Hemostasis Products Market Report Scope & Overview:

The Hemostasis Products Market size is estimated at USD 1.94 Billion in 2025 and is expected to reach USD 3.28 Billion by 2035 and grow at a CAGR of 5.41% over the forecast period of 2026–2035.

The global hemostasis products market analysis report provides comprehensive insights into market dynamics, product innovation, and clinical adoption trends. Rising surgical volumes, increasing trauma cases, advancements in minimally invasive procedures, and growing demand for effective bleeding control solutions are driving market growth during 2026–2035.

Hemostasis Product usage surpassed 320 million units in 2025, driven by rising surgical volumes and increasing adoption of advanced bleeding control solutions.

Market Size and Forecast:

-

Market Size in 2025: USD 1.94 Billion

-

Market Size by 2035: USD 3.28 Billion

-

CAGR: 5.41% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Hemostasis Products Market - Request Free Sample Report

Hemostasis Products Market Trends:

-

Rising number of surgical and minimally invasive procedures is increasing demand for effective bleeding control solutions.

-

Growing trauma cases and emergency care admissions are accelerating adoption of fast-acting hemostatic products.

-

Increased preference for topical, flowable, and bioactive hemostats is improving surgical efficiency and outcomes.

-

Advancements in biomaterials, sealants, and absorbable matrices are enhancing product performance and safety.

-

Expansion of ambulatory surgical centers is driving demand for easy-to-use and cost-effective hemostasis solutions.

-

Strategic partnerships between medical device manufacturers and healthcare providers are supporting innovation and market expansion.

U.S. Hemostasis Products Market Insights:

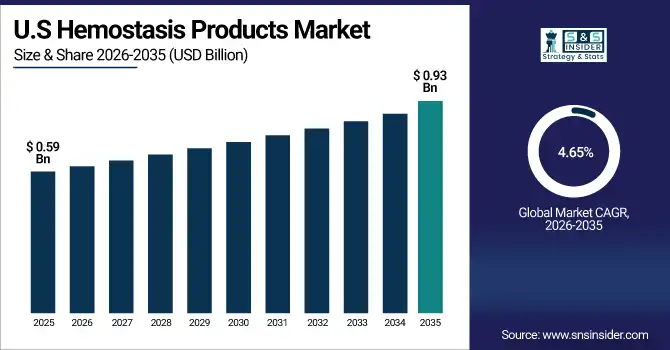

The U.S. Hemostasis Products Market is projected to grow from USD 0.59 Billion in 2025 to USD 0.93 Billion by 2035, at a CAGR of 4.65%. Growth is driven by rising surgical volumes, increasing trauma cases, adoption of advanced topical and flowable hemostats, and investments in minimally invasive procedures and hospital bleeding control solutions.

Hemostasis Products Market Growth Drivers:

-

Rising surgical volumes and trauma cases driving demand for effective and rapid bleeding control solutions.

Rising surgical volumes and increasing trauma cases are key drivers of Hemostasis Products Market growth. Hospitals and ambulatory surgical centers are adopting advanced topical, flowable, and sealant-based hemostatic solutions to control bleeding, reduce procedure time, and improve patient outcomes. Growth in minimally invasive and complex surgeries further increases demand for fast-acting, easy-to-use products. Expansion of emergency care infrastructure and continuous innovation in biomaterials, absorbable matrices, and bioactive sealants are enhancing clinical effectiveness and supporting sustained market growth.

Over 58% of hospitals and ambulatory surgical centers adopted advanced hemostatic products in 2025 to improve surgical bleeding control.

Hemostasis Products Market Restraints:

-

High costs of advanced hemostatic products and limited reimbursement coverage are restraining widespread market adoption.

High costs of advanced hemostatic products and limited reimbursement coverage remain key restraints for the Hemostasis Products Market. Premium topical agents, flowable matrices, and bioactive sealants increase procedural costs, limiting adoption among small and mid-sized hospitals and clinics. In many regions, inconsistent reimbursement policies discourage routine use, especially for elective procedures. Additionally, budget constraints, procurement challenges, and the need for clinician training on newer products further restrict widespread adoption, slowing market penetration despite growing surgical demand.

Hemostasis Products Market Opportunities:

-

Rising demand for minimally invasive surgeries and advanced bleeding control solutions presents significant market growth opportunities.

