Pediatric Palliative Care Market Report Scope & Overview:

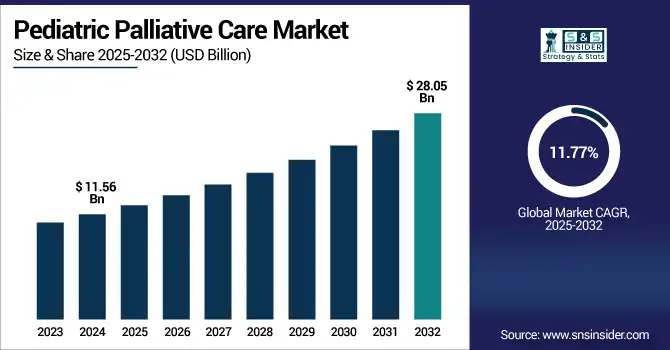

The pediatric palliative care market size was valued at USD 11.56 billion in 2024 and is expected to reach USD 28.05 billion by 2032, growing at a CAGR of 11.77% over the forecast period of 2025-2032.

To Get more information on Pediatric Palliative Care Market - Request Free Sample Report

Growing awareness of pediatric life-limiting illnesses, increasing prevalence of pediatric chronic disease, and rising demand for specialized care services are key factors driving the global pediatric palliative care market growth. Globally, improvements in healthcare infrastructure, government initiatives, and nonprofit input are improving access to integrated, multidisciplinary pediatric palliative care. Furthermore, patient-centric strategies are also being driven by the integration of home-based and telehealth models. As there is an increased awareness about the need for emotional, social, and spiritual support, the market is set for high growth, leading to high revenue generation in both developed and developing regions.

The U.S. pediatric palliative care market size was valued at USD 3.40 billion in 2024 and is expected to reach USD 8.10 billion by 2032, growing at a CAGR of 11.53% over the forecast period of 2025-2032.

North America holds the largest share of the pediatric palliative care market, led by the U.S. due to the well-developed healthcare system, the existence of specialized pediatric palliative care programs, a well-established research ecosystem in the U.S., and health services data collection systems, together with well-defined government-funded child health services programs.

Market Dynamics:

Drivers

-

Market Growth is Aided by Advances in Pediatric Healthcare Infrastructure

Continued efforts to build capacity and modernize pediatric healthcare infrastructure have resulted in improved access to specialized palliative care. More and more hospitals and clinics are equipped with specialty pediatric palliative care units, pain management equipment, and the involvement of multidisciplinary teams with physicians, psychologists, and child life specialists. This means that it can provide ongoing, tailored support for children with life-limiting conditions. Moreover, remote patient monitoring, electronic health records, telemedicine, and other technologies are creating seamlessness between care delivery and patient outcomes, contributing to the market development.

According to NCBI, pediatric palliative care can only be provided to less than 3% of children in high-income countries, even though more than 21 million children around the globe need palliative care for serious health-related needs of a noncurative nature.

-

The Market is Driven by Support from the Government and NGOs

Expansion of pediatric palliative care, particularly in low-resource settings, requires supportive governmental policies in partnership with non-governmental organizations (NGOs). Funding programs, policy frameworks, and national strategies to incorporate palliative care into primary healthcare systems are being established by governments. At the same time, NGOs are contributing to these efforts by addressing issues through awareness campaigns, training healthcare givers, and assisting families with counselling, equipment, and home care. Such collaborations are increasing access, quality, and continuity of care, and these factors are fueling the growth of the market.

According to WHO, 98% of children in need of palliative care live in low- and middle-income countries, where formal services are still scarce, stressing the need for development with policy and NGO-led solutions around the globe.

Restraint

-

Limited Access in Low- & Middle-Income Countries (LMICs) is Restraining the Market from Growing

The low- and middle-income countries (LMICs) with the majority of the population lacking access to awareness, care, and services. In these areas, the healthcare systems frequently do not have the basic infrastructure and finances available to deliver specialist services to children with life-limiting or life-threatening conditions. Due to a lack of dedicated services, trained professionals, and to lack of crucial medications, including pediatric formulations of pain relief, this service is highly limited. In addition, national health policies in many LMICs neither prioritize nor incorporate palliative care within their mainframes, providing limited institutional backing. The result is an inequity where millions of children everywhere, most strikingly in Africa, South Asia, and parts of Latin America, suffer from serious illness without adequate support or comfort services. This unavailability not only hinders growth in the market but also deepens the gap in global health inequities.

