Inductor Market Report Scope & Overview:

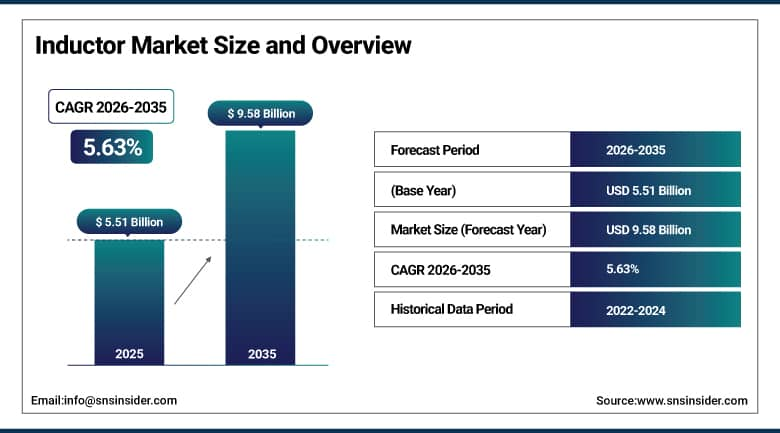

The Inductor Market was valued at USD 5.51 Billion in 2025 and is expected to reach USD 9.58 Billion by 2035, growing at a CAGR of 5.63% from 2026 to 2035.

The global inductor market is experiencing sustained and robust growth, driven by the expanding demand for compact, energy-efficient electronic components, and industrial automation applications. The market’s commercial expansion is propelled by the simultaneous advancement of multiple high-growth technology platforms, including the proliferation of 5G telecommunications infrastructure, low-loss RF inductors for base station and device applications, the extraordinary growth of electric vehicles, and the continuing miniaturization of consumer electronics. The trend toward surface-mount technology in electronic assembly is simultaneously driving multilayer and film-type inductor adoption whose compatibility with automated surface-mount assembly processes sustains volume procurement growth across the global electronics manufacturing base concentrated in Asia Pacific.

In January 2025, Murata Manufacturing Co. Ltd. introduced the world’s smallest 006003-inch size chip inductor measuring 0.16 mm x 0.08 mm, reducing volume by 75% compared to its predecessor. This breakthrough supports the miniaturization needs of mobile devices with high-density mounting requirements, enabling smartphone and wearable manufacturers to achieve higher circuit density without sacrificing the inductive component performance required for power regulation and signal filtering in next-generation ultra-thin consumer electronics.

Market Size and Forecast:

-

Market Size in 2026E: USD 5.82 Billion

-

Market Size by 2035: USD 9.58 Billion

-

CAGR: 5.63% from 2026 to 2035

-

Fastest Growing Application: Automotive

-

Largest Region: Asia Pacific

To Get More Information On Inductor Market - Request Free Sample Report

Inductor Market Trends:

-

Multilayer inductor miniaturization is supporting compact designs in smartphones, wearables, and IoT electronic devices.

-

Electric vehicle growth is increasing demand for high-current inductors used in power electronics systems.

-

Global 5G deployment is driving strong demand for RF inductors across infrastructure and connected devices.

-

Wide-bandgap semiconductor adoption is accelerating development of low-loss inductors for high-frequency power applications.

-

ADAS, V2X communication, and infotainment systems are increasing inductor content in modern vehicles.

