Fluorochemicals Market Report Scope & Overview:

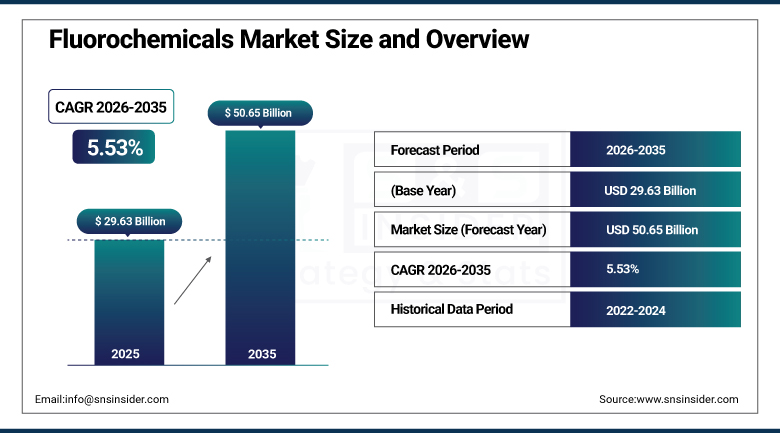

The Fluorochemicals Market was valued at USD 29.63 billion in 2025 and is expected to reach USD 50.65 billion by 2035, growing at a CAGR of 5.53% from 2026–2035.

The fluorochemicals market is witnessing steady growth in the global market owing to the increasing demand for refrigerants, fluoropolymers, and specialty fluorinated materials worldwide. The growing need for high-performance materials across industrial applications is promoting the usage of fluorochemicals in various sectors. Investments made by organizations in electric vehicles, semiconductor manufacturing, and sustainable cooling technologies are contributing to market growth. Increasing developments in advanced electronics and energy-efficient systems are playing a major role in driving the demand for fluorochemicals. Growth in chemical manufacturing activities and stringent environmental regulations are fueling the demand for fluorochemicals.

As stated by the International Energy Agency and the UN Environmental Programme, the global demand for fluorochemicals is significantly associated with energy transition technology. Over 17 million units of electric vehicles have been sold worldwide in 2024, while the installation of heat pumps is growing as nations strive towards achieving their decarbonization objectives. Moreover, signatories of the Kigali Amendment are reducing hydrofluorocarbons on a phased basis with a goal of cutting down usage by 80-85 percent over the next few decades.

Market Size and Forecast:

-

Market Size 2026E: USD 31.21 billion

-

Market Size 2035: USD 50.65 billion

-

CAGR (2026 - 2035): 5.53%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Fluorochemicals Market- Request Free Sample Report

Fluorochemicals Market Trends:

-

Regulatory PFAS restrictions across Europe and North America are accelerating investments in compliant fluoropolymer reformulations and traceability systems.

-

HFO refrigerant adoption is expanding as low-GWP cooling mandates reshape automotive, commercial refrigeration, and heat pump demand.

-

Semiconductor and EV battery supply chains are increasing fluoropolymer consumption for high-purity insulation and processing applications.

-

Producers are expanding Asia-Pacific manufacturing footprints to diversify supply chains and reduce geopolitical sourcing risks.

-

Global PFAS compliance spending is rising as over 5,600 stakeholder comments reshape European restriction frameworks.

-

Sustainable fluorochemical innovation is prioritizing circular recovery technologies, emission reduction, and waste minimization across production assets.

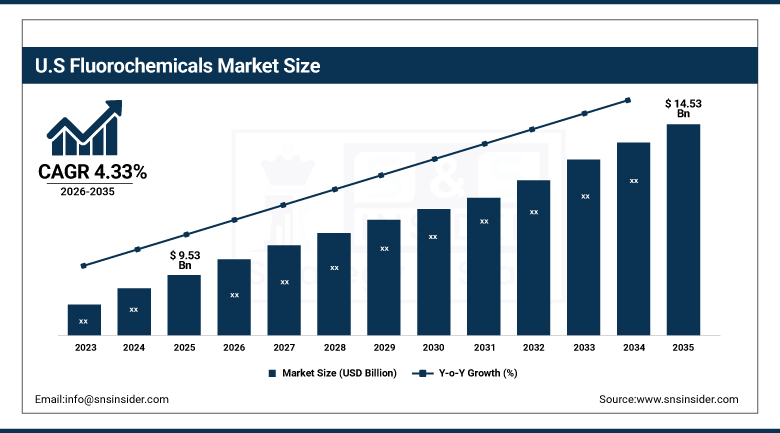

U.S. Fluorochemicals Market Size Outlook.

