Green Hydrogen Market Report Scope and Overview:

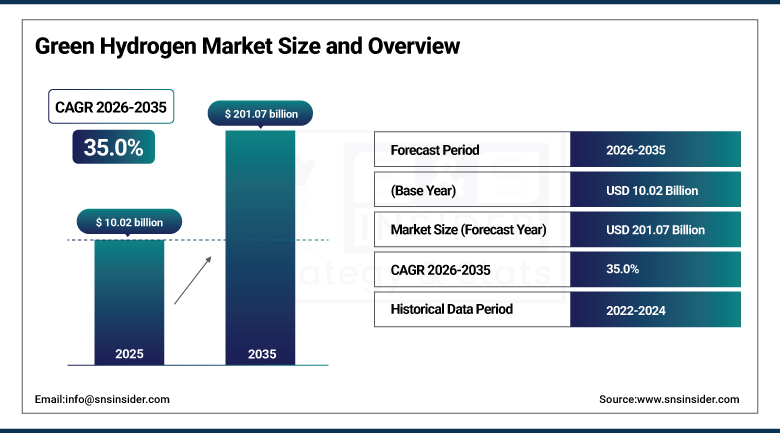

The Green Hydrogen Market was valued at USD 10.02 Billion in 2025 and is projected to reach USD 201.07 Billion by 2035, registering a CAGR of 35.0% from 2026 to 2035.

Solar and wind energy produce green hydrogen by splitting water molecules to separate hydrogen and oxygen atoms, generating hydrogen without using hydrocarbons and resulting in a genuine reduction in carbon emissions. Green hydrogen presently accounts for around 1% of total hydrogen production, and given its current lack of cost competitiveness relative to conventional gray hydrogen, the market is anticipated to grow rapidly during the forecast period as production costs continue falling and policy support continues expanding. Market estimates for this category vary considerably across independent research sources, reflecting the genuinely nascent, rapidly scaling nature of this technology category, where different firms capture different points along an extraordinarily steep early-stage growth curve. Increasing government initiatives and subsidies aimed at achieving net-zero emissions, coupled with growing investments in renewable hydrogen production infrastructure, continue accelerating market expansion worldwide.

India's National Green Hydrogen Mission earmarked USD 2.3 billion in incentives throughout 2025, complementing China's National Hydrogen Roadmap targets as both countries continued driving state-backed electrolyzer deployment across Asia Pacific's rapidly expanding green hydrogen production capacity.

Market Size and Forecast

- Market Size in 2026E: USD 13.50 Billion

- Market Size by 2035: USD 201.07 Billion

- CAGR: 35.0% from 2026 to 2035

- Fastest Growing Region: Europe

- Largest Region: Asia Pacific

To Get more information Green Hydrogen Market - Request Free Sample Report

Green Hydrogen Market Trends

- Artificial intelligence continues serving as a prominent tool in the green hydrogen value chain, assisting firms in making better decisions, reducing waste, and increasing energy savings.

- Smart sensors and AI models continue letting companies monitor hydrogen production in real time, particularly for electrolysis processes.

- Technological advancements in production methods, particularly electrolysis powered by renewable energy sources such as solar and wind, continue fueling market growth.

- Development of cost-effective and efficient storage and distribution solutions continues advancing alongside expanding production infrastructure.

- Iron and steel production continues transitioning toward Direct Reduced Iron processes that replace coal-based reduction methods with green hydrogen.

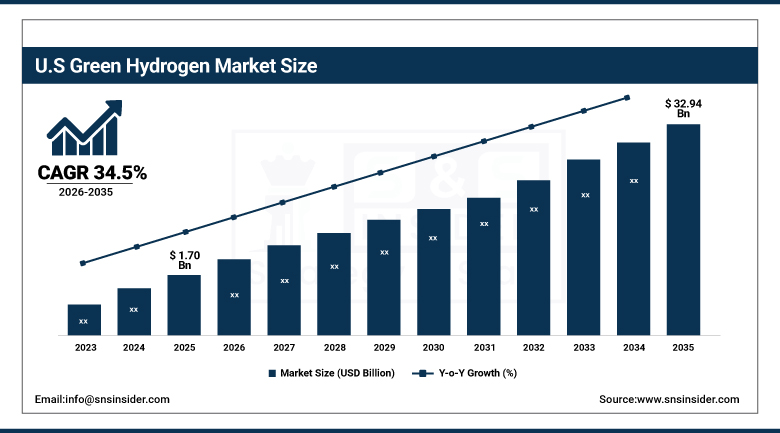

The US Green Hydrogen Market Outlook

The US Green Hydrogen Market was valued at approximately USD 1.70 Billion in 2025 and is projected to reach approximately USD 32.94 Billion by 2035, registering a CAGR of approximately 34.5% from 2026 to 2035.

