Gene Therapy Starting Materials Market Report Scope & Overview:

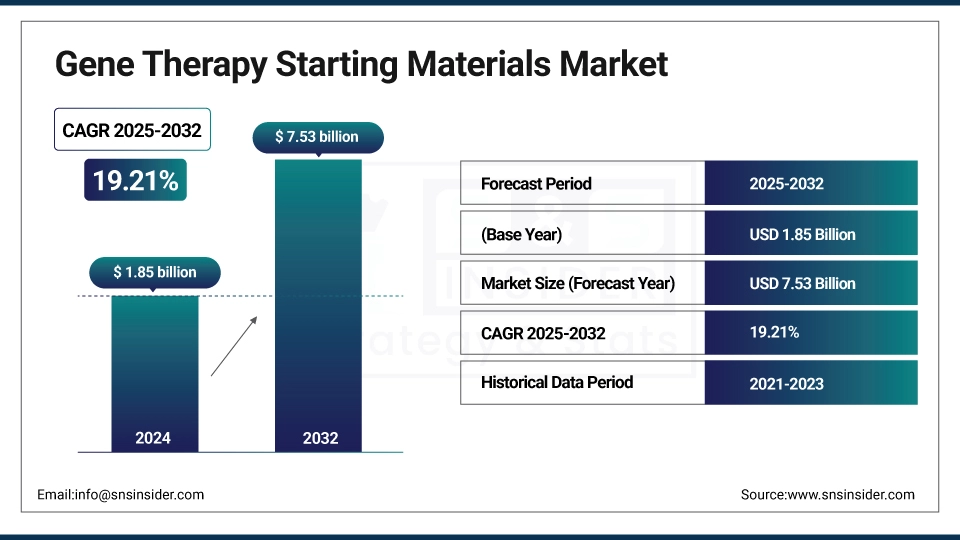

The gene therapy starting materials market was valued at USD 1.85 billion in 2024 and is expected to reach USD 7.53 billion by 2032, growing at a CAGR of 19.21% over the forecast period of 2025-2032.

An increase in demand for high-quality and uniform raw materials, including plasmids and viral vectors, is one of the major factors contributing to the global market for gene therapy starting materials market growth. These materials are essential to product quality, scale, and regulatory alignment. One of the major gene therapies starting materials market trends includes the transition to clinically viable GMP-grade, scalable, and affordable supply chains that help clinical dependability and mitigate manufacturing implementation risks, which fuel growth and innovation in the sector for the long term globally.

To Get more information On Gene Therapy Starting Materials Market - Request Free Sample Report

For instance, in February 2025, Aldevron reported a 28% year-over-year growth in plasmid DNA services, driven by rising global demand for high-quality gene therapy starting materials.

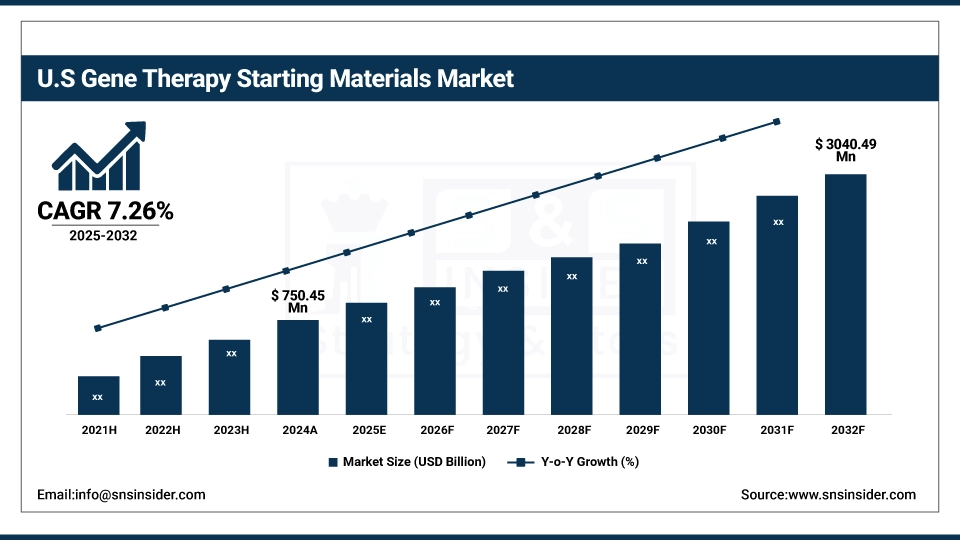

The U.S. gene therapy starting materials market was valued at USD 750.45 million in 2024 and is expected to reach USD 3040.49 million by 2032, growing at a CAGR of 19.13% over 2025-2032.

