Herbicides Market Report Scope & Overview:

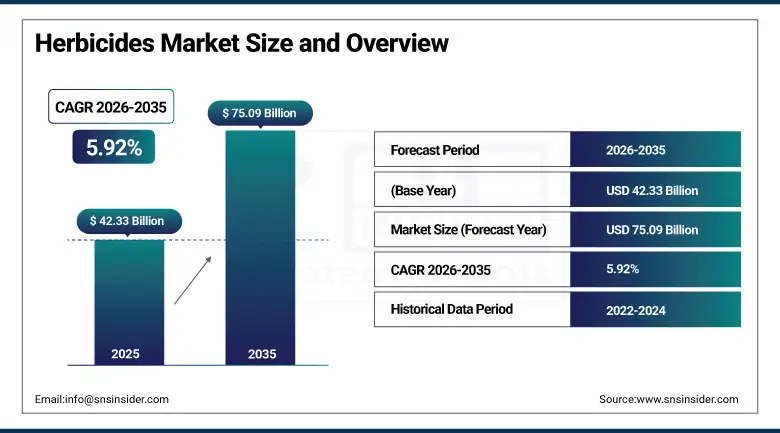

The Herbicides Market was valued at USD 42.33 Billion in 2025 and is expected to reach USD 75.09 Billion by 2035, growing at a CAGR of 5.92% from 2026–2035.

Herbicides are products used in agriculture to kill or manage weeds competing against crops for sunlight, water, nutrients, and growth space. The importance of herbicides cannot be overstated in agriculture since they help in limiting losses caused by weeds and ensuring that there is increased production. Herbicides find applications in cereals, oilseeds, fruit and vegetable plants, among other agricultural plants where weeds might be difficult to remove using physical labor. They can either be non-selective or selective, or they can be pre-emergence or post-emergence. Increasing demands for food and farm mechanization are key factors promoting their use around the world.

In May 2025, FMC Corporation and Bayer partnered to commercialise Isoflex herbicide across 30 million hectares of winter cereals in the European Union, combining FMC's Isoflex formulations with Bayer's registration and distribution capabilities to address the difficult weed challenges including blackgrass and ryegrass resistance that European cereal growers face with declining chemical options as regulatory restrictions reduce the available herbicide modes of action.

Market Size and Forecast

-

Market Size in 2026E: USD 44.83 Billion

-

Market Size by 2035: USD 75.09 Billion

-

CAGR: 5.92% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Herbicides Market - Request Free Sample Report

Herbicides Market Trends

-

Growing herbicide-resistant weed populations are increasing demand for new herbicide chemistries and novel modes of action to maintain effective weed control

-

Bio-herbicide development is expanding through plant-based and microbial solutions that support sustainable agriculture and organic farming practices

-

Precision spraying technologies using AI and smart sensors are improving herbicide application efficiency while reducing chemical usage and environmental impact

-

Rising adoption of herbicide-tolerant genetically modified crops is creating additional demand for compatible broad-spectrum herbicide products

-

Increasing use of pre-harvest desiccation herbicides is helping growers optimize harvest timing, improve crop management, and reduce post-harvest processing costs

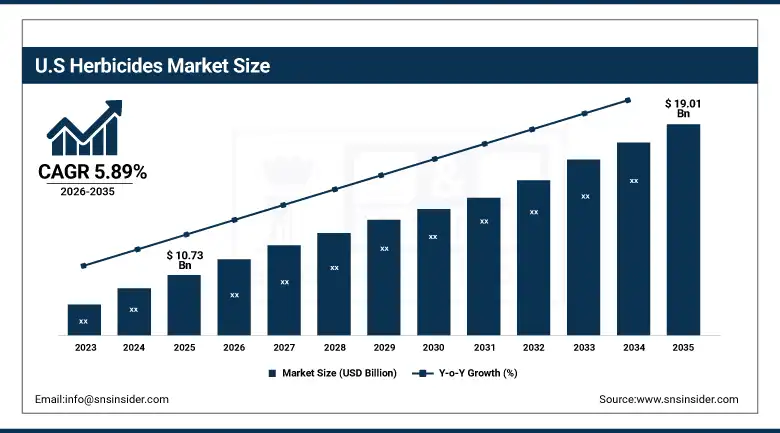

U.S. Herbicides Market Outlook

The U.S. Herbicides Market was valued at approximately USD 10.73 Billion in 2025 and is expected to reach approximately USD 19.01 Billion by 2035, growing at a CAGR of approximately 5.89%.

