Pharmaceutical Market Report Scope & Overview:

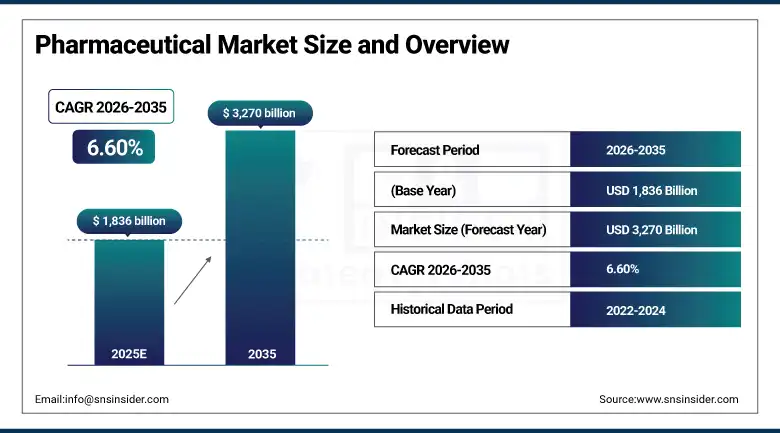

Pharmaceutical Market was valued at USD 1,836 billion in 2025 and is expected to reach USD 3,270 billion by 2035, growing at a CAGR of 6.60% from 2026-2035.

The pharmaceutical industry is experiencing an increase in its size owing to high global health problems, increasing population, and demand for sophisticated treatment methods. Research and development activities, increased accessibility in healthcare, and innovations in drug delivery methods ensure industry growth. Other factors include government initiatives and the increased availability of generic drugs and biosimilars.

The WHO estimates that non-communicable diseases account for 74% of all global deaths annually, driven by cardiovascular disease, cancer, diabetes, and respiratory conditions each requiring ongoing pharmaceutical treatment. The U.S. FDA approved 55 novel drugs in 2023, one of the highest annual totals in the agency's history, reflecting the pace of pharmaceutical innovation reaching commercial launch.

Pharmaceutical Market Size and Forecast

-

Market Size in 2025: USD 1,836 Billion

-

Market Size by 2035: USD 3,270 Billion

-

CAGR: 6.60% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information On Pharmaceutical Market - Request Free Sample Report

Pharmaceutical Market Trends

-

GLP-1 receptor agonists for obesity and type 2 diabetes including semaglutide and tirzepatide have become the fastest-growing drug category in pharmaceutical history, reshaping cardiovascular, metabolic, and obesity treatment paradigms.

-

AI-accelerated drug discovery is compressing development timelines, with AI-designed candidates reaching clinical trials in under a year compared to the conventional 4-6 year preclinical phase.

-

Biosimilar competition is intensifying as major biologic patents expire, with dozens of biosimilar approvals annually creating pricing pressure on originator biologics and expanding patient access globally.

-

Precision oncology matching cancer therapies to specific molecular tumor profiles through companion diagnostic testing is creating premium-priced targeted therapy market segments growing well above the broader oncology market rate.

-

Cell and gene therapy commercial launches are accelerating, with over 20 approved products in the U.S. and EU and growing manufacturing capacity investments making these ultra-premium therapies increasingly accessible.

-

Pharmaceutical companies are integrating AI and digital biomarker data into clinical trials, improving patient selection, endpoint measurement accuracy, and trial efficiency in ways that reduce development costs.

-

Sustainability pressures are reshaping pharmaceutical manufacturing, with companies setting Scope 1 and 2 emissions reduction targets, adopting green chemistry principles, and transitioning inhaler propellants to low-GWP formulations.

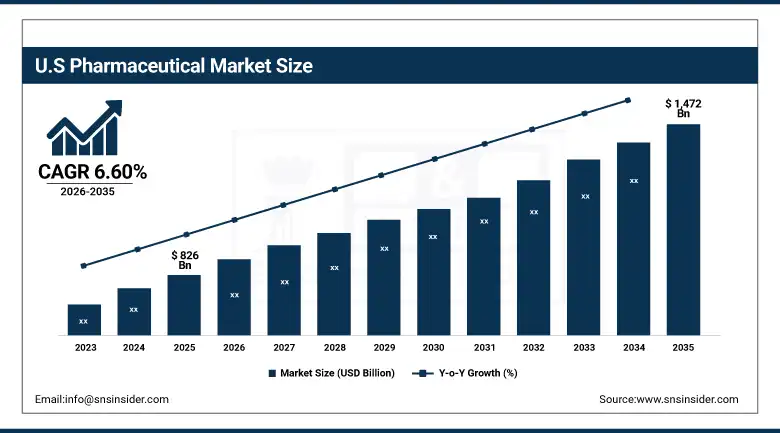

U.S. Pharmaceutical Market was valued at USD 826 billion in 2025 and is expected to reach USD 1,472 billion by 2035, growing at a CAGR of 6.60% from 2026-2035.

