Home Healthcare Services Market Report Scope & Overview

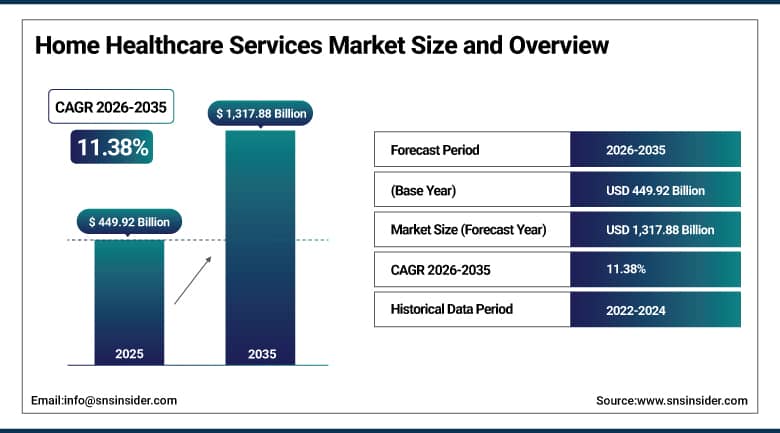

The Home Healthcare Services Market was valued at USD 449.92 Billion in 2025 and is expected to reach USD 1,317.88 Billion by 2035, growing at a CAGR of 11.38% from 2026 to 2035.

There is a structural change in decentralized provision of care that is growing the market. The drivers include the increasing prevalence of chronic diseases, ageing populations and a growing preference for in-home clinical and post-acute care services. Digital health platforms are enabling healthcare providers to add remote patient monitoring, home-based skilled nursing and rehabilitation services. Cost efficiency over hospital-based treatment and better patient outcomes are driving adoption across developed and emerging healthcare systems.

During the month of March 2024, due to the increase in expansion of hospital-at-home payment schemes as well as increased utilization of remote patient monitoring technology by care networks, there was an observed 28 percent growth in utilization of home-based acute care services among the American healthcare facilities.

Market Size and Forecast:

-

Market Size in 2026E: USD 499.59 Billion

-

Market Size by 2035: USD 1,317.88 Billion

-

CAGR: 11.38% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Home Healthcare Services Market - Request Free Sample Report

Market Trends:

-

Expansion of integrated acute care delivery frameworks across health systems to enable hospital-at-home models.

-

Integration of remote patient monitoring devices into standard chronic disease management and post-discharge pathways of care.

-

Increased use of telehealth-enabled home care platforms for continuing physician-patient interaction and care coordination.

-

Deployment of skilled home nursing services for long-term elderly and post-surgical patient management programmers.

-

Greater use of digital health ecosystems that bring together wearables, cloud-based records and AI-assisted care monitoring systems.

U.S. Home Healthcare Services Market Outlook:

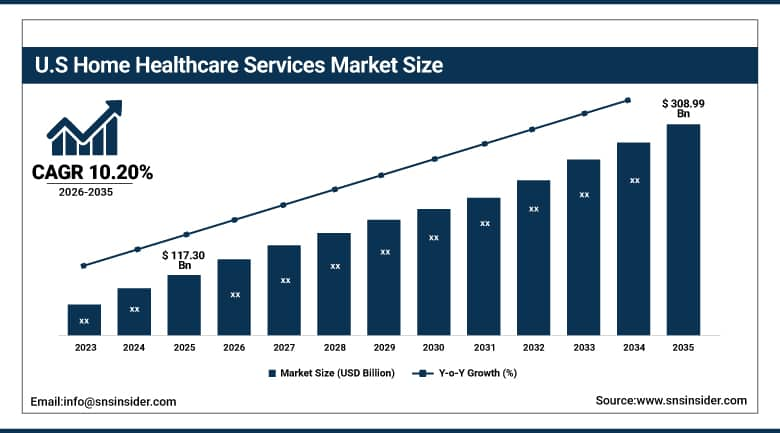

The U.S. Home Healthcare Services Market was valued at USD 117.30 Billion in 2025 and is expected to reach USD 308.99 Billion by 2035, growing at a CAGR of 10.20% from 2026 to 2035.