Rising demand for minimally invasive surgeries and advanced bleeding control solutions presents significant opportunities for the Hemostasis Products Market. Hospitals, ambulatory surgical centers, and clinics are increasingly adopting topical, flowable, and sealant-based hemostats to improve surgical efficiency, reduce blood loss, and enhance patient outcomes. Manufacturers offering innovative, easy-to-use, and cost-effective products can capitalize on this trend. Continuous advancements in biomaterials, absorbable matrices, and bioactive sealants enable broader adoption across surgical and emergency care settings.

Over 47% of hospitals and surgical centers adopted topical and flowable hemostatic products in 2025, driven by increasing trauma cases and surgical volumes.

Hemostasis Products Market Segmentation Analysis:

-

By Product Type, Topical Hemostats held the largest market share of 35.48% in 2025, while Flowable Hemostats are expected to grow at the fastest CAGR of 6.12% during 2026–2035.

-

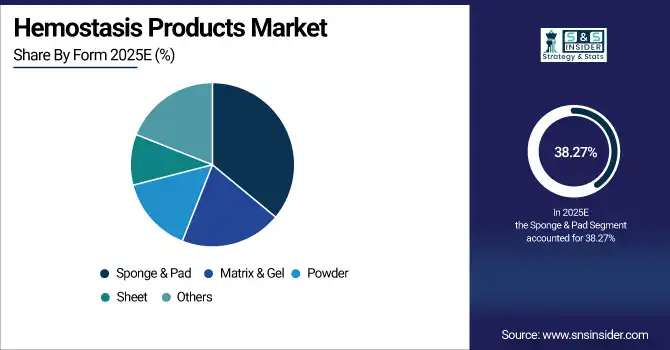

By Form, Sponge & Pad accounted for the highest market share of 38.27% in 2025, while Matrix & Gel is projected to record the fastest CAGR of 6.45% through 2026–2035.

-

By Application, Surgical Procedures dominated with a 42.13% share in 2025, while Trauma Care is expected to expand at the fastest CAGR of 6.03% during the forecast period.

-

By End-User, Hospitals held the largest share of 48.56% in 2025, while Ambulatory Surgical Centers are anticipated to grow at the fastest CAGR of 6.21% through 2026–2035.

By Product Type, Topical Hemostats Dominate While Flowable Hemostats Grow Rapidly:

Topical Hemostats segment dominated the market due to its ease of use, proven effectiveness in controlling surgical bleeding, and wide availability across hospitals and surgical centers. In 2025, usage of topical hemostats exceeded 115 million units, reflecting strong adoption in general, cardiovascular, and orthopedic surgeries.

Flowable Hemostats is the fastest-growing segment, driven by increasing demand for minimally invasive and complex procedures requiring precise bleeding control. Flowable products’ adaptability in irregular surgical sites accelerated adoption, with usage surpassing 72 million units in 2025, especially in trauma and laparoscopic surgeries.

By Form, Sponge & Pad Dominates While Matrix & Gel Grows Rapidly:

Sponge & Pad segment dominated the market due to its versatility, cost-effectiveness, and suitability for a wide range of surgical procedures. Its high absorption capacity and ease of application enhance surgical efficiency. In 2025, over 123 million units of sponge and pad hemostats were deployed, primarily in hospitals and ambulatory centers.

Matrix & Gel is the fastest-growing segment, driven by innovations in absorbable biomaterials and enhanced hemostatic efficacy. Surgeons increasingly prefer gels and matrices for complex or minimally invasive procedures. Usage of matrix & gel products reached 67 million units in 2025, highlighting rapid clinical adoption.

By Application, Surgical Procedures Dominate While Trauma Care Grows Rapidly:

Surgical Procedures segment dominated the market due to the sheer volume of elective, cardiovascular, orthopedic, and general surgeries. Rising surgical demand and aging population further boost growth. In 2025, hemostatic products were used in over 135 million surgical procedures, reflecting widespread hospital adoption.

Trauma Care is the fastest-growing segment, fueled by rising emergency surgeries, accidents, and battlefield or disaster care needs. Adoption of advanced hemostatic solutions in trauma settings reached 58 million cases in 2025, particularly in emergency rooms and trauma centers, driving segmental growth.

By End-User, Hospitals Dominate While Ambulatory Surgical Centers Grow Rapidly:

Hospitals segment dominated the market due to high surgical volumes, emergency care capabilities, and robust procurement budgets, ensuring consistent adoption of advanced hemostatic solutions. In 2025, hospitals accounted for over 160 million units of hemostatic products, representing the majority of total usage.

