EPC Engineering Procurement and Construction Market Report Scope & Overview:

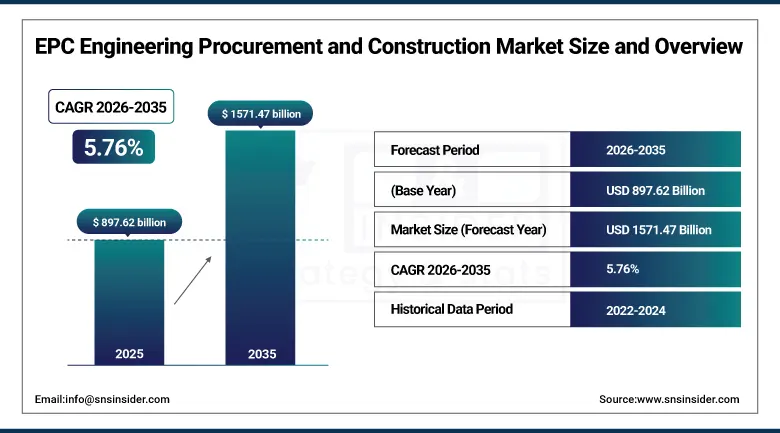

The EPC Engineering Procurement and Construction Market was valued at USD 897.62 Billion in 2025 and is expected to reach USD 1571.47 Billion by 2035, growing at a CAGR of 5.76% from 2026-2035.

The EPC engineering procurement and construction market is growing due to increasing global infrastructure projects, urbanization, and investment in projects related to energy, oil & gas, and renewable energy. There is an increasing focus from governments for massive infrastructure development projects in the form of transportation, smart cities, and industrial parks, along with more investment in utilities and construction from the private sector. The global trend toward clean energy transition, infrastructure modernization, and construction through advanced technologies like digital project management and modular construction is also fueling market growth.

Australia's Woodside Energy Group has secured an EPC contract with U.S. engineering firm Bechtel to develop the Louisiana liquefied natural gas (LNG) project. The project's first phase will consist of three production trains with a combined capacity of 16.5 million tons per annum. The Abu Dhabi National Oil Company (ADNOC) secured $5.5 billion worth of contracts to construct the Ruwais LNG plant, set to more than double the UAE’s LNG output. The plant aims to produce 9.6 million metric tons per annum of LNG, raising ADNOC’s total capacity to 15 million metric tons per annum.

Market Size and Forecast

-

Market Size 2026E: USD 949.32 Billion

-

Market Size 2035: USD 1571.47 Billion

-

CAGR (2026-2035): 5.76%

-

Fastest Growing Market: Asia Pacific

-

Largest Market: North America

To Get more information on EPC Engineering Procurement and Construction Market - Request Free Sample Report

EPC Engineering Procurement and Construction Market Trends

-

Rising infrastructure development and industrial projects are driving the EPC (Engineering, Procurement, and Construction) market.

-

Growing adoption across energy, oil & gas, power, and transportation sectors is boosting market growth.

-

Integration of digital tools, BIM, and project management software is enhancing efficiency and cost control.

-

Expansion of renewable energy and smart infrastructure projects is fueling demand for EPC services.

-

Increasing focus on timely project delivery, quality assurance, and risk management is shaping market trends.

