Commercial Insurance Market Report Scope & Overview:

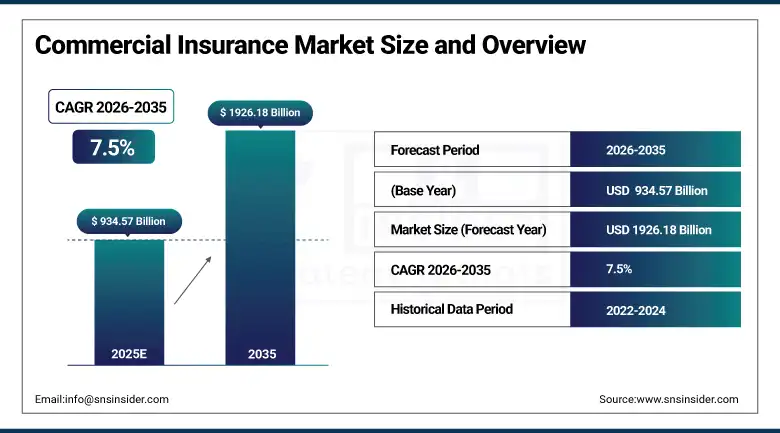

The Commercial Insurance Market was valued at USD 934.57 billion in 2025 and is expected to reach USD 1926.18 billion by 2035, growing at a CAGR of 7.5% from 2026-2035.

The Importance of the Commercial Insurance Market The commercial insurance market is an essential part of risk management for various industries such as construction, healthcare, manufacturing and transportation. Increasing knowledge of risk exposure and government policies is driving demand for bespoke insurance products. The Commercial Insurance Market is quickly integrating digital technology, allowing for the immediate procurement of insurance and payment of claims. A.I., blockchain and big data analytics are improving the accuracy of underwriting while combating fraud. Greater digital connectivity is prompting more SMEs to take action and insurers are developing products tailored towards specific industries, helping them to manage risks like cyber-attacks and climate change.

Commercial Insurance Market Size and Forecast:

-

Market Size in 2025: USD 934.57 Billion

-

Market Size by 2035: USD 1926.18 Billion

-

CAGR: 7.5% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Commercial Insurance Market - Request Free Sample Report

Commercial Insurance Market Trends

-

Rising business risks and growing awareness of liability coverage are driving the commercial insurance market.

-

Increasing adoption of digital platforms and AI-driven underwriting is enhancing policy management and claims processing.

-

Expansion of SMEs, large enterprises, and multinational corporations is boosting demand for tailored insurance solutions.

-

Growing focus on risk mitigation, regulatory compliance, and business continuity is shaping market trends.

-

Integration of telematics, IoT, and analytics is improving risk assessment and fraud detection.

-

Rising exposure to cyber threats, natural disasters, and supply chain disruptions is fueling product innovation.

-

Collaborations between insurers, brokers, and technology providers are accelerating adoption and digital transformation.

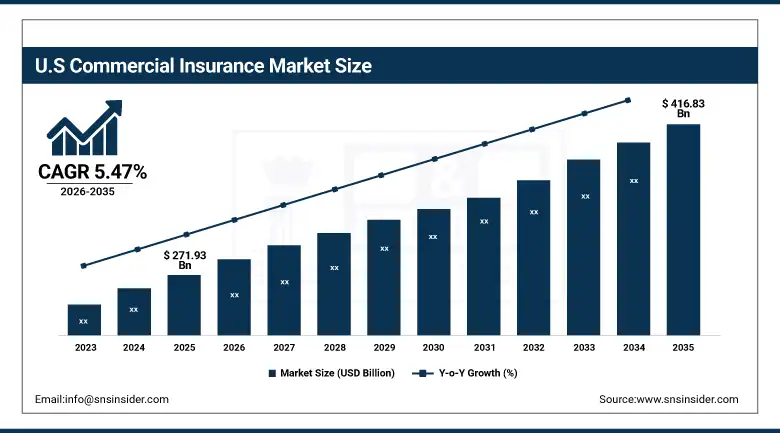

U.S. Commercial Insurance Market was valued at USD 271.93 billion in 2025 and is expected to reach USD 416.83 billion by 2035, growing at a CAGR of 5.47% from 2026-2035.

