Hydrogen Turbine Retrofits Market Report Scope & Overview:

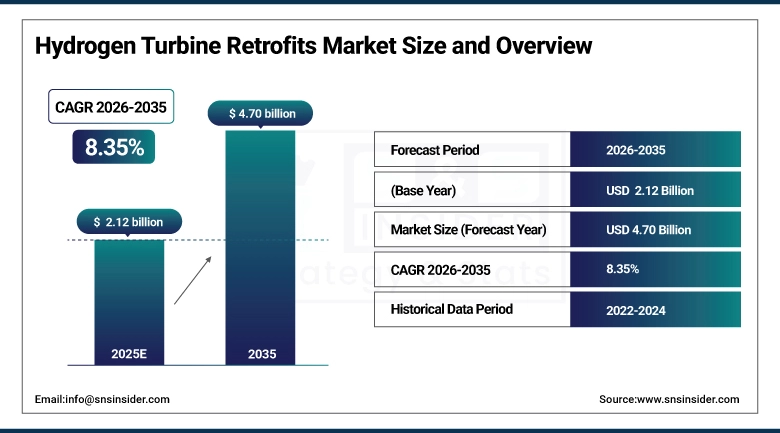

The Hydrogen Turbine Retrofits Market was valued at USD 2.12 billion in 2025 and is expected to reach USD 4.70 billion by 2035, growing at a CAGR of 8.35% from 2026-2035.

Factors such as rising global initiatives towards carbon emission reduction and cleaner energy transitions are driving the demand for hydrogen turbine retrofits market. Investments are being driven by increasing adoption of hydrogen as a clean fuel, encouraging government policies, and incentive for low-carbon technology. Sustainably, because retrofitting existing turbines is cheaper than a new installation, this allows utilities and industrial operators to increase efficiency, meet regulations, and deliver the increased quantity of energy with lower impact.

This trend is evident in California, where despite federal funding rollbacks, the Los Angeles Department of Water and Power is advancing an investment exceeding USD 800 million to retrofit the Scattergood Generating Station with hydrogen-ready turbines, underscoring the strong capital commitment toward hydrogen retrofit projects as part of long-term decarbonization strategies.

Hydrogen Turbine Retrofits Market Size and Growth:

-

Market Size in 2025: USD 2.12 Billion

-

Market Size by 2035: USD 4.70 Billion

-

CAGR: 8.35% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Hydrogen Turbine Retrofits Market - Request Free Sample Report

Hydrogen Turbine Retrofits Market Trends

-

Rising decarbonization goals and transition toward low-carbon power generation are driving the hydrogen turbine retrofits market.

-

Growing interest in repurposing existing gas turbines to run on hydrogen blends is boosting market growth.

-

Expansion of hydrogen infrastructure and green hydrogen production is fueling retrofit deployments.

-

Increasing focus on reducing CO₂ emissions while extending turbine asset life is shaping adoption trends.

-

Advancements in combustion systems, materials, and control technologies are enhancing hydrogen compatibility and safety.

-

Rising regulatory pressure and net-zero commitments are supporting market expansion.

-

Collaborations between turbine OEMs, energy utilities, and hydrogen technology providers are accelerating innovation and adoption.

U.S. Hydrogen Turbine Retrofits Market Size Outlook:

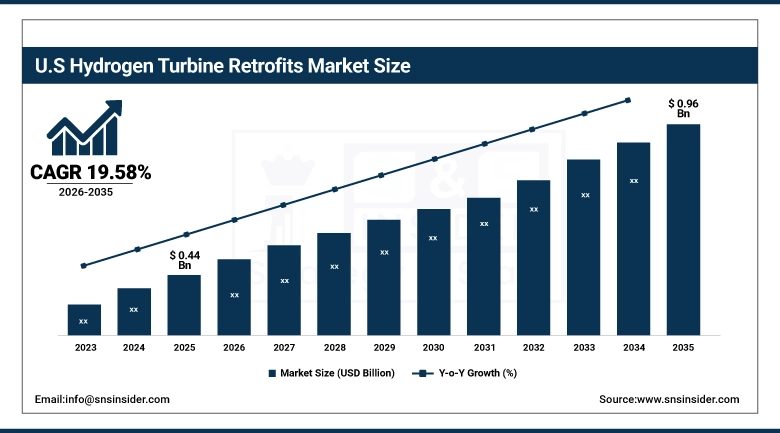

The U.S. Hydrogen Turbine Retrofits Market was valued at USD 0.44 billion in 2025 and is expected to reach USD 0.96 billion by 2035, growing at a CAGR of 7.98% from 2026-2035. The U.S. Hydrogen Turbine Retrofits Market as a result of governmental incentives, growing preference for clean hydrogen utilization and demand for lowering carbon emissions is propelling the growth of U.S. If existing turbines are retrofitted, such power generation will provide cost-effective and sustainable solutions for power generation and industrial applications.