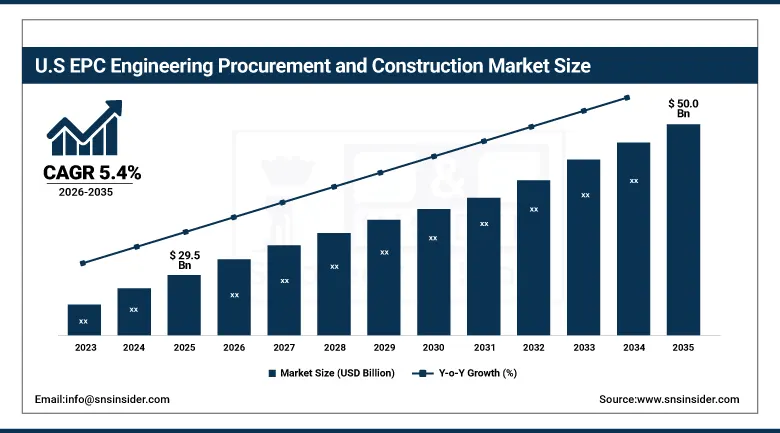

U.S. EPC Engineering Procurement and Construction Market Size Outlook

The U.S. EPC Engineering Procurement and Construction Market was valued at USD 29.5 billion in 2025 and is expected to reach USD 50 billion by 2035, growing at a CAGR of 5.4% from 2026-2035.

U.S. EPC Engineering, Procurement, and Construction market is expected to see growth owing to higher modernization of infrastructures, higher investment in renewable energy projects, and developments in the field of oil and gas. Government efforts towards building smart cities, automation, and energy transition, along with active participation by the private sector, are adding to growth momentum.

EPC Engineering Procurement and Construction Market Segment Analysis

-

-

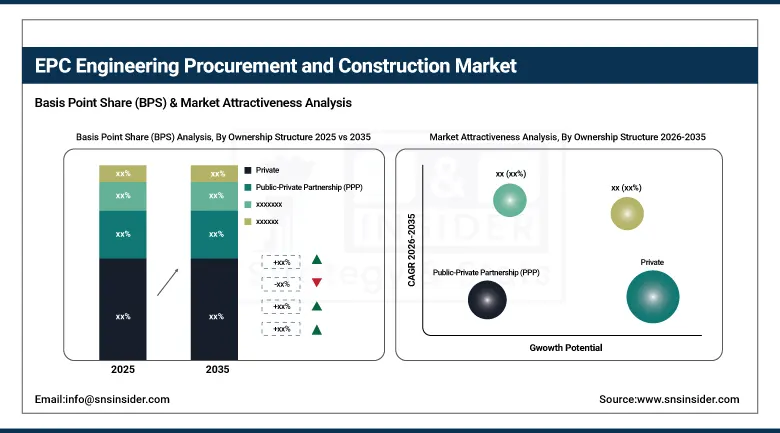

By Ownership Structure, private segment dominated the EPC engineering procurement and construction market in 2025 with 56% share; Public-Private Partnership (PPP) segment is the fastest-growing.

-

By Industry, oil and gas segment dominated the EPC engineering procurement and construction market in 2025 with 36% share; infrastructure segment is the fastest-growing.

-

By Service Type, construction segment dominated the EPC engineering procurement and construction market in 2025 with 29% share; turnkey segment is the fastest-growing.

-

By Contract Value, $10–50 million segment dominated the EPC engineering procurement and construction market in 2025 with 31% share; above $100 million segment is the fastest-growing.

-

By Project Type, greenfield projects segment dominated the EPC engineering procurement and construction market in 2025 with 63% share; greenfield projects segment is the fastest-growing.

-

By Ownership Structure, Private segment dominates the Market, Public-Private Partnership (PPP) segment expected to grow fastest

The private segment is considered dominant in the EPC engineering, procurement, and construction industry, owing to their high financial flexibility, quick decision-making process, and lower reliance on the time-consuming public approval procedures. The quick capital mobilization capabilities and tighter project management of the private organizations ensure quick completion of projects through an effective procurement process. The use of modern technologies for construction and the ability to forge strategic alliances improves the chances of winning larger industrial projects.

Public-Private Partnership (PPP) represents the highest growth segment in the EPC industry owing to the benefits associated with shared investments in projects by governments and the private sector, helping to minimize the burden on resources and lowering the risk factors. As the need for developing larger infrastructure projects in areas like transport, energy, and urban development is increasing, the popularity of PPPs in the EPC space is growing.

By Industry, Oil and Gas segment dominates the Market, Infrastructure segment expected to grow fastest

The oil and gas industry leads in the EPC engineering procurement and construction market owing to the continuous demand for energy worldwide, significant investment in the upstream and downstream sectors, and highly sophisticated infrastructure needs. Such an industry demands large investments in technological advancement, highly value-oriented business deals, and long project periods, thus creating more involvement in EPCs. The ongoing drilling and refining processes and pipeline expansion efforts along with steady consumption trends and massive investments in the private energy sector are helping maintain this leadership position.

