter healthcare providers from making capital investments in these technologies. This financial barrier slows market growth and restricts access to echocardiographic diagnostics in certain regions.

For instance,

-

Many governments, such as in Ghana, provide coverage for a limited number of basic healthcare services, and a large proportion of advanced procedures are often not covered by the National Health Insurance Scheme (NHIS), including echocardiography. As a consequence, patients who need echocardiographic evaluations are often required to incur out-of-pocket costs, which can impose considerable economic difficulties.

-

A study in India published by BioMed Central has shown that patients travelling from outside the State to avail free cardiac care had significant out-of-pocket expenditure on travel. For travel, patients traveled an average of 1,178 miles for care and incurred an average travel expenditure of USD 104, or 27 days of the daily wage. This financial burden highlights the necessity of resources that make diagnostic services such as echocardiography more affordable and accessible.

Echocardiography Market Segmentation Analysis

By Device Type

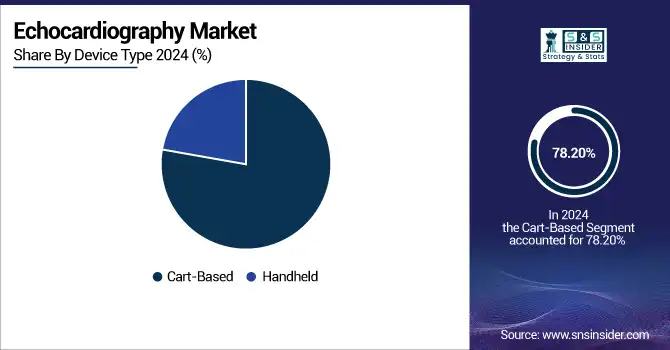

The Cart-Based segment dominated the echocardiography market share with a 78.20% in 2024 owing to its established presence in hospitals and diagnostics centers which need high-performance imaging systems. Such systems provide a better-quality image, 3D/4D imaging, and specially integrated reporting, making it the best choice for complete cardiac assessments. Well-equipped healthcare facilities prefer these due to their capability of handling high patient volumes and are supported by complex diagnostic workflows. Moreover, they integrate efficiently with AI tools, and large data can also be stored easily, which in turn improves clinical efficiency and contributes toward their more significant market share.

During the projected period, the handheld segment is expected to be the fastest-growing segment due to its portability, affordability, and increasing adoption in the point-of-care market. These handheld devices certainly come in handy in the emergency department, but also in rural clinics and home care, where immediate cardiac assessment is not a luxury, but a must. Recent advancements in wireless technology, artificial intelligence (AI), and smartphone integration have made them more user-friendly and diagnostic-sensitive than ever before. The shift towards decentralization of healthcare and point-of-care testing for quicker access to diagnostic tools is are major factor contributing to the growth of handheld echocardiography devices in developed and developing regions.

By Test Type

Transthoracic Echocardiography segment dominated the echocardiography market with a 42.05% market share in 2024, owing to its non-invasive, easy-to-use, and easily accessible nature. TTE is the most frequently used echocardiogram and generally serves as a first-line examination to assess cardiac function, chamber size, valvular disorders, and pericardial diseases. This imaging mode provides rapid, real-time images without requiring sedation, specialized procedures, and has made itself a widely preferred modality in outpatient and inpatient settings alike. Furthermore, ongoing improvements in TTE imaging technology have made it more accurate and can be used in diagnosing, which further helps TTE retain its leading market position.

The stress echocardiography segment is anticipated to exhibit the fastest-growing segment, which is due to the growing demand for functional and dynamic cardiac assessments. The identification of coronary artery disease and myocardial viability under physical or pharmacological demand has an important place for stress echocardiography. A rising international threat from ischemic heart disease, combined with increasing awareness around preventive cardiology and early detection, is compounding calls for more functional testing strategies. In addition, improvements in imaging software and integration with exercise and pharmacological protocols are increasing test accuracy and facilitating rapid dissemination in clinical and outpatient practices.

By Technology

In 2024, the 2D segment dominated the echocardiography market with a 66.30% market share, known for its significant usage and proven capability as a cardiac imaging life science, Due to its high reliability, ease of use and economical price, it has been the first-order method of choice for routine echocardiographic assessment in hospitals and diagnostic centers. Two-dimensional (2D) echocardiography, which gives clinicians clear, real-time images of heart structures, plays a critical role in the diagnosis of many cardiovascular conditions. Its compatibility with current ultrasound systems and wide clinical acceptance further enhance its leading market share.