U.S. Inductor Market Outlook:

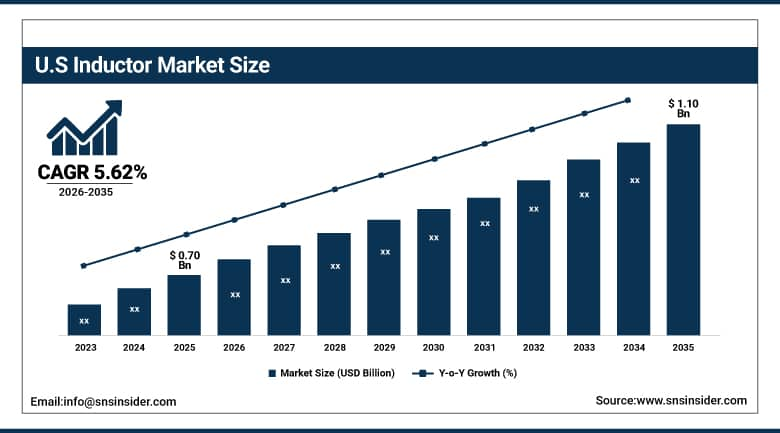

The U.S. Inductor Market was valued at approximately USD 0.70 Billion in 2025 and is expected to reach approximately USD 1.10 Billion by 2035, growing at a CAGR of approximately 5.62%.

The U.S. is the most commercially significant inductor market within North America, driven by high adoption of smartphones and tablets, the extraordinary growth of electric vehicle production including Tesla, GM, and Ford’s EV programmes, industrial automation investment, and the concentration of defense electronics procurement that creates above-average high-reliability inductor specification. Coilcraft, Vishay Intertechnology, Bourns, and Bel Fuse define the domestic commercial landscape alongside the U.S. operations of Japanese and Taiwanese inductor manufacturers. The U.S. government’s CHIPS Act investment in domestic semiconductor manufacturing creates inductor procurement growth for the passive component supply chains that support semiconductor fabrication equipment and chip testing systems.

In March 2025, TDK Corporation launched the ADL3225VF series automotive power-over-coax inductors supporting up to 1,600 mA and a wide frequency range, targeting advanced driver-assistance system applications in automotive electronics. The product demonstrates the commercial direction of automotive inductor development toward higher current capacity, wider frequency range, and improved reliability specifications that the growing ADAS content per vehicle and the transition to software-defined vehicle architectures require.

Inductor Market Segment Analysis:

-

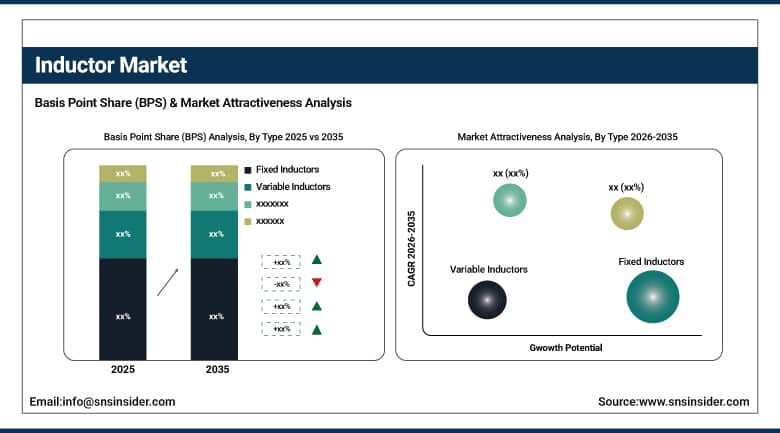

By Type, the Fixed Inductors segment dominated the Inductor Market with the largest revenue share in 2025, while the Multilayered Inductors sub-segment is the fastest growing.

-

By Core Material, the Ferromagnetic/Ferrite Core segment dominated the Inductor Market with the largest revenue share in 2025, while the Air Core segment is the fastest growing as growing.

-

By Shielding, Shielded segment dominated the Inductor Market with the 62.4% share in 2025 and is also the fastest growing market.

-

By Application, the Consumer Electronics segment dominated the Inductor Market with approximately 36.5% share in 2025, while the Automotive segment is the fastest growing.

