Frozen Snacks Market Report Scope & Overview:

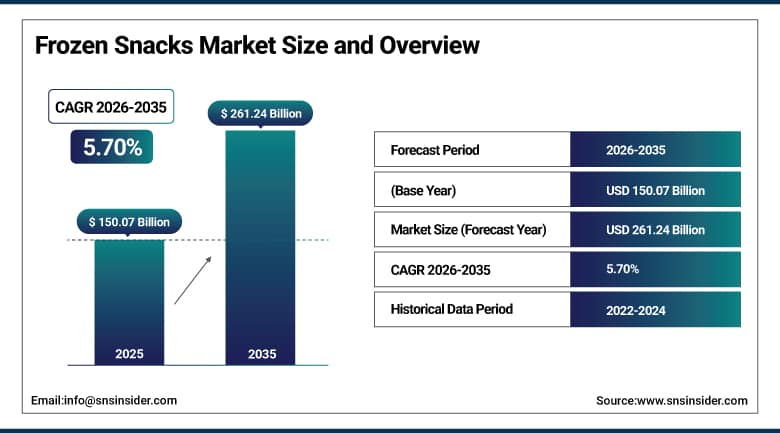

The Frozen Snacks Market was valued at USD 150.07 Billion in 2025 and is expected to reach USD 261.24 Billion by 2035, growing at a CAGR of 5.70% from 2026–2035.

The frozen snacks market has experienced a phase of consistent transformation driven by changes in consumer lifestyles, investments in retail structure, and innovations in the products within both developed and developing countries during the last few years. While the category started as one focused on convenience, it has now evolved to become a diverse industry offering various kinds of snacks for consumption at home and away-from-home occasions, as well as for food service and institutions. These products include vegetarian snacks, bakery products, seafood, meat, and dairy, among others.

General Mills launched its Nature Valley Frozen Protein Bars in October 2025, bringing a high-protein convenience format into frozen retail and validating the category’s expansion into functional snacking. Conagra Brands unveiled over 50 new frozen food products in June 2025, including plant-based and gluten-free formats, reinforcing how aggressively major producers are pursuing product diversification to capture incremental demand.

Market Size and Forecast

-

Market Size in 2026E: USD 158.62 Billion

-

Market Size by 2035: USD 261.24 Billion

-

CAGR: 5.70% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Frozen Snacks Market - Request Free Sample Report

Frozen Snacks Market Trends

-

Consumer preference for air fryer compatible frozen snacks is growing steadily across North American and European markets, with major producers redesigning product formats and packaging to address this shift in home cooking equipment ownership.

-

The rise of clean label and reduced additive formulations is reshaping product development across frozen vegetables, bakery snacks, and protein-based frozen formats as health-conscious households scrutinize ingredient lists more carefully.

-

Online grocery and quick commerce platforms with cold chain capability are opening new distribution channels for frozen snack brands, particularly in urban markets across China, India, and Southeast Asia.

-

Plant-based frozen snack formats including meat alternatives, dairy-free options, and vegetable-forward finger foods are gaining shelf space in mainstream retail channels as producers respond to shifting dietary preferences across major markets.

-

Foodservice operators including restaurant chains, institutional caterers, and quick service restaurants are increasing their reliance on frozen snack inputs to manage labour costs, reduce kitchen preparation time, and maintain consistent product quality across multiple locations.

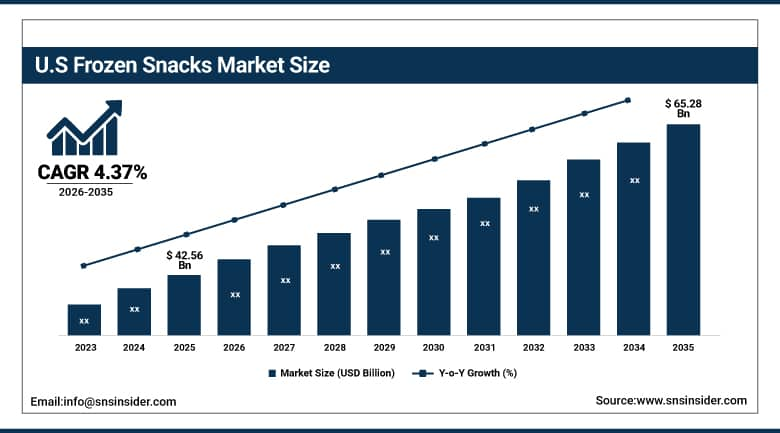

The U.S. Frozen Snacks Market Outlook

The U.S. Frozen Snacks Market was valued at approximately USD 42.56 Billion in 2025 and is expected to reach approximately USD 65.28 Billion by 2035, growing at a CAGR of 4.37%.