The infrastructure segment grows at the highest rate among all segments owing to increasing urbanization rates and dense populations, as well as high government spending on infrastructure projects, particularly transport and energy infrastructure. Growing infrastructure requirements such as road construction and railway construction, together with infrastructural modernization and major infrastructure projects in developing economies, have resulted in increasing EPCs.

By Service Type, Construction segment dominates the EPC Engineering Procurement and Construction Market, Turnkey segment expected to grow fastest

The construction segment dominates the EPC engineering procurement and construction market owing to its critical importance in executing projects that include civil work, structural work, and construction at the site. It forms the backbone of all EPC projects in both industrial, infrastructure, and energy segments. The strong demand for extensive construction activities, labor-intensive nature, and continuous capital infusion make it a dominant segment, driven by growth in urbanization and industrialization worldwide.

The turnkey segment is the fastest-growing segment, owing to the increase in preference for single-point responsibility in EPC projects, wherein a single contractor is responsible for all three elements of design, procurement, and construction. The growing preference for turnkey services for large industrial and infrastructure projects, owing to their cost-effectiveness and easy project execution, is driving the growth of the turnkey EPC segment across the globe.

By Contract Value, $10–50 million segment dominates the Market, Above $100 million segment expected to grow fastest

The $10–50 million contract value segment dominates the EPC engineering procurement and construction market due to the ideal blend of project size, low risk, and consistent availability in industrial and infrastructure projects. This segment is highly popular because it offers the advantages of easy finance arrangements, swift approval process, and assured completion within an expected time period. The segment caters to medium-sized project demands in energy, utility, and commercial construction industries.

The above $100 million segment is the fastest growing since there is increasing demand for mega infrastructure development projects such as smart cities, highway roads, airports, and mega energy projects. Increasing governmental investment and increased participation from private players in these projects are rapidly leading to the growth of the above $100 million contract value segment.

By Project Type, Greenfield projects dominate the EPC Engineering Procurement and Construction Market, Greenfield projects also expected to grow fastest

Greenfield projects account for the majority share in the EPC market owing to their larger scale of development requiring the construction of new facilities on undeveloped land. These projects provide high revenue generation, more design possibilities, and investment opportunities on a long term basis. Urbanization, industrialization, and increased demands for infrastructure have been the factors promoting the growth of such projects around the world. Greenfield projects have been witnessing the highest growth in terms of revenues owing to increasing investment opportunities in developing countries, smart cities, and

