In Vivo CRO Market Report Scope & Overview:

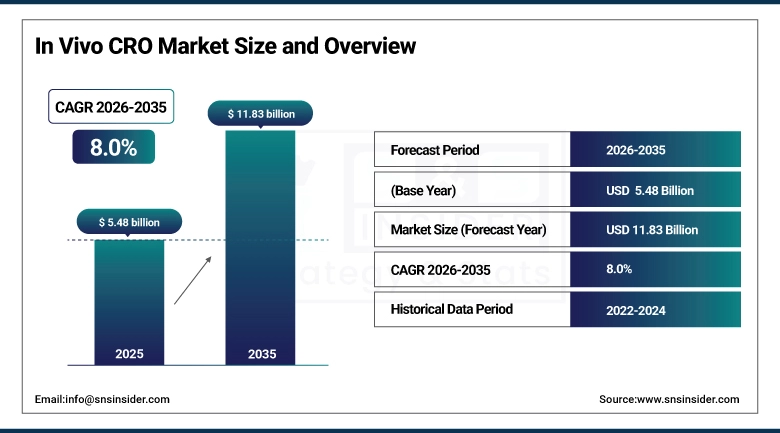

The In Vivo CRO Market was valued at USD 5.48 Billion in 2025 and is expected to reach USD 11.83 Billion by 2035, growing at a CAGR of 8.0% from 2026-2035.

Drug development has always required testing in living systems before any molecule can enter a human clinical trial. That requirement is not a regulatory preference it reflects the irreducible complexity of predicting how a compound will behave inside an organism, where absorption, distribution, metabolism, elimination, and toxicity interact across organ systems in ways that cell cultures and computer models cannot fully replicate. In vivo contract research organizations have built their commercial existence around exactly this necessity: providing the animal models, GLP-compliant facilities, experienced scientific staff, and regulatory expertise that pharmaceutical and biotechnology companies need to generate the preclinical safety and efficacy data that regulatory agencies require before allowing first-in-human trials. The market's growth reflects a broader pharmaceutical industry trend toward outsourcing preclinical work rather than maintaining expensive vivarium infrastructure internally, companies increasingly prefer to contract with specialized CROs who can execute studies more efficiently, at lower fixed cost, and with access to more advanced model systems than any single company could justify building internally.

PhRMA's 2024 annual member survey documents that the U.S. biopharmaceutical industry invested USD 102 billion in R&D in 2023, the largest single-year R&D investment in the industry's history. The NIH invested USD 41.7 billion in research grants in 2023, representing the largest public biomedical research funding program globally and sustaining the academic research ecosystem that generates the early-stage candidates that CROs subsequently advance through preclinical testing.

Market Size and Forecast:

-

Market Size in 2025: USD 5.48 Billion

-

Market Size by 2035: USD 11.83 Billion

-

CAGR: 8.0% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on In Vivo CRO Market - Request Free Sample Report

In Vivo CRO Market Trends:

-

AI-powered in vivo imaging analysis platforms are reducing data processing time for PET, MRI, and fluorescence imaging studies by up to 40%, enabling faster study turnaround without compromising endpoint quality.

-

Genetically engineered and patient-derived xenograft (PDX) mouse models are becoming the standard for oncology drug efficacy studies, enabling more clinically predictive cancer models than conventional cell-line xenograft approaches.

-

Humanized mouse models engrafted with human immune systems or specific human tissue types are expanding the translational relevance of in vivo immunology and infectious disease studies for biologics and cell therapy developers.

-

GLP toxicology demand is increasing as more drug candidates reach IND-enabling stages, driven by the growing pipeline of oncology, rare disease, and gene therapy programs requiring regulatory-grade safety packages.

-

3Rs (Replacement, Reduction, Refinement) regulatory pressure in the EU and progressively in the U.S. is driving CROs to invest in advanced in vitro and computational methods that reduce animal use while maintaining study quality.

-

Outsourcing penetration is expanding beyond large pharma into mid-size biotechs and academic spinouts whose asset portfolios require CRO support but whose fixed-cost structures cannot support internal preclinical infrastructure.

-

India and China are emerging as significant in vivo CRO geographies, attracting Western pharmaceutical companies with lower operational costs, skilled scientific workforces, and improving regulatory infrastructure.