The U.S. Commercial Insurance Market is growing at a steady pace owing to the rising demand for customized insurance services. Organizations are also concentrating on risk management services pertaining to cyber attacks, property damage, and liability protection. Technology is also helping organizations to process insurance policies quickly and optimize claims processing. The U.S. Commercial Insurance Market is also benefiting from digitalization, which is providing SMEs with improved access to insurance services. Organizations are also concentrating on industry-specific insurance services to meet the rising demand from businesses.

Commercial Insurance Market Growth Drivers:

-

Increasing Business Risk Awareness and Regulatory Compliance Pushes Growth in the Commercial Insurance Market

The increasing awareness among businesses about the possibility of financial risks due to unforeseen circumstances such as cyber attacks, natural disasters, or business risks is a major driving factor for the Commercial Insurance Market. Organizations are now actively looking for comprehensive insurance coverage to counter risks and ensure business continuity.

Furthermore, governments and trade associations are strictly implementing regulations related to employee safety, environmental, and data protection, forcing businesses to invest in industry-specific insurance coverage. This is particularly evident in sectors such as construction, healthcare, and technology, which are more prone to risks. Insurers are now developing more complex and industry-specific packages and using technology to improve customer experience and risk analysis. As a result, commercial insurance is gradually shifting from a luxury to a necessity.

Commercial Insurance Market Restraints:

-

Complex Policy Structures and High Premium Costs Restrain the Commercial Insurance Market Growth

One of the major constraints in the Commercial Insurance Market is the complexity of the insurance products and the consequent high cost of premiums. It has been noticed that small and medium-scale enterprises (SMEs) are unable to understand and afford full-fledged commercial insurance policies, which come with various layers of coverage and exclusions, as well as legal jargon. This makes them reluctant to purchase and results in underinsurance or basic insurance purchase, which may not be adequate.

Further, high premiums, especially in sectors that are more likely to make claims, such as logistics and manufacturing, create a cost burden that some organizations are unwilling or unable to bear.

Commercial Insurance Market Opportunities:

-

Growing Integration of AI and Big Data Analytics Offers New Opportunities in the Commercial Insurance Market

The adoption of new technologies such as Artificial Intelligence (AI) and big data analytics is a great development opportunity for the Commercial Insurance Market. These technologies are revolutionizing the way insurers price and assess risks, as well as the way they process claims. The use of real-time data from IoT devices, telematics, and customer platforms enables insurers to develop dynamic and usage-based insurance products that are more aligned with the current business practices.

Moreover, predictive analytics can be used to forecast risk patterns and customer behavior, enabling insurers to design products more effectively. This paradigm shift towards technology-enabled services not only improves efficiency and customer satisfaction but also provides an opportunity for digital-born SMEs seeking accessible, fast, and flexible insurance solutions.

Commercial Insurance Market Challenge:

-

High Vulnerability to Evolving Risks, Such as Cyberattacks, Presents a Major Challenge in the Commercial Insurance Market

The constantly evolving nature of risks, particularly cyber risks, is a challenge to the Commercial Insurance Market. The traditional structures and products of insurance are not adequate to provide the speed, complexity, and financial scale of the emerging risks associated with ransomware attacks, phishing, and data breaches. The increasing digitization of businesses exposes companies to risks in a manner that has never been experienced before, and insurance products have not yet provided adequate protection against these risks.

This lack of standardized risk assessment tools and historical data means these kinds of dynamic risks cannot be properly priced. Insurers will also have to innovate in terms of products and services while educating the wide range of consumers about emerging risks. If these risks are not tackled then this will not only diminish the value proposition of commercial insurance but which also may threaten market sustainability.

Commercial Insurance Market Segment Analysis

By Distribution Channel, Agents & Brokers led in 2025 with 59% revenue share. Direct Response growing fastest.

