I2C Bus Market Report Scope & Overview:

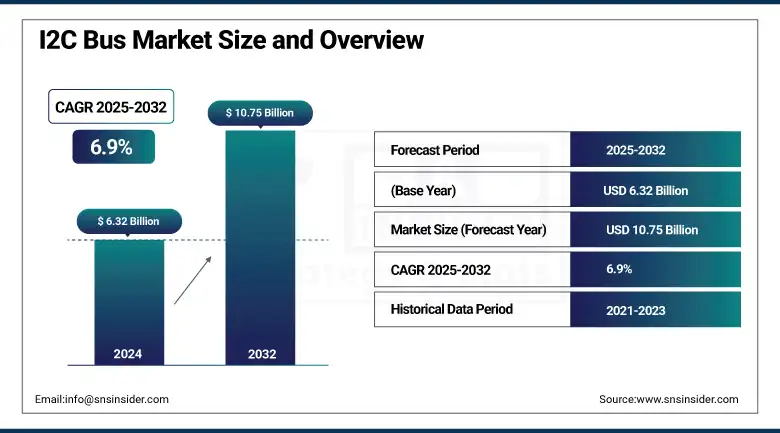

The I2C Bus Market size was valued at USD 6.32 billion in 2024 and is expected to reach USD 10.75 billion by 2032, expanding at a CAGR of 6.9% over the forecast period of 2025-2032.

The I2C (Inter-Integrated Circuit) Bus Market is growing because most embedded system designs require a simple, elegant, low-speed, short-distance communication method means that I2C will always have a place in the system; it is not intended for long-distance communication or high bandwidth applications. For consumer electronics, automotive, industrial, and IoT applications, the two-wire architecture also enables easy multi-device connectivity. Use of sensors and microcontrollers is increasing day by day, and I2C is widely used due to its simplicity, scalability, and low power consumption. Fast-mode Plus and other enhanced variants are broadening their use, while legacy support is ensuring ubiquity. While I3C is a new interconnect type on the horizon and there are alternatives like SPI, I2C is still ideal for high-volume electronics and smart device ecosystems where affordability and small footprint are important.

To Get more information On I2C Bus Market - Request Free Sample Report

According to research, I2C is preferred in battery-powered, edge AI, and wearable devices, offering up to 30% lower power consumption and supporting over 60–80% of sensor communication due to its efficiency and scalability.

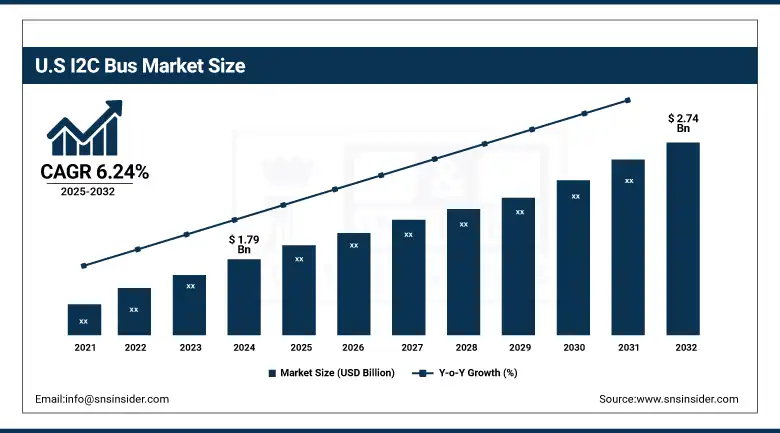

The U.S I2C Bus Market size reached USD 1.79 billion in 2024 and is expected to reach USD 2.74 billion in 2032 at a CAGR of 6.24% from 2025 to 2032.

The U.S. dominates the global I2C bus market due to the growth of its semiconductor I2C bus market industry, the presence of various key market players, and the high demand for embedded systems in automotive, aerospace, and consumer electronics. The proliferation of smart devices, the growing implementation of IoT solutions, and the rising need for compact and efficient communication protocols are among the crucial factors driving the I2C Bus Market growth of the market. The expansion of the U.S. I2C market is driven by additional government support for domestic chip manufacturing, along with continued innovation in automation and medical electronics.