The 3D & 4D segment is anticipated to witness the fastest growth during the forecast period, owing to rising demand for precise cardiac imaging. These state-of-the-art imaging modalities allow for three-dimensional (3D) and real-time visualisation of the heart, enhancing evaluation of complex anatomical structures and diagnostic accuracy. 4D scanning, which captures heart motion dynamically, enhances clinical decision-making in a setting of interventions as well as surgical planning. The 3D and 4D echocardiography market is gaining popularity, driven by the growing penetration of 3D and 4D echocardiography in both specialist cardiac centers and general healthcare centers, along with technological innovations that reduce the potential barriers of 3D echocardiography by reducing costs and making trisomies easier to use.

By End-User

The Hospitals & ASCs segment held the largest share of the echocardiography market in 2024, with a 76.19%, as hospitals and ASCs have the required infrastructure, trained staff, and advanced imagery systems to perform a variety of echocardiographic procedures. In places with significant patient volume, such as hospitals and ASCs, there is a need to address complex cardiac cases requiring advanced imaging and diagnostic capabilities. They are best suited as end-users with their integrated care from diagnosis to treatment with an echocardiography system. And in these settings, reimbursement policies and funding further entrench the use of advanced, high-cost echocardiography technologies and their dominant position in the market.

The diagnostic center segment is anticipated to lead in growth during the forecast period, owing to a rising number of standalone outpatient facilities that focus on specialized cardiac diagnostics. These centers offer accessible, cost-effective, and timely echocardiography services and attract patients due to the reduced waiting time for diagnosis without the need for hospital admission. Increasing awareness regarding cardiovascular health and preventive care is boosting the demand for non-invasive cardiac tests in diagnostic centers. Additionally, the rapid market growth of these centers in the urban and underserved areas is also due to technological advancements such as portable and handheld devices, which are making it easier to offer more services.

Echocardiography Market Regional Insights

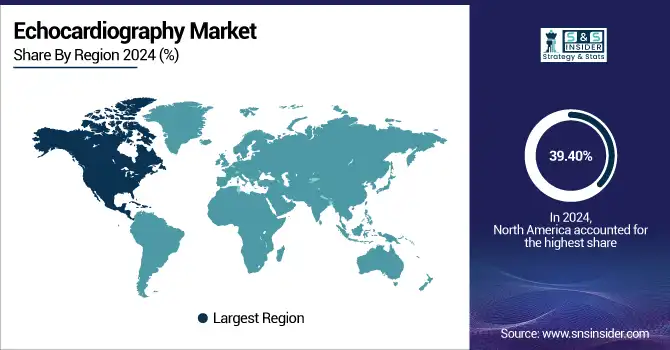

North America dominated the echocardiography market with a 39.40% market share in 2024, owing to its developed healthcare infrastructure, high healthcare expenditure, and adoption of advanced diagnostic technologies, with a niche for cutting-edge technologies. This is due to the high prevalence of cardiovascular diseases in the region, which increases the demand for non-invasive imaging techniques, particularly echocardiographic technical reports. Moreover, the presence of key industry players such as GE HealthCare, Philips Healthcare, and Siemens Healthineers boosts innovation and accessibility. North America will continue its reign as the global market leader, backed by favorable reimbursement frameworks coupled with unprecedented government and private sector investments in healthcare.

The echocardiography market fastest-growing region is Asia Pacific, with 8.60% CAGR over the forecast period, due to the increasing prevalence of cardiovascular diseases along with growing awareness and investments in health infrastructure. The increasing prevalence of heart diseases due to rapid urbanization and changing lifestyles in developing nations such as China, India, and Japan is driving the echocardiography market over the forecast period. In addition, the rapid increase of the middle-class population and better access to healthcare services in the region, combined with the government's efforts toward modernization of the healthcare system, are driving the market growth exponentially. Affordable and portable newer generation echocardiography devices are also allowing more have access to the service, including rural and underserved areas.

The echocardiography market in Europe is growing due to the high prevalence of cardiovascular diseases and a higher emphasis on early diagnosis and preventive healthcare. This expansion range is driven by a few countries such as Germany, France, and the UK, owing to their robust healthcare systems and high investments in medical imaging technologies.