Since 2021, DOE has committed approximately USD 147 million across multiple hydrogen turbine performance improvement initiatives, underscoring long-term policy and funding commitment.

Additional turbine-focused research funding includes USD 6.4 million awarded in September 2023 and earlier grants totaling USD 4.7 million in 2022 for advanced materials and turbine component development, supporting higher efficiency, lower emissions, and improved technical viability of hydrogen turbine retrofits.

Hydrogen Turbine Retrofits Market Growth Drivers:

-

Increasing global adoption of hydrogen fuel for turbines is driving demand for retrofitting existing turbine infrastructure efficiently and sustainably

Hydrogen-ready turbines are being adopted faster due to increasing global focus on clean energy and carbon neutrality. Retrofitting existing gas turbines for hydrogen blends or pure hydrogen combustion provides an opportunity for utilities and industrial players to newly achieve significant reductions in carbon emissions. This also encourages operational efficiency and extending turbines' longevity, but at the same time, reducing the need for entirely new installations. Moreover, all over the world, government incentives and supportive renewable energy policies also boost investments in hydrogen turbine retrofits. Retrofitting is viewed an economical option for industrial players to achieve sustainability targets and a means of staying ahead in a rapidly developing energy landscape.

This is further reinforced by U.S. Department of Energy supported projects that include the development of retrofittable dry low-emissions industrial gas turbine combustion systems capable of operating on 100% hydrogen or hydrogen natural gas blends.

Hydrogen Turbine Retrofits Market Restraints:

-

Limited hydrogen infrastructure and supply chain challenges are constraining the growth and deployment of retrofitted turbine solutions

Supply chain depends on hydrogen availability and distribution networks which are still at infancy stage in many parts of the world presenting considerable challenges in turbine retrofit project. Availability of hydrogen is vital for stable operations and since it is not produced in most regions or needs to be transported, will lead to reliance on imports, which may be more expensive. Moreover, hydrogen integration warrants mammoth planning and investments in storage, compression and safety. While hydrogen turbine retrofits help overcome existing limitations preventing large-scale adoption of hydrogen-based energy generation especially in emerging markets. Hydrogen supply inconsistency translates into project delays and low confidence among investors in retrofit market, imposing logistical and operational risks on the operators.

This uncertainty is reinforced by the International Energy Agency, which has significantly lowered its 2030 low-emissions hydrogen production outlook, citing project cancellations and slower infrastructure development, weakening confidence in scalable hydrogen supply chains.

Hydrogen Turbine Retrofits Market Opportunities:

-

Increasing global investment in renewable hydrogen production and technology innovations presents growth opportunities for turbine retrofits

The utilities and industrial operators have a reason to advocate for retrofit of old turbines for hydrogen as the green hydrogen production scales up. And new developments combustion technology, materials, and hybrid systems allow for cost-effective retrofits and drive technical improvements that make previously less attractive projects much more viable. The increasing partnerships between turbine players and hydrogen suppliers pave the across turnkey retrofitting solutions. Government incentives and programs targeting climate action also ensure the business case for retrofit projects. As hydrogen becomes increasingly accessible, and with continued technological advancements and favorable government policies, the market is well-situated for long-term growth as producers of energy transition seamlessly with minimal cost and emissions to a sustainable future in line with global decarbonization targets.

The U.S. Bipartisan Infrastructure Law has allocated USD 7 billion to develop regional hydrogen hubs that will create clean hydrogen supply chains foundational infrastructure that can feed hydrogen into turbines and support retrofit projects.

Hydrogen Turbine Retrofits Market Segment Highlights

-

By Technology, Partial Retrofit dominated the Hydrogen Turbine Retrofits Market with ~61% share in 2025; Full Retrofit fastest growing (CAGR).

-

By End-User, Utilities dominated the Hydrogen Turbine Retrofits Market with ~50% share in 2025; Industrial fastest growing (CAGR).

-

By Turbine Capacity, 100–300 MW dominated the Hydrogen Turbine Retrofits Market with ~48% share in 2025; Above 300 MW fastest growing (CAGR).

