Epithelioma Treatment Market Report Scope & Overview:

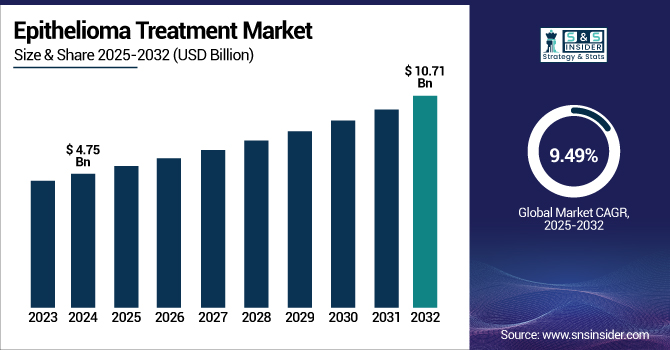

The Epithelioma Treatment Market size was valued at USD 4.75 billion in 2024 and is expected to reach USD 10.71 billion by 2032, growing at a CAGR of 9.49% over the forecast period of 2025-2032.

To Get more information on Epithelioma Treatment Market - Request Free Sample Report

The epithelioma treatment market is growing with a surge in the incidence of skin cancers, especially basal cell carcinoma (BCC) and squamous cell carcinoma (SCC) worldwide. The epithelioma treatment market growth is fueled by increasing cases of non-melanoma skin cancers (NMSCs) and basal and squamous cell carcinomas, attributed to increased UV radiation and an aging population. Government policies, public health campaigns, and increased investments in research to combat cancer have greatly increased early detection and favorable patient outcomes.

For instance, according to the American Cancer Society, “the U.S. is anticipated to have nearly 104,960 new cases of melanoma in 2025, which underlines the necessity to have effective therapies to combat melanoma.”

Regulatory agencies, such as the FDA have accelerated product approvals for new therapies, enabling patients to have faster access to innovative medicines and driving the growth of the market for epithelioma treatment. Governments, such as the NIH, with a 2.5 billion funding for research of skin cancer in 2024, and public awareness campaigns, such as the Surgeon General’s "Call to Action on Skin Cancer" in 2024, prioritize early diagnosis and new therapies, driving market growth.

Market Dynamics:

Drivers:

-

Increasing Incidence Skin Cancers Rate and rising UV Exposure Drive Epithelioma Treatment Demand

The growing incidence of skin cancers, especially basal cell carcinoma (BCC) and squamous cell carcinoma (SCC), is rapidly driving the need for epithelioma treatments globally. This development owes a lot to the increased exposure to ultraviolet (UV) radiation due to environmental factors, such as the depletion of the ozone layer and lifestyle shifts that promote outdoor activities and tanning.

For instance, occupational ultraviolet radiation increases the risk of non-melanoma skin cancer by 60%, impacting nearly 1.6 billion workers globally and causing thousands of deaths every year, says the World Health Organization and the International Labour Organization.

With skin cancer being one of the most prevalent malignancies, the sheer volume of cases reported and fueled by increased sun exposure and an aging population further highlights the situation, calling for efficient and innovative strategies in treating this disease. This epithelioma treatment market trend is reflected in the rising market value, with new cases reported every year in the millions, especially in areas with increased UV exposure, driving sustained growth in the treatment of epithelioma.

Restraints:

-

Complex Regulatory Approvals and Policy Variability Can Restrict Market Expansion

The variability and complexity of regulatory approval procedures in various regions greatly reduce the availability of new and potentially life-saving epithelioma therapies. Diverse and stringent regulatory requirements can lead to lengthy timelines for data submission, clinical trials, and approval of a product, postponing patients' access to advanced therapies. Companies have to navigate a patchwork of policies, reimbursement, and healthcare regulations, all of which complicate market entry and raise operational expenses. Inconsistent availability of treatment and coverage under insurance plans further limits patients' access, especially in less advanced healthcare infrastructures. Additionally, the availability of alternative therapies and limited overall awareness of early diagnosis account for late-stage presentation and poor results, further limiting the potential of the market to expand and innovate.

Market Segmentation:

By Type

Basal cell epithelioma segment held the leading market position and commanded a 60% share in 2024. Basal cell epithelioma (BCC) represents the leading type of non-melanoma skin cancer globally and accounts for approximately 80% of skin cancers in the U.S., according to the American Cancer Society. The reasons behind the common occurrence include factors, such as extensive UV radiation exposure, an aging population, and heightened awareness resulting in early diagnosis, further driving segment’s growth.

For instance, there are about 5.4 million basal and squamous cell skin cancers that occur each year in the U.S. and affect some 3.3 million people, with BCC accounting for the most.

BCC's slow growth and low rate of metastasis make it suitable for a spectrum of therapies, starting with surgical removal to targeted therapies, which further enhances its market dominance. Government initiatives have played a pivotal role in this trend. Healthcare professionals have been aided and guided by public health campaigns by the Skin Cancer Foundation and the American Academy of Dermatology to raise public awareness of the risks associated with UV rays and the need to have skin checked routinely.