The U.S. Fluorochemicals Market was valued at USD 9.53 billion in 2025 and is expected to reach around USD 14.53 billion by 2035, growing at a CAGR of 4.33% from 2026–2035.

The U.S. fluorochemicals market is growing consistently owing to increased demand in refrigeration, semiconductor manufacturing, and advanced industrial applications. The usage of fluorochemicals in fluoropolymers, specialty coatings, and high-performance materials has contributed to market growth in a consistent manner. Increased spending in the development of energy-efficient cooling systems has generated an increase in demand for advanced fluorinated materials. Development of chemical production facilities, electric vehicle manufacturing, and electronics industries is further driving the demand for this product.

The U.S. Environmental Protection Agency, together with the U.S. Energy Information Administration, indicate that the demand for fluorochemicals in the United States is determined by the policy changes regarding the shift from using refrigerants and the process of electrification. Thus, the AIM Act aims at the phased reduction in hydrofluorocarbon use of 85% until 2036 relative to the baseline year. Moreover, electric vehicles sales are estimated at around 1.3 million units in 2024.

Fluorochemicals Market Segment Analysis:

-

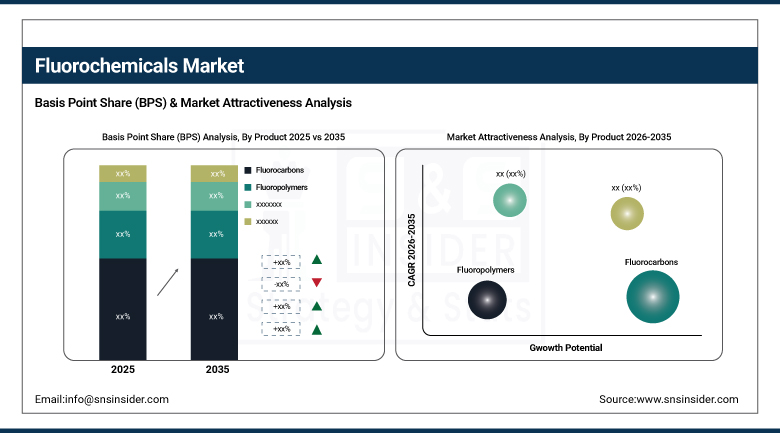

By Product, fluorocarbons dominated the fluorochemicals market with 53.20% share in 2025; while fluoropolymers are the fastest growing segment with CAGR of 7.78% during 2026 to 2035.

-

By Application, refrigeration dominated the fluorochemicals market with 42.60% share in 2025; while automobile is the fastest growing segment with CAGR of 10.58% during 2026 to 2035.

-

By End-User, chemical industry dominated the fluorochemicals market with 31.80% share in 2025; while electrical & electronics is the fastest growing segment with CAGR of 10.06% during 2026 to 2035.

By Product, fluorocarbons dominated the fluorochemicals market, while fluoropolymers are the fastest growing segment.

The fluorochemicals segment dominated the share of revenue in the global fluorochemicals market in 2025 due to their widespread use in cooling equipment like refrigerators, air conditioners, and industrial coolants across the globe. There has been a surge in demand due to applications in commercial constructions, cold chain logistics, and food storage segments, which led to the growth of this market. Continued replacement of existing cooling technologies and increase in demand for energy-efficient refrigerants will drive the use of these chemicals.

The fluoropolymers segment is projected to register the fastest growth during the forecast period from 2026-2035 due to increasing demand from electric vehicles, semiconductors, and electronics manufacturing sectors across the world. Growing demand from battery parts, insulators, and high-performance coatings is driving market growth. Demand from renewable energy infrastructure and future industrial applications will also boost demand for these materials.

By Application, refrigeration dominated the fluorochemicals market, while automobile is the fastest growing segment.