By Type, fixed inductors dominate, multilayered grows fastest

Fixed inductors retained the dominant type position with the largest revenue share of the inductor market in 2025. The commercial primacy of fixed inductors reflects their universal applicability across the complete range of electronic applications. Wire wound inductors’ high inductance value capability and current handling capacity sustain their dominance in power electronics and industrial applications, while multilayer inductors’ compact form factor serves miniaturized consumer electronics and telecommunication applications simultaneously. The surface-mount fixed inductor’s compatibility with automated assembly processes creates procurement preference in high-volume electronics manufacturing whose per-unit cost reduction from automated assembly sustains fixed inductor specification above through-hole alternatives.

Multilayer inductors are the fastest growing sub-segment because the extraordinary miniaturization trend in consumer electronics, wearables, and IoT devices creates design requirements for the smallest possible inductor footprint that provides adequate inductance value. Murata Manufacturing’s January 2025 launch of the world’s smallest 006003-inch chip inductor, reducing volume by 75%, demonstrates the commercial innovation trajectory whose miniaturization achievement creates new design possibilities for ultra-compact consumer electronic products. The 5G device proliferation creating demand for smaller, higher-frequency multilayer inductors in smartphone front-end modules compounds with wearable device growth to sustain the sub-segment’s fastest-growing designation.

By Application, consumer electronics dominates, automotive grows fastest

Consumer electronics retained the dominant application position with approximately 36.5% of the inductor market in 2025. The commercial primacy of consumer electronics reflects the extraordinary volume of smartphones, tablets, laptops, wearables, and smart home devices whose per-device inductor content creates cumulative procurement that no other application vertical approaches in aggregate annual volume. Each new smartphone generation that integrates power management inductors for charging, audio, and display circuits, multilayer RF inductors for antenna switching and signal conditioning, and coupled inductors for wireless charging creates inductor procurement proportional to global smartphone shipments of approximately 1.3 billion units annually.

Automotive is the fastest growing application because the unprecedented expansion of electric vehicle production creates new high-current power inductor demand categories that previous internal combustion engine vehicle content did not include at comparable volume or specification. Each electric vehicle’s traction inverter, onboard AC charger, DC-DC converter system, and battery management electronics require high-current, high-frequency power inductors whose specification requirements create premium product procurement above the commodity inductor pricing of consumer electronics applications. The automotive segment’s growth trajectory from EV production expansion, ADAS radar sensor proliferation, and connected vehicle communication module deployment creates structural above-market inductor procurement growth through the forecast period.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Israel |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Inductor Market Insights

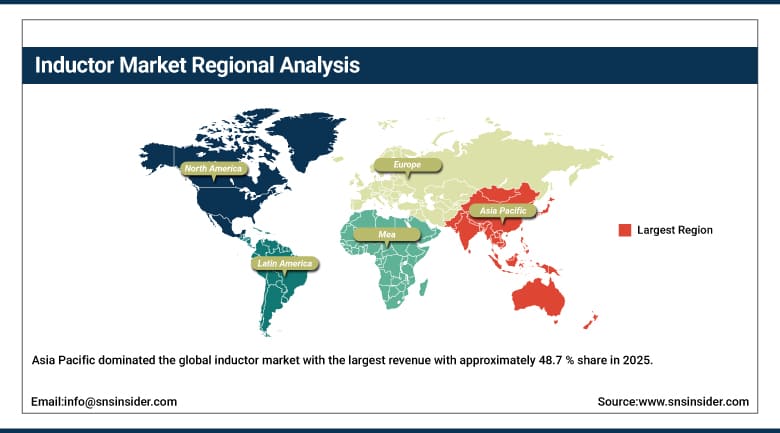

Asia Pacific dominated the global inductor market with the largest revenue with approximately 48.7 % share in 2025, driven by the world’s most concentrated electronics manufacturing base in China, Japan, South Korea, and Taiwan, the presence of leading inductor manufacturers including Murata, TDK, Taiyo Yuden, Chilisin, and Sunlord, and the extraordinary consumer electronics and EV production volumes that create the highest per-region inductor procurement globally. China accounts for approximately 44.8% of Asia Pacific revenues through its electronics manufacturing concentration, EV production leadership, and the government’s Made in China 2025 electronics industry investment.