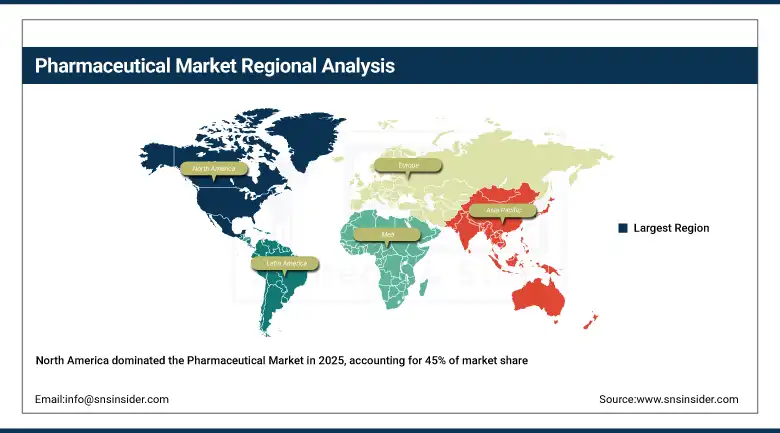

North America accounted for 45% of global pharmaceutical market revenue in 2023, and the United States is overwhelmingly the source of that position. The U.S. is the world's most important pharmaceutical market not just by size but by price drug prices in the U.S. are typically 2-4 times higher than in other developed markets for the same products, which means the U.S. often generates more than half of global pharmaceutical revenues for branded products.

The FDA's Center for Drug Evaluation and Research approved 55 novel drugs in 2023, including 12 first-in-class medicines. The Inflation Reduction Act's Medicare Drug Price Negotiation Program selected the first 10 drugs for negotiation in 2023, with negotiated prices taking effect in 2026 representing the first direct federal pharmaceutical price negotiation in Medicare history.

Pharmaceutical Market Segment Analysis

-

By Molecule Type, Conventional/Small Molecule dominated with ~54% share in 2025; Biologics fastest growing (CAGR).

-

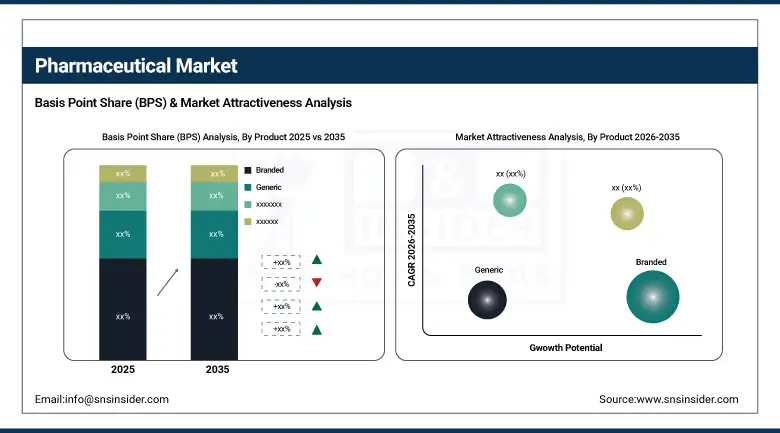

By Product, Branded segment dominated with ~66% share in 2025; Generic segment growing with patent expirations.

-

By Type, Prescription segment dominated with ~88% share in 2025; OTC growing in consumer health.

-

By Disease, Cancer dominated with ~17% share in 2025; Neurology and metabolic disease fastest growing.

-

By Route of Administration, Oral route dominated with ~57% share in 2025; Injectable growing with biologic expansion.

-

By Formulation, Tablets dominated with ~27% share in 2025; Advanced delivery formats growing.

-

By End Market, Hospitals dominated with ~53% share in 2025; Online Pharmacies fastest growing (CAGR).

