HVAC Filters Market Report Scope & Overview:

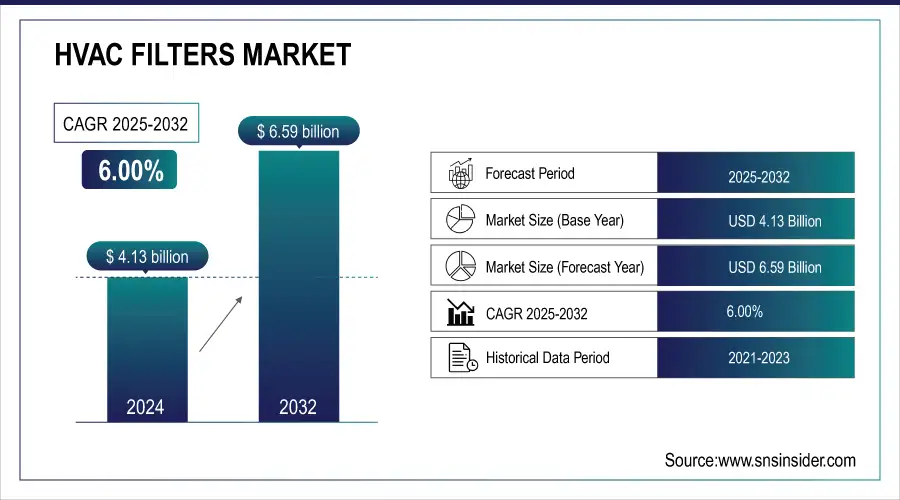

The HVAC Filters Market size was valued at USD 4.13 billion in 2024 and is expected to reach USD 6.59 billion by 2032 and grow at a CAGR of 6.00% over the forecast period of 2025-2032.

HVAC filters are an important part of any heating, ventilation, and air conditioning system because they remove foreign particles from the air. Indoor air quality (IAQ) is kept up by using these filters to filter out pollen, dust, and chemical pollutants in enclosed spaces. Few HVAC filters are very good at catching around 99.97% of particles up to 0.3 microns in size. Also, HVAC filters keep pollutants from getting into HVAC equipment, which makes it less likely that large foreign particles will damage the equipment. For instance, in 2023, the China Department for Housing and Urban Development announced plans to begin investing heavily in new urban housing projects in the coming decade. As a part of these new investments, builders, and engineers will require advanced HVAC systems and filters to help the new urban development reach their modern energy efficiency standards. This trend is visible in the activities of the key industry players. In 2023, Daikin Industries announced plans to expand the production capacity of their HVAC component factor in India, which the company believes will help compensate for the drop in demand for automotive filters and also ensure uninterrupted delivery of HVAC systems and filters to the market.

Get More Information on HVAC Filters Market - Request Sample Report

Key HVAC Filters Market Trends

-

Growing adoption of high-efficiency filters (HEPA, MERV 13+) to improve indoor air quality in residential and commercial spaces.

-

Rising demand for smart and IoT-enabled HVAC filters with real-time monitoring and predictive maintenance features.

-

Shift towards sustainable and eco-friendly filter materials, including recyclable and low-emission options.

-

Expansion of HVAC filter usage in healthcare, pharma, and cleanroom applications due to stricter air quality regulations.

-

Increasing replacement demand driven by awareness of health risks from airborne pollutants, allergens, and viruses.

-

Integration of HVAC filters in green building certifications (LEED, WELL) boosting premium filter adoption.

HVAC Filters Market Growth Drivers

-

Rising demand for the HAVC system drives the market growth.

One of the most significant drivers of market growth is the increasing demand for HVAC systems. It is a critical factor because the HVAC filters usually belong to HVAC systems. As urbanization continues developing and residents of most countries get the possibility to incur their living standards, the interest in premium indoor climate control environments in residential, commercial, and industrial buildings grows. The reasons for such a significant increase in demand can be identified as a growing interest in improving air quality, requirements related to energy-efficient buildings, and the fact that the construction sector has been developing significantly. When it comes to energy efficiency, filters can be discussed as a tool that can help in immense filtration in HVAC systems to contribute to the energy-saving process. Without these filters, the amounts of energy and time used for maintenance practices will have to increase. Moreover, the construction sector is also one of the leading consumers. As new buildings and existing ones are equipped with HVAC devices, the filters for these devices are also needed. Thus, the drivers are significant, and the market is growing because the need for the product is increasing significantly.In the United States, the Department of Energy reported that HVAC systems account for about 48% of the energy use in a typical U.S. home, making energy efficiency in HVAC systems a critical focus. This has led to increased adoption of energy-efficient HVAC systems and the need for advanced filters that support these systems.

HVAC Filters Market Restraints

-

High Preliminary Costs may hamper the market growth.

High initial costs associated with advanced HVAC filters can significantly hamper market growth. These filters, designed to offer superior air quality and energy efficiency, often come with a price tag that is considerably higher than standard filters. For businesses and homeowners, the upfront investment in these high-performance filters can be a deterrent, particularly in regions where cost considerations are a primary concern. This is especially true in emerging markets, where the focus may be on affordability rather than advanced features.