Segmentation Analysis:

By Disease Condition

HIV segment dominated the pediatric palliative care market share with 28.5% in 2024 due to infants who are HIV-positive remaining a major public health concern, due to the long burden of pediatric HIV in low- and middle-income countries. To address the implications of long-term symptom care, psychosocial support, and multidisciplinary care, children infected with HIV are typically complicated by the presence of comorbid conditions, including opportunistic infections, neurological conditions, and developmental delays. In this specific context, palliative care entails issues of pain, nutrition, mental health, and quality of life, which have become an increasingly prominent feature of HIV programs, notably with the influence of global health initiatives and donor funding.

The cancer segment is anticipated to be the fastest-growing segment in the pediatric palliative care market during the forecast years. Drivers of the need for improved care include the increasing rates of pediatric cancers globally and recognition of the potential of an early palliative approach to address complex, sometimes refractory, symptoms such as pain, fatigue, emotional distress, etc. Rising accessibility to pediatric oncology services, coupled with greater numbers of multidisciplinary palliative teams and growing inclusion of palliative care within treatment guidelines in established and developing nations, is driving demand.

By Provider

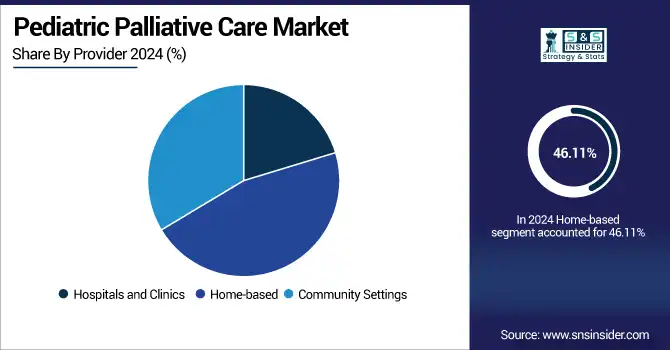

In 2024, the pediatric palliative care market dominated by the home-based segment, with a 46.11% share % as more care is being delivered in familiar, more comfortable environments such as the family's home, which also provides a superior emotional impact on the pediatric patient and their families. A home-based care operating model enables personalized, family-centered care, with limited hospitalizations and health care costs, and larger changes to health care supply and capacity towards home. Palliative care programs have often grown to include home visits by the multidisciplinary teams that include nurses, counselors, and social workers, too, particularly in low-resource settings, where the number of hospital beds is scarce or where patients may not have access to a specialized care facility within a reasonable distance, such as in many rural settings.

The hospitals and clinics segment is projected to grow at the fastest rate within the pediatric palliative care market during the forecast period, owing to the growing number of specialized pediatric palliative care units in hospitals. As more children live with life-limiting conditions, healthcare systems are shoring up institutional models of care that integrate palliative care along with curative treatment. In addition, access to state-of-the-art diagnostic and therapeutic resources, interdisciplinary expertise, and integrated inpatient and outpatient care is prompting more families to pursue comprehensive pediatric palliative care through hospitals and clinics.

By Service Type

In 2024, the pediatric palliative care market was dominated by inpatient care, which captured the largest share owing to the requirement of ongoing and targeted medical care for pediatric patients with complex, end-of-life illnesses. In an increasingly complex medical toolbox, inpatient facilities offer pediatric palliative specialists, pain management, and other critical support services around the clock, which are vital in advanced stages of illness. In addition, they are centres of concerted care planning, emergency care, and support for families, a response to acute symptoms, and an effective location for total, multidisciplinary care.