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

91.9% |

|

Europe |

United Kingdom |

24.6% |

|

Asia Pacific |

Australia |

9.1% |

|

Middle East & Africa |

UAE |

18.7% |

|

Latin America |

Brazil |

53.8% |

North America EPC Engineering Procurement and Construction Market Insights

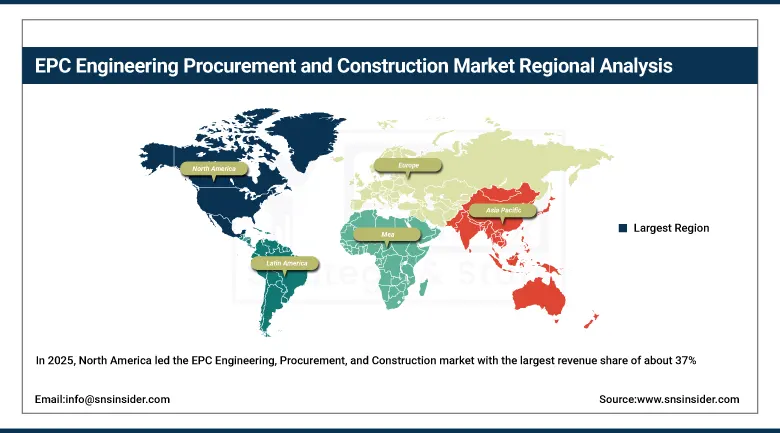

In 2025, North America led the EPC Engineering, Procurement, and Construction market with the largest revenue share of about 37%, owing to considerable investment into infrastructure development, energy shift initiatives, and industrial growth. North America enjoys advantages in terms of state-of-the-art engineering services, presence of reputed construction companies, and considerable government investment in transport, utilities, and renewable energy generation. Moreover, growing requirements of upgrading oil and gas installations coupled with rising trends in digital construction and sustainability will reinforce North America’s dominance in the international EPC market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe EPC Engineering Procurement and Construction Market Insights

The Europe EPC engineering procurement and construction market is primarily influenced by substantial investments in renewable energy, infrastructure modernization, and decarbonization initiatives in the industry. This region has seen considerable advancements in offshore wind power, hydrogen, and smart grid projects due to stringent environmental policies and zero-emission goals. Modernization of existing infrastructure and innovative construction techniques have added to the efficiency of these projects. Public funding and PPPs are contributing significantly to the growth of transport and energy projects within the region.

Asia Pacific EPC Engineering Procurement and Construction Market Insights

The Asia Pacific region is predicted to witness the highest growth at a CAGR of 7.31% between 2026 and 2035 in the EPC market. The reason behind the increasing demand is fast-paced urbanization, extensive infrastructure development, and investments in energy, transportation, and industrial sectors. Government initiatives toward building smart cities and use of renewable energy sources are supporting the growth rate in the region. Apart from that, growing FDI in the region along with the booming manufacturing sector and high population growth are propelling the growth of the EPC market in the region.

Middle East & Africa and Latin America EPC Engineering Procurement and Construction Market Insights

The Middle East and Africa as well as the Latin America EPC markets are growing owing to the increasing investments made in oil and gas production, mining activities, power plants, and the transport sector. The Middle East has been experiencing the effect of big projects and economic diversification policies. Similarly, in Africa, there are increased investments in energy production and industrialization. Latin America has received support from infrastructure developments and renewables.

Market Dynamics

Growth Drivers: Growing adoption of renewable energy projects accelerating demand for comprehensive engineering, procurement, and construction services worldwide

The increase in the trend of adopting renewable energy sources, such as solar power, wind power, and hydroelectric plants, is pushing up the demand for EPC services. There has been government promotion of clean energy infrastructure, favoring big projects that call for a combination of engineering, procurement, and construction processes. In addition, the increase in the amount of capital from both the private sector and joint ventures between the private and government sectors for the adoption of sustainable energy sources creates an even larger market.

China's Solar Expansion: In 2023, China installed 120 GWac of utility-scale photovoltaic (PV) capacity, marking a 275% increase from 2022, driven by lower module prices and enhanced construction of renewable energy infrastructure, including land approval and interconnection for utility-scale projects.

Cedar Creek Energy: Cedar Creek Energy specializes in solar energy projects, providing full-service EPC solutions, highlighting the importance of specialized EPC contractors in successful renewable energy system deployment.

Restraints: Fluctuating raw material costs and supply chain disruptions creating uncertainty in engineering, procurement, and construction projects worldwide

The fluctuating prices of steel, cement, and other construction materials are important factors in determining budgets, timelines, and profits in EPC projects. Problems within the international logistics chain as a result of geopolitical tension, logistical delays, or lack of raw materials may prove problematic when implementing EPC projects. Higher costs, the risk of fines, and the preservation of quality in the process are important issues that EPC companies need to consider. It is even harder due to currency fluctuations and import dependencies.

Opportunities: Technological advancements in digitalization, automation, and smart construction enabling more efficient and cost-effective EPC project delivery

The use of BIM, IoT, AI, and automation in construction engineering will increase efficiency, accuracy, and management of resources. The EPC companies will be able to enhance the processes of designing, sourcing, and scheduling to cut on costs and risks. Construction technologies will enable real-time monitoring, predictive maintenance, and enhanced safety management. Project management software will improve collaboration among the project partners to ensure proper implementation of the projects. The clients will have the need for technology-enabled approaches to handle their projects. There is an opportunity for the EPC companies to take advantage of large-scale projects by using technology.