India is expected to witness the highest CAGR within Asia Pacific through the government’s Production Linked Incentive scheme for electronics manufacturing, the growing smartphone assembly sector, and the emerging domestic EV production programme creating local component procurement.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Inductor Market Insights

North America represents the second-largest regional market for inductors, supported by strong demand from industrial automation, advanced manufacturing, consumer electronics, electric vehicles, aerospace, and defense applications. The region benefits from extensive adoption of smartphones, tablets, connected devices, and high-performance computing infrastructure, which require sophisticated inductor components for power management and signal processing. The United States dominates the regional market, accounting for approximately 87.4% of North American revenues, driven by the presence of major industry participants such as Coilcraft, Vishay, Bourns, and Bel Fuse, alongside substantial procurement from leading Japanese and Taiwanese component manufacturers. Growing investments in EV production, renewable energy systems, 5G infrastructure deployment, and defense electronics modernization continue to strengthen demand for advanced inductor technologies.

Canada contributes approximately 12.6% of North American revenues through its consumer electronics market, the automotive manufacturing sector’s component procurement, and the growing industrial automation investment creating power inductor demand.

Europe Inductor Market Insights

Europe is a technically sophisticated inductor market where the automotive industry’s EV and ADAS transition creates above-average automotive inductor demand growth, the industrial automation sector’s drive for efficiency creates power inductor investment, and TDK’s German operations sustain European supply capability. Germany accounts for approximately 22.3% of European revenues through its automotive manufacturing sector’s inductor procurement, Siemens’ industrial electronics investment, and the growing renewable energy sector’s power electronics inductor demand.

The United Kingdom, France, and the Nordic countries are significant secondary markets where automotive electrification, industrial IoT deployment, and 5G network build-out create consistent inductor procurement from established electronics procurement bases.

MEA & Latin America Inductor Market Insights

Israel leads MEA revenues at approximately 31.2% through its advanced semiconductor and defense electronics sector’s precision inductor procurement, the growing technology startup ecosystem’s electronic product development, and medical device manufacturing’s specialty inductor demand. UAE’s growing electronics manufacturing sector adds Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its consumer electronics market, the automotive manufacturing sector’s component procurement, and the growing industrial automation investment. Mexico’s automotive manufacturing exports and Argentina’s electronics sector collectively sustain regional market development through 2035.

Market Dynamics:

Growth Drivers: Rising EV production and expanding 5G infrastructure deployment

Electric vehicle production expansion is the inductor market’s most commercially significant structural growth driver beyond the baseline consumer electronics demand trajectory. Each EV’s traction inverter power electronics, onboard charger system, DC-DC converter, and battery management control unit require high-current, high-frequency power inductors whose specification requirements and commercial value per unit substantially exceed equivalent consumer electronics inductor alternatives. Global EV production growing from approximately 10 million vehicles in 2022 toward 30 to 40 million annually by 2030 creates automotive power inductor demand whose commercial aggregate sustains above-market inductor market growth through the automotive transition.

5G infrastructure deployment sustaining RF inductor procurement creates consistent above-baseline demand growth as base station radio units, massive MIMO antenna systems, and small cell deployment each require multiple high-frequency RF inductors whose aggregate per-base-station procurement creates commercial volume proportional to the global 5G base station installation rate.

Restraints: Raw material price volatility and miniaturization complexity increasing manufacturing cost

Raw material price volatility for ferrite core materials, copper winding wire, and rare earth elements used in high-performance inductor cores creates manufacturing cost unpredictability that moderates pricing stability for inductor procurement across long-duration supply contracts. Each commodity price spike that creates inductor average selling price elevation moderates demand from cost-sensitive consumer electronics manufacturers whose bill of materials optimization creates specification substitution pressure.

Miniaturization complexity as inductor dimensions continue shrinking toward sub-millimeter scales creates manufacturing process challenges whose yield improvement investment and specialized equipment requirements concentrate production capability in leading manufacturers, creating supply chain concentration risk for customers in electronics markets that require the smallest available inductor formats.