In the forecast period, the tele-palliative care segment will grow faster due to the developments in digital health infrastructure and evolving demands for increased access to remote care. With tele-palliative care, follow-ups, emotional support, and symptom management consultations can all be done virtually, benefitting families in remote or underserved areas. It also lessens the burden of travel, increases continuity of care, and allows for instant communication between caregivers and specialists to ensure the patient receives the proper care they need. There is no doubt that this momentum was amplified by the pandemic, where telehealth models were adopted rapidly and are now embedded across healthcare settings, including for pediatric palliative care pathways.

By End User

In 2024, the pediatric palliative care market, dominated by the hospitals segment, due to the well-established system of medical amenities offered by hospitals, availability of pediatric specialists, and integrated care services. For many children with a complex and or life-threatening condition, hospitals are a focal point for diagnosis, treatment, and advanced care planning. Such institutions grant immediacy to advanced medical technologies, pain management modalities, and critical care, and thus represent the preferred venue for acute and chronic pediatric palliative interventions in a consistent and multi-disciplinary manner.

The palliative care centers segment is expected to see the fastest growth as healthcare systems are now realizing the need for specialized and dedicated pediatric palliative care facilities. These centers specialize only in enhancing the quality of life of sick children who suffer from serious diseases by offering personalized care, emotional support, and family counseling. A growing awareness, enabling policy environments, and philanthropic attention to developing stand-alone pediatric palliative care units (particularly in community and hospice settings) are also contributing to the growth.

Regional Analysis:

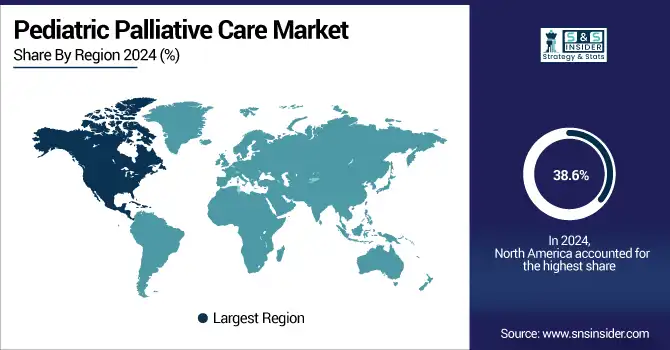

North America dominated the pediatric palliative care market trend with a 38.6% market share, as it has a well-established healthcare ecosystem with robust healthcare policies and the presence of advanced pediatric palliative care services. Hospitals, specialty clinics, and home healthcare have seen significant progress towards pediatric palliative care integration in countries such as the United States and Canada. In addition, the availability of well-trained health care personnel, early implementation of clinical and multidisciplinary care models, and various governmental initiatives further accelerate the establishment of high-quality child-centered palliative care in the region.

Asia Pacific is projected to be a significantly growing region of the pediatric palliative care market during the forecast period, owing to the rise in awareness, pediatric disease burden, healthcare infrastructure, and economic growth. In countries such as India, China, and Indonesia, governments and non-profit organizations are encouraging the establishment of palliative services, which are home-based and community-based. Training programs for pediatric care providers are also growing, as are public-private partnerships focused on expanding the reach of compassionate end-of-life care for children, along with their families, in underserved and rural areas of the region.

The European pediatric palliative care market is growing substantially, fueled by healthcare policies and structures that are more supportive, dedicated funding venues, and more growth in service frameworks. There is a growing trend towards integrated care models in this region, involving home-and hospital-based care. Programs, initiatives, and activities such as EU4Health and pediatric palliative initiatives taking place in different countries have significantly contributed to enhancing access and quality of care. Leading the way are the UK and Germany with innovation in service delivery and professional training. For instance, the newly developed training initiative by the Children’s Palliative Care Leadership Institute, which was launched in February 2024 in partnership with Two Worlds Cancer Collaboration and the International Children’s Palliative Care Network (ICPCN) to help develop a cohort of pediatric care providers across Europe.

The Latin America and Middle East & Africa (MEA) pediatric palliative care market is expected to show moderate growth in the forecast years, due to increasing awareness related to the benefits of palliative care and gradual development of healthcare infrastructure in the region. The introduction of palliative care into pediatric services in Latin America has been a slow process, with only a few countries (e.g., Brazil and Mexico) developing protocols to facilitate this part of care, all aided by pediatric associations and NGOs at both national and regional levels. Still, the speed of creation is uneven all around the region, depending on the quantity of budget, training, and accessibility.