Preference for clinical management at home rather than long hospital stays, increasing burden of chronic diseases and shift towards value-based care models are some of the key factors driving the growth of the market. Healthcare systems are seeing improvements in the delivery of post-acute care through the use of hospital-at-home programmers, remote patient monitoring, skilled nursing services and digital health platforms. Increasing prevalence of chronic diseases and an ageing population are further accelerating the adoption of home-based care solutions in the U.S. healthcare landscape.

In February 2025, expansion of Medicare-supported hospital-at-home reimbursement frameworks and wider deployment of remote patient monitoring across integrated care networks led to a 31% rise in home-based acute care admissions across major U.S. hospital systems, improving care continuity and reducing inpatient bed occupancy rates.

Home Healthcare Services Market Segment Analysis:

-

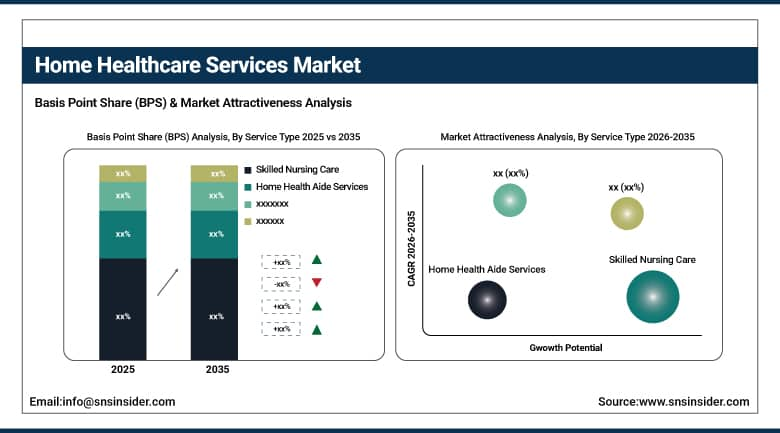

By Service Type, Skilled Nursing Care dominated the Home Healthcare Services Market with 36.50% share in 2025, while Remote/Telehealth-enabled Home Health Aide Services are the fastest growing segment from 2026 to 2035.

-

By Service Model, In-home Care dominated the Home Healthcare Services Market with 52.00% share in 2025, while Hospital-at-Home Services are the fastest growing segment from 2026 to 2035.

-

By Patient Type, Elderly Population dominated the Home Healthcare Services Market with 58.00% share in 2025, while Chronic Disease Patients are the fastest growing segment from 2026 to 2035.

-

By Payment Mode, Public Insurance dominated the Home Healthcare Services Market with 49.00% share in 2025, while Out-of-pocket payments are the fastest growing segment from 2026 to 2035.

By Service Type, skilled nursing care dominates, remote/telehealth-enabled home health aide services grow fastest

In 2025, the Home Healthcare Services Market’s dominant revenue share was held by skilled nursing care, which is expected to reach about 36.50% owing to its vital role in post-acute care management, chronic disease monitoring, wound care, medication administration, and rehabilitation support provided directly in the homes of patients. This segment is supported by robust hospital discharge procedures, ageing population dependence and clinical need for licensed nursing oversight in complex medical cases. Skilled nursing care delivered in home-based settings gained prominence across both developed and emerging healthcare systems due to mounting pressure on hospital beds and cost containment initiatives.

Home health aides assisted through remote health and telemedicine are the fastest-growing segment between 2026 and 2035, owing to the rapid adoption of digital health care, remote patient monitoring, and advanced healthcare coordination platforms using AI. The development in wearables, Internet-of-things-based health care solutions, and remote nursing supervision is making it possible for semi-skilled home health care providers to provide structured care with constant clinical supervision. Health care service providers are focusing on hybrid home health care delivery through a combination of physical and remote care, which can be delivered at lower costs per patient.

By Service Model, in-home care dominates, hospital-at-home services grow fastest

The in-house care service delivery was the most dominant service delivery type, holding around 52.00% of the market share due to the existing infrastructure and wide acceptance by patients in various settings such as the elderly, rehabilitation centers, and treatment for long-term illness conditions. The in-house service delivery remains at the center of home healthcare services since it is flexible, inexpensive relative to institutionalization, and offers continuous support for medical and non-medical support for the patients. Availability of caregivers and association with the primary healthcare system made the service more popular in urban areas.