The US stands out as the largest national market for frozen snacks in the world, owing to the presence of widespread use of freezers in households, organized sections of frozen foods in retail outlets, and the prevalent food culture that has traditionally favored meals in the form of ready-to-eat snacks. Consumption of frozen snacks across demographics within the US includes singles living alone in urban areas seeking meal solutions in the form of quick bites, as well as large families where frozen veggies and snacks are incorporated into the routine meal planning week by week. The American market is seeing considerable product premiumization along with the growth of volume in mainstream products. Consumers have shown their readiness to pay premium prices for snacks based on wholesome ingredients, lower sodium content, and clean labels.

Frozen Snacks Market Segment Analysis

-

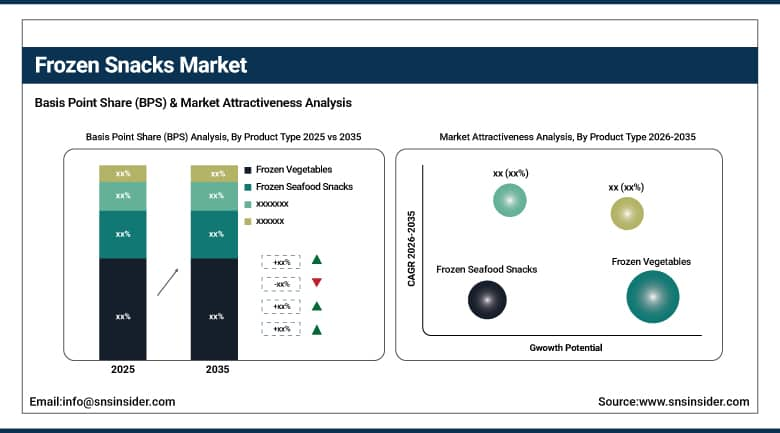

By Product Type, Frozen Vegetables held the largest share of approximately 32.45% in 2025; Frozen Seafood Snacks is expected to register the fastest CAGR of 7.12% during 2026–2035.

-

By Category, Ready-to-Cook dominated the market with approximately 58.63% share in 2025; Ready-to-Eat is projected to grow at the fastest CAGR of 6.45% through the forecast period.

-

By End User, Households accounted for the highest market share of approximately 67.28% in 2025; Foodservice is expected to register the fastest CAGR of 6.88% during 2026–2035.

-

By Distribution Channel, Supermarkets & Hypermarkets held the leading share of approximately 52.91% in 2025; Online Retail is projected to grow at the highest CAGR of 7.22% through 2035.

By Product Type, frozen vegetables dominate, frozen seafood snacks grow fastest

Frozen Vegetables continued their hold as the dominating product type category, commanding around 32.45% of the total share in the market of frozen snacks in 2025. The position held by this segment stems from the widespread use of frozen vegetables in everyday meals in North American and European households. Frozen vegetables are seen as the most economical, cost-free, and nutrient-filled alternative for consumers looking for a cheaper substitute to fresh vegetables.

Frozen Seafood Snacks emerged as the fastest growing product type with a CAGR of 7.12% over the period up to 2035. This indicates that seafood consumption among health-conscious individuals is gradually increasing and that the demand for seafood products has been gaining traction both in Western and Asian countries. This can be attributed to the preference towards seafood due to its being a source of lean protein.

By Category, ready-to-cook dominates, ready-to-eat grows fastest

The category which held the highest market share position at a value of 58.63% was Ready-to-Cook. This was due to the prevailing consumer preference towards frozen snacks that would require some form of preparation from the consumers prior to their consumption. The attractiveness of the category lies in the provision of a freshly prepared snack from its frozen state, whereby consumers enjoy the taste, texture, and aroma derived from cooking frozen snacks using traditional heating appliances.

Ready-to-Eat was the fastest-growing category among all categories in terms of the CAGR of 6.45% up to 2035. The increase in the time available for food preparation is becoming scarce for urban consumers from developed as well as fast-developing economies, resulting in higher opportunity costs of time. Frozen snacks that could be eaten immediately without requiring any preparation or only some time for warming or thawing are ideal for single-person consumers, commuters, and workplace consumption occasions.

By End User, households dominate, foodservice grows fastest

Household emerged as the largest market segment accounting for 67.28% of the total frozen snacks industry in 2025, thus, validating its status as the key driving force in terms of demand for frozen snacks among manufacturers and distributors. This is a reflection of the high penetration of domestic refrigerators/freezers in advanced market economies where frozen snacks have become a pantry staple for meals. Growth in double-income households in the North American region, Europe, and Asia Pacific markets is driving demand from consumers who have increasingly less time to prepare meals.