The continued growth of the domestic market was due to an increase in the number of governmental measures and subsidies that were geared towards making the net-zero emissions. There were announcements from projects in the U.S. Gulf Coast Hydrogen Hub Corridors that were continually reinforcing the domestic capacity of production investment, as North America’s second-largest regional market grew stronger through electrolyzer manufacturing and the creation of renewable energy infrastructure. There were growing investments in renewable hydrogen production infrastructure coupled with developments in electrolysis technology powered by the sun and wind.

Plug Power continued expanding its green hydrogen production and electrolyzer manufacturing capacity throughout 2025, targeting American refining, chemicals, and transportation customers seeking domestically produced, renewably powered hydrogen supply capable of supporting industrial decarbonization commitments.

Green Hydrogen Market Segment Analysis

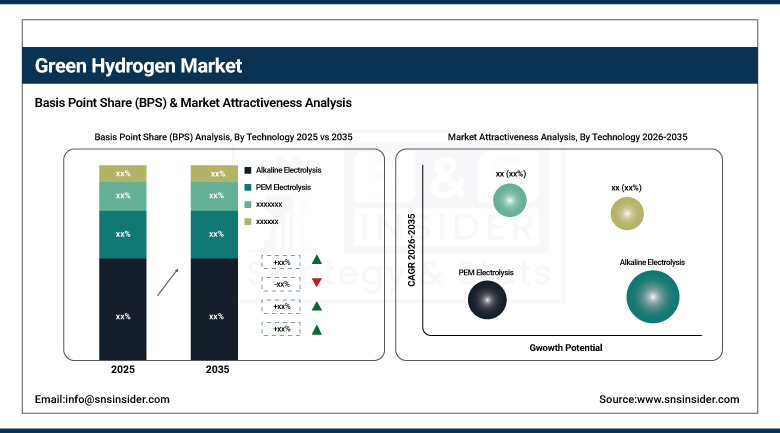

- By Technology, alkaline electrolysis led the market with around 55.1% share in 2025, while PEM electrolysis is the fastest-growing technology, tracking a rapid CAGR outpacing the broader market average.

- By Source, wind led the market with an estimated 47.8% share in 2025.

- By End-User Industry, refining led the market with an approximate 35.5% share in 2025, while chemicals is the fastest-growing end-user industry, tracking rapid green ammonia commitment expansion.

By Technology, Alkaline Electrolysis led the market, PEM Electrolysis grew fastest

Alkaline electrolysis captured 55.1% of installed capacity, anchored by mature stack designs and lower upfront capital intensity relative to alternative electrolysis technologies. Strong deployment in chemical processing, refining, and power-to-hydrogen applications, along with supportive government policies and funding for renewable hydrogen infrastructure, continued reinforcing alkaline electrolysis's dominant position by a considerable margin over PEM, solid oxide, and AEM alternatives.

PEM electrolysis is forecast to register the highest segment CAGR among technology types tracked in this market, driven by superior dynamic-response capability that lets these systems more effectively match variable renewable electricity output. As electrolyzer manufacturers continue scaling PEM production and driving down costs, that genuine technical performance advantage keeps this technology category's growth rate climbing well ahead of the broader, still-dominant alkaline electrolysis segment.

By Source, Wind led the market

The wind segment captured a revenue share of over 47.8%, reflecting wind power's genuinely favorable levelized cost of electricity and established renewable energy infrastructure in many leading green hydrogen production regions. That combination of cost competitiveness and infrastructure maturity kept wind the dominant renewable source category by a considerable margin over solar and other renewable alternatives.