HVAC Filters Market Segment Outlook:

By Material

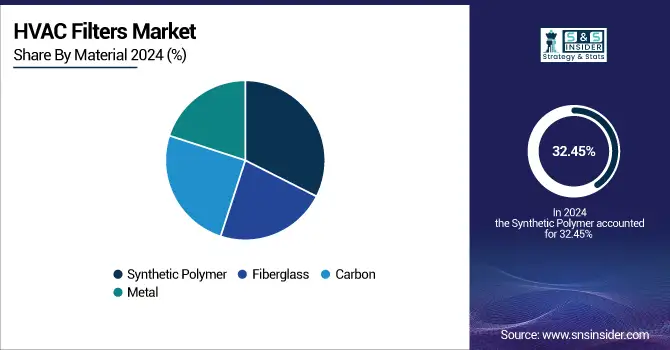

The synthetic polymer segment held the largest market share around 32.45% in 2023. Synthetic polymers, such as polyester and polypropylene, stand as the leading material in the HVAC filters market. The material is often favored for its versatility, durability, and affordability. Not only do these filters have high levels of filtration efficiency, but they are also light and easy to manufacture. The reactors typically take place over limited times, with the polymers cooling quickly. This allows for the particles to undergo a readily controlled crystallization process with aggregates that undertake variation above 140o. The high manufacturability rate, as such, also contributes to the low costs associated with this material. On top of that, many synthetic polymer filters are also reusable and washable, which appeals to commercial offices and homes alike. High expenditure associated with the maintenance of HVAC systems in commercial buildings is noted to be an issue, and as such, the lower replacement costs can provide value.

By Technology

High-Efficiency Particulate Air filtration is leading among the technologies used in HVAC filters. HEPA filters are renowned for their exceptional ability to capture particles as small as 0.3 microns with an efficiency of 99.97%, making them the gold standard in air filtration. This technology is widely used in environments where air quality is critical, such as hospitals, laboratories, and cleanrooms, as well as in residential and commercial HVAC systems where reducing allergens, pollutants, and airborne pathogens is a priority.

By End-Use Industry

The building & construction industry held the largest market share in the HVAC filters market by end-use industry around 43.45% in 2023. This dominance is driven by the widespread application of HVAC systems in residential, commercial, and industrial buildings, where air quality and energy efficiency are critical. As urbanization accelerates, particularly in emerging economies, the demand for new buildings outfitted with advanced HVAC systems continues to grow, leading to increased consumption of HVAC filters. Additionally, regulations and standards related to indoor air quality and energy efficiency, such as those enforced by the U.S. Environmental Protection Agency (EPA) and the European Union's Energy Performance of Buildings Directive (EPBD), have made it mandatory for buildings to integrate high-efficiency filtration systems.

HVAC Filters Market Regional Analysis

Asia Pacific HVAC Filters Market Insights

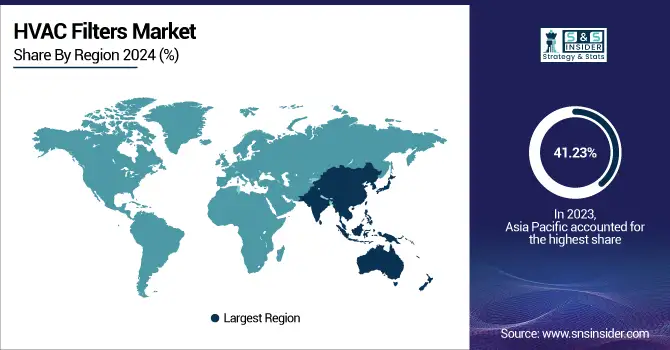

Asia Pacific held the largest market share with around 41.23% in 2023. The region's booming construction industry, particularly in countries like China, India, and Southeast Asian nations, is a major driver. For instance, China's government, under its 14th Five-Year Plan (2021-2025), is heavily investing in green and smart building projects, leading to a surge in demand for advanced HVAC systems and filters. Similarly, India's Smart Cities Mission, which aims to develop 100 smart cities, is driving the adoption of energy-efficient HVAC systems equipped with high-performance filters.

Moreover, government regulations focused on improving air quality are also propelling market growth. In 2020, the Chinese government introduced the "Blue Sky" initiative, which mandates stricter air pollution controls in urban areas, directly boosting the demand for high-efficiency HVAC filters. Additionally, Japan's focus on energy efficiency, supported by subsidies for green buildings, has further accelerated the adoption of advanced HVAC systems.

North America HVAC Filters Market Insights

North America, in 2024, is leading the HVAC filters market which is directed by the strict indoor air quality (IAQ) regulation with high penetration of energy efficient construction wall systems within the region deriving high residential and commercial market. Overall, the U.S. is the most developed market in the region, with a diversified installation base in commercial offices, healthcare and industrial plants, whereas Canada is gradually picking up pace over the years due to the imposition of green building regulations. Rising health awareness coupled with the need to minimize air pollutants will propel the market.