Jan 2023 Pie Medical Imaging Releases AI-Driven Echocardiography Platform The CAAS Qardia 2.0, which is an update to the CAAS Qardia echocardiography software platform, includes AI-enabled workflows and advanced imaging and analysis for cardiac measurements.

Moreover, the expanding importance of value-based healthcare and a surge in clinical research throughout more European countries all contribute to an increased endorsement of echocardiographic practices. Novel echocardiography devices that are portable and/or integrate artificial intelligence are also catching on, especially in outpatient and primary care settings. The combined above-mentioned factors make Europe a high revenue contributing and continuously growing regional market of the global echocardiography market.

The echocardiography market analysis in Latin America is growing moderately due to rising awareness of cardiovascular health, as well as a few measures for further development of the healthcare infrastructure in a few countries. Some of the countries spearheading this growth are Brazil and Mexico, with the support of government initiatives and medical device companies. On the other hand, factors such as economic instability and low healthcare may stagnate adoption. Continuous innovation in portable and AI-powered echocardiography systems, introduction of cost-effective solutions in the market, and rising demand for accurate and early diagnosis are among some of the factors, which expected to fuel demand for echocardiography.

In the Middle East and Africa (MEA) region, moderate growth of the echocardiography market is driven by the enhancement of healthcare infrastructure along with rising awareness regarding heart diseases. This expansion is being supported through government initiatives and several collaborations with international medical device companies. But, economic issues and a shortage of tax-funded healthcare may slow rapid take-up. Thus, rising utilization of portable echocardiographs and integration of artificial intelligence in echographic devices are anticipated to propel the regional market progress throughout the analysis.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players in the Echocardiography Market

GE HealthCare, Philips Healthcare, Siemens Healthineers, Canon Medical Systems Corporation, Mindray Medical International Limited, FUJIFILM Sonosite, Samsung Medison, Esaote SpA, Hitachi, Konica Minolta Healthcare Americas, and other players.

Recent Developments

-

June 2024 – Royal Philips announced the launch of its next-generation AI-enabled cardiovascular ultrasound platform. This advanced system is designed to accelerate cardiac ultrasound analysis using proven artificial intelligence technology, aiming to reduce the workload on echocardiography laboratories and improve diagnostic efficiency.

-

August 2024 – GE HealthCare received CE Mark approval for its Vscan Air SL, a wireless handheld ultrasound system integrated with Caption AI. This AI-powered software tool enables rapid cardiac assessments at the point of care. Additionally, the company introduced ECG-less cardiac CT scanning on its Revolution Apex platform, which allows clinicians to capture cardiac images without relying on the patient's electrocardiogram (ECG) signal.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.04 Billion |

| Market Size by 2032 | USD 3.68 Billion |

| CAGR | CAGR of 7.67% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Device Type (Cart-Based, Handheld) • By Test Type (Transthoracic Echocardiography, Transesophageal Echocardiography, Stress Echocardiography, Others) • By Technology (2D, 3D & 4D, Doppler Imaging) • By End-user (Hospitals & ASCs, Diagnostic Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | GE HealthCare, Philips Healthcare, Siemens Healthineers, Canon Medical Systems Corporation, Mindray Medical International Limited, FUJIFILM Sonosite, Samsung Medison, Esaote SpA, Hitachi, Konica Minolta Healthcare Americas, and other players |

Frequently Asked Questions

Ans: By device type, the cart-based segment is anticipated to dominate the market.

Ans: The benefits of echocardiography over other cardiac diagnostic procedures and the increased frequency of heart disease are the main market-driving drivers.

Ans: The Key Players in the Echocardiography Market GE Healthcare, Koninklijke Philips, Siemens Healthcare, Toshiba Medical Systems, ALPINION MEDICAL SYSTEMS, Bay Labs, Biosense Webster, Boston Scientific, Bracco Imaging, Carestream Health, CHISON, ContextVision, Digirad, Ecare Medical and others.

Ans: Echocardiography market was estimated at US$ 1.76 billion in 2022 and is expected to reach US$ 3.05 billion by 2030.

Ans: The CAGR Growth rate of Echocardiography Market is approx. CAGR of 7.1% predicted for the forecast period of 2023-2030.

Get in Touch