The Foodservice segment has been forecasted to be the most dynamic and fastest growing market over the period 2026-2035, exhibiting a Compound Annual Growth Rate (CAGR) of 6.88%. This segment shows the commercial partnership that exists between frozen snack providers and the Foodservice sector. The need for affordable and quality products by restaurant and institution caterers, airlines, and quick service restaurants is driving demand from foodservice operators for frozen snacks which serve as an alternative to freshly made products.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

78.72% |

|

Europe |

Germany |

22.15% |

|

Asia Pacific |

China |

31.40% |

|

Middle East & Africa |

UAE |

28.70% |

|

Latin America |

Brazil |

35.60% |

North America Frozen Snacks Market Insights

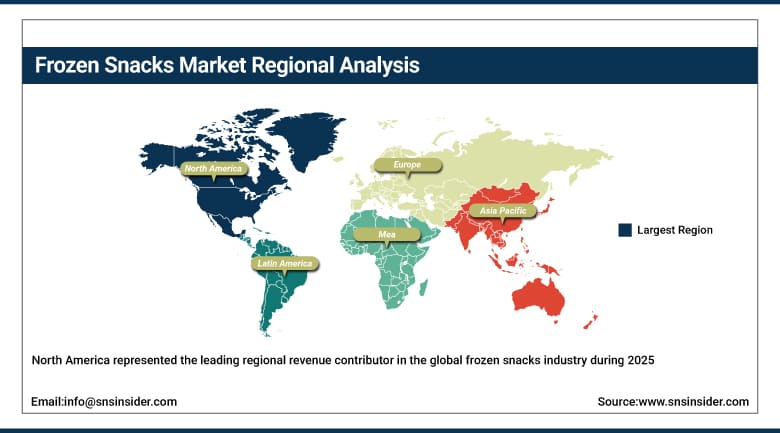

North America represented the leading regional revenue contributor in the global frozen snacks industry during 2025, contributing around 38.72% to total revenue generated globally. In North America, the U.S. represents the major national market, driven by the region’s advanced infrastructure related to household freezer penetration, retail frozen foods, and consumption culture based on convenience. Demand from consumers in North America is for the entire range of frozen snack products, from vegetable side dishes and snacks made from potatoes to premium seafood options and plant-based varieties. Conagra Brands, General Mills, Tyson Foods, and McCain Foods are some of the key producers of frozen snacks with considerable commercial presence in the North American market. Canada provides a commercially significant contribution to the total North American revenue, with a developed retail grocery infrastructure and a consumer culture similar to that in the U.S. in frozen snack consumption.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Frozen Snacks Market Insights

Europe constitutes an established and commercialized frozen snacks market, fueled by extensive retail chain distribution in western Europe and increasing consumption in eastern Europe with the growth in consumer discretionary incomes driving supermarket development. Among the national markets of the region, Germany, the UK, France, and Italy are the largest in terms of revenue contributions. All four have established frozen aisles distribution in large grocery formats and convenience grocers. Germany comprises about 22.15% of the total frozen snack sales in Europe, owing to the size of its economy as the largest food retailing one in the EU, as well as the pragmatic outlook of its consumers on cost-effective food products. Europe is experiencing significant premiumization trends, as seen from investment in clean ingredients, additives reduction, and packaging sustainability made by regional companies such as Nomad Foods and Dr. Oetker.

Asia Pacific Frozen Snacks Market Insights

Asia Pacific is the fastest-growing frozen snacks market on a regional basis, having grown at a CAGR of roughly 7.02% through to 2035. The major players driving demand within the region are China, India, Japan, and South Korea at various stages of frozen snack product category evolution. Japan has some of the world’s most advanced frozen food cultures and a robust production industry coupled with extensive retail infrastructure and a fully normalised consumer population enjoying frozen snack products across a diverse array of meals. China stands out in the region in terms of largest absolute growth opportunity, owing to rising urban middle-class demand for convenience snacks, supported by substantial cold chain investments from domestic and foreign retailers. China makes up around 31.40% of the regional revenues for the Asia Pacific in 2025 and is bolstered by domestic regional companies such as Ajinomoto and others.

MEA & Latin America Frozen Snacks Market Insights

The Middle East and Africa and Latin America are emerging markets for frozen snack products due to factors like increasing urbanization, improved cold chain infrastructure, and increasing modern retail penetration that are making business environments in these regions ripe for investment in the frozen snacks category by both domestic players and foreign firms. In the MEA region, the UAE generates the highest revenue contribution within the frozen snack category with an estimated market share of 28.70%, owing to the advanced nature of retailing in the emirate and the expatriate population that is familiar with the consumption of frozen snacks from their native regions. The South African market remains the most commercially matured emerging market in MEA for frozen snack products.