By Molecule Type, Conventional/Small Molecule segment dominates the Pharmaceutical Market, Biologics segment expected to grow fastest

Conventional drugs small molecule compounds synthesized through chemical processesheld approximately 54% of pharmaceutical market revenue in 2025. Their dominance reflects the breadth and depth of established small molecule therapy across virtually every disease category: cardiovascular drugs, antibiotics, antidiabetics, analgesics, antivirals, and psychiatric medications are all predominantly small molecule. Well-developed manufacturing processes, established regulatory pathways, oral bioavailability that enables patient self-administration, and predictable pharmacokinetics make small molecules the reliable foundation of pharmaceutical treatment across most disease areas.

Large molecule biologic drugs such as monoclonal antibodies, gene therapies, vaccines, and recombinant proteins are currently the leading market, owing to the breakthrough clinical performance of these drugs in areas like cancer and rare diseases, where small molecule medicines do not offer any cure. Drugs such as checkpoint inhibitors, CAR T-cells, bispecific antibodies, and mRNA vaccines have paved the way for the growth of biologics.

By Product, Branded segment dominates the Pharmaceutical Market, Generic segment growing with patent expirations

Branded drugs accounted for the highest market share of around 66%, owing to their high brand visibility, perceived high quality, patient and prescribing physician trust, and higher premiums charged because of the innovation-driven portfolio. The pharma industry is highly invested in building brand visibility through consumer direct marketing in the United States and physician detailing worldwide. The government’s focus on encouraging pharmaceutical research and development innovation has been crucial in the development of branded drugs. In particular, the United States has had an exclusive period of 12 years for biologicals and five years for small molecules for complete premium pricing.

Generic drugs are steadily increasing as brand name drug patents expire, and the pharmaceutical industry is currently facing a very large patent cliff over the years of 2025 to 2030, where drugs earning more than USD 200 billion annually will be coming off their patent protection. The strength of the Indian pharmaceutical industry in generic production is very crucial in terms of producing 20% of world generics and almost 40% of generics used in the U.S.

By End Market, Hospitals segment dominates the Pharmaceutical Market, Online Pharmacies expected to grow fastest

Hospitals held the largest end-market revenue share of approximately 53% in 2025. This is a structural position, not a coincidence: hospitals treat the sickest patients who require the most expensive medicines oncology infusions, immunosuppressants for organ transplants, antifungal treatment for critically ill patients and they purchase pharmaceuticals through institutional procurement programs that generate large and predictable order volumes. Hospital formulary decisions made by pharmacy and therapeutics committees determine which drugs get used in inpatient settings, giving hospitals significant influence over pharmaceutical consumption patterns that extends beyond their walls through the prescribing habits of hospital-based physicians.

Online pharmacies are growing fastest among end-market channels, driven by the combination of post-pandemic consumer comfort with digital healthcare services, convenience advantages over traditional retail pharmacy visits, competitive pricing enabled by lower overhead structures, and expanding insurance coverage that includes digital pharmacy benefit management. Platforms like Amazon Pharmacy, Hims & Hers, and numerous market-specific online pharmacy services are reaching consumer segments that traditional retail pharmacies serve inadequately particularly in rural areas, for patients with mobility limitations, and for consumers of ongoing maintenance medications who value the predictability of subscription delivery over monthly pharmacy trips.

Pharmaceutical Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

91% |

|

Europe |

Germany |

25% |

|

Asia Pacific |

Japan |

35% |

|

Middle East & Africa |

Saudi Arabia |

35% |

|

Latin America |

Brazil |

45% |

North America Pharmaceutical Market Insights

North America dominated the global Pharmaceutical Market with approximately 45% revenue share in 2023, anchored entirely by the United States' unique combination of premium drug pricing, world-leading pharmaceutical innovation, the largest concentration of blockbuster drug launches, and the highest per-capita pharmaceutical expenditure of any country. The U.S. pharmaceutical market's premium is not just a price story it is an innovation story. The country houses the majority of the world's most innovative pharmaceutical companies, and the venture capital ecosystem that funds early-stage drug development is more active in the U.S. than anywhere else. The Inflation Reduction Act's drug pricing provisions are introducing market dynamics that pharmaceutical companies must navigate, but the structural attractiveness of the U.S. market for new drug launches remains fundamentally intact.

Get Customized Report as per Your Business Requirement - Enquiry Now

The NIH invested USD 47.5 billion in biomedical research in fiscal year 2023, providing the foundational research that underpins U.S. pharmaceutical innovation. PhRMA member companies invested USD 102.3 billion in pharmaceutical R&D in the U.S. in 2023, the highest annual R&D investment in the industry's history.