-

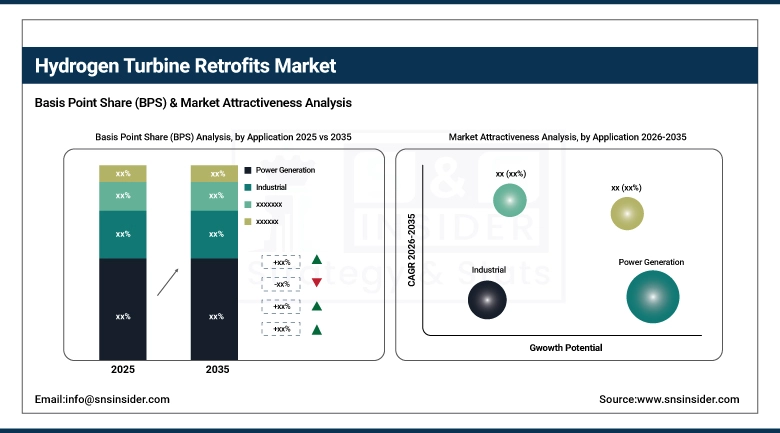

By Application, Power Generation dominated the Hydrogen Turbine Retrofits Market with ~65% share in 2025; Industrial fastest growing (CAGR).

By Application, Power Generation segment dominates the Market, Industrial segment expected to grow fastest

Power Generation segment dominated the Hydrogen Turbine Retrofits Market in 2025 as most of the retrofits are being performed in utility and commercial power plants. This means adapting turbines, providing flexibility so that the grid can continue to safely transition to hydrogen. Having an emphasis on low-carbon power supply, operational efficiency, and compliance with environmental regulations, the leading application for turbine retrofits is power generation.

Industrial segment is expected to grow at the fastest CAGR from 2026-2035 as industries target the decarbonization of their energy-intensive processes. Turbine hydrogen retrofits lower emissions and boost efficiencies, whilst meeting regulations. The key factors driving the retrofitted hydrogen turbine market size include the rapid adoption of these solutions by industrial operators to meet sustainability goals and enable cleaner energy integration.

By Technology, Partial Retrofit segment dominates the Market, Full Retrofit expected to grow fastest

Partial Retrofit segment dominated the Hydrogen Turbine Retrofits Market in 2025 owing to the economic viability of the approach with the least downtime. Partial retrofits can be implemented on existing turbines to enable hydrogen blends without major infrastructure modifications. Hence, it makes partial retrofits a way better option for operators who want a cost-effective solution to minimize carbon emissions without interrupting turbine operations and energy supply.

Full Retrofit segment is expected to grow at the fastest CAGR from 2026-2035 owing to rising hydrogen adoption and stringent emission regulations. It further supports the full retrofitting of turbines to run on higher percentages of hydrogen, making them more efficient and easier to comply with regulations. Utilities and industrial operators are making investments in full transformations to drive long-term viability, cleaner energy production, and compliance with decarbonization and climate targets.

By End-User, Utilities segment dominates the Market, Industrial segment expected to grow fastest

Utilities segment dominated the Hydrogen Turbine Retrofits Market in 2025 because large-scale power producers are primarily targeting on reducing their carbon emissions and comply with regulatory mandates. Utilities also like to replace old turbines to add hydrogen into the mix while using existing infrastructure. Utilities will be the largest end-users of hydrogen turbines for years because this approach provides consistent electricity supply, preserves profitability and meets international energy transition policies.

Industrial segment is expected to grow at the fastest CAGR from 2026-2035 due to increasing energy demand from the industrial sector and ongoing efforts for decarbonization. It is known that industries retrofitting turbines to hydrogen as a cleaner fuel. These upgrades assist in cutting down emissions, increasing operational efficiency, and complying with environmental regulations. More industrial players are seeking to deploy hydrogen for green energy and green ammonia for that benefit in the long term.

By Turbine Capacity, 100–300 MW segment dominates the Market, Above 300 MW expected to grow fastest

100–300 MW segment dominated the Hydrogen Turbine Retrofits Market in 2025 as this range of capacity is used in most of the mid-sized power plants. It is cost-effective to retrofit such a turbine, but also provides operational flexibility. This enables operators to adapt hydrogen blends optimally, all while keeping output and reliability. These capacity ranges are the sweet spot for cost-effective conversion of existing turbines to cleaner fuels.

Above 300 MW segment is expected to grow at the fastest CAGR from 2026-2035 owing to rising demand for large-scale low-carbon power generation. Plants with large capacities are upgrading the turbines to enable hydrogen operation for lower emissions and higher efficiency. Decarbonization trends & renewable integration will favour this segment, enable the development of large scale sustainable energy projects and long-term growth as well.