For instance, the United Nations Conference on Environment and Development (UNCED) declared the INTERSUN program offers information, practical guidance, and sound scientific forecasts of the health effects and environmental impacts of UV and urges action by countries to decrease UV-related health hazards.

These have contributed to earlier diagnosis and treatment, with a consequent increase in patients accessing BCC care. The expedited approvals by the U.S. FDA have also made new drugs, such as vismodegib and sonidegib, designed to focus on advanced BCC, more accessible.

During the forecasted period, the squamous cell epithelioma (SCC) segment is anticipated to record the highest CAGR. The growth is fueled by a growing incidence, especially in aging and chronically sun-exposed patients or those with a history of immunosuppression. SCC prevalence increases due to better detection technologies, such as digital dermoscopy and teledermatology, allowing more accurate and earlier diagnosis.

By Drug Class

The hedgehog pathway inhibitors segment accounted for the highest revenue share of 42% in 2024. The Hedgehog pathway inhibitors, such as vismodegib and sonidegib are now the front-runner drug class in treating epithelioma, especially advanced and metastatic basal cell carcinoma. The drugs act specifically against the molecular pathways that cause tumor growth and provide a more efficient and less toxic alternative to standard chemotherapy and radiation.

The hedgehog signal pathway is essential to cell growth and cell differentiation. Defects in genes, such as PTCH1 or SMO can interfere with this pathway and are a significant contributing factor to basal cell carcinoma (BCC) market development.

Government data and regulatory actions have played an important role in this expansion. The FDA’s expedited approval of hedgehog pathway inhibitors has made it possible to rapidly provide patients with access to these therapies, and continued research funded by the government is investigating their wider uses. The National Cancer Institute and public agencies have sponsored clinical trials of the use of hedgehog inhibitors against both BCC and other cancers of the epithelial category, further establishing their utility in a clinical setting.

The immune checkpoint inhibitors segment is anticipated to have the highest growth rate during the projected period. The growth is driven by their immense influence over the treatment of cancers, increased approvals by regulatory bodies, and wider use in various cancers. Pembrolizumab (Keytruda) and nivolumab (Opdivo) are some of the drugs that have revolutionized the practice of oncology by blocking the action of PD-1 and PD-L1 proteins that enable the immune system to identify and destroy cancer cells more effectively.

By Distribution Channel

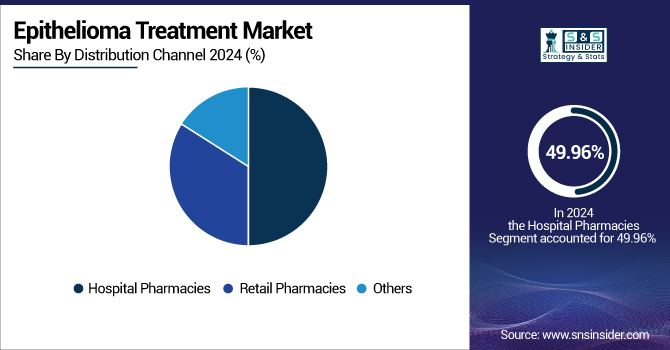

In 2024, hospital pharmacies held a 49.96% share with a 2.59 billion epithelioma treatment market size, representing their important role in the provision of sophisticated therapies, such as hedgehog pathway inhibitors and immune checkpoint inhibitors. Hospital pharmacies are capable of managing specialized storage, preparation, and administration procedures that are necessary to ensure the effective and safe use of these drugs. A steadily increasing level of hospitalizations due to BCC and SCC, fueled by augmented screening and early detection programs, is indicated by government data.

For instance, the survey of the American Academy of Dermatology indicates, more and more people in the U.S. are at risk of skin cancer and that over 1 in every 3 adults received a sunburn in 2024.

Hospitals also act as referral centers for complicated cases enabling patients to have access to multidisciplinary teams of specialists and the most recent therapeutic technologies.

The others (specialty pharmacies, online pharmacies, and lab and diagnostics services providers) segment is expected to register the highest CAGR of 10.43% during the forecasted period. The increased development of online health platforms and telemedicine has enabled patients to seek medications remotely, predominantly in underserved or rural regions. Specialty pharmacies are especially skilled at managing intricate therapies, educating patients, and coordinating treatment with many providers.

Government programs to extend telehealth services and make healthcare more accessible have fueled this shift. For instance, the U.S. Department of Health and Human Services has made investments in digital infrastructures to enable remote consultation and electronic prescribing, allowing patients to easily access the care that they require.