Solar and other renewable sources continued representing meaningful additional demand beyond the dominant wind segment, with solar in particular continuing to gain share in regions with genuinely favorable solar resource availability and declining photovoltaic system costs. As renewable electricity generation costs continue falling across both wind and solar technologies, that broader cost decline keeps expanding the overall addressable market for electrolysis-based green hydrogen production regardless of the specific renewable source deployed.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|

Asia Pacific |

China |

37.90% |

|

Europe |

Germany |

24.05% |

|

North America |

United States |

80.30% |

|

Middle East and Africa |

UAE |

26.60% |

|

Latin America |

Brazil |

34.15% |

North America Green Hydrogen Market Insights

North America accounted for the second-largest share among all regions tracked in this report, underpinned by project announcements across the U.S. Gulf Coast hydrogen hub corridors. That combination of substantial industrial hydrogen demand and expanding domestic production infrastructure investment kept the continent a genuinely significant contributor to global green hydrogen revenue throughout the year.

The United States accounted for roughly 80.30% of regional revenue, anchored by extensive Gulf Coast hydrogen hub development and growing government incentive support. Canada added further regional demand through its own developing green hydrogen production sector, and that combined strength kept North America positioned among the market's most important regional contributors through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Green Hydrogen Market Insights

Europe is expected to advance at the fastest CAGR among all regions tracked in this report, propelled by binding renewable-hydrogen mandates under the revised Renewable Energy Directive. Carbon border adjustment obligations and REPowerEU mandates continue compelling industrial buyers to lock in green hydrogen supply, driving accelerated regional investment throughout the year.

Germany led demand at roughly 24.05% of European revenue, supported by its substantial industrial hydrogen offtake and renewable energy infrastructure. The UK, which held the largest revenue share within Europe according to certain sources, along with France contributed substantial additional demand, and continued European regulatory mandate expansion should keep regional demand climbing through the forecast period.

Asia Pacific Green Hydrogen Market Insights

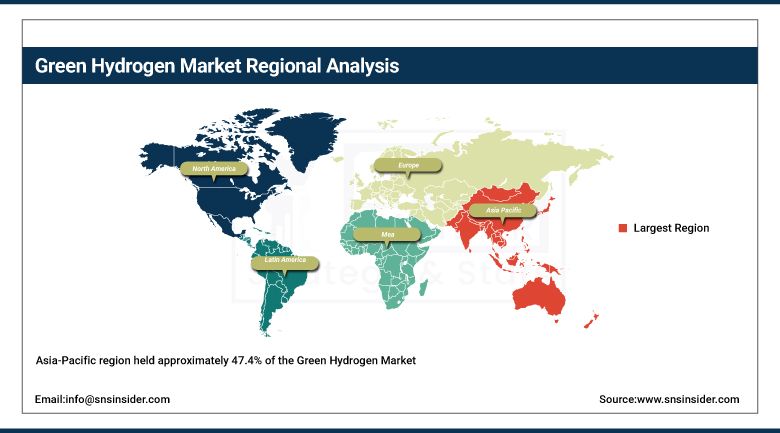

Asia-Pacific region held approximately 47.4% of the Green Hydrogen Market owing to the goals set out in China's National Hydrogen Roadmap and India's National Green Hydrogen Mission, in which huge amounts of incentive funding were allocated. China is the leader in terms of market share in the Asia-Pacific green hydrogen market due to its high hydrogen production output in the region.

China emerged as the market leader, backed by the use of electrolyzers by the government and huge investments made in renewable energy projects. India also made significant contributions in the form of incentives provided under its National Green Hydrogen Mission.

MEA and Latin America Green Hydrogen Market Insights

The Middle East and Africa and Latin America both showed meaningful growth, with the Middle East in particular representing a genuinely significant emerging production hub given substantial renewable energy resource availability. Latin America continued showing steady growth over the same period, with the region positioned by some sources as a genuinely fast-growing market given its abundant renewable energy potential.

The UAE led Middle East and Africa demand, supported by substantial renewable energy investment and growing green hydrogen export infrastructure ambitions. Saudi Arabia contributed further demand through its own large-scale green hydrogen production programs. In Latin America, Brazil accounted for the largest share of regional revenue, with growing renewable energy investment continuing to anchor regional demand for green hydrogen production.

Market Dynamics

Growth Drivers: Net-Zero Policy Support and Industrial Decarbonization Pressure

Increasing government initiatives and subsidies aimed at achieving net-zero emissions, coupled with growing investments in renewable hydrogen production infrastructure, continue accelerating market expansion. Technological advancements in green hydrogen production methods, particularly electrolysis powered by renewable energy sources such as solar and wind, continue fueling sustained market growth.