In the MEA, especially in the relatively more advanced areas of the Gulf Cooperation Council (GCC), pediatric palliative care is emerging as an essential element of child health services. The UAE and Saudi Arabia, for instance, are working to integrate palliative care into national health plans. However, barriers such as a lack of trained specialized workforce, stigmas around end-of-life care in general, and limited access, especially in rural or underserved regions, inhibit fast market growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players:

The pediatric palliative care market companies are Boston Children's Hospital, Children's National Hospital, St. Jude Children’s Research Hospital, Great Ormond Street Hospital for Children NHS Foundation Trust, The Hospital for Sick Children (SickKids), Nationwide Children’s Hospital, CHU Sainte-Justine, Children’s Hospital Los Angeles (CHLA), Cincinnati Children’s Hospital Medical Center, Ann & Robert H. Lurie Children's Hospital of Chicago, Helen & Douglas House, Together for Short Lives, Canuck Place Children's Hospice, Starship Children's Hospital, Rachel House, Children’s Hospice South West (CHSW), Butterfly Children’s Hospices, Sunflower Children’s Hospice, Little Stars Project (ICPCN), Two Worlds Cancer Collaboration, and other players.

Recent Developments:

-

In April 2024, Niloufer Hospital collaborated with the Pain Relief and Palliative Care Society to enhance pediatric palliative care services in Hyderabad, India. The partnership involved the strengthening of perinatal and neonatal care, and pediatric training and capacity-building programs.

-

In April 2023 RWJBarnabas Health, a premier integrated health care system in New Jersey, in April 2023, increased its pediatric palliative care program at Children's Specialized Hospital. The project was to expand inpatient and outpatient pediatric palliative services throughout the health system and its network affiliates.

Pediatric Palliative Care Market Report Scope:

Report Attributes Details Market Size in 2024 USD 11.56 Billion Market Size by 2032 USD 28.05 Billion CAGR CAGR of 11.77% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Disease Condition (HIV, Premature Birth and Trauma, Congenital Malformations, Injury, Poisoning and External Causes, Cancer, Congenital Disorders, Neurological Disorders, Cardiovascular Disorders, Genetic Disorders, Others [e.g., rare diseases, infectious diseases])

• By Provider (Hospitals and Clinics, Home-based, Community Settings)

• By Service Type (Inpatient Care, Outpatient Care, Home-based Care, Hospice Care, Respite Care, Consultation Services, Tele-palliative Care)

• By End User (Hospitals, Pediatric Specialty Clinics, Home Healthcare Providers, Palliative Care Centers, Long-term Care Facilities)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles The pediatric palliative care market companies are Boston Children's Hospital, Children's National Hospital, St. Jude Children’s Research Hospital, Great Ormond Street Hospital for Children NHS Foundation Trust, The Hospital for Sick Children (SickKids), Nationwide Children’s Hospital, CHU Sainte-Justine, Children’s Hospital Los Angeles (CHLA), Cincinnati Children’s Hospital Medical Center, Ann & Robert H. Lurie Children's Hospital of Chicago, Helen & Douglas House, Together for Short Lives, Canuck Place Children's Hospice, Starship Children's Hospital, Rachel House, Children’s Hospice South West (CHSW), Butterfly Children’s Hospices, Sunflower Children’s Hospice, Little Stars Project (ICPCN), Two Worlds Cancer Collaboration, and other players.

Frequently Asked Questions

Ans: North America dominated the Pediatric Palliative Care Market in 2024.

Ans: The “HIV” segment dominated the Pediatric Palliative Care Market.

Ans: Market Growth is Aided by Advances in Pediatric Healthcare Infrastructure.

Ans: The Pediatric Palliative Care Market was USD 11.56 billion in 2024 and is expected to reach USD 28.05 billion by 2032.

Ans: The Pediatric Palliative Care Market is expected to grow at a CAGR of 11.77% from 2025 to 2032.

Get in Touch