The U.S. is a leader in the gene therapy starting materials market due to its leadership in innovation, robust biotech industry, high R&D spending, and government support initiatives. Favorable investment trends, sophisticated GMP manufacturing, and academic-industry partnerships underpin scale and quality. This extensive value chain is the foundation for the U.S. leadership, as evidenced in recent gene therapy starting material market analysis reports.

For instance, in May 2025, the U.S. government allocated USD 3.5 billion under the National Biotechnology Initiative to boost domestic manufacturing of gene therapy starting materials and reduce foreign dependency.

Market Dynamics:

Drivers:

-

COVID-19 Pandemic is Driving the Gene Therapy Starting Materials Market Growth

The COVID-19 pandemic derailed supply, and then it actually enhanced the gene therapy starting materials market by increasing innovation, automation, and regulatory permissions. Businesses emphasized the need to secure supplies of raw materials and diversify their sources. The result was improved efficiency of production and investment that fueled only long-term growth. These changes had a big impact on the gene therapy starting materials market share, increasing its global reach and strategic relevance.

For instance, in February 2025, ARM reported a 40% increase in global CGT manufacturing capacity since 2020, driven by pandemic-era demand for plasmids and viral vectors in gene therapy.

Restraints:

-

Workforce Shortages and Complex Regulatory Standards are a Significant Restraint on the Gene Therapy Starting Materials Market Growth

Occupational shortages and convoluted regulations stifle the advancement of the gene therapy starting materials market growth as they lead to delays in production, under-utilized capacity, and compliance obstacles. Manufacturing and quality control skill gaps hinder scalability, and diverse global regulations drive up cost and complexity. Together, these factors act as barriers to efficient supply chains, postponing patient access and restricting global adoption of gene therapy breakthroughs.

For instance, in January 2025, 58% of CGT companies reported skilled workforce shortages in GMP manufacturing and QC, leading to production delays and impacting the gene therapy starting materials market growth.

Segmentation Analysis:

By Product

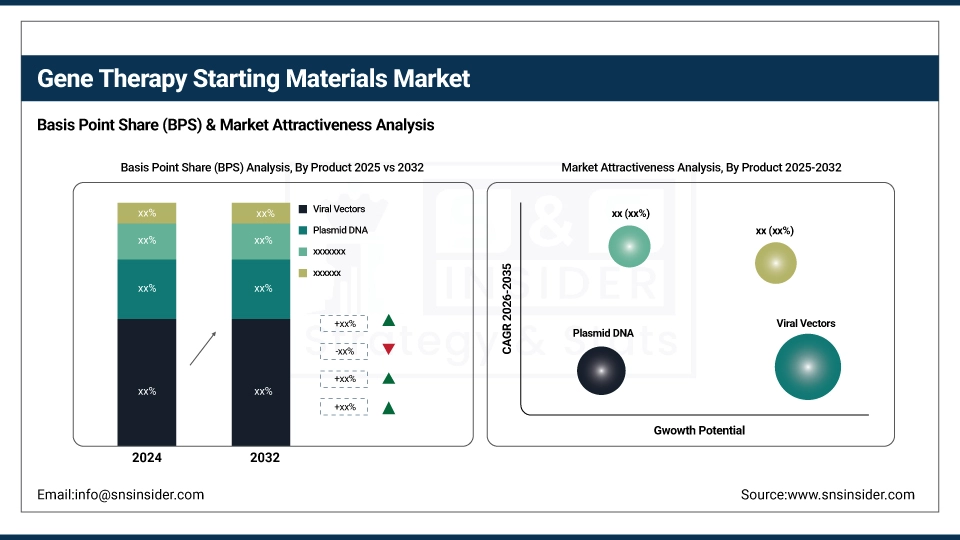

The viral vectors are the dominant segment in the gene therapy starting materials market, with a 43.94% share in 2024 as they are highly efficient gene transfer ability into the target cells. They provide predictable gene expression and are already being used in approved therapies, including Luxturna and Zolgensma. Robust clinical success, progression in vector engineering technology, and heightened need for AAV and lentiviral vectors are pivotal determinants of this expansion.

The plasmid DNA segment is emerging as the fastest growing with a CAGR of 19.82% in the gene therapy starting materials market, owing to its importance as a viral vector precursor. Demand is further bolstered by non-viral gene therapies and mRNA platforms. Rising number of approvals of advanced therapies, rising demand for GMP-grade plasmids, and growing investments in high-purity, scalable production technologies are some of the factors driving growth.