Asia Pacific Pharmaceutical Market Insights

Asia-Pacific is the fastest-growing market in the pharma industry owing to the presence of India as the leader in the production of generics, Japan and South Korea as innovators in the pharmaceutical field, the huge domestic market of China, and the increasing spending on health care in the growing middle-class population of the Asia-Pacific region. India, which has 20% of total generics and ranks number three in the world in the manufacture of pharmaceuticals, is the pharmacy of the world in producing cheap medicine that contributes 40% to the total generic prescriptions in the U.S. and 25% to the total medicines produced in the UK. The domestic pharmaceutical market in China is the second largest in the world.

India's government aims to increase healthcare expenditure to 2.5% of GDP by 2025, supporting pharmaceutical market expansion. India's Production-Linked Incentive (PLI) scheme for pharmaceutical APIs has attracted over USD 2 billion in committed manufacturing investments from domestic and international companies.

Europe Pharmaceutical Market Insights

About 20% of the pharmaceuticals market belongs to Europe, where the major contributors include Germany, France, Switzerland, UK, and Scandinavia. European companies like Roche, Novartis, AstraZeneca, Sanofi, and Bayer belong to the league of most innovative pharmaceutical companies globally with extensive investments in research & development and global drug development programs originating from European institutes. The European Medicines Agency has gradually simplified the approval process for innovative drugs using adaptive licensing and conditional approval methods.

The EMA approved 89 new medicines in 2023, including 31 orphan medicines for rare diseases. The EU's Pharmaceutical Legislation reform package proposes reducing data exclusivity for branded medicines from 8 to 6 years while introducing incentives for medicines addressing unmet medical needs in conditions disproportionately affecting low-income populations.

Middle East & Africa and Latin America Pharmaceutical Market Insights

These two markets continue to witness growth in the pharmaceutical market due to developments in healthcare infrastructures, insurance penetration, and treatment accessibility. The Saudi Arabian Vision 2030 initiative for reforming the country’s healthcare sector involves developing the pharmaceutical industry and creating incentives for local production of drugs. Similarly, the UAE government has established a regulatory framework for the country's pharmaceutical industry that is meeting international standards, which has lured foreign companies to invest in manufacturing in the UAE. In Latin America, the public health program SUS of Brazil offers free medicines to millions of Brazilians, providing consistent public procurement demand along with the private market demand.

Brazil's Ministry of Health pharmaceutical expenditure exceeds BRL 15 billion annually through the SUS public pharmaceutical assistance program. Saudi Arabia's Saudi Food and Drug Authority (SFDA) has established pharmaceutical manufacturing standards and local content requirements under Vision 2030 that are driving domestic pharmaceutical production investment.

Pharmaceutical Market Growth Drivers:

-

Rising chronic disease prevalence and sustainable energy-efficient pharmaceutical innovation driving global pharmaceutical market expansion

The fundamental demand driver of pharmaceutical market growth is demographic and epidemiological inevitability: more people, living longer, with chronic diseases requiring ongoing treatment. Global cancer cases are projected to reach 22 million annually by 2030. Diabetes affects over 530 million people globally with that number growing. Cardiovascular disease remains the world's leading cause of death, requiring continuous pharmaceutical management. None of these disease burdens are abating they are intensifying as populations age and as obesity, sedentary lifestyles, and environmental factors compound biological aging. Simultaneously, the pharmaceutical innovation pipeline has never been richer: targeted oncology, gene therapy, GLP-1 metabolic medicine, and mRNA vaccine technology are each generating new drug classes that command premium pricing for genuine clinical advancement, sustaining revenue growth beyond volume-driven demand alone.

The WHO projects global cancer cases will reach 22 million annually by 2030. The International Diabetes Federation reports that diabetes prevalence will affect 783 million people globally by 2045, creating an enormous expanding market for antidiabetic medicines including GLP-1 receptor agonists.

Pharmaceutical Market Restraints:

-

Stringent regulatory frameworks and high R&D costs creating compliance complexity and limiting timely introduction of new therapies

The pharmaceutical industry operates under some of the most stringent regulatory requirements of any global industry, and those requirements are becoming more complex rather than less. The FDA, EMA, PMDA in Japan, and equivalent agencies in major markets each maintain comprehensive requirements for clinical evidence, manufacturing quality, pharmacovigilance, and post-market commitments that impose substantial ongoing compliance costs. Over 65% of pharmaceutical firms reported increased compliance costs in 2024 due to changing regulatory guidelines across key markets according to IFPMA data. The average cost of developing a new drug exceeds USD 2 billion and takes more than 10 years a timeline and investment level that concentrates pharmaceutical R&D capacity in the largest companies and creates barriers to smaller innovators bringing genuinely novel approaches to market at competitive timescales.

