Hemodynamic Monitoring Devices Market Report Scope & Overview:

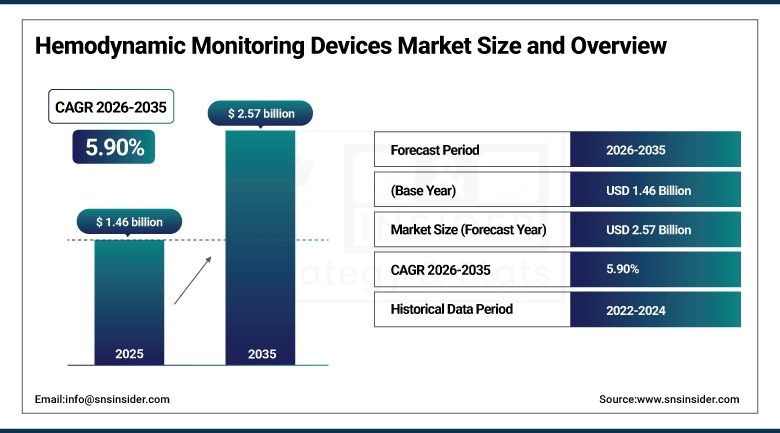

The Hemodynamic Monitoring Devices Market size is valued at USD 1.46 Billion in 2025 and is projected to reach USD 2.57 Billion by 2035, growing at a CAGR of 5.90% during the forecast period 2026–2035.

The Hemodynamic Monitoring Devices Market Analysis Report offers an in-depth evaluation of market dynamics, technologies used, and clinical application areas. The hemodynamic monitoring devices market is being driven by increased use of critical care monitoring, high incidences of cardiovascular diseases and respiratory disorders, higher adoption rates of non-invasive and AI-based hemodynamic monitoring devices, and improved healthcare infrastructure between 2026 and 2035.

More than 25 million hemodynamic monitoring procedures have been performed in ICUs as of 2025 due to increased number of surgeries and the requirement of critical care monitoring.

Market Size and Forecast:

-

Market Size in 2025: USD 1.46 Billion

-

Market Size by 2035: USD 2.57 Billion

-

CAGR: 5.90% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Hemodynamic Monitoring Devices Market - Request Free Sample Report

Hemodynamic Monitoring Devices Market Trends:

-

The movement toward more non-invasive monitoring techniques is on the rise due to patient comfort and safety against infections.

-

A faster transition into AI-based platforms that can perform predictive monitoring and timely interventions.

-

Development of more home-based and remote monitoring technologies in support of chronic diseases management in hospitals.

-

Increased demand for portable and wireless monitors in emergencies and ambulatory care environments.

-

Conspicuous growth in emerging economies due to increasing availability of ICU facilities and investments in healthcare.

-

Focus on sustainability practices through minimal use of disposable plastic components and sustainable sensors.

-

An increased focus on cybersecurity issues and patient data privacy amid the growing prevalence of IoT systems.

-

The deployment of wearable monitoring systems during pre-op and post-op procedures for consistent patient monitoring.

U.S. Hemodynamic Monitoring Devices Market Insights:

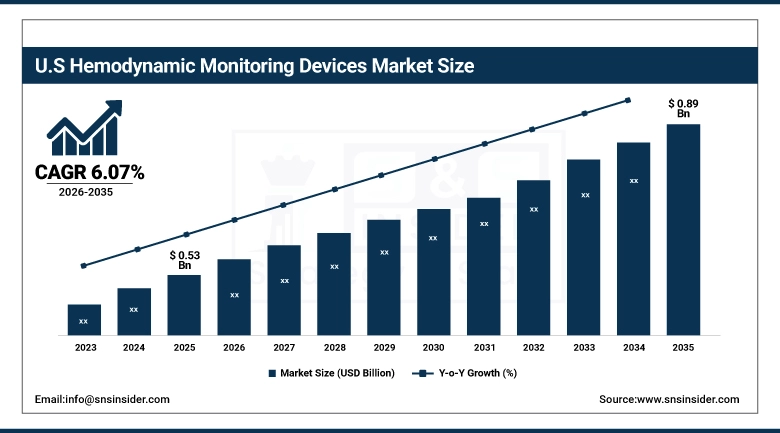

The U.S. Hemodynamic Monitoring Devices market is estimated to grow from USD 0.53 Billion in 2025 to USD 0.89 Billion in 2035 at a CAGR of 6.07%. Factors driving growth include increased numbers of ICU beds, a greater number of surgeries being performed, and the use of predictive analysis in peri-operative and emergency monitoring. Moreover, an increasing preference for non-invasive and minimally invasive approaches is changing medical practices.