By Stage

In 2024, clinical therapeutics dominated the gene therapy starting materials industry with a 46.76% market share, fueled by growing approvals of gene therapies for rare and genetic diseases. Clinical trial growth, heavy biopharma investment, and regulatory assignments foster demand. The requirement for GMP-compatible starting materials guarantees the availability of a high-quality supply for late-phase trials and commercial therapeutic purposes.

The pre-clinical therapeutics segment is the fastest growing segment of the gene therapy starting materials analysis, owing to the high R&D spending and expansion of the early-stage pipeline. Pre-clinical studies by biopharma and academia to investigate new gene targets are moving forward at an accelerated pace. There is a growing requirement for high-purity and scalable starting materials, including plasmid DNA and viral vectors, which is being driven by innovation grants, venture capital, and joint research programs.

By Application

Oncology held a dominant gene therapy starting materials market share of 38.40% in the gene therapy starting materials industry in 2024, as a result of the high global cancer burden and need for tailored and personalized therapies. Gene therapies, including CAR-T and oncolytic viruses also need specialized starting materials, including viral vectors and plasmid DNA. Growth in the FDA approvals and robust clinical trial pipelines, and investment into cancer gene therapies are some of the key factors driving the market leadership of this segment.

Genetic disease is emerging as the fastest growing segment in the gene therapy starting materials industry with the highest CAGR of 20.21%, owing to an increase in diagnoses, progress in genomics, and more approvals of gene-based treatments for rare inherited diseases. Increasing investment in R&D, patient advocacy, and regulatory incentives, including orphan drug designations, is speeding the development of personalized therapies and, in turn, raising the requirement for high-quality starting materials, including plasmid DNA and viral vectors.

By End-User

Biopharmaceutical & Pharmaceutical Companies are the largest segment of end users for the gene therapy starting materials industry, supported by strong internal manufacturing, solid financial support, and regulatory know-how. Their ability to buy up biotech firms, optimize supply chains, and ramp up production globally is one of their competitive advantages. These companies are also spending significant amounts on GMP-capable facilities to maintain quality, consistency, and supply security across clinical and commercial operations.

The CROs & CMOs segment is witnessing the highest growth in the gene therapy starting materials market, as biopharma companies outsource more of their work seeking cost savings, scale, and regulatory backing. These companies provide expertise in production and viral vector and plasmid technology, allowing for accelerated time-to-market. Workforce shortages are also fueling their rapid growth within clinical and commercial pipelines.

Regional Analysis:

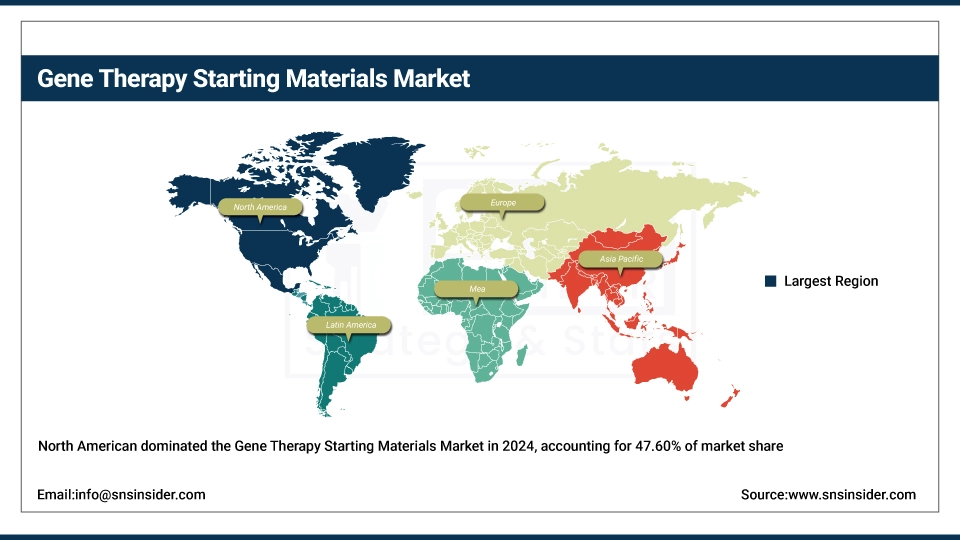

In 2024, the North American region holds the largest market share of the gene therapy starting materials market and dominates the market with a 47.60% market share, owing to its strong biotechnology environment, highly developed healthcare system, and investment in R&D. The existence of large biopharma players, leading research institutions and friendly regulation, including the FDA’s accelerated pathways, also exist in favor of gene therapy. Moreover, a surge in the demand for viral vectors, plasmid DNA, & other raw materials, and strategic partnerships and new clinical trials supplement the market growth. The U.S. is a leader with many hoods and FDA-approved therapies and CGTs manufacturing capacities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is becoming a significant market player for gene therapy starting materials due to favorable regulatory environments, including the EMA’s PRIME initiative and increasing investments in novel therapies. Led by countries including Germany, the U.K., and France, the Western Europe region is one of the key markets for melanoma drugs. The area is supported by public-private partnerships and the expansion of local CROs/CMOs focused on gene therapy materials and technologies, along with an increase in rare disease research funding.