Market Dynamics:

Drivers:

-

Increased Integration of Embedded Systems in Consumer Electronics and Automotive Enhances Communication Interface Adoption

With consumer electronics and automotive systems becoming increasingly sophisticated, the demand for embedded communication including I2C is growing even faster. Since devices demand effortless, low-power interconnections between several sensors, displays, and microcontrollers, I2C is the protocol of choice with its two-wire, low-power, and multi-slave scalability. The increasing trend of electric vehicles and advanced driver-assistance systems (ADAS) in the automotive sector is urging the integration of components enabled with I2C, a communication option. Recent I2C bus market trends indicate increasing adoption in IoT and automotive sectors due to its low power consumption and scalability.

According to research, approximately 85% of smart home hubs and controllers use I2C buses to manage multi-sensor arrays and peripheral devices efficiently.

Restraints:

-

Limited Data Rate and Communication Speed Restricts Suitability for High-Performance Applications in Industrial and Commercial Systems

I2C is straightforward and inexpensive, it has a low transfer rate it rarely exceeding 3.4 Mbps in high-speed modes, which is not suitable for applications where you desire fast and massive data throughput. Protocols, such as SPI or Ethernet are preferred for their better performance in high-performance systems including industrial automation and high-end computing platforms. As devices become increasingly data-dependent, this limitation becomes a heavy constraint. As a result, performance reliability, particularly in time-sensitive circumstances, also suffers from clock stretching, bus contention, and from a poor multi-master capability.

Opportunities:

-

Rising Adoption of Smart and Connected Devices in IoT Ecosystems Presents Growth Potential for Low-Power Communication Protocols

The growing penetration of IoT applications in home, factory, and clinic setups is providing significant growth opportunities for low-power, small-size communication standards such as I2C. Being smart devices, internal interconnects among the different elements making up the device, including sensors, processors, and displays, are numerous, and I2C is popular as it can have minimal wiring and power usage. Applications, such as Smart metering, remote environmental monitoring, and wearable medical devices have recently deployed I2C.

Challenges:

-

Complexity in Managing Multiple Slave Devices on a Shared Bus Increases Design and Debugging Challenges for Developers

Managing the integrity of communications becomes increasingly difficult as systems scale and the number of I2C slave devices that are connected increases. Long trace lengths, excessive electrical noise, or both can cause problems like address clashes, bus arbitration, and signal degradation. Solving these issues requires careful timing, custom board development, and often more debugging time than you have planned for, pushing out your development schedule and increasing costs. In addition, similar to all standard I2Cs, there are no built-in error-checking mechanisms in I3C that can detect a malfunction while in operation.

Segmentation Analysis

By Type

In 2024, the Unidirectional I2C Bus segment held the largest revenue share of 55.30% due to its large-scale provision in applications with straightforward, single-direction data transmission from master to slave devices. Providing lower design overhead, it is implemented in low-cost and low-power systems, such as wearables or devices of home automation. For improved connectivity, I2C bus market companies, such as NXP Semiconductors and Microchip Technology have introduced I2C-compatible unidirectional microcontrollers and EEPROMs.

The Bidirectional I2C Bus segment is expected to witness the fastest CAGR of 8.50% due to the need for flexible, two-way data communication in smart devices, automotive electronics, and industrial automation systems. The easy, bi-directional switching of master-slave roles and real-time data feedback capabilities are both indispensable assets in complex embedded applications. Advanced bidirectional transceivers for high-reliability systems and I2C expanders with very high temperature functionality were introduced by companies, such as NXP Semiconductors and Microchip Technology.