Opportunities: Wide bandgap semiconductor integration and IoT device proliferation

Wide bandgap semiconductor integration with inductors represents the most technically demanding and commercially premium near-term opportunity whose Silicon Carbide and Gallium Nitride device switching frequency requirements create new high-frequency, low-loss power inductor specifications that command premium pricing above conventional ferrite core alternatives. Each power conversion system that transitions from silicon to wide bandgap semiconductors creates inductor procurement whose advanced core material and winding design requirements sustain above-commodity pricing.

IoT device proliferation creating above-average multilayer inductor demand from billions of connected sensors, smart home devices, and industrial monitoring nodes whose ultra-compact form factor and ultra-low power requirements create specification demand for the most advanced miniaturized inductor products sustains above-average market growth through the forecast period.

Recent Developments:

-

2026: Murata Manufacturing Co., Ltd. expanded production capacity for high-frequency multilayer inductors to support increasing demand from AI servers, 5G infrastructure, and automotive electronics.

-

2026: YAGEO Corporation increased investments in automotive-grade passive component manufacturing, including inductors targeted at EV powertrain and industrial automation applications.

-

2025: TDK Corporation launched next-generation compact power inductors for electric vehicles and ADAS applications, offering enhanced current handling and improved power efficiency.

-

2025: Taiyo Yuden Co., Ltd. introduced ultra-miniaturized multilayer inductors designed for smartphones, wearables, and compact consumer electronics requiring high-density circuit integration.

Inductor Market Key Players are:

-

Murata Manufacturing Co., Ltd.

-

TDK Corporation

-

Taiyo Yuden Co., Ltd.

-

Vishay Intertechnology, Inc.

-

Coilcraft, Inc.

-

Delta Electronics, Inc.

-

Chilisin Electronics Corp.

-

Sumida Corporation

-

Panasonic Corporation

-

ABC Taiwan Electronics Corp.

-

Shenzhen Sunlord Electronics Co., Ltd.

-

Bourns, Inc.

-

Bel Fuse Inc.

-

YAGEO Corporation

-

Pulse Electronics, Inc.

-

Eaton Corporation

-

Cyntec Co., Ltd.

-

Samsung Electro-Mechanics Co., Ltd.

-

Wurth Elektronik Group

-

ICE Components, Inc.

Inductor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.51 Billion |

| Market Size by 2035 | USD 9.58 Billion |

| CAGR | CAGR of 5.63% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Fixed Inductors, Variable Inductors) • By Core Material (Ferromagnetic/Ferrite Core, Air Core, Iron Core, Others) • By Shielding (Shielded, Unshielded) • By Application (Consumer Electronics, Automotive, RF & Telecommunication, Industrial, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Murata Manufacturing Co., Ltd., TDK Corporation, Taiyo Yuden Co., Ltd., Vishay Intertechnology, Inc., Coilcraft, Inc., Delta Electronics, Inc., Chilisin Electronics Corp., Sumida Corporation, Panasonic Corporation, ABC Taiwan Electronics Corp., Shenzhen Sunlord Electronics Co., Ltd., Bourns, Inc., Bel Fuse Inc., YAGEO Corporation, Pulse Electronics, Inc., Eaton Corporation, Cyntec Co., Ltd., Samsung Electro-Mechanics Co., Ltd., Wurth Elektronik Group, ICE Components, Inc. |

Frequently Asked Questions

Asia Pacific dominated the Inductor Market in 2025 with the largest revenue share.

The Inductor Market is expected to grow at a CAGR of 5.63% from 2026 to 2035.

The Inductor Market was valued at USD 5.51 Billion in 2025.

Electric vehicle production expansion creating high-current power inductor demand for motor drive, charging, and battery management electronics.

Fixed Inductors dominated the Inductor Market in 2025.

Get in Touch