In 2025, the Agents & Brokers market was dominated by the Commercial Insurance Market, with a share of 59% of the revenue. The traditional market - dependent on the personal touch, with agents and brokers organising bespoke insurance solutions based on comprehensive risk assessments. For clients, this means leveraging extensive network and experience, as companies like Willis Towers Watson definitely do, to connect clients with full insurance. This marketplace has been the obvious choice for a considerable amount of businesses for various reasons, primarily due to the fact that this marketplace comes with its own trusted agents and brokers who have a long-lasting relationship with their client. Clients are used to collaborating with their brokers who have intimate knowledge of their business and ask for sustainable customized insurance packages.

The Direct Response market is expected to register the highest growth rate, with a CAGR of 8.96% during the forecast period of 2026-2035. This market employs digital technology to offer insurance services directly to consumers, making it easier for them to purchase. The use of technology in this industry is evident, with Arch Insurance's acquisition of Thimble enhancing its ability to offer on-demand insurance services through user-friendly apps and websites. This is especially attractive to small and medium-sized businesses seeking flexible insurance options.

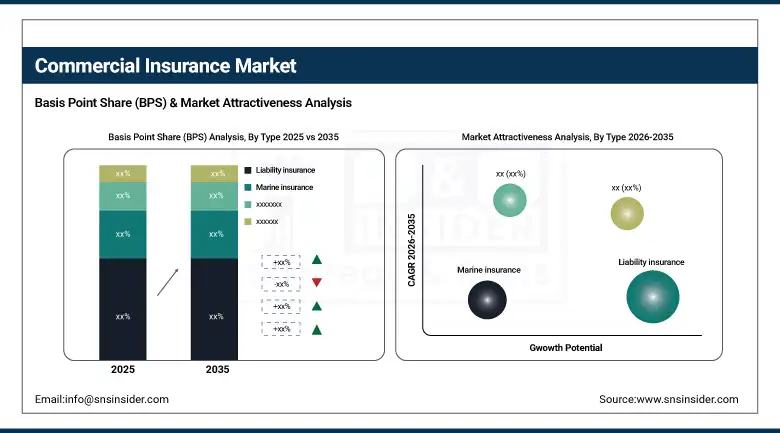

By Type, Liability Insurance led in 2025 with 35% revenue share. Commercial Property Insurance growing fastest.

In 2025, the Liability Insurance segment contributed 35% to the Commercial Insurance Market revenue, emphasizing its importance in safeguarding businesses against lawsuits and financial risks. This segment provides various types of insurance policies, such as general liability, professional indemnity, and product liability insurance, to suit different industries. Companies such as Beazley plc have been at the forefront in offering specialized products in liability insurance that meet the emerging risks. For instance, the entry of Beazley plc into the cyber liability insurance market shows the growing need for protection against cyber risks. The need for liability insurance is also shown by the increasing number of litigation cases and tough regulatory environments, which make organizations seek protection.

The Commercial Property Insurance segment has been receiving a great recognition. It is projected to witness a CAGR of 9.21% over the forecast period mainly because of the growing awareness for protection of asset from potential cause of loss of property due to natural hazards and unexpected events. Organizations are adapting to this increased demand; in April of 2023, Arch Insurance acquired Thimble, providing on-demand insurance solutions for small businesses. IT & Telecom growing fastest

By Industrial Vertical, Transportation & Logistics dominated in 2025 with 22% revenue share. IT & Telecom growing fastest.

In 2025, the Transportation & Logistics industry topped the Commercial Insurance Market with a 22% revenue share, emphasizing its dependence on comprehensive insurance solutions. This industry is exposed to diverse risks, ranging from cargo damage to challenges in regulatory compliance. The industry's response is being met with specialized insurance products; for example, Beazley plc has designed customized insurance coverage that specifically targets the needs of logistics firms. The industry's expansion is also fueled by the global rise of e-commerce and supply chain complexities, which require effective insurance structures.

The IT & Telecom industry is projected to record the highest CAGR of 8.59% in the Commercial Insurance Market over the forecast period. This is because the industry is becoming increasingly susceptible to cyber attacks, data breaches, and technology disruptions. The industry's reaction is being met with innovative insurance offerings; for instance, Beazley plc launched Beazley Security in 2024, which offers comprehensive cyber risk management solutions, including managed detection and response services. With the increasing pace of digitalization and increased regulatory pressures, IT and telecom firms are increasingly focusing on comprehensive insurance protection to safeguard against potential risks.