Ambulatory Surgical Centers (ASCs) are the fastest-growing segment, driven by rising outpatient procedures, minimally invasive surgeries, and demand for quick bleeding control solutions. ASCs adopted over 69 million units in 2025, reflecting rapid expansion and increasing investments in advanced hemostatic products.

Hemostasis Products Market Regional Analysis:

North America Hemostasis Products Market Insights:

The North America Hemostasis Products Market is dominated, holding a 41.62% share in 2025, driven by high surgical volumes and advanced hospital infrastructure across the U.S. and Canada. Strong adoption of topical, flowable, and sealant-based hemostats in hospitals and ambulatory surgical centers fuels growth. Rising trauma cases, minimally invasive procedures, and investments in innovative bleeding control solutions further support market expansion. Advanced clinician training, robust procurement budgets, and supportive healthcare policies reinforce North America’s leadership in this mature market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Hemostasis Products Market Insights:

The U.S. Hemostasis Products Market is strongly driven by high surgical volumes, advanced hospital infrastructure, and widespread adoption of topical, flowable, and sealant-based hemostats. Increasing demand for minimally invasive procedures, trauma care, and emergency bleeding management, coupled with investments in innovative biomaterials and clinician training, reinforces the U.S. as the dominant market in North America.

Asia-Pacific Hemostasis Products Market Insights:

The Asia-Pacific Hemostasis Products Market is the fastest-growing region, projected to expand at a CAGR of 6.63% during 2026–2035. Growth is driven by rising surgical volumes, increasing trauma cases, and expanding healthcare infrastructure across China, India, Japan, and Southeast Asia. Adoption of advanced topical, flowable, and sealant-based hemostats, investments in minimally invasive procedures, and improving hospital and ambulatory surgical center capabilities are accelerating product uptake and strengthening Asia-Pacific’s dynamic market growth.

China Hemostasis Products Market Insights:

The China Hemostasis Products Market is driven by rising surgical volumes, increasing trauma cases, and expanding hospital infrastructure. Rapid adoption of advanced topical, flowable, and sealant-based hemostats, growing investments in minimally invasive procedures, and strengthening emergency care capabilities are accelerating product uptake, positioning China as a key contributor to Asia-Pacific market growth.

Europe Hemostasis Products Market Insights:

The Europe Hemostasis Products Market is driven by increasing surgical volumes, advanced hospital infrastructure, and investments in minimally invasive procedures. Countries such as Germany, France, and the UK are shaping regional demand through widespread adoption of topical, flowable, and sealant-based hemostats. Expansion of ambulatory surgical centers, emergency care facilities, and strong regulatory support for surgical safety are boosting product adoption. Continuous innovations in biomaterials and clinician training are reinforcing Europe’s significance in the hemostasis products market.

Germany Hemostasis Products Market Insights:

Germany is a key market in the European Hemostasis Products landscape, driven by advanced hospital infrastructure and high surgical volumes. Growth is supported by widespread adoption of topical, flowable, and sealant-based hemostats, investments in minimally invasive procedures, and strong regulatory focus on surgical safety, clinician training, and procedural efficiency.

Latin America Hemostasis Products Market Insights:

The Latin America Hemostasis Products Market is growing due to rising surgical volumes and expanding healthcare infrastructure. Adoption is supported by increasing use of topical, flowable, and sealant-based hemostats across Brazil, Mexico, and Argentina, with investments in minimally invasive procedures, emergency care, and clinician training driving regional market growth.

Middle East and Africa Hemostasis Products Market Insights:

The Middle East & Africa Hemostasis Products Market is expanding due to increasing surgical procedures and improving healthcare infrastructure. Rising adoption of topical, flowable, and sealant-based hemostats in hospitals and surgical centers is driving demand, with Saudi Arabia, the UAE, and South Africa emerging as key regional markets.

Hemostasis Products Market Competitive Landscape:

Johnson & Johnson, through its Ethicon division, is a leader in the hemostasis products market, offering widely used surgical hemostats and sealants such as SURGICEL and VISTASEAL. Ethicon dominates due to its high-quality, reliable products for controlling bleeding in surgical, trauma, and minimally invasive procedures. Extensive distribution, continuous R&D investment, regulatory approvals, and strategic acquisitions expand its biosurgery portfolio. Innovations in hemostatic technologies and integration with comprehensive surgical solutions reinforce Ethicon’s leadership and market presence.