Market Dynamics

Growth Drivers: Rising convenience food demand and expanding cold chain retail infrastructure driving category growth

The fundamental commercial driver of frozen snacks market growth is the expanding global demand for convenient, ready-to-prepare food formats among consumers whose daily time budgets for meal preparation are shrinking. Urban population growth across Asia Pacific, Latin America, and the Middle East is expanding the size of the consumer demographic that relies on convenient food formats as a practical solution to busy lifestyles. The growing prevalence of dual-income households and single-occupant urban living arrangements in North America and Europe is sustaining demand in the world’s two largest established markets while the structural conditions for category growth in emerging economies are improving in parallel. Cold chain infrastructure investment by modern retail operators is directly enabling frozen snack category growth by extending commercial reach into markets and consumer segments that were previously inaccessible.

Restraints: Cold chain infrastructure gaps and private label competition limiting growth

Cold chain infrastructure gaps in developing markets represent a genuine commercial constraint on frozen snacks market growth in Asia Pacific, Latin America, and Africa. Reliable electricity supply for retail cold storage, investment in temperature-controlled distribution fleets, and last-mile delivery capability are all prerequisites for commercially viable frozen snack distribution in markets where this infrastructure remains underdeveloped. The capital requirements for cold chain build-out are significant, and the pace of infrastructure improvement varies considerably across individual markets and regions within countries. Private label frozen snack growth in major Western European and North American retail chains is creating pricing pressure for branded producers.

Opportunities: Product innovation and foodservice channel expansion offering significant growth potential

The intersection of frozen snack product innovation and shifting dietary preferences across developed markets is creating commercially significant opportunities for producers willing to invest in reformulation and new format development. Consumer interest in plant-based proteins, clean label ingredients, high-protein formats, and ethnic-inspired flavour profiles is generating premium product demand that existing frozen snack portfolios are not fully addressing. Producers who develop frozen snack formats that credibly serve health-conscious consumer segments without sacrificing the convenience and taste quality that defines the category’s value proposition will be well positioned to capture this growth through 2035.

Recent Developments:

-

2025: General Mills, Inc. introduced Nature Valley Frozen Protein Bars in October 2025, bringing a high-protein, on-the-go format into frozen retail channels and directly addressing the growing urban consumer demand for convenient, nutritionally functional frozen snack options that fit active lifestyle needs.

-

2025: Conagra Brands, Inc. unveiled over 50 new frozen food products in June 2025, encompassing single-serve meals, plant-based alternatives, and gluten-free formats across both retail and e-commerce distribution, reinforcing the company’s strategy of diversifying its frozen snacks portfolio to capture a wider range of consumer dietary preferences.

-

2025: McCain Foods Limited expanded its air fryer-optimised product range across North American and European retail markets during 2025, investing in new format development and dedicated on-pack cooking guidance to capture incremental demand from the rapidly growing household air fryer user base.

Frozen Snacks Market Key Players are:

-

Nestlé S.A.

-

General Mills, Inc.

-

Conagra Brands, Inc.

-

McCain Foods Limited

-

The Kraft Heinz Company

-

Tyson Foods, Inc.

-

Nomad Foods Limited

-

Ajinomoto Co., Inc.

-

Dr. Oetker GmbH

-

Hormel Foods Corporation

-

Rich Products Corporation

-

Pinnacle Foods, Inc.

-

Bellisio Foods, Inc.

-

Amy’s Kitchen, Inc.

-

Saffron Road Foods

-

Maple Leaf Foods Inc.

-

JBS S.A.

-

Greencore Group plc

-

Iceland Foods Ltd.

-

Goya Foods, Inc.

Frozen Snacks Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 150.07 Billion |

| Market Size by 2035 | USD 261.24 Billion |

| CAGR | CAGR of 5.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Frozen Vegetables, Frozen Meat Snacks, Frozen Bakery Snacks, Frozen Seafood Snacks, Frozen Dairy Snacks, Others) • By Category (Ready-to-Cook, Ready-to-Eat) • By End User (Households, Foodservice, Institutional Buyers, Others) • By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Specialty Stores, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Dr. Oetker GmbH, Hormel Foods Corporation, Rich Products Corporation, Pinnacle Foods, Inc., Bellisio Foods, Inc., Amy’s Kitchen, Inc., Saffron Road Foods, Maple Leaf Foods Inc., JBS S.A., Greencore Group plc, Iceland Foods Ltd., and Goya Foods, Inc. |

Frequently Asked Questions

North America dominated the Frozen Snacks Market in 2025, holding approximately 38.72% of global revenues.

Frozen Vegetables dominated with approximately 32.45% of revenues in 2025.

Rising consumer demand for convenient and ready-to-cook food formats, driven by increasingly busy urban lifestyles and expanding cold chain retail infrastructure across emerging economies, is the primary growth factor for the Frozen Snacks Market.

The Frozen Snacks Market was valued at USD 150.07 Billion in 2025.

The Frozen Snacks Market is expected to grow at a CAGR of 5.70% from 2026 to 2035.

Get in Touch