Commercial Insurance Market Regional Analysis

North America Commercial Insurance Market Insights

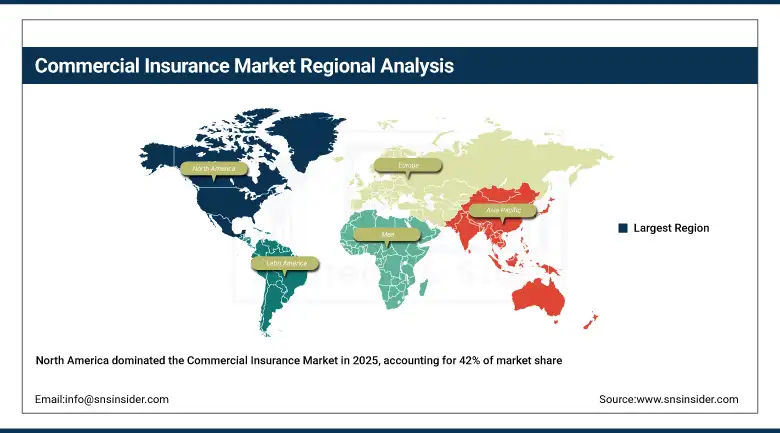

In the year 2025, the North America region was leading the Commercial Insurance Market with a predicted market share of approximately 42%. This is because of the presence of prominent insurance companies such as Chubb Limited, AIG, and Marsh & McLennan, along with a well-organized regulatory framework and ecosystem. The strong economy and adoption of commercial insurance offerings in the construction, healthcare, manufacturing, and logistics sectors have been some of the key driving factors in the market. Moreover, the increasing demand for specialized insurance offerings such as cyber liability insurance, environmental liability insurance, and professional indemnity insurance is encouraging organizations to expand their offerings. For example, in 2024, AIG introduced their cyber insurance offerings specifically for SMEs in North America, thus further cementing the region’s dominant position in the global market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Commercial Insurance Market Insights

The Asia-Pacific region is emerging as the fastest-growing market for commercial insurance, with an estimated CAGR of 11.55% during the forecast period 2026-2035. The main factors that have contributed to this growth are rapid urbanization, industrialization, and growing awareness of risk management among businesses. Countries like China, India, and Southeast Asia are experiencing a rise in the adoption of commercial insurance products. For example, in 2023, AXA and Allianz have extended their commercial insurance offerings in the Asia-Pacific region using digital platforms to target the underinsured SMEs and startups. The Asia-Pacific region’s dynamic business environment and rising investments in infrastructure and technology are creating lucrative opportunities for commercial insurers.

Europe Commercial Insurance Market Insights

Europe leads the Commercial Insurance Market due to the established insurance system and the presence of a large number of multinational companies. Effective regulations, sophisticated risk management techniques, and growing demand for property, liability, and specialty insurance drive the market. The adoption of digital insurance platforms and innovations in product development improves customer accessibility and efficiency. Growing awareness of risk mitigation and corporate compliance further drives the market across Western and Northern Europe.

Middle East & Africa and Latin America Commercial Insurance Market Insights

The Middle East & Africa and Latin America Commercial Insurance Markets are witnessing steady growth driven by increasing industrialization, infrastructure development, and foreign investments. Rising awareness of risk management and regulatory compliance is boosting demand for commercial insurance solutions. Additionally, digitalization and tailored insurance products are improving accessibility and adoption. Expansion in sectors like construction, energy, and transportation further fuels market growth, making these regions attractive for insurance providers seeking emerging opportunities.

Commercial Insurance Market Competitive Landscape:

AIG

AIG, founded in 1919 and headquartered in New York, is a global insurance and financial services company offering life, property, casualty, and retirement solutions. The company provides a diverse portfolio of products to individuals, businesses, and institutions worldwide. With a strategic focus on core U.S. operations, risk management, and financial stability, AIG continues to optimize its global portfolio while maintaining leadership in insurance and retirement solutions.