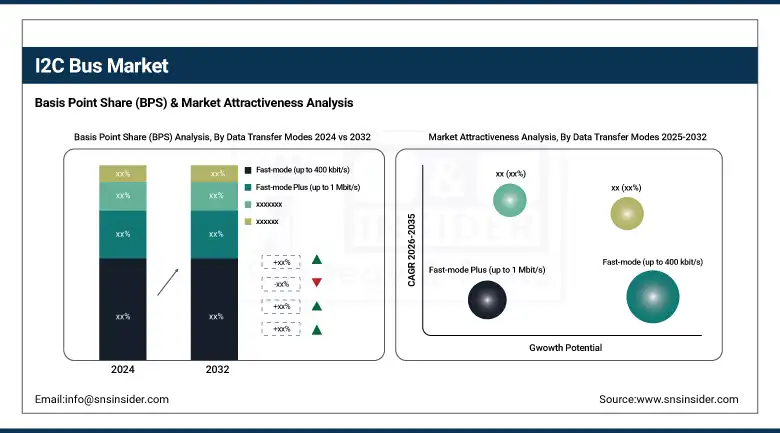

By Data Transfer Modes

The Fast-mode (up to 400 kbit/s) segment accounted for the largest revenue share in 2024 at 25.13%, as it offers a good balance between speed and reliability for mass-market applications. It is prevalent in consumer electronics, memory modules, and sensor interfaces. To meet the growth stemming from home automation, smart appliance companies have launched Fast-mode compatible ICs, such as those from Texas Instruments and Renesas Electronics. A key driver is the growing demand for medium-speed communication in devices with a moderate level of complexity.

The Fast-mode Plus (up to 1 Mbit/s) is projected to be the fastest-growing segment with a CAGR of 8.81% during the forecast period, owing to the increasing demand for rapid communication in the identified applications with advanced sensor arrays, industrial control systems, and infotainment modules. Some of the latest products are Analog Devices’ high-speed I2C-compatible digital isolators for rugged industrial applications. It enables longer cables and higher capacitance; thus, this mode supports a more flexible system design.

By Application

The SMBus held the fastest share in 2024 at 31.52% and is important for monitoring and management components, thus system health and status in computers, servers, and battery systems. The key factors driving the market include the rising need for thermal and voltage management in data centres and laptops. SMBus has been incorporated by companies including Intel and ON Semiconductor directly into power management ICs and processor support chips. Its compatibility with existing I2C infrastructure and widespread use in servers and industrial systems strengthens its dynamic role in expanding Inter-Integrated Circuit (I2C) Bus Market applications.

The PMBus segment is anticipated to post the fastest CAGR of 8.81% over the forecast period due to the growing requirement for smart power supply monitoring in telecom, data centers, and industrial automation. It enables power supply units to be configured and faulted in real-time, improving reliability and energy efficiency. Examples include PMBus power modules for cloud infrastructure from Infineon Technologies and Monolithic Power Systems. PMBus provides scalable, programmable solutions that are ideally matched to increasing power density, operational complexity, and green energy mandates.

Regional Analysis:

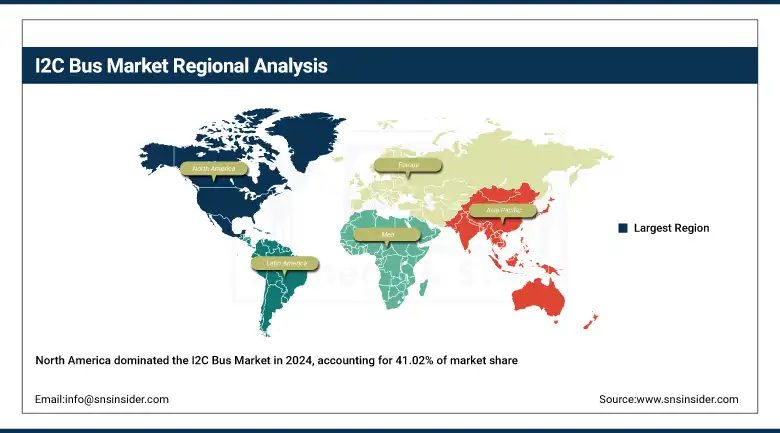

North America leads the market, accounting for 41.02% of market share, owing to a strong consumer electronics industry, an innovative automotive industry, and a developing industrial automation segment. This shift toward I2C-enabled legacy and next-gen applications, such as IoT and smart healthcare, is propelled by the region’s advanced semiconductor infrastructure and strong R&D capabilities.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. will continue to lead the regional space given its robust semiconductor manufacturing base, technological know-how, and large usage of I2C across automotive, aerospace, and medical equipment.

Europe Market develops the shooting of automobile hardware, with the demand for efficient integrated solutions and industrial management systems. Driven by sustainable initiatives and intelligent infrastructure, the area implements I2C in other sensor networks, EV components, and energy monitoring applications, aided by an increasing number of private and public collaborations.

Germany is the leader due to the automotive innovation, the engineering ecosystem, and the use of I2C in precision engineering and Industry 4.0.

Asia Pacific is the fastest-growing region with a CAGR of 9.46% over the forecast period, owing to the high-volume production of electronics-intensive products, IoT expansion, and favourable government initiatives for domestic semiconductor ecosystem development. Low production costs with the availability of OEMs will propel the adoption of I2C in smartphones, wearables, and industrial automation equipment.

China drives innovation, powered by a massive consumer electronics manufacturing base, rapid industrial digitalization, and major investments in chip fab and smart device ecosystems.

The Middle East & Africa and Latin America is expected to grow steadily over the forecast period, owing to the automation investments, Smart city initiatives, emergence of embedded systems in Industrial, automotive, and agriculture applications.

Key Players:

The major key players of the I2C Bus Market are Texas Instruments Incorporated, NXP Semiconductors N.V., STMicroelectronics N.V., Analog Devices, Inc., ON Semiconductor Corporation, Renesas Electronics Corporation, Microchip Technology Inc., Infineon Technologies AG, Broadcom Inc., Maxim Integrated Products, Inc., and others.

Key Developments:

-

In May 2024, Infineon Technologies introduced a new NFC-to-I2C bridge tag providing secure, Contactless configuration and authentication for IoT devices, and boosting security by making setup easier in smart homes and wearables.

-

in April 2024, NXP Semiconductors recorded a 5% year-over-year fall in revenue to USD12.61 billion but retained healthy margins and revealed a USD 307 million purchase of Kinara to augment edge AI functionality.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 6.32 Billion |

| Market Size by 2032 | USD 10.75 Billion |

| CAGR | CAGR of 6.9% from 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Bidirectional I2C Bus, Unidirectional I2C Bus) •By Data Transfer Modes (Standard-mode, Fast-mode, Fast-mode Plus, High-speed mode, Ultra-fast mode) •By Application (System Management Bus (SMBus), Power Management Bus (PMBus), Intelligent Platform Management Interface (IPMI), Display Data Channel (DDC), Advanced Telecom Computing Architecture (ATCA)) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Texas Instruments Incorporated, NXP Semiconductors N.V., STMicroelectronics N.V., Analog Devices, Inc., ON Semiconductor Corporation, Renesas Electronics Corporation, Microchip Technology Inc., Infineon Technologies AG, Broadcom Inc., Maxim Integrated Products, Inc. |

Frequently Asked Questions

North America dominated the I2C Bus Market in 2024, accounting for 41.02% of the market share, driven by strong growth in consumer electronics, automotive, and industrial automation sectors.

The Unidirectional I2C Bus segment dominated the market in 2024, holding the largest revenue share of 55.30%, due to its widespread use in simple, single-direction data transmission applications like wearables and home automation.

The major growth factor is the increased integration of embedded systems

The market size of the I2C Bus Market in 2024 was USD 6.32 billion.

The I2C Bus Market is expected to expand at a CAGR of 6.9% over the forecast period from 2025 to 2032.

Get in Touch