The United States herbicides market is anchored by the glyphosate-tolerant soybean and corn systems whose Roundup Ready trait adoption across approximately 90% of domestic soybean acreage and 90% of corn acreage creates a structurally large annual glyphosate procurement base that sustains market volume despite pricing pressure from generic glyphosate competition. The commercial challenge of managing glyphosate-resistant Palmer amaranth, waterhemp, and ryegrass populations across major corn and soybean growing regions is creating above-trend demand for alternative and complementary herbicide modes of action including dicamba, 2,4-D, isoxaflutole, and new HPPD inhibitor formulations whose commercial success in managing resistant weed populations sustains premium herbicide product revenue growth above the generic glyphosate price base.

In March 2025, Syngenta acquired Novartis's repository of natural compounds and genetic strains for agricultural use, while establishing a biologicals production facility in Orangeburg, South Carolina, to serve the Americas market for biological alternatives to glyphosate and other synthetic herbicides.

Herbicides Market Segment Analysis

-

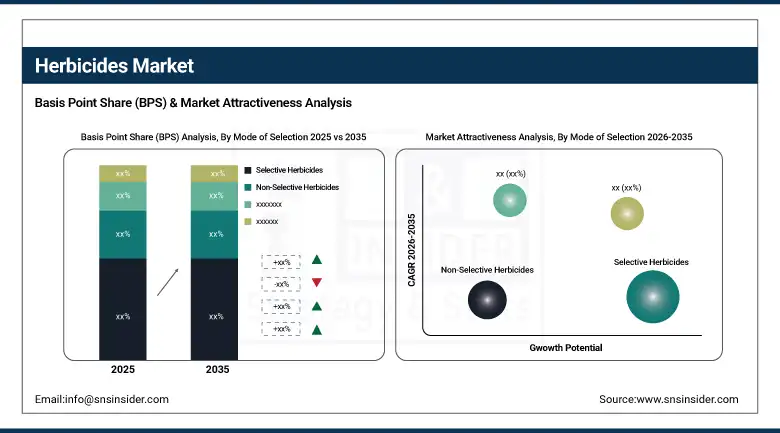

By Mode of Selection, the Selective Herbicides segment dominated the Herbicides Market with approximately 65.3% share in 2025, while the Non-Selective Herbicides segment is the fastest growing.

-

By Type, the Glyphosate segment dominated the Herbicides Market with approximately 29.5% share in 2025, while the Bio-herbicides segment is the fastest growing.

-

By Mode of Application, the Foliar Spray segment dominated the Herbicides Market with approximately 48.2% share in 2025, while the Soil Treatment segment is the fastest growing.

-

By Crop Type, the Cereals & Grains segment dominated the Herbicides Market with approximately 41.8% share in 2025, while the Fruits & Vegetables segment is the fastest growing.

By Mode of Selection, selective herbicides dominate, bioherbicides grow fastest

The Selective Herbicides segment captured about 65.3% of the herbicides market share in 2025 owing to the efficient weed suppression while ensuring the crop remains healthy in cereals, oilseeds, and row crops. The herbicides offer farmers flexibility in managing the post-emergence of weeds in various crops. They are extensively utilized in the agriculture industry because of their efficacy in crop management. This wide use continues to drive growth in the segment and ensures dominance in the market.