-

In June 2025, Ethicon launched the ETHICON 4000 Stapler with 3D Staple Technology and enhanced Gripping Surface, improving tissue compression, reducing bleeding, and supporting open, laparoscopic, and future robotic surgeries.

Baxter International Inc., headquartered in the U.S., is a leading player in the hemostasis products market, offering gelatin-based and thrombin-based hemostats through its Advanced Surgery division. The company’s products improve surgical performance, reduce intraoperative bleeding, and enhance patient outcomes. Baxter’s broad distribution across more than 100 countries ensures strong accessibility in developed and emerging markets. Strategic R&D investments and acquisitions expand its product portfolio, while a focus on clinical efficacy and innovation strengthens its market dominance and competitive position.

-

In April 2025, Baxter introduced the Hemopatch Sealing Hemostat with room-temperature storage, enabling rapid bleeding control and tissue sealing in open and minimally invasive surgeries, improving OR efficiency and accessibility, supporting faster patient recovery times.

B. Braun Melsungen AG, headquartered in Germany, is a major medical device company with a strong presence in the hemostasis products market. Its portfolio includes surgical and trauma care hemostats designed for efficiency and patient safety. B. Braun leverages manufacturing and distribution networks to serve over 60 countries. Its long-standing reputation, commitment to quality, and continuous product innovation in absorbable and specialty hemostats support market leadership. Strategic expansion in emerging regions further reinforces B. Braun’s position and growth potential.

-

In July 2025, B. Braun expanded its hemostatic and related medical portfolio by launching an expanded Heparin Sodium Premixed Injection product line, adding new high‑dose formulations to its heparin offering and enhancing bleeding management support in surgical and catheter care settings across the U.S. market.

Hemostasis Products Market Key Players:

Some of the Hemostasis Products Companies are:

-

Johnson & Johnson (Ethicon)

-

Baxter International Inc.

-

B. Braun Melsungen AG

-

Becton, Dickinson and Company (BD)

-

Medtronic plc

-

Pfizer Inc.

-

CSL Behring

-

CryoLife, Inc.

-

Integra LifeSciences Corporation

-

Abbott Laboratories

-

Grifols, S.A.

-

Teleflex Incorporated

-

Advanced Medical Solutions Group plc

-

Stago Group

-

Sysmex Corporation

-

Zimmer Biomet Holdings, Inc.

-

Marine Polymer Technologies, Inc.

-

Hemostasis LLC

-

Arch Therapeutics, Inc.

-

Pfm Medical, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.94 Billion |

| Market Size by 2035 | USD 3.28 Billion |

| CAGR | CAGR of 5.41% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Topical Hemostats, Mechanical Hemostats, Flowable Hemostats, Adhesive & Sealants) • By Form (Matrix & Gel, Sponge & Pad, Powder, Sheet, Others) • By Application (Surgical Procedures, Trauma Care, Wound Management, Dental Procedures, Others) • By End-User (Hospitals, Ambulatory Surgical Centers, Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Johnson & Johnson (Ethicon), Baxter International Inc., B. Braun Melsungen AG, Becton, Dickinson and Company (BD), Medtronic plc, Pfizer Inc., CSL Behring, CryoLife, Inc., Integra LifeSciences Corporation, Abbott Laboratories, Grifols, S.A., Teleflex Incorporated, Advanced Medical Solutions Group plc, Stago Group, Sysmex Corporation, Zimmer Biomet Holdings, Inc., Marine Polymer Technologies, Inc., Hemostasis LLC, Arch Therapeutics, Inc., Pfm Medical, Inc. |

Frequently Asked Questions

North America dominated with a 41.62% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 6.63% during 2026–2035.

Topical Hemostats dominated with a 35.48% share in 2025, while Flowable Hemostats are projected to grow at the fastest CAGR of 6.12% during 2026–2035.

Growth is driven by rising surgical volumes, increasing trauma cases, demand for minimally invasive procedures, and adoption of advanced bleeding control solutions.

The market is valued at USD 1.94 Billion in 2025 and is projected to reach USD 3.28 Billion by 2035.

The Hemostasis Products Market is expected to grow at a CAGR of 5.41% during 2026–2035.

Get in Touch