As petroleum processors and industrial manufacturers increasingly face scope-1 decarbonization targets, that genuine regulatory and stakeholder pressure continues driving green hydrogen adoption across refining, chemicals, and iron and steel production. That combination of genuine policy necessity and expanding industrial decarbonization commitment is exactly what keeps demand climbing at such a rapid, sustained pace across virtually every major consuming region this market serves.

Restraints: Cost Competitiveness Gap and Infrastructure Development Requirements

Green hydrogen presently accounts for around 1% of total hydrogen production, and its current lack of cost competitiveness relative to conventional gray hydrogen continues posing a genuine restraint on faster market-wide adoption. That cost gap keeps green hydrogen's addressable market genuinely concentrated among customers with strong decarbonization mandates or premium market positioning rather than pure cost-driven procurement decisions.

The development of cost-effective and efficient storage and distribution solutions continues posing a further restraint, as hydrogen's genuinely challenging physical properties require specialized, capital-intensive infrastructure investment across production, transport, and end-use application. That infrastructure requirement keeps full-scale green hydrogen value chain development a genuinely multi-year undertaking for most producing regions.

Opportunities: PEM Technology Scale-Up and Iron and Steel Decarbonization

PEM electrolysis's superior dynamic-response capability represents a genuinely significant opportunity, as this technology category's fastest-growing status among all segments tracked in this market reflects genuine demand for systems capable of effectively matching variable renewable electricity output. Vendors offering genuinely proven, cost-competitive PEM electrolyzer technology stand to capture meaningful share as this technology category continues scaling toward broader commercial deployment.

Iron and steel production's transition toward Direct Reduced Iron processes offers a second substantial opportunity, as rising carbon pricing continues making this decarbonization pathway increasingly economically viable. Vendors positioned to serve this expanding heavy-industry decarbonization customer base stand to capture meaningful share as this end-user category continues expanding well beyond the market's traditional refining stronghold.

Recent Developments:

- 2025: Linde continued expanding its large-scale green hydrogen production and liquefaction capacity, targeting industrial customers seeking reliable, renewably produced hydrogen supply across refining and chemicals applications.

- 2025: ITM Power continued advancing its PEM electrolyzer manufacturing capability, targeting energy companies seeking scalable, dynamically responsive green hydrogen production technology.

- 2024: thyssenkrupp nucera continued expanding its alkaline electrolyzer manufacturing capacity, targeting large-scale industrial customers seeking cost-competitive green hydrogen production technology for chemicals and refining applications.

Green Hydrogen Market key players are:

- Linde plc

- Air Liquide S.A.

- Air Products and Chemicals, Inc.

- ENGIE SA

- Uniper SE

- Siemens Energy AG

- Cummins Inc.

- Toshiba Energy Systems & Solutions Corporation

- Nel ASA

- ITM Power plc

- Plug Power Inc.

- thyssenkrupp nucera AG & Co. KGaA

- McPhy Energy S.A.

- Enapter S.r.l.

- Ørsted A/S

- TotalEnergies SE

- Shell plc

- BP p.l.c.

- Iberdrola S.A.

- Green Hydrogen Systems A/S

Green Hydrogen Market Report Scope:

| Report Attributes | Details |

|---|---|

|

Table Of Contents 1. Market Context & Strategic Relevance 1.1 Opening Context (Why the market matters) 1.1.1 Why This Market Is Gaining Strategic Attention 1.1.2 Business Decisions This Report Supports 1.2 Scope 2. Executive Summary 2.1 Market Snapshot 2.2 Market Absolute $ Opportunity Assessment & Y-o-Y Analysis, 2022–2035 2.3 Market Size & Forecast, By Segmentation, 2022–2035 2.3.1 Market Size by Source 2.3.2 Market Size by Technology 2.3.3 Market Size by End-User Industry 2.4 Market Share & Bps Analysis by Region, 2025 2.5 Industry Growth Scenarios – Conservative, Likely & Optimistic 2.6 Industry CxO’s Perspective 3. Market Overview 3.1 Market Dynamics 3.1.1 Drivers 3.1.2 Restraints 3.1.3 Opportunities 3.1.4 Key Market Trends 3.2 Industry PESTLE Analysis 3.3 Key Industry Forces (Porter’s) Impacting Market Growth 3.4 Industry Supply Chain Analysis 3.4.1 Raw Material Suppliers 3.4.2 Manufacturers 3.4.3 Distributors/Suppliers 3.4.4 Customers/End-Users 3.5 Industry Life Cycle Assessment 4. Statistical Insights & Trends Reporting 4.1 Production Technology Metrics 4.1.1 Share (%) of installed green hydrogen capacity by alkaline, PEM, SOEC, and AEM electrolysis. 4.1.2 Growth (%) in global electrolyzer manufacturing capacity. 4.1.3 Increase (%) in renewable-powered hydrogen production projects. 4.2 End-User Industry Metrics 4.2.1 Share (%) of green hydrogen demand by refining, chemicals, steel, mobility, power generation, and others. 4.2.2 Growth (%) in green ammonia and green methanol production capacity. 4.2.3 Increase (%) in industrial hydrogen substitution across hard-to-abate sectors. 4.3 Infrastructure & Investment Metrics 4.3.1 Share (%) of investments in hydrogen production, storage, and distribution infrastructure. 4.3.2 Growth (%) in hydrogen refueling stations and transportation networks. 4.3.3 Increase (%) in public and private funding for green hydrogen projects. 4.4 Sustainability & Policy Metrics 4.4.1 Share (%) of green hydrogen projects supported by government incentives and subsidies. 4.4.2 Growth (%) in renewable electricity integration for hydrogen production. 4.4.3 Increase (%) in carbon emission reduction through green hydrogen adoption. 5. Green Hydrogen Market Segmental Analysis & Forecast, By Source, 2022–2035, Value (USD Billion) 5.1 Introduction 5.2 Wind 5.2.1 Key Trends 5.2.2 Market Size & Forecast, 2022–2035 5.3 Solar 5.4 Other Renewable Sources 6. Green Hydrogen Market Segmental Analysis & Forecast, By Technology, 2022–2035, Value (USD Billion) 6.1 Introduction 6.2 Alkaline Electrolysis 6.2.1 Key Trends 6.2.2 Market Size & Forecast, 2022–2035 6.3 PEM Electrolysis 6.4 Solid Oxide Electrolysis 6.5 AEM Electrolysis 7. Green Hydrogen Market Segmental Analysis & Forecast, By End-User Industry, 2022–2035, Value (USD Billion) 7.1 Introduction 7.2 Refining 7.2.1 Key Trends 7.2.2 Market Size & Forecast, 2022–2035 7.3 Chemicals 7.4 Iron and Steel 7.5 Transportation 8. Green Hydrogen Market Segmental Analysis & Forecast, By Region, 2022–2035, Value (USD Billion) 8.1 Introduction 8.2 North America 8.2.1 Key Trends 8.2.2 Green Hydrogen Market Size & Forecast, By Source, 2022–2035 8.2.3 Green Hydrogen Market Size & Forecast, By Technology, 2022–2035 8.2.4 Green Hydrogen Market Size & Forecast, By End-User Industry, 2022–2035 8.2.5 Green Hydrogen Market Size & Forecast, By Country, 2022–2035 8.2.5.1 USA 8.2.5.2 Canada 8.3 Europe 8.3.1 Key Trends 8.3.2 Green Hydrogen Market Size & Forecast, By Source, 2022–2035 8.3.3 Green Hydrogen Market Size & Forecast, By Technology, 2022–2035 8.3.4 Green Hydrogen Market Size & Forecast, By End-User Industry, 