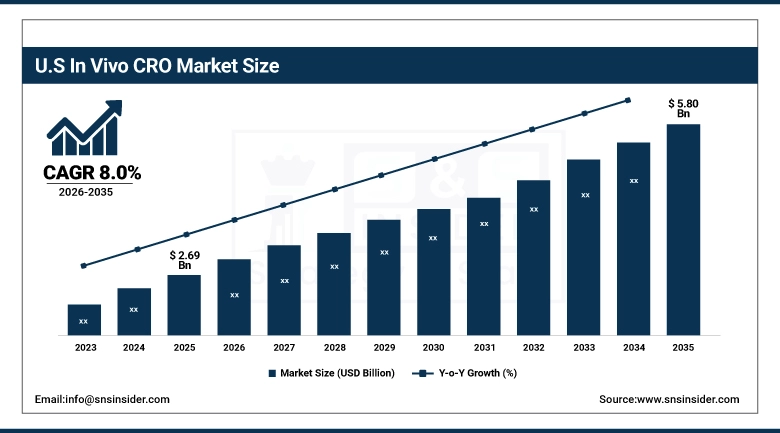

U.S. In Vivo CRO Market was valued at USD 2.69 Billion in 2025 and is expected to reach USD 5.80 Billion by 2035, growing at a CAGR of 8.0% from 2026-2035.

North America dominated the global In Vivo CRO Market with approximately 49% of revenue in 2025, anchored by the United States' extraordinary pharmaceutical and biotechnology R&D ecosystem. The U.S. biopharmaceutical sector with its global headquarters concentration, largest drug development pipeline, and highest drug approval volume generates the world's highest volume of in vivo CRO procurement. Charles River Laboratories, Covance (Labcorp Drug Development), and Envigo each maintain large-scale preclinical research facilities in the U.S. that serve domestic pharmaceutical company clients. The NIH's USD 41.7 billion research budget sustains academic research institutions that run their own in vivo programs and generate the early-stage candidates that commercial CROs later advance through IND-enabling studies.

The FDA's Center for Drug Evaluation and Research approved 55 novel drugs in 2023, each requiring comprehensive in vivo preclinical safety packages that sustained CRO demand. PhRMA data documents that the average biopharmaceutical company invests 10-15 years and USD 2.6 billion to bring a new drug from discovery to approval, with preclinical in vivo testing representing 2-4 years of that timeline.

In Vivo CRO Market Segment Analysis:

-

By Model Type, Rodent-based segment dominated with 80% share in 2025; Non-rodent models growing for higher translational accuracy and regulatory validation studies.

-

By Modality, Small Molecules dominated the market in 2025; Cell & Gene Therapy growing fastest driven by rising demand for advanced biologics and precision therapies.

-

By Indication, Oncology dominated the market in 2025; CNS Conditions and Autoimmune disorders growing due to increasing chronic disease burden and R&D focus.

-

By GLP Type, GLP Toxicology dominated the In Vivo CRO Market in 2025; Non-GLP studies growing with early-stage pipeline expansion.

By Model Type: Rodent-based dominates, Non-rodent expanding for translational and regulatory needs

The rodent-based segment dominated the In Vivo CRO Market in 2025, accounting for nearly 80% share due to its cost-effectiveness, well-established biological relevance, and widespread regulatory acceptance in preclinical research. Rodent models, particularly mice and rats, are extensively used in pharmacokinetics, toxicology, and disease modeling studies, making them the backbone of early-stage drug development pipelines. Their short life cycles, genetic manipulability, and availability of transgenic variants further strengthen their dominance across pharmaceutical and biotechnology research.

However, non-rodent models such as canines, non-human primates, and minipigs are gaining traction as demand rises for higher translational accuracy and regulatory validation in advanced therapeutic areas. These models are increasingly utilized in complex biologics, immunology, and safety assessment studies where rodent data alone is insufficient for clinical predictability..

By Modality: Small Molecules dominate, Cell & Gene Therapy accelerating with advanced pipelines

Small molecules dominated the In Vivo CRO Market in 2025, supported by their long-standing presence in drug discovery pipelines, cost efficiency, and well-defined pharmacological pathways. These compounds remain the primary focus of pharmaceutical development due to established synthesis methods, predictable absorption and metabolism profiles, and broad therapeutic applicability across chronic and acute diseases.

However, cell and gene therapy is emerging as the fastest-growing modality, driven by increasing investment in precision medicine, regenerative therapies, and targeted treatment approaches for previously incurable diseases. The complexity of biologics, including CAR-T therapies, viral vector-based treatments, and genome editing technologies, is accelerating demand for specialized in vivo CRO services. These studies require advanced animal models and highly controlled environments to evaluate efficacy, safety, and long-term therapeutic outcomes.