Hydrogen Turbine Retrofits Market Regional Analysis

Europe Hydrogen Turbine Retrofits Market Insights

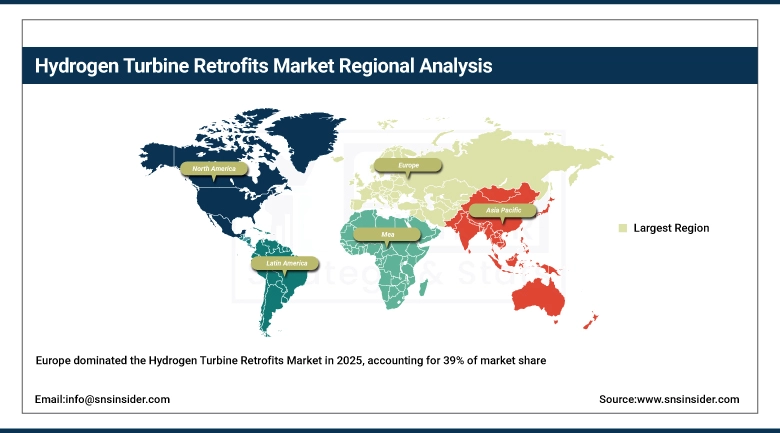

Europe dominated the Hydrogen Turbine Retrofits Market with the highest revenue share of about 39% in 2025 attributed to unwavering government backing for clean energy, stringent carbon emissions regulations, and highly advanced technological infrastructure. As a consequence, utilities and industrial operators are pouring billions of dollars into retrofitting existing turbines to hydrogen-ready systems that can help mitigate greenhouse gas emissions and meet aggressive climate targets. With well-established power networks and a highly skilled workforce, large-scale deployment is possible, which makes Europe the region of the world leading the way in hydrogen turbine retrofit adoption and implementation.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Hydrogen Turbine Retrofits Market Insights

Asia Pacific segment is expected to grow at the fastest CAGR of about 9.80% from 2026-2035 owing to the rapid industrialization, increasing energy demand, and an increasing adoption of hydrogen technologies. Increased investments in renewable energy, supportive government policies, and continued expansion of wind energy-related infrastructure promote turbine retrofitting. Also, deployment is being accelerated by cheap manufacturing, cross-border technology partnerships, and increasing environmental consciousness. This, along with sustainable development and economic growth, makes Asia Pacific the fastest growing hydrogen turbine retrofit market in the world.

North America Hydrogen Turbine Retrofits Market Insights

North America holds a significant position in the Hydrogen Turbine Retrofits Market owing to better technological infrastructure and strong initiatives towards the clean energy transition. As a solution to new regulations, hydrogen-ready turbines are being adopted by utilities and industrial operators to bring down carbon emissions. Ongoing investments in retrofitting existing gas turbines, supportive government policies & incentives for renewable energy, and the ability to maintain a leading position in hydrogen turbine retrofit deployment are maintaining the growth of the North America market.

Middle East & Africa and Latin America Hydrogen Turbine Retrofits Market Insights

Hydrogen Turbine Retrofits market in emerging economies of Middle East & Africa and Latin America is expected to witness significant growth due to increasing energy demand coupled with efforts for cleaner power generation. This helps for attracting investments in infrastructure for renewable energy and the government initiatives for promoting low carbon technologies urges retrofitting of turbines manufactured earlier. However, wide adoption of hydrogen-ready turbines is aided by international collaborations despite local manufacturing limitations. This steady rise in demand is further supported by increasing cognizance of sustainability as well as energy efficiency in these regions.

Hydrogen Turbine Retrofits Market Competitive Landscape:

Mitsubishi Power

Mitsubishi Power, a part of the Mitsubishi Heavy Industries group, is a premier engineer and manufacturer of power generation solutions, providing state-of-the-art gas and steam turbines, hydrogen-ready systems, and decarbonization technologies. It is specialized in the development of high-efficiency, low-emission turbines that can be operated on standard fuels and renewable hydrogen blends. Mitsubishi Power's Retrofit Solutions for Existing Assets and New Installations helps energy producers get to net-zero without the loss of reliability, operational flexibility and with scalable integration of hydrogen and other low-carbon fuels in power grids around the world.

-

2023: Mitsubishi Power operated its advanced class gas turbine with 30% hydrogen co-firing, achieving low NOx emissions and demonstrating feasibility for hydrogen fuel blending retrofits.