Hemodynamic Monitoring Devices Market Growth Drivers:

- Rising ICU admissions and surgical volumes are driving demand for advanced hemodynamic monitoring solutions.

U.S. Growth Drivers include the expansion of critical care capacity, increase in cardiovascular and respiratory diseases, and the rising demand for perioperative and emergency monitoring. Hospitals, ASCs, and homecare settings are increasingly using non-invasive hemodynamic monitoring devices and systems powered by artificial intelligence for better patient safety, reduced risks of infection, and greater clinical efficiency. The integration of the technology into EHRs and telehealth platforms is boosting adoption rates, leading to enhanced outcomes and continued market growth.

In 2025, more than 62 percent of hospitals and surgical centers in the United States were employing advanced hemodynamic monitoring devices.

Hemodynamic Monitoring Devices Market Restraints:

-

High device costs and reimbursement challenges are limiting broader adoption of advanced monitoring systems.

U.S. Markets encounter restrictions due to substantial costs of invasive and AI-powered systems along with additional training and maintenance costs. Shortages in reimbursements for the use of complex monitoring techniques, especially those employed in an ambulatory and at-home setting, act as barriers to market penetration. Data security and privacy issues along with possible cyberattacks in interconnected systems create additional impediments. In addition to these factors, limited knowledge among small-scale healthcare institutions regarding advanced monitoring techniques is likely to act as a barrier to continued market growth.

In 2025, more than 41% of U.S. healthcare institutions cited financial constraints as the key impediment in upgrading to advanced hemodynamic monitoring equipment.

Hemodynamic Monitoring Devices Market Opportunities:

-

Rising adoption of AI‑enabled and telehealth‑integrated monitoring systems is creating new growth opportunities.

The US market for hemodynamic monitoring devices will be well placed to capitalize on the development of advanced digital health networks, higher emphasis on patient-centric treatment approaches, and use of predictive analysis. The growth areas include the quick advancements in portable and wireless monitoring tools that allow constant monitoring outside the confines of hospitals. The growing trend toward sustainability, green sensors, and cloud computing further boosts the growth prospects. Collaboration between healthcare organizations and tech firms will foster innovations that can bring about better patient outcomes and revenue streams.

More than 35% of hospitals in the US started piloting their AI-based hemodynamic monitoring programs by 2025.

Hemodynamic Monitoring Devices Market Segmentation Analysis:

-

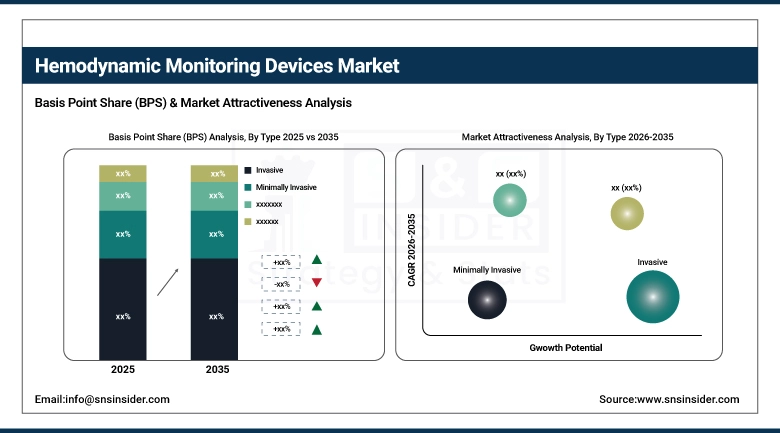

By Type, Invasive held the largest market share of 34.62% in 2025, while Non-invasive are expected to grow at the fastest CAGR of 6.66% during 2026–2035.

-

By Product, Disposables (catheters, sensors) dominated with 54.28% market share in 2025, whereas Software & Data Analytics (AI-driven platforms) are projected to record the fastest CAGR of 7.81% through 2026–2035.