Regional Analysis:

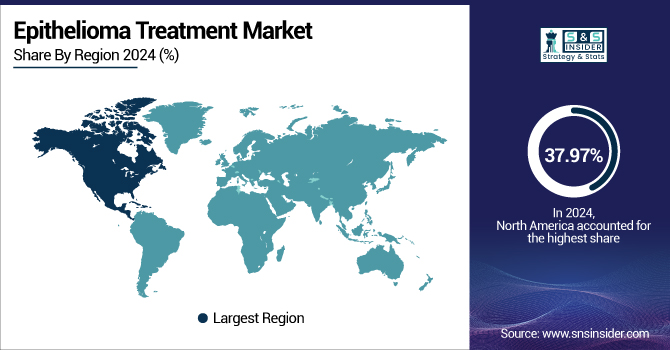

In 2024, North America led with 37.97% of the global share. The U.S. epithelioma treatment market was valued at USD 1.68 billion in 2024 and is expected to grow to USD 3.42 billion, growing at a CAGR of about 9.33% from 2025-2032 due to a high prevalence of skin cancers, sophisticated healthcare infrastructure, and a firm regulatory framework that favors the adoption of new therapies at a faster rate.

For instance, according to the American Academy of Dermatology, there were projected to be approximately 200,340 new cases of melanoma diagnosed in the U.S. in 2024, in addition to millions of BCC and SCC cases. Over the past 15 years, the rate at which new invasive melanomas were diagnosed rose by 46%.

The prevalence of non-melanoma skin cancers is especially elevated with the pervasive UV exposure and aging population that exists, leading to persistent demand for effective therapies.

The Asia Pacific region, and notably countries such as China, India, and Japan, is anticipated to witness the highest CAGR over the projected period. The cause of this growth is foreseen to be enhanced awareness, better healthcare accessibility, and rising investments in cancer care. The healthcare systems in such economies are introducing large-scale screening and increasing coverage under health insurance policies to provide more people with better access to advanced therapies.

For instance, in China, malignant melanoma ranks among the cancers that are most regularly diagnosed, and its incidence is increasing by 3%–5% every year. although the overall incidence is still relatively low, it is rising rapidly, with approximately 20,000 new cases annually. Mortality rates are also on the rise in the country.

The European region is expanding with a substantial growth rate in the epithelioma treatment market, fueled by a large incidence of skin cancers, a sound healthcare structure, and considerable investments in research and development. Germany, the U.K., and France are leading the pack, with Germany itself recording more than 300,000 new skin cancer cases each year, driving the skin cancer treatment market, backed by firm governmental support for research and advanced healthcare practices. The region is backed by a dynamic regulatory framework, and the European Medicines Agency (EMA) has approved new medications such as pembrolizumab and nivolumab for advanced skin cancers, with additional improvement to treatment and patient results.

The Latin America, Middle East, and Africa (LAMEA) epithelioma treatment market is witnessing steady growth in the market for treating epithelioma. Growth is fueled by the rising prevalence of cancer rising awareness, and a gradually improving healthcare infrastructure. Challenges confronting the market include healthcare disparities, the cost of treating patients, and regulatory lags that prevent the adoption of sophisticated therapies at a wider level. Despite this, initiatives by the public sector and investments in the area of caring for patients with cancer are filling some of the gaps, particularly in major urban centers.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players:

The key players operating in the market are Amgen, Regeneron Pharmaceuticals, AstraZeneca, Johnson & Johnson, BeiGene, Merck and Co., Pfizer, Bristol-Myers Squibb, F. Hoffmann-La Roche, Novartis, Sanofi, and Sun Pharmaceutical Industries.

Recent Developments:

-

In April 2025, Amgen announced that the U.S. Food and Drug Administration (FDA) had approved UPLIZNA as the first and only treatment for adults with Immunoglobulin G4-related disease (IgG4-RD).

-

KEYTRUDA, in combination with pemetrexed and platinum chemotherapy, was given FDA approval as a first-line treatment for unresectable advanced or metastatic malignant pleural mesothelioma in September 2024. Improved survival outcomes from clinical trials have provided the basis for this approval and thus introduced a new standard of care for an entity that had a notorious reputation for poor prognosis.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.92 Billion |

| Market Size by 2032 | USD 10.7 Billion |

| CAGR | CAGR of 9.49% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Squamous Cell Epithelioma, Basal Cell Epithelioma, Others) • By Drug Class (Hedgehog Pathway Inhibitors, Chemotherapeutic Agents, Immune Checkpoint Inhibitors, Others) • By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Amgen, Regeneron Pharmaceuticals, AstraZeneca, Johnson & Johnson, BeiGene, Merck and Co., Pfizer, Bristol-Myers Squibb, F. Hoffmann-La Roche, Novartis, Sanofi, Sun Pharmaceutical Industries |

Frequently Asked Questions

The Hospital Pharmacies segment dominated the Epithelioma Treatment Market.

Complex regulatory approvals, policy variability & slow introduction of new treatments and limit market expansion.

The CAGR of the Epithelioma Treatment Market is 9.49% during the forecast period of 2025-2032.

The North America region dominated the Epithelioma Treatment Market in 2024.

The projected market size for the Epithelioma Treatment Market is USD 10.7 billion by 2032.

Get in Touch