By Indication: Oncology leads, CNS and Autoimmune conditions expanding with rising disease burden

Oncology dominated the In Vivo CRO Market in 2025 due to the high global cancer burden, continuous pipeline expansion, and strong funding support for anti-cancer drug development. In vivo studies play a critical role in tumor modeling, efficacy validation, and toxicity profiling for novel oncology therapeutics, including immunotherapies and targeted agents.

However, CNS disorders and autoimmune diseases are witnessing rapid growth driven by rising prevalence of neurological conditions such as Alzheimer’s, Parkinson’s, and depression, along with increasing autoimmune disorder incidence globally. These complex disease areas require sophisticated in vivo models to better understand disease progression and therapeutic response. Pharmaceutical companies are intensifying R&D efforts in these segments, leading to higher outsourcing of preclinical testing to CROs with specialized expertise in neurobiology and immunology.

By GLP Type: GLP Toxicology dominates, Non-GLP studies expanding with early-stage innovation

GLP toxicology dominated the In Vivo CRO Market in 2025, as regulatory-compliant safety studies are mandatory for drug approval processes across global regulatory agencies such as the FDA and EMA. These studies ensure that new drug candidates meet strict safety standards before progressing to clinical trials, making them a critical component of the pharmaceutical development lifecycle. GLP-compliant studies are widely outsourced to CROs due to their requirement for specialized infrastructure, standardized protocols, and regulatory expertise.

Meanwhile, non-GLP studies are growing steadily, driven by increased early-stage drug discovery activity and the expansion of preclinical pipelines in biotech and academic research. These studies offer flexibility, faster turnaround times, and cost advantages, supporting exploratory research, proof-of-concept validation, and early efficacy screening before formal regulatory testing begins.

Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

91% |

|

Europe |

United Kingdom |

28% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

Israel |

40% |

|

Latin America |

Brazil |

50% |

North America In Vivo CRO Market Insights:

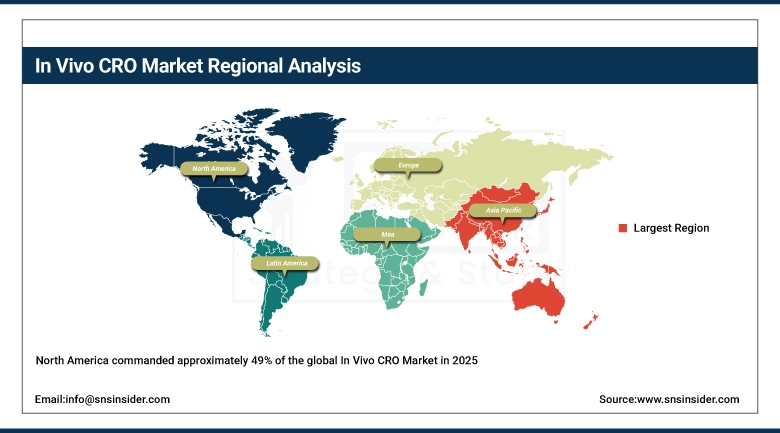

North America commanded approximately 49% of the global In Vivo CRO Market in 2025, a position sustained by the world's highest pharmaceutical R&D investment, the densest concentration of drug development companies from discovery-stage biotechs to global pharmaceutical leaders, and the presence of industry-leading CRO organizations including Charles River Laboratories and Labcorp Drug Development. The U.S. market's unique characteristic is its clinical trial activity level: with the FDA approving more novel drugs than any other regulatory agency and the U.S. biotech sector leading global venture investment, the pipeline of compounds requiring preclinical in vivo packages is both the largest and the fastest-growing of any national market. Boston, San Francisco, San Diego, and the Research Triangle Park are geographic hubs where CRO service providers co-locate with the pharmaceutical companies whose programs drive their business.

In January 2024, Labcorp Drug Development announced the launch of a new GLP-compliant toxicology testing facility in the U.S. to meet growing demand for preclinical safety studies an investment reflecting the capacity pressures that growing pharmaceutical pipeline volumes place on GLP CRO providers.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific In Vivo CRO Market Insights:

Asia Pacific is the fastest-growing regional In Vivo CRO Market, with India expected to register the highest country-level CAGR in the region through the forecast period. India's combination of experienced scientific talent, operational cost advantages of 40-60% below U.S. levels, improving regulatory infrastructure, and government support through 'Pharma Vision' programs is attracting increasing outsourcing from global pharmaceutical companies seeking cost-effective preclinical execution. China's 'Healthy China 2030' initiative and the country's investment in domestic biomedical research infrastructure are supporting the growth of Chinese CROs including WuXi AppTec, which has become one of the world's largest CRO organizations from its base in Shanghai. Japan and South Korea contribute sophisticated oncology and biologics preclinical expertise to the regional market.