-

By Application, ICU/CCU accounted for the highest market share of 39.29% in 2025, while Emergency Dept. are expected to grow at the fastest CAGR of 8.50% during the forecast period.

-

By End User, Hospitals held the largest share of 64.16% in 2025, while Home Care Settings are expected to grow at the fastest CAGR of 8.89% during the forecast period.

By Type, Invasive dominates while Non‑invasive grows rapidly:

Invasive monitoring equipment segment is dominating due to it’s currently in vogue as they are reliable, given their accuracy in critical care and operating rooms. In the year 2025, more than 15 million procedures were carried out using invasive equipment, as their reliability was proved in dealing with patients who have high risks.

Non-invasive monitoring equipment has witnessed fastest growth owing to increasing preferences for comfort and low chances of infections and telehealth applications. More than 9 million procedures were recorded using non-invasive monitoring equipment. A growing emphasis on patient‑centric care and integration with wearable technologies is further accelerating adoption, making non‑invasive systems a preferred choice across outpatient and home care settings.

By Product, Disposables dominate while Software & Analytics grow rapidly:

Disposables catheters and sensors will retain their dominance owing to the important part that they play in invasive and non-invasive monitoring, being widely used in ICUs and surgery wards. Around 120 million devices were being used as there was a heavy dependence on single-use disposables for the accurate results they provided and to prevent infections.

Software/Data Analytics category is the fast-growing one due to the emergence of AI-based predictive monitoring systems, interoperability with EHRs, and the requirement of real-time clinical decision support systems. The installation rate of these solutions increased rapidly, and over 45,000 devices had been installed in coming years.

By Application, ICU/CCU dominates while Emergency grows rapidly:

The ICU/CCU applications remain popular due to the constant increase in the need for constant monitoring among the patients in critical condition, making up an integral part of any hospital that deals with complicated respiratory or cardiovascular cases. According to forecasts for 2025, their implementation would surpass 10 million procedures annually due to the importance of hemodynamic monitoring in ICU practice.

Emergency room applications represent the quickest-growing segment due to the increased number of accidents, surgical cases, and the necessity to stabilize patients in a timely manner. Growing reliance on rapid, non‑invasive monitoring technologies and integration with portable devices is further accelerating adoption, ensuring faster decision‑making and improved patient outcomes in emergency care environments.

By End User, Hospitals dominate while Home Care grows rapidly:

Hospitals retain their dominance due to their large ICU capabilities, advanced surgery wings, and dependence on invasive and noninvasive monitoring systems in providing intensive care. For instance, hospital use was estimated at more than 18 million, showing the key role that hospitals play in handling complicated cases of cardiovascular problems and perioperative procedures.

Home Care Settings are the fastest-growing market segment due to growing demand for remote monitoring and telehealth. The number of home care procedures grew exponentially, reaching 7 million in 2025, owing to the increased use of wearable and wireless monitoring technologies.

Hemodynamic Monitoring Devices Market Regional Analysis:

North America Hemodynamic Monitoring Devices Market Insights:

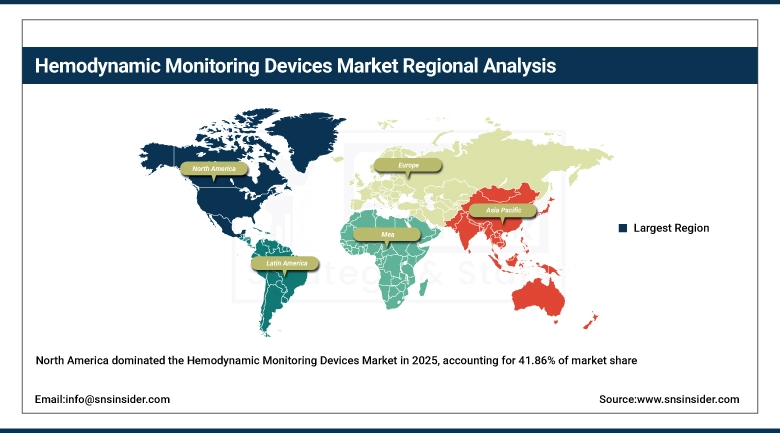

North America continues to be the leader in terms of market share, accounting for 41.86%. This dominance can be attributed to the presence of a robust healthcare sector, high demand for surgeries, and the widespread use of both invasive and non-invasive monitoring technologies. The United States and Canada are the frontrunners of growth within this region due to the rising prevalence of cardiovascular and respiratory diseases, growing number of Intensive Care Units (ICUs), and higher number of organ transplants. The hospitals and specialty clinics within this region are increasingly focusing on AI-based prediction monitoring and telemedicine.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Hemodynamic Monitoring Devices Market Insights:

North America being home to the largest market comes from the high number of surgeries, presence of intensive care units, and usage of high-tech monitoring equipment in the market. The increase in the rate of cardiovascular diseases, autoimmune diseases, and organ transplants in the country creates the need for invasive and non-invasive technologies. The adoption of electronic health record integration through artificial intelligence and telemedicine platforms is increasing fast.

Asia Pacific Hemodynamic Monitoring Devices Market Insights:

Asia Pacific region witnesses rapid growth in the rate of 8.04% CAGR due to increase in number of surgeries, availability of more ICUs, and increase in patients suffering from cardiovascular diseases and respiratory issues. India, Japan, and South Korea lead in the adoption of such monitoring technologies owing to increased government spending on healthcare, and expansion in private hospitals in these countries. Growing awareness regarding patient safety, use of telemedicine services, and reduction in costs favor adoption of these products.

China Hemodynamic Monitoring Devices Market Insights:

The China is experiencing vigorous expansion thanks to the expansion of healthcare facilities, increase in surgical procedures, and growing incidences of chronic heart disease. The strong government investment in upgrading hospitals and ensuring intensive care unit capability is promoting the implementation of advanced monitoring systems. There has been a growing preference for non-invasive monitoring devices that are powered by artificial intelligence, especially among hospitals and specialized centers located in urban areas.

Europe Hemodynamic Monitoring Devices Market Insights:

The European market has a mature status due to its healthcare facilities, strict guidelines, and availability of advanced monitoring systems both invasive and noninvasive. The growing cases of heart-related diseases, lung ailments, and surgery procedures, are among the drivers of this industry. There are countries such as France, Italy, and Spain that have embraced telemedicine services and the incorporation of artificial intelligence for monitoring. Eco-friendly sensors are among the trends in this industry.

Germany Hemodynamic Monitoring Devices Market Insights:

Germany leads the European healthcare industry with factors such as the presence of superior hospital infrastructure, attention to critical care, and use of invasive monitoring devices. Increased surgical procedures, high incidence of cardiovascular diseases, and investments made in digital health systems contribute to market growth. The use of non-invasive and AI-based monitoring products is picking up pace especially at universities and specialized hospitals.

Latin America Hemodynamic Monitoring Devices Market Insights:

The Latin American market is experiencing steady growth, driven by the increased healthcare infrastructure, the number of surgical procedures performed, and the prevalence of heart and respiratory ailments. Brazil and Mexico are the pioneers in adopting these technologies, with the implementation of both invasive and non-invasive patient monitoring solutions in various hospitals. Low awareness levels and financial limitations are hindrances, but with governmental and commercial investments, progress is being made.

Middle East & Africa Hemodynamic Monitoring Devices Market Insights:

The Middle East & Africa segment is experiencing growth as a result of increased investments in hospitals and the increase in the number of surgeries conducted, alongside the rising prevalence of heart ailments among people. Countries such as Saudi Arabia and the UAE are at the forefront of adoption, due to the presence of government initiatives for healthcare modernization. Monitoring devices that can be used easily outside the confines of a hospital setting have gained popularity in the private hospital and clinic environment.

Hemodynamic Monitoring Devices Market Competitive Landscape:

Edwards Lifesciences

Edwards Lifesciences is an American medical technology company that is known globally for being the leader in hemodynamic monitoring with its range of invasive and minimally invasive products, which include Swan Ganz catheters and FloTrac sensors. The focus of the products offered by Edwards Lifesciences includes cardiac output measurements and perioperative monitoring, especially in ICUs. However, the company is making efforts toward developing its non-invasive product range with AI and collaboration with other healthcare organizations.