The hospital-at-home care service is one of the fastest growing segments between 2026 and 2035 due to the increasing instances of hospital congestion, adoption of value-based healthcare and development of portable diagnostic and therapeutic technologies. Hospital-at-home is a method of delivering acute level care, such as intravenous administration, oxygen support and surgical aftercare, in patients’ homes while being monitored from a hospital setting. Top healthcare providers are expanding hospital-at-home services to improve patient health outcomes in a cost-efficient way. Insurance payment schemes and digital patient monitoring solutions help in the process.

By Patient Type, elderly population dominates, chronic disease patients grow fastest

In 2025, elderly patients represented the largest Home Healthcare Services market share of 58.00%. This is because of an ageing population base and increasing life expectancy with many elderly people experiencing health conditions related to age. Elderly patients require constant support for movement, medication compliance, surgical after-care and monitoring of underlying health conditions. An increase in the number of facilities for elderly patients and government initiatives for elder care has significantly increased the demand.

The chronic disease patient segment is expected to be the fastest growing segment during the forecast period 2026-2035. The growth of this segment is being driven by the increasing prevalence of diabetes, cardiovascular diseases, respiratory disorders, and renal conditions globally, which need long-term management. Technologies for continuous monitoring, home-based diagnostic tools and care plans enabled by telehealth are permitting effective management of diseases outside the hospital setting. Healthcare systems are increasingly shifting to preventive and constant care models to reduce hospital readmissions and long-term treatment costs. Insurance companies and health systems are also expanding chronic care management programmers, driving adoption of home-based treatment and monitoring solutions at a rapid pace.

By Payment Mode, public insurance dominates, out-of-pocket payments grow fastest

Public insurance held the leading market share of around 49.00% within the Home Healthcare Services Market in 2025, owing to its backing from health insurance provided under government-run healthcare systems, growing insurance cover for senior healthcare, and home-based medical services reimbursement programs. Such an offering is favored due to well-defined national health programs and social security schemes providing financial support for such requirements in cases involving senior patients or patients suffering from chronic ailments.

The fastest growing segment from 2026 to 2035 is out-of-pocket payments. The growth is attributed to the increasing middle-class income levels, growing demand for premium personalized homecare services, and gaps in insurance coverage for certain non-critical care services. Patients are choosing personalized care services, sophisticated home monitoring systems and rapid response medical assistance, which are not fully covered by public schemes. Moreover, the growing private health care spending and rising awareness of health care in urban areas are also increasing direct consumer spending. The trend reflects a broader shift towards personalized care models where patients place a higher value on convenience, quality and speed of service than on reimbursement dependency.

Regional Analysis:

North America Home Healthcare Services Market Insights

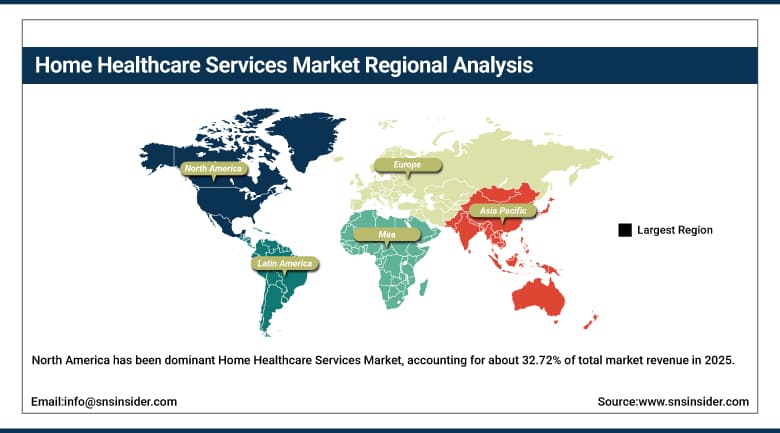

North America has been dominant within the Global Home Healthcare Services Market, accounting for about 32.72% of total market revenue in 2025. This is attributed to its superior healthcare delivery infrastructure, extensive adoption of advanced health technology, strong insurance penetration, and developed ecosystem for delivering home healthcare services. Increased cost pressures within hospitals and push towards the home care delivery models further aid in establishing a stronghold of North America in the market.