Ansaldo Energia

Ansaldo Energia is an Italian power generation company offering gas, steam, and hybrid turbine solutions with an emphasis on hydrogen-capable and flexible fuel systems. The company invests in both in-house R&D projects and external partnerships & EU-Funded projects to improve turbine fuel flexibility as well as retrofit existing asset for hydrogen operation. Ansaldo Energia emphasizes sequential combustion and advanced turbine technology to lower emissions, meet renewable fuel requirements, and facilitate the transition to net-zero electricity generation in a wide array of both industrial and utility applications globally.

-

2023: Ansaldo Energia launched FLEX4H2 project to develop hydrogen-fuel-flexible combustion systems, supporting retrofits for turbines capable of 0–100% hydrogen operation.

-

2024: FLEX4H2 project demonstrated Ansaldo’s GT36 gas turbine sequential combustion technology operating on 100% hydrogen fuel, marking a fuel-flexibility milestone for turbine retrofits.

Wärtsilä

As a leader in the field of smart energy solutions, Wärtsilä provides power plants, hybrid energy systems, and hydrogen-ready engines through the company and the world. They design technologies for low-carbon energy generation with a focus on flexibility, fuel switching and renewable energy integration. By prefitting its solutions for hydrogen, Wärtsilä also provides a transition pathway from natural gas to hydrogen, thus supporting net-zero trajectories, a more resilient grid, and scalable deployments of hydrogen. With its focus utility, industrial and islanded grids, it optimizes sustainable and efficient energy production and minimizes greenhouse gas emissions.

-

2024: Wärtsilä launched the world’s first large-scale hydrogen-ready engine power plant, capable of converting from natural gas to hydrogen to support net-zero decarbonisation.

GE Vernova (GE Power)

GE Vernova, the energy-focused subsidiary of GE, provided utility and industrial gas turbines, aeroderivative, and hydrogen power enablement solutions. Renewable fuels, turbine retrofits and zero-carbon products are the focus of the company. Hydrogen solutions from GE Vernova will allow for flexible fuel operations compatible with renewable electricity generation without compromising efficiency and availability. The firm also holds the R&D needed to deploy 100% renewable hydrogen turbines at commercial scale, supporting the energy transition and realizing industrial decarbonization schemes across the globe.

-

2025: GE Vernova announced its first aeroderivative gas turbine solution designed for 100% renewable hydrogen operation, advancing hydrogen turbine retrofits at commercial scale.

Hydrogen Turbine Retrofits Companies:

-

Siemens Energy

-

General Electric (GE Power / GE Vernova)

-

Ansaldo Energia

-

Baker Hughes

-

MAN Energy Solutions

-

Solar Turbines (Caterpillar Inc.)

-

Rolls-Royce Holdings

-

Doosan Heavy Industries & Construction

-

Hitachi Energy

-

OPRA Turbines

-

Capstone Green Energy

-

EthosEnergy

-

MHPS (Mitsubishi Hitachi Power Systems)

-

ABB Group

-

Wärtsilä

-

Siemens Gamesa Renewable Energy

-

Zhejiang Hengyun Power

-

Turboden (Mitsubishi Heavy Industries Group)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.12 Billion |

| Market Size by 2035 | USD 4.70 Billion |

| CAGR | CAGR of 8.35% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Partial Retrofit, Full Retrofit) • By Turbine Capacity (Up to 100 MW, 100–300 MW, Above 300 MW) • By Application (Power Generation, Industrial, Oil & Gas, Others) • By End-User (Utilities, Independent Power Producers, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens Energy, General Electric (GE Power / GE Vernova), Mitsubishi Power, Ansaldo Energia, Baker Hughes, MAN Energy Solutions, Solar Turbines (Caterpillar Inc.), Rolls-Royce Holdings, Kawasaki Heavy Industries, Doosan Heavy Industries & Construction, Hitachi Energy, OPRA Turbines, Capstone Green Energy, EthosEnergy, MHPS (Mitsubishi Hitachi Power Systems), ABB Group, Wärtsilä, Siemens Gamesa Renewable Energy, Zhejiang Hengyun Power, Turboden (Mitsubishi Heavy Industries Group). |

Frequently Asked Questions

Europe dominated the Hydrogen Turbine Retrofits Market in 2025.

The Utilities segment dominated the Hydrogen Turbine Retrofits Market in 2025.

Increasing global adoption of hydrogen fuel for turbines is driving demand for retrofitting existing turbine infrastructure efficiently and sustainably.

The Hydrogen Turbine Retrofits Market was valued at USD 2.12 billion in 2025.

The Hydrogen Turbine Retrofits Market is expected to grow at a CAGR of 8.35% from 2026 to 2035.

Get in Touch