-

In August 2025, Edwards advanced its Acumen IQ sensor platform with enhanced predictive algorithms for hypotension management, strengthening its leadership in perioperative monitoring.

Koninklijke Philips (Philips Healthcare)

Koninklijke Philips (Philips Healthcare), which is headquartered in the Netherlands, plays a significant role in the provision of systems that monitor hemodynamics through noninvasive or minimally invasive methods. Philips’ IntelliVue Monitoring System and their software platforms serve the purposes of monitoring patients both in the operating theater and ICU settings. Philips has made its strength in connectivity, interoperability, and artificial intelligence-based analytics. Their focus involves advancing their capabilities in remote patient monitoring and the use of cloud-based platforms to achieve predictive patient monitoring.

-

In April 2025, Philips expanded its IntelliVue X3 portable monitor line with wireless hemodynamic modules, enhancing mobility and remote patient monitoring in critical care environments.

GE HealthCare Technologies Inc.

GE Healthcare Technologies Inc. is a healthcare technology firm based out of the United States that specializes in developing cutting-edge monitoring technologies especially used in intensive care units and perioperative settings. The CARESCAPE monitoring system offered by GE provides clinicians with the ability to make informed decisions using hemodynamic measurements and other patient data. Innovation in data analytics, artificial intelligence, and compatibility with electronic health record systems is GE’s core focus, allowing healthcare providers to enhance their operations.

-

In December 2025, GE HealthCare launched upgrades to its CARESCAPE platform with advanced hemodynamic modules, strengthening its competitive positioning in high-acuity care settings.

Hemodynamic Monitoring Devices Market Key Players:

Some of the Hemodynamic Monitoring Devices Market Companies are:

-

Edwards Lifesciences

-

Koninklijke Philips

-

GE HealthCare Technologies Inc.

-

Getinge AB

-

Baxter International Inc.

-

LiDCO Group

-

ICU Medical Inc.

-

Drägerwerk AG & Co. KGaA

-

Mindray Medical International

-

Nihon Kohden Corporation

-

Siemens Healthineers

-

Medtronic plc

-

Becton Dickinson (BD)

-

Terumo Corporation

-

Abbott Laboratories

-

Schiller AG

-

Deltex Medical Group

-

Pulsion Medical Systems (Maquet/Getinge subsidiary)

-

Osypka Medical GmbH

-

CNSystems Medizintechnik GmbH

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.46 Billion |

| Market Size by 2035 | USD 2.57 Billion |

| CAGR | CAGR of 5.90% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Invasive, Minimally Invasive, Non-Invasive, Others), • By Product (Disposables (catheters, sensors), Monitors (systems, software), Software & Data Analytics (AI-driven platforms), Accessories (cables, connectors, disposables linked to monitors), Others) , • By Application (ICU/CCU, Cardiopulmonary Department, Neurosurgery, Emergency Department, Others), • By End Use (Hospitals, Ambulatory Surgical Centers, Home Care Settings, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Edwards Lifesciences, Koninklijke Philips, GE HealthCare Technologies Inc., Getinge AB, Baxter International Inc., LiDCO Group, ICU Medical Inc., Drägerwerk AG & Co. KGaA, Mindray Medical International, Nihon Kohden Corporation, Siemens Healthineers, Medtronic plc, Becton Dickinson (BD), Terumo Corporation, Abbott Laboratories, Schiller AG, Deltex Medical Group, Pulsion Medical Systems (Maquet/Getinge subsidiary), Osypka Medical GmbH, CNSystems Medizintechnik GmbH |

Frequently Asked Questions

The integration of wireless and wearable hemodynamic monitoring devices into telehealth ecosystems is creating new opportunities for personalized, real-time patient management at home.

Home care settings are the fastest-growing with CAGR of 8.89%, supported by remote monitoring technologies and rising chronic disease management outside hospitals.

ICU/CCU remains the largest application segment, accounting for 39.29% of the market, due to high demand for continuous monitoring in critical care.

Software & data analytics, including AI-driven platforms, is the fastest-growing, with a CAGR of 7.81%, reflecting the digital transformation of healthcare.

Non-invasive devices are projected to lead with market share of 35.68%, driven by patient comfort, reduced infection risk, and integration with telehealth platforms

Get in Touch