United States has a share of about 82.5% within North America in 2025 due to the presence of extensive Medicare schemes and insurance reimbursement framework for skilled nursing, telehealth and hospital at home programs. Extensive penetration of remote monitoring and integration in healthcare networks facilitates adoption in the country. Publicly funded healthcare in Canada increases the share of North America, along with Mexico, where adoption is on the rise from private healthcare service providers.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Home Healthcare Services Market Insights

The Europe held the largest share of the Home Healthcare Services Market in 2025, with a share of 30.40% due to the strong public healthcare systems, ageing demographic trends, and widespread adoption of community-based care models. The region will profit from the development of structured policies for long-term care, a high degree of access to healthcare, and the growing incorporation of digital monitoring solutions in eldercare and chronic disease management systems.

With a strong nursing workforce, vast healthcare infrastructure, and significant investment in home-based clinical care services, Germany’s market share of around 22.4% is the highest in the regional market. Other key contributors include France, Italy and the Nordic countries where government supported elderly care schemes and policies to de-congest hospitals are fueling demand for homecare. The UK also has a crucial role to play through NHS supported home treatment pathways and digital health transformation initiatives across primary care systems

Asia Pacific Home Healthcare Services Market Insights

The Asia Pacific region is the fastest growing regional market and is expected to grow at a CAGR of 12.86%. The region held approximately 28.69% share of the global Home Healthcare Services Market in 2025. Growth is attributed to rapid urbanization, rising access to healthcare, growing burden of chronic diseases and increasing adoption of cost-effective home-based care solutions across emerging economies.

China is the leading contributor to the regional market with a share of nearly 44.8%, due to its large elderly population and increasing digital health ecosystem including telemedicine and remote monitoring platforms, as well as rising healthcare infrastructure. Japan and South Korea have made a significant contribution in the form of advanced geriatric care systems and high adoption of medical robotics and smart homecare technologies. India is fast becoming a high growth market supported by expanding private healthcare networks, rising medical expenditure and fast digital health adoption that enables scalable home healthcare delivery models.

Middle East & Africa & Latin America Home Healthcare Services Market Insights

According to the statistics available, the Middle East & Africa accounted for an estimated 3.38% share in the global Home Healthcare Services Market in 2025 owing to the slow but steady process of modernizing their healthcare facilities, increased cases of chronic diseases, and the development of non-hospital care settings through initiatives taken by their governments.

As per the estimates, the country dominating the regional market is the United Arab Emirates accounting for about 22.8% of the total market share due to its advanced healthcare system, widespread insurance coverage, and the availability of hospital at home concept. The rapid growth can be seen in Saudi Arabia owing to the introduction of reforms in their healthcare systems according to their Vision 2030 strategy.

Market Dynamics:

Growth Drivers: Expanding shift toward decentralized care delivery and rising demand for cost-efficient home-based healthcare systems

One of the key growth drivers of the Home Healthcare Services Market is the increasing shift away from hospital-based, towards decentralized, home-based healthcare delivery systems. This shift is well supported by increasing healthcare spending, hospital overcrowding and rising demand for cost-efficient long-term care solutions for ageing populations and chronic disease patients. Governments and private healthcare providers are aggressively advocating for homecare integration into larger healthcare ecosystems to reduce inpatient burden and improve patient outcomes.

Another key component is the expansion of digital health infrastructure, such as telehealth platforms, remote patient monitoring tools, and AI-enabled care coordination systems. Over 70% of healthcare providers in developed economies now employ hybrid care models that mix physical home visits with virtual monitoring. Wearable health technologies, cloud-based medical records and real-time diagnostics dramatically increase clinical efficiency. Further acceleration of global market penetration is achieved through large-scale expansion of insurance reimbursement for home-based services.

Restraints: Workforce shortages and high operational complexity limiting scalable home healthcare service expansion

One of the prime restraints in Home Healthcare Services Market is the increasing shortage of skilled healthcare professionals such as nurses, physiotherapists, and trained carers. This labor gap is causing bottlenecks in operations, especially in regions where the population is ageing rapidly and there is a growing need for chronic care. The labor-intensive nature of homecare service delivery makes services expensive, and limits providers’ ability to efficiently scale across geographies.