Asia Pacific emerges as the fastest-growing region with the highest CAGR of 20.15%, driven by a surge in biotech investments, government support, and increasing prevalence of genetic disorders. Countries including China, Japan, South Korea, and India are expanding gene therapy research and manufacturing infrastructure. China, for instance, has accelerated clinical trial approvals and invested heavily in viral vector and plasmid DNA production. Japan’s regulatory reforms and regenerative medicine laws have encouraged fast-track development. Additionally, a large patient pool, rising awareness, and increasing partnerships between global biopharma companies and regional CROs/CMOs are fueling growth. Competitive manufacturing costs and the rise of local biotech startups are further accelerating demand for high-quality starting materials, making Asia Pacific a pivotal region for market expansion.

The Middle East & Africa is the least growing region in the gene therapy starting materials market due to weak R&D infrastructure, low healthcare expenditure, and lack of access to treatments. Moreover, regulatory challenges, shortage of trained professionals, and a smaller number of trials in the area make it difficult to adapt quickly, leading market penetration and investment lagging far behind those in other global regions.

The Latin American gene therapy starting materials industry is witnessing a steady rise in growth, as the healthcare infrastructure is developing, local manufacturing is restricted, and a smaller number of clinical trials. Nevertheless, the biotech sector in countries including Brazil and Mexico is on the rise, and regulations are getting better. Increased awareness, government efforts, and collaborations with international biopharma firms are likely to fuel future market growth. However, obstacles including expense and lack of skills, remain.

Key Players:

Gene therapy starting materials Companies, including Thermo Fisher Scientific, Sartorius AG, Merck KGaA, Catalent Inc., WuXi Advanced Therapies, Aldevron, Charles River Laboratories, Lonza Group AG, AGC Biologics, Oxford Biomedica, Vigene Biosciences, Brammer Bio, GenScript Biotech, Takara Bio Inc., VGXI, Inc., CBM, Andelyn Biosciences, VIVEbiotech, Touchlight Genetics, MilliporeSigma, and other players.

Recent Developments:

-

In May 2024, Aldevron introduced an ultra-pure research-grade plasmid DNA platform in May 2024, streamlining early-stage gene therapy workflows and accelerating transitions over preclinical discovery to clinical-grade manufacturing.

-

In April 2024, Touchlight Genetics partnered with OXGENE to develop scalable, antibiotic-free AAV gene therapy platforms using doggybone DNA (dbDNA) technology, boosting manufacturing efficiency and regulatory compliance.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.85 billion |

| Market Size by 2032 | USD 7.53 billion |

| CAGR | CAGR of 19.21% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Viral Vectors, Plasmid DNA, Cell Lines, Others) • By Stage (Pre-clinical Therapeutics, Clinical Therapeutics, Marketed Therapeutics) • By Application (Oncology, Infectious Disease, Genetic Disease, Others) •By End User(Biopharmaceutical & Pharmaceutical Companies, CROs & CMOs, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific, Sartorius AG, Merck KGaA, Catalent Inc., WuXi Advanced Therapies, Aldevron, Charles River Laboratories, Lonza Group AG, AGC Biologics, Oxford Biomedica, Vigene Biosciences, Brammer Bio, GenScript Biotech, Takara Bio Inc., VGXI, Inc., CBM, Andelyn Biosciences, VIVEbiotech, Touchlight Genetics, MilliporeSigma, and other players. |

Frequently Asked Questions

Thermo Fisher Scientific, Sartorius AG, Merck KGaA, Catalent Inc., WuXi Advanced Therapies, Aldevron, Charles River Laboratories, and Lonza Group AG, are the major players in the Gene Therapy Starting Materials Market.

Workforce Shortages and Complex Regulatory Standards Are a Significant Restraint on the Gene Therapy Starting Materials Market Growth.

The CAGR of the Gene Therapy Starting Materials Market is 19.21% during the forecast period of 2025-2032.

The North American region dominated the Gene Therapy Starting Materials Market in 2024.

The current size of the Gene Therapy Starting Materials Market is USD 2.20 billion globally.

Get in Touch