2022–2035 8.3.5 Green Hydrogen Market Size & Forecast, By Country, 2022–2035 8.3.5.1 Germany 8.3.5.2 UK 8.3.5.3 France 8.3.5.4 Italy 8.3.5.5 Spain 8.3.5.6 Russia 8.3.5.7 Poland 8.3.5.8 Rest of Europe 8.4 Asia-Pacific 8.4.1 Key Trends 8.4.2 Green Hydrogen Market Size & Forecast, By Source, 2022–2035 8.4.3 Green Hydrogen Market Size & Forecast, By Technology, 2022–2035 8.4.4 Green Hydrogen Market Size & Forecast, By End-User Industry, 2022–2035 8.4.5 Green Hydrogen Market Size & Forecast, By Country, 2022–2035 8.4.5.1 China 8.4.5.2 India 8.4.5.3 Japan 8.4.5.4 South Korea 8.4.5.5 Australia 8.4.5.6 ASEAN Countries 8.4.5.7 Rest of Asia-Pacific 8.5 Latin America 8.5.1 Key Trends 8.5.2 Green Hydrogen Market Size & Forecast, By Source, 2022–2035 8.5.3 Green Hydrogen Market Size & Forecast, By Technology, 2022–2035 8.5.4 Green Hydrogen Market Size & Forecast, By End-User Industry, 2022–2035 8.5.5 Green Hydrogen Market Size & Forecast, By Country, 2022–2035 8.5.5.1 Brazil 8.5.5.2 Argentina 8.5.5.3 Mexico 8.5.5.4 Colombia 8.5.5.5 Rest of Latin America 8.6 Middle East & Africa 8.6.1 Key Trends 8.6.2 Green Hydrogen Market Size & Forecast, By Source, 2022–2035 8.6.3 Green Hydrogen Market Size & Forecast, By Technology, 2022–2035 8.6.4 Green Hydrogen Market Size & Forecast, By End-User Industry, 2022–2035 8.6.5 Green Hydrogen Market Size & Forecast, By Country, 2022–2035 8.6.5.1 UAE 8.6.5.2 Saudi Arabia 8.6.5.3 Qatar 8.6.5.4 South Africa 8.6.5.5 Rest of Middle East & Africa 9. Competitive Landscape 9.1 Key Players' Positioning 9.2 Competitive Developments 9.2.1 Key Strategies Adopted (%), By Key Players, 2025 9.2.2 Year-Wise Strategies & Development, 2022–2025 9.2.3 Number Of Strategies Adopted By Key Players, 2025 9.3 Market Share Analysis, 2025 9.4 Product/Service & Application Benchmarking 9.4.1 Product/Service Specifications & Features By Key Players 9.4.2 Product/Service Heatmap By Key Players 9.4.3 Application Heatmap By Key Players 9.5 Industry Start-Up & Innovation Landscape 9.6 Key Company Profiles 9.6.1 Linde plc 9.6.1.1 Company Overview & Snapshot 9.6.1.2 Product/Service Portfolio 9.6.1.3 Key Company Financials 9.6.1.4 SWOT Analysis 9.6.2 Air Liquide S.A. 9.6.3 Air Products and Chemicals, Inc. 9.6.4 ENGIE SA 9.6.5 Uniper SE 9.6.6 Siemens Energy AG 9.6.7 Cummins Inc. 9.6.8 Toshiba Energy Systems & Solutions Corporation 9.6.9 Nel ASA 9.6.10 ITM Power plc 9.6.11 Plug Power Inc. 9.6.12 thyssenkrupp nucera AG & Co. KGaA 9.6.13 McPhy Energy S.A. 9.6.14 Enapter S.r.l. 9.6.15 Ørsted A/S 9.6.16 TotalEnergies SE 9.6.17 Shell plc 9.6.18 BP p.l.c. 9.6.19 Iberdrola S.A. 9.6.20 Green Hydrogen Systems A/S 10. Analyst Recommendations 10.1 SNS Insider Opportunity Map 10.2 Industry Low-Hanging Fruit Assessment 10.3 Market Entry & Growth Strategy 10.4 Analyst Viewpoint & Suggestions On Market Growth 11. Assumptions 12. Disclaimer 13. Appendix 13.1 List Of Tables 13.2 List Of Figures |

|

Frequently Asked Questions

The Green Hydrogen Market is expected to grow at a CAGR of approximately 35.0% from 2026 to 2035, based on triangulated secondary research estimates.

The Green Hydrogen Market was valued at approximately USD 10.02 Billion in 2025.

The major growth factor is increasing government initiatives and subsidies aimed at achieving net-zero emissions combined with growing investments in renewable hydrogen production infrastructure.

The Alkaline Electrolysis segment dominated the Green Hydrogen Market by technology, representing an estimated 55.1% of installed capacity in 2025.

Asia Pacific dominated the Green Hydrogen Market in 2025, holding an estimated 46% share of total global market revenue.

Get in Touch