Another challenge is the high operational complexity of coordinating distributed delivery of care. Homecare, as opposed to institutional healthcare settings, needs distributed logistics, real-time communication systems and tailored patient management plans. Regional regulatory fragmentation and inconsistent reimbursement frameworks further complicate service standardization. Moreover, cybersecurity risks associated with remote monitoring systems and the sharing of patient data create additional compliance and infrastructure burdens for providers.

Opportunities: Digital health integration and hospital-at-home expansion creating scalable next-generation care models

One of the key opportunities in the Home Healthcare Services Market is the rapid expansion of hospital-at-home programmers which provide acute-level care in residential settings. These models are increasingly adopted by healthcare systems to decrease the costs of inpatient, increase the recovery rate of patients, and better utilize hospital beds. Advanced portable diagnostic equipment, mobile imaging systems and remote clinical monitoring technologies are enabling complex treatments to be safely and effectively delivered outside hospitals.

Another major opportunity is the deep integration of digital health ecosystems including AI-driven predictive analytics, IoT-enabled patient monitoring and automated care coordination platforms. These technologies are making care more efficient by enabling disease detection early and continuous monitoring of patients. Providers are also investing big in hybrid care networks that combine in-person carers with telehealth oversight. We anticipate the convergence of healthcare with digital infrastructure will drastically enhance scalability, reduce costs and improve access to home-based medical services globally.

Recent Developments:

-

In March 2025, Amedisys Inc. expanded its Medicare-certified home health and hospice network across the U.S., strengthening post-acute care capacity amid rising demand for hospital-to-home transition services and value-based care models.

-

In February 2025, BAYADA Home Health Care implemented workforce restructuring and operational optimization initiatives to manage rising caregiver costs and reimbursement pressure while continuing to expand skilled nursing and pediatric home care services.

-

In January 2025, Addus HomeCare Corporation reported continued expansion in personal care and hospice services across key U.S. states, supported by improved Medicaid reimbursement rates and increasing demand for long-term elderly care solutions.

Home Healthcare Services Market Key Players are:

-

Amedisys Inc.

-

BAYADA Home Health Care

-

Addus HomeCare Corporation

-

Enhabit Inc.

-

AccentCare Inc.

-

Interim HealthCare Inc.

-

Elara Caring

-

BrightSpring Health Services

-

VITAS Healthcare

-

Visiting Nurse Service of New York (VNS Health)

-

Home Instead (Honor Technology)

-

Comfort Keepers

-

Right at Home

-

Brookdale Senior Living (Home Health Division)

-

Trinity Health At Home

-

Genesis Healthcare

-

Maxim Healthcare Services

-

LHC Group (Optum – still operational brand)

-

CareCentrix Inc.

-

MedStar Health Home Care

Home Healthcare Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 449.92 Billion |

| Market Size by 2035 | USD 1,317.88 Billion |

| CAGR | CAGR of 11.38% From 2025 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Skilled Nursing Care, Physical Therapy, Occupational Therapy, Speech Therapy, Medical Social Services, Home Health Aide Services) • By Service Model (In-home Care, Remote Patient Monitoring, Hospital-at-Home Services, Telehealth-enabled Services) • By Patient Type (Elderly Population, Chronic Disease Patients, Post-surgical Patients, Disabled Patients) • By Payment Mode (Public Insurance, Private Insurance, Out-of-pocket) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Amedisys Inc., BAYADA Home Health Care, Addus HomeCare Corporation, Enhabit Inc., AccentCare Inc., Interim HealthCare Inc., Elara Caring, BrightSpring Health Services, VITAS Healthcare, VNS Health, Home Instead, Comfort Keepers, Right at Home, Brookdale Senior Living, Trinity Health At Home, Genesis Healthcare, Maxim Healthcare Services, LHC Group, CareCentrix Inc., and MedStar Health Home Care. |

Frequently Asked Questions

The Home Healthcare Services Market is expected to grow at a CAGR of 11.38% during the forecast period.

The Home Healthcare Services Market was valued at approximately USD 449.92 Billion in 2025.

The major factor driving the Home Healthcare Services Market is the rapid shift toward cost-effective, hospital-to-home decentralized care driven by aging populations and rising chronic disease burden.

Skilled nursing care dominated the market in 2025.

North America dominated the Home Healthcare Services Market in 2025.

Get in Touch