Refrigeration emerged as the key contributor to revenues, contributing the dominated share to the fluorochemicals market in 2025. The segment benefitted significantly from the high level of demand for refrigerants in the cooling systems in residential and commercial and industrial buildings. Improved infrastructure for cold chains and HVAC helped drive the sustained usage of fluorochemicals through end users around the world. Energy conservation standards also promoted the uptake of advanced refrigerant solutions in various applications.

Automobile segment is forecasted to register the fastest CAGR between 2026-2035 owing to rapid electrification of vehicles. High levels of production of electric vehicles require the use of fluoropolymers and thermally stable materials for batteries in vehicles. Manufacturers are making increased investment in the production of lightweight and energy efficient systems for battery cooling in automobiles. Governments are offering incentives to accelerate the use of fluorochemicals in automobiles.

By End-User, chemical industry dominated the fluorochemicals market, while electrical & electronics is the fastest growing segment.

Chemical industry segment accounted for the dominated revenue share in the fluorochemicals market in 2025 owing to their extensive use as raw materials, intermediates, and process chemicals. The growing demand for refrigerants, fluoropolymers, and chemicals from various industries will support the growth of the segment. Investments made by industries for the production of specialty chemicals will boost the consumption in the future as well.

The electrical and electronics segment is expected to register the fastest CAGR during the forecast period owing to the rising manufacture of semiconductors and electronic equipment worldwide. Increasing investments in data centers, electric vehicles, and energy storage will fuel the usage of fluorochemicals. Demand for pure fluoride products, insulating components, and specialty gases will also accelerate the growth rate.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

87.40% |

|

Europe |

Germany |

24.80% |

|

Asia Pacific |

China |

42.30% |

|

Middle East & Africa |

UAE |

17.20% |

|

Latin America |

Brazil |

46.10% |

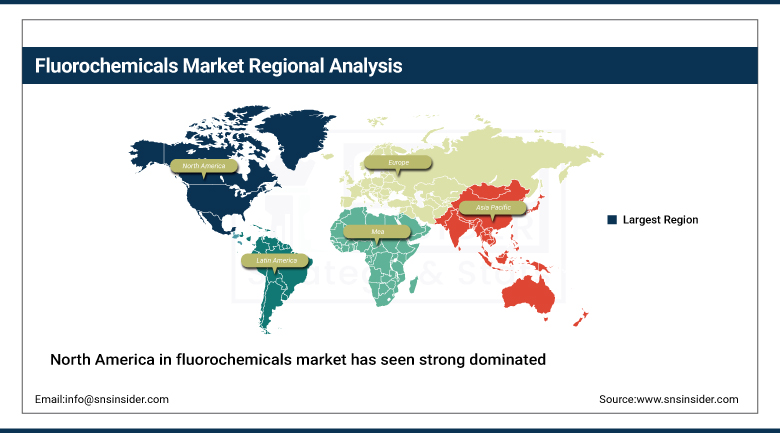

North America Fluorochemicals Market Insights.

North America in fluorochemicals market has seen strong dominance with a market share of about 36.80% in 2025 due to advanced chemical manufacturing and industrial infrastructure. The region benefits from strong refrigeration demand, semiconductor production, and aerospace applications. Increasing demand for high performance materials, refrigerants, and specialty fluorochemicals is driving market expansion across the United States and Canada. Rising adoption in electronics and EV related applications is further supporting market leadership. Strict environmental regulations are strengthening controlled fluorochemical usage.

According to the U.S. Environmental Protection Agency and Kigali Amendment under Montreal Protocol, fluorochemicals regulations in North America are driven by an 85% phasedown of hydrofluorocarbons mandated under the U.S. AIM Act by 2036, using a 2011–2013 baseline. Canada has adopted Kigali-aligned regulations targeting an 85% HFC reduction over the same timeframe. These policy-driven reductions directly influence refrigerant demand, semiconductor manufacturing inputs, and industrial fluoropolymer usage across region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Fluorochemicals Market Insights.

The Europe fluorochemicals market shows strong presence in 2025 due to strict environmental regulations and sustainability initiatives. Countries like Germany, France, United Kingdom, and Italy are key contributors to demand. High focus on refrigerants, fluoropolymers, and industrial chemical applications is supporting steady market growth across the region. Increasing adoption in automotive, electronics, and construction applications is further strengthening consumption. Expanding regulatory frameworks for low emission technologies is driving adoption across industries.