The Non-Selective Herbicides segment is one of the fastest-growing segments in the herbicides market. This segment growth is attributed to the increased usage in no-tillage farming, burndown herbicide applications before planting, industrial vegetation management, and herbicide-tolerant crops. The herbicides have broad-spectrum activity on grass, broadleaves, and sedges. The rising shortage of labor, expansion in conservation agriculture, and weed suppression requirements drive demand for this product type in the global market.

By Crop Type, cereals & grains dominate, fruits & vegetables grow fastest

The Cereals & Grains remained the leading segment in the herbicides market during 2025 on account of the widespread cultivation of wheat, corn, rice, barley, and sorghum across the world. The cultivation of these major cereal grains occupies maximum area in terms of agriculture across the world; therefore, herbicides continue to be used extensively in this segment owing to the recurring demand of such agricultural products. Moreover, the increasing incidence of herbicide resistance issues is prompting farmers to employ improved weed management practices, which ensures continued consumption of herbicides in this segment.

The Fruits & Vegetables accounted for the fastest growth rate in the herbicides market because of the increase in global consumption and demand for fresh produce alongside the development of high value agriculture. Fruit and vegetable crops are significantly susceptible to weed competition, hence, effective weed management is crucial for yield performance, as well as for ensuring the appearance and quality of produce. Rising urbanization trends along with shifting consumer preferences towards healthier diets are contributing towards the increased use of herbicides in this segment. In addition, the exports-oriented approach of fruit & vegetable production is also boosting the usage of herbicides in this segment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

Egypt |

22.8% |

|

Latin America |

Brazil |

44.2% |

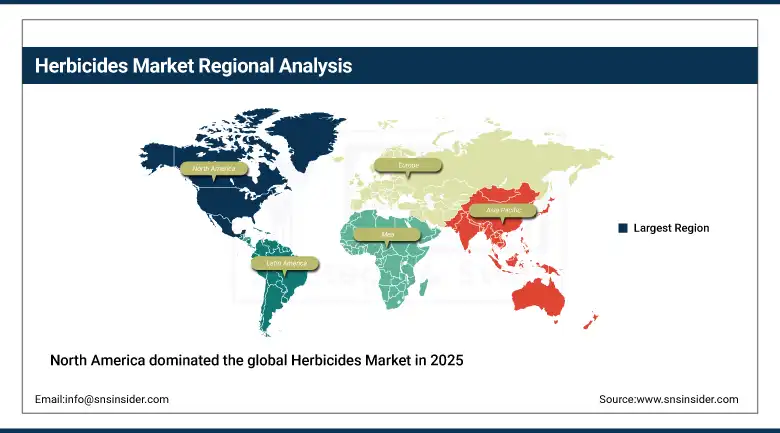

North America Herbicides Market Insights

North America dominated the global Herbicides Market in 2025, accounting for the largest regional share. The United States accounts for approximately 82.5% of North American revenues through the world's most intensive glyphosate-tolerant GM crop system whose soybean, corn, and cotton herbicide programmes create the highest per-country herbicide consumption globally. The structural shift toward herbicide-resistant weed management in U.S. row crops is creating sustained premium herbicide product demand as glyphosate performance decline in resistant weed populations motivates adoption of supplementary herbicide modes of action at higher per-unit pricing than generic glyphosate. Canada contributes supplementary demand through its canola, wheat, and pulse crop herbicide markets and the growing canola acreage whose pre-harvest desiccation requirements create specific herbicide procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Herbicides Market Insights

Europe held a significant share of the global Herbicides Market in 2025. France, Germany, Ukraine, the United Kingdom, and Spain are the leading national markets whose extensive cereal, oilseed, and sugar beet production creates consistent and technically sophisticated herbicide demand. Germany accounts for approximately 28.5% of European revenues through its large cereal and oilseed crop acreage, the commercial presence of BASF and Bayer whose European headquarters sustain product development and regulatory engagement for European market registration, and the increasingly complex weed management challenges from blackgrass, brome grass, and waterhemp resistance that are creating premium herbicide investment in resistant weed management programmes.