Recent Developments:

-

September 30, 2025: L&T secured a $700 million Sustainability-Linked Trade Facility from Standard Chartered, aligning financing with sustainability goals. This strengthens its financial flexibility and reinforces its commitment to green infrastructure and long-term sustainable business practices.

-

April 2, 2025: Fluor executed an EPCM contract for a large pharmaceutical facility in Lebanon, Indiana, focused on manufacturing peptide-based drugs for Type 2 diabetes and weight management, expanding its footprint in advanced healthcare manufacturing infrastructure.

-

March 5, 2025: McDermott completed an EPCIC project in the Gulf of Mexico for Shell Offshore Inc., marking a key offshore oil production milestone and demonstrating strong execution capability in complex deepwater energy infrastructure projects.

-

November 15, 2024: Samsung Engineering secured a $215 million EPC contract for the Qatar RLP Ethylene Storage Plant, supporting petrochemical infrastructure development and strengthening its presence in large-scale industrial and energy sector projects.

-

September 15, 2024: SNC-Lavalin signed a $4 billion offshore EPC contract in Qatar focused on subsea services, reinforcing its position in large-scale offshore energy infrastructure and complex engineering project execution.

-

September 2, 2024: L&T expanded its renewable EPC vertical spun off from its power transmission and distribution segment, focusing on energy transition projects and strengthening its position in sustainable infrastructure development globally.

EPC Engineering Procurement and Construction Market Key Players are:

-

Bechtel Corporation

-

Fluor Corporation

-

TechnipFMC

-

SNC-Lavalin Group Inc.

-

McDermott International Ltd.

-

Samsung Engineering Co., Ltd.

-

Larsen & Toubro Limited (L&T)

-

Saipem S.p.A.

-

Petrofac Limited

-

Wood Group PLC

-

KBR Inc.

-

Hyundai Heavy Industries Co., Ltd.

-

Quanta Services, Inc.

-

John Wood Group PLC

-

Technip Energies

-

Sinopec Engineering (Group) Co., Ltd.

-

WorleyParsons Limited

-

Peiyang Chemical Engineering Service Corporation (PCCS)

-

Blattner Energy Inc.

-

Blue Ridge Power

EPC Engineering Procurement and Construction Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 897.62 Billion |

| Market Size by 2035 | USD 1571.47 Billion |

| CAGR | CAGR of 5.76% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Project Type (Greenfield Projects, Brownfield Projects) • By Industry (Oil and Gas, Chemicals, Power, Mining, Infrastructure) • By Service Type (Engineering, Procurement, Construction, Turnkey, Operations and Maintenance) • By Ownership Structure (Public, Private, Public-Private Partnership (PPP)) • By Contract Value ($1-10 million, $10-50 million, $50-100 million, Above $100 million) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Bechtel Corporation, Fluor Corporation, TechnipFMC, SNC-Lavalin Group Inc., McDermott International Ltd., Samsung Engineering Co., Ltd., Larsen & Toubro Limited (L&T), Saipem S.p.A., Petrofac Limited, Wood Group PLC, KBR Inc., Hyundai Heavy Industries Co., Ltd., Quanta Services, Inc., John Wood Group PLC, Technip Energies, Sinopec Engineering (Group) Co., Ltd., WorleyParsons Limited, Peiyang Chemical Engineering Service Corporation (PCCS), Blattner Energy Inc., Blue Ridge Power |

Frequently Asked Questions

North America dominated the EPC Engineering Procurement and Construction Market in 2025.

The private segment dominated the EPC Engineering Procurement and Construction Market in 2025.

Growing adoption of renewable energy projects accelerating demand for comprehensive engineering, procurement, and construction services worldwide.

The EPC Engineering Procurement and Construction Market was valued at USD 897.62 billion in 2025.

The EPC Engineering Procurement and Construction Market is expected to grow at a CAGR of 5.76% from 2026 to 2035.

Get in Touch