According to the European Environment Agency, fluorinated gases account for about 2.5% of total EU greenhouse gas emissions. The EU enforces a phasedown of hydrofluorocarbons targeting a 79% reduction by 2030 compared with 2015 baseline levels. Under the Kigali Amendment framework, participating countries commit to an 80–85% global HFC reduction trajectory, driving structural demand shifts in fluorochemicals across refrigeration, insulation, and industrial applications in Europe as stated by UNEP.

Asia Pacific Fluorochemicals Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the fluorochemicals market during the forecast period with a market share of about 6.62% in 2025. Rapid industrialization and manufacturing expansion are driving strong demand across China, India, Japan, South Korea, and Southeast Asia. Expanding electronics production, EV manufacturing, and chemical industries are significantly boosting adoption. Rising demand for refrigerants and fluoropolymers is further accelerating market growth. Large scale industrial development supports strong regional demand outlook.

According to the United Nations Environment Programme Ozone Secretariat, parties to the Montreal Protocol have achieved over 99% phase-out of controlled ozone-depleting substances globally, with Asia Pacific countries implementing accelerated HFC phasedown schedules under the Kigali Amendment.

According to IEA tracking, Asia accounts for more than 50% of global cooling demand growth, driven by rising temperatures and urbanization, while electric vehicle adoption surpassed 17 million units globally in 2024, reinforcing demand for fluorochemical-based refrigerants, electrolytes, and semiconductor-grade materials.

Middle East & Africa and Latin America Fluorochemicals Market Insights.

The Middle East & Africa region along with Latin America is witnessing steady growth in the fluorochemicals market due to rising industrial development. Countries like UAE, Saudi Arabia, South Africa, Brazil, and Mexico are emerging as key demand centers. Increasing investments in refrigeration systems, construction activities, and industrial processing are supporting market expansion. Growing need for energy efficient cooling and specialty chemicals is further boosting product adoption. Rising industrialization strengthens long term demand outlook.

According to the United Nations Environment Programme and the Montreal Protocol Kigali Amendment framework, over 150 countries are committed to phased reduction of hydrofluorocarbons by 80–85% by mid-century. The World Bank reports that cooling demand in developing regions, including Africa and Latin America, is expected to increase significantly as urban populations rise above 80% in Latin America and 43% in Africa. Additionally, International Energy Agency data indicates global air conditioning stock could triple by 2050, driving fluorochemical refrigerant adoption across MEA and Latin America regions.

Market Dynamics:

Growth Drivers: Expanding applications in electronics, semiconductors, and electric vehicles manufacturing industries worldwide rapidly

The quick development in the electronics, semiconductor production, and EV manufacturing industry is majorly responsible for the growing demand for Fluorochemicals. There are a lot of applications of fluoropolymers and specialty gases in the production of chips, insulators, and components of high performance. Growing application of batteries and modern automotive parts is also adding to the demand for materials. Increased use of electronics and digitalization will lead to greater use of fluorine compounds. The increase in investment in clean energy and manufacturing technologies will add to the demand.

According to IEA Global EV Outlook 2024, electric cars accounted for about 14% of global car sales in 2023, with China exceeding 60% of EV sales. As per UNCTAD, information and communication technology goods represent around 14% of global merchandise exports. These measurable adoption indicators in EV and electronics manufacturing reflect rapid industrial expansion, increasing demand for high-performance fluorochemical materials used in semiconductors, batteries, and advanced electronics production.

Restraints: Strict environmental regulations and phase down policies impacting fluorinated compound usage globally

Stricter regulatory laws for greenhouse gases and depletion of the ozone layer are hindering the development of Fluorochemicals. Phase down regulations on high global warming potential refrigerants are being enforced in most parts of the world. Increased costs of complying with these laws have affected production and use of some fluorinated compounds. Industry is compelled to focus on products that emit less into the environment. Such restrictions have affected demand stability over time. A lot of money has been allocated to research in line with changing environmental regulations worldwide.