Europe HVAC Filters Market Insights

Europe HVAC filters industry is poised to grow significantly by 2024 driven by stringent rules adopted by EU regarding air quality, carbon emissions, and energy consumption. Leading companies among these include those in Germany, the U.K., and France as the demand for advanced filtration products in commercial buildings, hospitals, and manufacturing plants continues to increase. Retrofitting in older structures and the region’s focus on sustainable and green HVAC systems also contribute to the market.

Latin America (LATAM) HVAC Filters Market Insights

The Latin America HVAC filters industry is growing on account of growing urbanization, infrastructure development and industrialization which is auguring well for clean indoor air solutions. The leading and growing markets are Brazil and Mexico which are experiencing increasing construction activity and exposure to health and comfort standards in residential and commercial segments. Market up-take is growing with increasing investment in modern building systems and programs to improve air quality – the cost sensitivity of the market is however still a barrier to wider adoption.

Middle East & Africa (MEA) HVAC Filters Market Insights

MEA market trends in 2024 Climatic extremes, construction of high-rises and airports boost demand for HVAC/HEPA filters in MEA Rise in HVAC filters demand across the MEA region has been increasingly influenced by climatic conditions, a slew of massive infrastructural projets as well as need for more commercial properties, hospitals and airport facilities. Saudi Arabia, the UAE and South Africa are key contributors, with government efforts targeted at energy efficiency and indoor air quality standards. The growing number of smart city projects and growing penetration of air conditioning systems are also driving the market growth in the region.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Competitive Landscape for HVAC Filters Market:

3M Company

3M is a diversified global technology company recognized for its expertise in filtration, adhesives, and advanced materials. Within the HVAC Filters segment, the company focuses on developing innovative solutions that enhance indoor air quality, energy efficiency, and sustainability for both residential and commercial applications.

-

In 2024: 3M introduced a new line of high-efficiency HVAC filters designed to improve air quality and energy efficiency in commercial and residential applications. These filters incorporate advanced electrostatic technology to capture finer particles and allergens.

Honeywell International Inc.

Honeywell is a global leader in technology and manufacturing, offering solutions in aerospace, building technologies, performance materials, and safety products. In the HVAC Filters segment, the company provides advanced air filtration systems aimed at improving health, comfort, and operational efficiency across residential, commercial, and industrial sectors.

- In 2024, Honeywell acquired a leading manufacturer of high-performance HVAC filters to enhance its product portfolio and expand its market presence. This strategic acquisition bolsters Honeywell’s capabilities in delivering advanced filtration solutions and supports its long-term growth in the HVAC industry.

HVAC Filters Companies are:

- Filtration Group Corporation

- Ahlstrom-Munksjö

- 3M Company

- MANN+HUMMEL

- Parker-Hannifin Corporation

- Sogefi Group

- American Air Filter Company, Inc.

- Camfil AB

- Donaldson Company, Inc.,

- Freudenberg Group

- Daikin Industries, Ltd.

- Lennox International Inc.

- Trane Technologies plc

- Carrier Global Corporation

- Johnson Controls International plc

- LG Electronics Inc.

- Sharp Corporation

- Samsung Electronics Co., Ltd.

- Atlas Copco AB

- Nederman Holding AB

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | US$ 4.13 Billion |

| Market Size by 2032 | US$ 6.59 Billion |

| CAGR | CAGR of 6.00% From 2024 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Fiberglass, Synthetic Polymer, Carbon, Metal) • By Technology (Electrostatic Precipitator, Activated Carbon, UV Filtration, HEPA Filtration, Ionic Filtration) • By End-Use Industry (Building & Construction, Pharmaceutical, Food & Beverage, Automotive, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | Filtration Group Corporation, Ahlstrom-Munksjö, 3M Company, Mann+Hummel, Parker-Hannifin Corporation, Sogefi Group, American Air Filter Company, Inc., Camfil AB, Donaldson Company, Inc., Freudenberg Group |

Frequently Asked Questions

Ans: HVAC Filters Market Size was valued at USD 4.13 billion in 2024, and expected to reach USD 6.59 billion by 2032, and grow at a CAGR of 6.00% over the forecast period 2025-2032.

Ans: More people want HVAC systems, Indoor Air Quality Is Getting More Attention and Government rules and policies for filtering that works well are the drivers for HVAC Filters Market.

Ans: The most common way for COVID-19 to spread is from person to person. Social distance is an important way to stop the spread of COVID-19, but respiratory droplets can still infect other people through a building's HVAC system even if social distance is taken. In a recent survey by Air Conditioning, Heating and Refrigeration (ACHR) Magazine to find out how COVID-19 is affecting the industry, more than half of the people who answered said "business is slowing down" or "business has dropped off a lot."

Ans: Primary or secondary type of research done by this reports.

Ans: Manufacturers, Consultant, aftermarket players, association, Research institute, private and universities libraries, suppliers and distributors of the product.

Get in Touch