China increased biomedical research funding by 20% in 2023 according to the National Natural Science Foundation of China data. India saw a 15% increase in pharma R&D investment in 2023, sustaining the demand growth that in vivo CROs serving Indian pharmaceutical clients are experiencing.

Europe In Vivo CRO Market Insights:

Europe holds a significant In Vivo CRO Market share, with the UK, Germany, France, and Switzerland as primary national markets. European CRO operations serve both domestic pharmaceutical industry clients and U.S. companies seeking geographic diversification of their preclinical programs. The EU's 3Rs regulatory framework which requires justification of every animal used and encourages reduction in animal study numbers is more stringent than U.S. requirements, pushing European CROs to develop more sophisticated in vitro and computational alternative methods alongside their in vivo programs. European CROs including Envigo, Evotec, and Janvier Labs serve the continent's pharmaceutical industry from established vivarium and laboratory facilities.

Middle East & Africa and Latin America In Vivo CRO Market Insights:

Middle East & Africa (MEA) and Latin America are two emerging but growing geographies in the In Vivo CRO Market, as their healthcare infrastructure is gradually improving along with opportunity for pharmaceutical R&D activity due to a concentrated size of global companies seeking comparatively lower cost and slow-growing internationally-diverse outsourcing destination. Although both regions currently possess smaller market shares compared to North America and Europe, they are growing in strategic importance driven by cost advantages, deepening pools of scientific talent, and government policy support for strengthening life sciences ecosystems.

The MEA region is expected to emerge as a region having high market growth led by countries such as the UAE, Saudi Arabia and South Africa seeking to transform their national healthcare framework through increasing investment in biomedical research coupled with rising demand for preclinical and translational studies especially in biologics, vaccines and infectious diseases. The Vision 2030 initiative is attracting the establishment of new infrastructure and proposals for international collaborations, although limited capacity in terms of CRO resources will still be a challenge, as will variability of regulation across regions.

In Latin America, equally with Brazil, Mexico and Argentina lead the regional forefront, backed by expanding pharmaceutical industries, reconstructing regulatory atmospheres, and increasing clinical trial action. Brazil is the top leader by virtue of its domestic pharma base, while Mexico offers advantage over proximity to the U.S., encouraging cross-border research. The CRO sectors in both geographical regions are expanding gradually, with global and regional players competing for market share by capitalizing on cost advantages and access to a wide range of research environments. MEA and Latin America are emerging as important complementing markets for preclinical outsourcing barring some issues like economic volatility, regulatory fragmentation, and infrastructure gaps on the ground especially for early-stage research and for region-specific studies that require performing animal tests.

Market Growth Drivers: Pharmaceutical pipeline expansion and preclinical outsourcing adoption driving sustained in vivo CRO market growth globally

The fundamental commercial logic of the in vivo CRO market is that pharmaceutical companies have discovered it is more efficient to outsource preclinical testing to specialized providers than to maintain the complex, expensive infrastructure required to run high-quality in vivo studies internally. Running a GLP-compliant vivarium requires dedicated animal care staff, specialized facility design meeting regulatory standards, quality assurance programs, and continuous documentation that represents significant fixed cost regardless of study volume fluctuations. A CRO that runs these facilities at scale across multiple clients achieves utilization economics that any single pharmaceutical company cannot match with its own infrastructure. This outsourcing logic has progressively extended to more study types from simple acute toxicology to complex chronic studies and specialized efficacy models as CRO capability has expanded and pharmaceutical company comfort with outsourcing has grown. The expanding oncology pipeline which accounts for approximately 25% of in vivo CRO market volume is a particularly powerful demand driver, as each oncology drug candidate requires extensive efficacy validation in tumor models alongside its safety toxicology package.

Market Restraints: Regulatory stringency and animal welfare legislation creating compliance challenges for in vivo CRO market participants

In vivo CRO operations face regulatory requirements that are among the most demanding of any contract research service sector. GLP compliance requires meticulous study conduct documentation, equipment calibration records, personnel training files, and quality assurance audit programs that add significant operational overhead relative to non-GLP laboratory operations. Animal welfare regulations USDA’s Animal Welfare Act in the U.S. and the EU's Directive 2010/63/EU impose facility design, veterinary care, and study protocol review requirements that limit operational flexibility. The growing regulatory and public pressure to reduce animal use in research while scientifically justified in many contexts creates a tension with the pharmaceutical industry's continuing requirement for in vivo safety data that regulatory agencies require before permitting human clinical trials.