The European Commission's Farm to Fork strategy whose pesticide use reduction targets, the EU's revision of the Sustainable Use of Pesticides Directive, and the progressive active ingredient re-evaluation that is restricting or withdrawing several herbicide registrations are creating a regulatory-driven market restructuring that is simultaneously reducing generic product availability and creating premium opportunities for novel herbicide modes of action and bio-herbicide alternatives whose regulatory profile meets the tightening standards that EU approval requires.

Asia Pacific Herbicides Market Insights

Asia Pacific is the fastest-growing regional Herbicides Market, driven by the intensification of rice, wheat, and soybean production across China, India, Vietnam, and Indonesia whose adoption of mechanised harvesting and direct seeding systems creates herbicide adoption at rates that transplanted and manually weeded traditional cultivation practices did not require.

China accounts for approximately 38.5% of Asia Pacific revenues as both the world's largest herbicide manufacturing country and a major consumption market whose rice, corn, and wheat acreage requires systematic weed management at scale. India is growing fastest within the region where government food security programmes are promoting adoption of weed management technology in rice and wheat cultivation systems.

Southeast Asian markets including Vietnam, Thailand, and Indonesia are experiencing accelerating herbicide adoption as mechanised rice cultivation requiring herbicide-based weed management replaces traditional transplanted paddy cultivation, and as palm oil and rubber plantation expansion creates non-crop vegetation management demand. Japan and South Korea contribute premium regional demand through their high-value rice and horticulture herbicide markets.

MEA & Latin America Herbicides Market Insights

Egypt leads MEA revenues at approximately 22.8% of the regional total through its extensive cotton, wheat, and vegetable production whose herbicide programmes are growing with farming intensification and expanding cultivated area under irrigation expansion programmes. South Africa, Morocco, and Kenya contribute growing regional demand through their commercial agricultural sectors whose herbicide adoption is increasing with farm mechanisation.

Brazil leads Latin American revenues at approximately 44.2% of the regional total as the world's largest soybean producer whose glyphosate-tolerant GMO system creates the most extensive single-crop herbicide consumption programme outside the United States. Brazil's annual soybean acreage expansion into the Cerrado and MATOPIBA regions creates consistent new herbicide procurement as each hectare brought into production requires initial weed management investment. Argentina, Paraguay, and Uruguay contribute substantial regional demand through their soybean and corn herbicide programmes aligned with South American GM crop adoption.

Market Dynamics

Growth Drivers: Expanding global food demand requiring intensive weed management and herbicide-resistant weed population proliferation

A significant growth in the market of herbicides is observed due to growing needs of global food demand as a result of population growth, urbanization, and dietary changes. With population growth, agricultural producers are expected to be more efficient in the process of growing crops and obtain as much yield as possible from their current cultivated land. Weed management is an important part of agriculture since weed growths may substantially decrease crop yields and agricultural efficiency. As a result, herbicides will become the most important crop protection measure for farmers.

Moreover, a significant growth in the number of weeds that are not sensitive to existing herbicides serves as a driver for the development of the market. The need to develop new ways of combating these weeds results in the implementation of more advanced weed management practices such as combination and rotation of herbicide modes of action. Such developments will positively contribute to further growth in the market.

Restraints: Regulatory scrutiny of key herbicide active ingredients and herbicide resistance development reducing efficacy of established product chemistry

The herbicides market faces significant challenges from increasingly stringent regulatory scrutiny of widely used active ingredients such as glyphosate, atrazine, and 2,4-D. Regulatory agencies across major agricultural markets are conducting extensive safety and environmental reviews, leading to usage restrictions, registration delays, and, in some cases, product withdrawals. These developments create uncertainty for manufacturers and growers while increasing the cost and complexity of bringing new herbicide products to market.

Another major restraint is the growing prevalence of herbicide-resistant weeds. Continuous use of the same herbicide modes of action has accelerated the development of resistant weed populations, reducing product effectiveness and increasing weed management costs. As resistance spreads, growers must adopt more complex and expensive control strategies, while manufacturers face increasing pressure to develop innovative herbicide chemistries and resistance management solutions.