-

September 2023: AIG's subsidiary, Corebridge Financial, agreed to sell its UK life insurance business, AIG Life Limited, to Aviva plc for £460 million. This divestiture is part of AIG's strategy to streamline its portfolio and focus on core U.S. life and retirement solutions.

Aon plc

Aon, founded in 1982 and headquartered in London, UK, is a leading global professional services firm providing risk management, insurance brokerage, and human capital solutions. The company focuses on designing innovative risk transfer and consulting solutions for businesses, governments, and nonprofits. Aon supports large-scale risk mitigation, insurance programs, and strategic advisory services worldwide, helping clients manage uncertainty, improve resilience, and capitalize on growth opportunities in diverse industries and emerging Commercial Insurance Markets.

-

June 2023: Aon, in collaboration with the U.S. International Development Finance Corporation, launched a USD 350 million war risk insurance scheme to support Ukrainian businesses. This initiative includes a $50 million reinsurance facility and $300 million coverage for projects in healthcare and agriculture, aiming to bolster Ukraine's wartime economy and reconstruction efforts.

Aviva plc

Aviva plc, founded in 1696 and headquartered in London, UK, is a multinational insurance company offering life, general, health, and pensions products. Aviva serves millions of customers across the UK, Europe, and Asia, providing innovative insurance solutions and risk management services. With a focus on strategic acquisitions and digital transformation, Aviva aims to expand its Commercial Insurance Market presence, diversify product offerings, and deliver sustainable value to policyholders and shareholders alike.

-

December 2024: Aviva agreed to acquire Direct Line Insurance Group plc for approximately £3.7 billion. This acquisition will create the UK's largest motor insurer, expanding Aviva's footprint in the commercial insurance sector and enhancing its product offerings.

Key Players

-

American International Group Inc.

-

Aon plc

-

Aviva plc

-

Axa S.A.

-

Direct Line Insurance Group plc

-

Marsh & McLennan Companies Inc.

-

Willis Towers Watson Public Limited Company

-

Zurich Insurance Group Ltd.

-

Tokio Marine Holdings, Inc.

-

CNA Financial Corporation

-

Liberty Mutual Insurance Group

-

Hartford Financial Services Group, Inc.

-

Travelers Companies, Inc.

-

Berkshire Hathaway Specialty Insurance

-

Munich Re

-

Sompo Holdings, Inc.

-

Swiss Re Ltd.

-

Generali Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 934.57 Billion |

| Market Size by 2035 | USD 1926.18 Billion |

| CAGR | CAGR of 7.5% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Liability Insurance, Commercial Motor Insurance, Commercial Property Insurance, Marine Insurance, Others) • By Enterprise Size (Large Enterprises, Small & Medium Enterprises [SME]) • By Distribution Channel (Agents & Brokers, Direct Response, Others) • By Industry Vertical (Transportation & Logistics, Manufacturing, Construction, IT & Telecom, Healthcare, Energy & Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles |

Allianz SE, American International Group Inc., Aon plc, Aviva plc, Axa S.A., Chubb Limited, Direct Line Insurance Group plc, Marsh & McLennan Companies Inc., Willis Towers Watson Public Limited Company, Zurich Insurance Group Ltd., Tokio Marine Holdings, Inc., CNA Financial Corporation, Liberty Mutual Insurance Group, Hartford Financial Services Group, Inc., Travelers Companies, Inc., Berkshire Hathaway Specialty Insurance, Munich Re, Sompo Holdings, Inc., Swiss Re Ltd., Generali Group |

Frequently Asked Questions

North America dominated the market in 2025, accounting for approximately 42% of the global Commercial Insurance Market revenue share.

By type, Liability Insurance dominated in 2025 with 35% revenue share, while Commercial Property Insurance is projected to grow fastest in coming years.

Key growth drivers include increasing business risks, digital platforms, AI-driven underwriting, SME expansion, and rising awareness of liability and risk mitigation.

The Commercial Insurance Market was valued at USD 934.57 billion in 2025, reflecting growing demand for liability and tailored insurance solutions.

The Commercial Insurance Market is expected to grow at a CAGR of 7.5% from 2026 to 2035, driven by rising business risks and digital adoption.

Get in Touch