Pharmaceutical Market Opportunities:

-

AI-accelerated drug discovery and biologics innovation creating transformative new pharmaceutical development and commercial opportunities

AI is genuinely reshaping what pharmaceutical R&D can accomplish and at what cost. Drug candidates that once took 4-6 years to progress from target identification to clinical trial entry are now reaching IND submission in under a year through AI-accelerated structure prediction, molecular dynamics simulation, and automated synthesis pathway optimization. Exscientia's AI-designed drug DSP-1181 reaching clinical trials in under a year compared to the conventional multi-year timeline is the type of case study that is reshaping R&D budget allocation at major pharmaceutical companies. Beyond speed, AI-enabled patient selection for clinical trials using biomarker profiles and real-world evidence is improving trial success rates in ways that reduce the enormous sunk cost of late-stage trial failures. The biologics innovation wave GLP-1, checkpoint immunotherapy, cell therapy, gene editing is simultaneously creating premium commercial opportunities for companies with the scientific and manufacturing capabilities to compete in these advanced therapy categories.

Recent Developments:

-

2025: Eli Lilly received FDA approval for tirzepatide (Zepbound) for obstructive sleep apnea in adults with obesity expanding the clinical indication for its blockbuster GLP-1/GIP dual agonist beyond weight management and type 2 diabetes to a condition affecting over 30 million Americans, significantly expanding the drug's addressable patient population.

-

2025: Pfizer launched a comprehensive portfolio restructuring program following its COVID-19 product revenue normalization, announcing USD 4 billion in annual cost savings while accelerating oncology and specialty medicine pipeline investments including RNA-based therapeutics and targeted protein degradation platforms for next-generation cancer treatment.

-

2026: Novo Nordisk reported pivotal Phase 3 trial data for its next-generation oral semaglutide formulation demonstrating superior efficacy to existing injectable versions in both cardiovascular risk reduction and body weight management, potentially establishing oral GLP-1 therapy as a first-line treatment option for the hundreds of millions of patients who decline injectable medications.

Pharmaceutical Market Key Players

Some of the Pharmaceutical Market Companies

-

Pfizer Inc.

-

Johnson & Johnson

-

Roche Holding AG

-

Novartis AG

-

Merck & Co., Inc.

-

Sanofi S.A.

-

AstraZeneca PLC

-

GlaxoSmithKline plc (GSK)

-

Eli Lilly and Company

-

Bristol-Myers Squibb Company

-

AbbVie Inc.

-

Moderna, Inc.

-

Gilead Sciences, Inc.

-

Bayer AG

-

Takeda Pharmaceutical Company Ltd.

-

Amgen Inc.

-

Biogen Inc.

-

Regeneron Pharmaceuticals, Inc.

-

Boehringer Ingelheim GmbH

-

Teva Pharmaceutical Industries Ltd.

Pharmaceutical Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1,836 Billion |

| Market Size by 2035 | USD 3,270 Billion |

| CAGR | CAGR of 6.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Molecule Type (Conventional/Small Molecule, Biologics) • By Product (Branded, Generic) • By Type (Prescription, OTC) • By Disease (Cancer, Cardiovascular, Diabetes, Musculoskeletal, Neurology, Others) • By Route of Administration (Oral, Injectable, Topical, Others) • By Formulation (Tablets, Capsules, Injectables, Topical, Others) • By End Market (Hospitals, Retail Pharmacies, Online Pharmacies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Pfizer Inc., Johnson & Johnson, Roche Holding AG, Novartis AG, Merck & Co., Inc., Sanofi S.A., AstraZeneca PLC, GlaxoSmithKline plc (GSK), Eli Lilly and Company, Bristol-Myers Squibb Company, AbbVie Inc., Moderna, Inc., Gilead Sciences, Inc., Bayer AG, Takeda Pharmaceutical Company Ltd., Amgen Inc., Biogen Inc., Regeneron Pharmaceuticals, Inc., Boehringer Ingelheim GmbH, and Teva Pharmaceutical Industries Ltd. |

Frequently Asked Questions

North America dominated the Pharmaceutical Market with approximately 45% share in 2025.

The Online Pharmacies segment is expected to register the fastest CAGR in the Pharmaceutical Market through 2035.

The Conventional/Small Molecule segment dominated with approximately 54% share in 2025.

The Pharmaceutical Market was valued at USD 1,836 billion in 2025.

The Pharmaceutical Market is expected to grow at a CAGR of 6.60% from 2026 to 2035.

Get in Touch