Market Opportunities: Emerging market expansion and advanced animal model innovation creating significant in vivo CRO growth opportunities globally

Humanized animal models mice engrafted with human immune systems, human liver cells, or human tumor tissue represent the in vivo CRO market's most commercially valuable innovation frontier. These models bridge the gap between conventional mouse biology and human therapeutic response in ways that standard inbred strains cannot, enabling pharmacological studies in contexts that are genuinely predictive of clinical outcomes for biologics, cell therapies, and cancer immunotherapy. The growing pipeline of immuno-oncology drugs checkpoint inhibitors, CAR-T therapies, bispecific T-cell engagers requires humanized immune system models for efficacy testing because standard immunocompetent mouse immune systems respond differently to human-targeted therapies than human immune systems do. CROs that develop and maintain validated humanized model platforms command premium pricing and sustained competitive differentiation.

Recent Developments:

-

2025: Charles River Laboratories expanded its portfolio of CRISPR-engineered disease models for rare disease preclinical research, adding 45 new validated mouse models covering inherited metabolic, neurological, and cardiovascular conditions enabling pharmaceutical companies working in rare disease therapeutic areas to access characterized disease models without the 12-18 month development timeline required to create custom models independently.

-

2025: WuXi AppTec launched a dedicated GLP toxicology expansion at its Suzhou facility, adding 200,000 square feet of AAALAC-accredited vivarium and laboratory space to meet growing demand from global pharmaceutical clients for GLP-compliant toxicology services in Asia, reporting full booking of new capacity within six months of commissioning.

-

2026: Labcorp Drug Development introduced an AI-powered in vivo imaging analysis platform that reduces histopathology slide scoring time by 45% through automated lesion detection and classification, enabling faster pathology report generation for GLP toxicology studies without reducing the expert pathologist oversight that regulatory agencies require for GLP-compliant histopathology endpoints.

In Vivo CRO Market Key Players:

-

Labcorp Drug Development (Covance)

-

WuXi AppTec Co. Ltd.

-

Envigo (Inotiv)

-

Medpace Holdings Inc.

-

PRA Health Sciences (ICON)

-

Syneos Health Inc.

-

PPD (Pharmaceutical Product Development)

-

Crown Bioscience (JSR)

-

Taconic Biosciences Inc.

-

The Jackson Laboratory

-

Champions Oncology Inc.

-

GemPharmatech Co. Ltd.

-

Biocytogen Pharmaceuticals Ltd.

-

Evotec SE

-

Calvert Laboratories

-

EPL Bio Analytical Services

-

BioAnalytical Systems Inc. (BAS)

In Vivo CRO Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.48 Billion |

| Market Size by 2035 | USD 11.83 Billion |

| CAGR | CAGR of 8.0% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Model Type (Rodent based, Non-Rodent base) • By Indication (Oncology, CNS Conditions, Diabetes, Obesity, Pain management, Autoimmune/inflammation conditions, Others) • By Modality (Small Molecules, Large Molecules) • By GLP Type (GLP Toxicology, Non GLP) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Charles River Laboratories International Inc., Labcorp Drug Development (Covance), ICON plc, WuXi AppTec Co. Ltd., Envigo (Inotiv), Eurofins Scientific SE, Medpace Holdings Inc., PRA Health Sciences (ICON), Syneos Health Inc., PPD (Pharmaceutical Product Development), Crown Bioscience (JSR), Taconic Biosciences Inc., The Jackson Laboratory, Champions Oncology Inc., GemPharmatech Co. Ltd., Biocytogen Pharmaceuticals Ltd., Evotec SE, Calvert Laboratories, EPL Bio Analytical Services, BioAnalytical Systems Inc. (BAS). |

Frequently Asked Questions

Asia Pacific is expected to register the fastest CAGR, with India projected to have the highest CAGR within the region.

North America dominated the In Vivo CRO Market with approximately 49% share in 2025.

Rodent-based models dominated with approximately 80% share in 2025.

The In Vivo CRO Market was valued at USD 5.48 billion in 2025.

The In Vivo CRO Market is expected to grow at a CAGR of 8.0% from 2026 to 2035.

Get in Touch