Opportunities: Precision spot-spray technology dramatically reducing herbicide application volumes and bio-herbicide innovation

Technologies for precision herbicide application are among the main opportunities within the herbicides market. Sophisticated technologies involving the use of artificial intelligence, machine vision, and weed detection in real time make it possible to spray herbicides only in those places where weeds can be found, which makes it possible to cut down the use of chemicals significantly without any loss of effectiveness of weed suppression. This trend promotes cost-effectiveness, efficient herbicide application, and sustainability goals.

The other area with considerable potential in the herbicides market is associated with bio-herbicides and other sustainable weed control solutions. The rising need for sustainable products, growing cultivation of organic crops, and increased regulation of traditional herbicides give a good basis for developing alternative biological solutions. The innovation in this area can contribute to market opportunities and resistance management in agriculture.

Recent Developments:

-

2025: FMC Corporation and Bayer partnered to commercialise Isoflex herbicide across 30 million hectares of European winter cereals, combining FMC's novel mode of action formulations with Bayer's registration and distribution network to address blackgrass and ryegrass resistance management in European cereal production.

-

2025: Syngenta acquired Novartis's repository of natural compounds and genetic strains for agricultural biologicals and established a biologicals production facility in Orangeburg, South Carolina, advancing its strategy of building biological herbicide alternatives to complement its synthetic herbicide portfolio.

-

2023: BASF launched Luximo herbicide containing the new mode of action active ingredient isoxaflutole in combination with thiencarbazone-methyl for broad-spectrum weed management in European corn production, addressing the weed control challenges created by progressive restriction of atrazine and other established corn herbicide options.

Herbicides Market Key Players

-

Bayer AG

-

BASF SE

-

Syngenta AG (ChemChina)

-

Corteva Agriscience

-

FMC Corporation

-

UPL Ltd.

-

Adama Agricultural Solutions Ltd. (ChemChina)

-

Nufarm Ltd.

-

Sumitomo Chemical Co. Ltd.

-

Arysta LifeScience (UPL)

-

Nichino America Inc.

-

American Vanguard Corporation

-

Albaugh LLC

-

Sipcam Oxon SpA

-

Sapec Agro SA

-

Helena Chemical Company

-

Drexel Chemical Company

-

Wilbur-Ellis Holdings Inc.

-

Wynca Group (Hangzhou Wynca Chemical)

-

Rainbow Chemical Co. Ltd.

Herbicides Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 42.33 Billion |

| Market Size by 2035 | USD 75.09 Billion |

| CAGR | CAGR of 5.92% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Mode of Selection (Selective Herbicides, Non-Selective Herbicides) • By Type (Glyphosate, Atrazine, 2,4-D, Acetochlor, Glufosinate, Bio-herbicides, Others) • By Mode of Application (Foliar Spray, Soil Treatment, Seed Treatment, Others) • By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Bayer AG, BASF SE, Syngenta AG (ChemChina), Corteva Agriscience, FMC Corporation UPL Ltd., Adama Agricultural Solutions Ltd. (ChemChina), Nufarm Ltd., Sumitomo Chemical Co. Ltd., Arysta LifeScience (UPL), Nichino America Inc., American Vanguard Corporation, Albaugh LLC, Sipcam Oxon SpA, Sapec Agro SA, Helena Chemical Company, Drexel Chemical Company, Wilbur-Ellis Holdings Inc., Wynca Group (Hangzhou Wynca Chemical), Rainbow Chemical Co. Ltd. |

Frequently Asked Questions

The Herbicides Market is expected to grow at a CAGR of 5.92% from 2026 to 2035.

The Herbicides Market was valued at USD 42.33 Billion in 2025.

Global food demand growth, increasing herbicide-resistant weeds, expanding herbicide-tolerant GM crop adoption, precision spraying technology advancements.

The Selective Herbicides segment dominated the Herbicides Market with approximately 65.3% share in 2025.

North America dominated the Herbicides Market in 2025 with the largest regional share..

Get in Touch