Opportunities: Rapid growth in electric vehicles and renewable energy industries creating strong demand potential globally

Growth of electric vehicles manufacturing and development of renewable energy sources has brought a lot of opportunities to develop the market of Fluorochemicals. Fluoropolymers are used in batteries, insulations of wires, and various automotive parts. Growing use of solar energy systems and wind energy installations has led to increased demand for chemicals that are resistant to adverse environmental factors. Development of energy storage systems contributes to growing usage of fluorine-containing chemicals. Growing emphasis on lightweight, heat-resistant, and chemically stable materials accelerates their development prospects in the long run.

According to the International Energy Agency Global EV Outlook 2024 and IRENA Renewable Capacity Statistics 2024, electric vehicle sales surpassed 14 million units in 2023, accounting for about 18% of global car sales. IRENA reports renewable energy added around 473 GW of capacity in 2023, with renewables representing approximately 86% of total global capacity additions. These measurable shifts in electrification and clean energy deployment indicate rising industrial demand for fluorochemicals in batteries, refrigerants, and energy systems.

Recent Developments:

-

2026: Arkema expands PVDF capacity in China by 20% to support lithium-ion battery, semiconductor, and energy storage application demand growth.

-

2025: The Chemours Company advances circular economy initiatives, refrigerant portfolio optimization, and manufacturing efficiency improvements supporting global fluorochemical demand stability.

-

2025: Honeywell International Inc. expands Quantinuum quantum computing ecosystem, building automation platforms, and low-global-warming refrigerant solutions globally deployment initiatives.

-

2024: Daikin Industries, Ltd. invests in HVAC manufacturing expansion, refrigerant innovation, and energy-efficient cooling systems for residential commercial markets.

Fluorochemicals Market Key Players are:

-

The Chemours Company

-

Honeywell International Inc.

-

Daikin Industries, Ltd.

-

Arkema S.A.

-

Solvay S.A.

-

AGC Inc.

-

Dongyue Group Limited

-

Orbia Advance Corporation, S.A.B. de C.V.

-

Gujarat Fluorochemicals Limited

-

Navin Fluorine International Limited

-

SRF Limited

-

3M Company

-

Sinochem Holdings Corporation Ltd.

-

Zhejiang Juhua Co., Ltd.

-

Shandong Hualu-Hengsheng Chemical Co., Ltd.

-

Kureha Corporation

-

The Mitsubishi Chemical Group

-

Linde plc

-

BASF SE

-

Merck KGaA

Fluorochemicals Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 29.63 Billion |

| Market Size by 2035 | USD 50.65 Billion |

| CAGR | CAGR of 5.53% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Fluorocarbons, Fluoropolymers, Inorganics & Specialties Chemicals and Materials) • By Application (Refrigeration, Aluminum, Automobile, Films, Tubings, Blowing Agents, Others) • By End-User (Chemical Industry, Automotive & Transportation, Electrical & Electronics, Healthcare & Pharmaceuticals, Building & Construction, Aerospace & Defense, Packaging, Food & Beverage, Agriculture, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | The Chemours Company, Honeywell International Inc., Daikin Industries, Ltd., Arkema S.A., Solvay S.A., AGC Inc., Dongyue Group Limited, Orbia Advance Corporation, S.A.B. de C.V., Gujarat Fluorochemicals Limited, Navin Fluorine International Limited, SRF Limited, 3M Company, Sinochem Holdings Corporation Ltd., Zhejiang Juhua Co., Ltd., Shandong Hualu-Hengsheng Chemical Co., Ltd., Kureha Corporation, The Mitsubishi Chemical Group, Linde plc, BASF SE, Merck KGaA |

Frequently Asked Questions

The fluorochemicals market is expected to grow at a CAGR of 5.53% from 2026 to 2035.

The fluorochemicals market was valued at USD 29.63 billion in 2025.

Expanding demand from refrigeration, semiconductors, electric vehicles, and high-performance industrial materials is driving global fluorochemicals demand.

The fluorocarbons segment dominated the market in 2025 due to extensive use in refrigeration, cooling systems, and industrial refrigerants.

North America dominated the fluorochemicals market due to strong industrial infrastructure, high refrigerant demand, and advanced chemical manufacturing capabilities.

Get in Touch