Wireless Charging Market Report Scope & Overview:

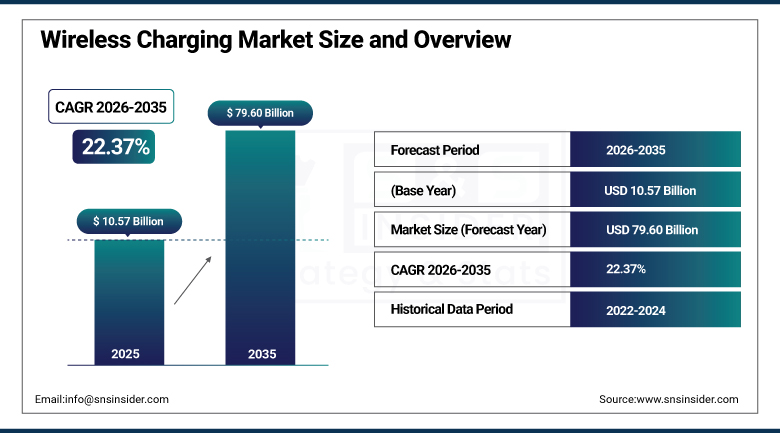

The Wireless Charging Market size was valued at USD 10.57 Billion in 2025 and is expected to reach USD 79.60 Billion by 2035, growing at a CAGR of 22.37% from 2026 to 2035.

The Wireless Charging Market continues to accelerate as contact-free power delivery shifts from a premium convenience to an expected baseline across smartphones, vehicles, and industrial automation platforms. Manufacturing sector players integrating operations with the Internet of Things continue selecting wireless charging as a business automation strategy, driving demand for flexible, energy-efficient power solutions in IoT-enabled devices. The Qi2 evolution folding Apple's Magnetic Power Profile into the open charging standard continues raising ceiling power to twenty-five watts while tightening charging efficiency into the eighty-five to ninety percent band, and integration of charging transmitters into furniture, countertops, and air conditioning units continues widening the technology's reach well beyond its original smartphone-centric roots.

Infineon Technologies introduced its OPTIREG TLF35585 power management integrated circuit in February 2025, achieving ISO 26262 compliance to serve safety-critical electronic control units within automotive wireless charging and power delivery applications.

Market Size and Forecast

-

Market Size in 2026E: USD 12.94 Billion

-

Market Size by 2035: USD 79.60 Billion

-

CAGR: 22.37% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Wireless Charging Market - Request Free Sample Report

Wireless Charging Market Trends

-

The Qi2 evolution incorporating Apple's Magnetic Power Profile is raising ceiling power to twenty-five watts across the open charging standard.

-

Integration of charging transmitters into furniture, countertops, and automotive interiors continues widening deployment beyond smartphones.

-

Rising electric vehicle adoption is driving integration of wireless charging technology into automotive applications.

-

Manufacturing sector automation strategies increasingly incorporate wireless charging for IoT-enabled industrial devices.

-

Silicon carbide power semiconductor adoption is improving efficiency in high-voltage automotive wireless charging systems.

US Wireless Charging Market Size Outlook

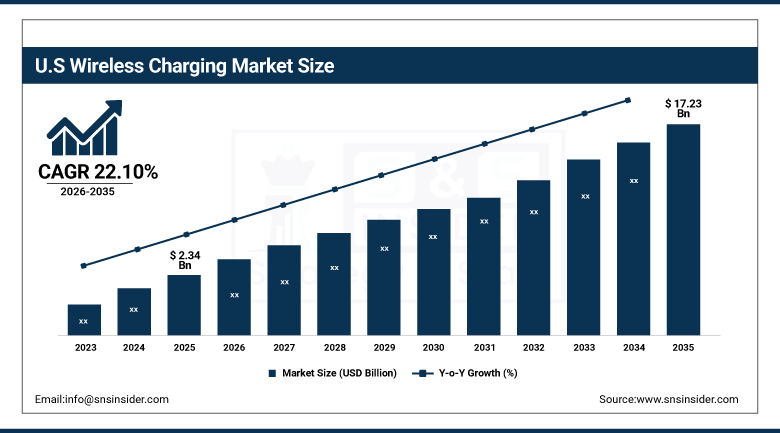

The US Wireless Charging Market was valued at USD 2.34 Billion in 2025 and is expected to reach USD 17.23 Billion by 2035, growing at a CAGR of 22.10% from 2026 to 2035.

The US held a dominant share in the North America wireless charging demand driven by extensive adoption of electric cars and sustainability focus amongst consumers and regional government policies. Penetration of advanced consumer electronics coupled with the trend of integrating wireless charging in consumer products helped maintain the US as one of the fastest growing countries in terms of wireless charging demand through the year.

Onsemi, a company based out of Scottsdale, Arizona, made an acquisition of USD 115 million in January 2025 in Qorvo's silicon carbide junction field-effect transistor portfolio in order to extend its EliteSiC offering for high voltage wireless charging and power delivery.

Wireless Charging Market Segment Analysis

-

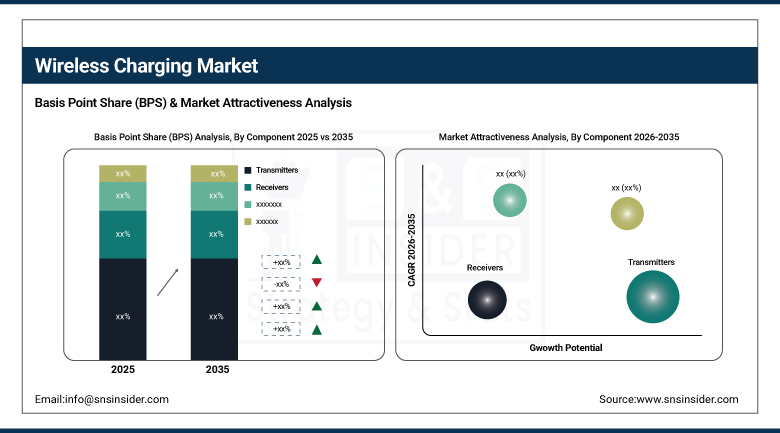

By Component, the Transmitters segment held approximately 66.00% share in 2025, while the same segment is also the fastest growing.

-

By Technology, the Inductive segment held approximately 55.40% share in 2025, while the Resonant segment is the fastest growing.

-

By Application, the Consumer Electronics segment held approximately 46.00% share in 2025, while the Automotive segment is the fastest growing.

By Component, Transmitters led the market and grew fastest

The Transmitters segment dominated the component category in 2025, holding approximately 66.00% of total revenue, and is also projected to grow at the fastest rate through 2035. Integration of transmitters into furniture, countertops, air conditioning units, and automotive consoles continues multiplying infrastructure nodes at a pace receiver-side integration cannot match, since every new charging pad, dock, or vehicle console requires its own dedicated transmitter component.

Receivers continue holding a meaningful share of overall component revenue, integrated directly into smartphones, wearables, and other portable consumer electronics that depend on wireless charging compatibility. That steady receiver-side integration keeps this component category relevant even as transmitter infrastructure expansion continues capturing a disproportionate share of incremental market growth.

By Technology, Inductive led the market, Resonant grew fastest

The Inductive segment held the largest technology share in 2025, at approximately 55.40%, favored for its simplicity and cost-effectiveness that continue making it the default choice for consumer electronics charging pads and docks. That combination of proven reliability and low manufacturing cost keeps inductive charging firmly at the top of the broader technology segmentation across the majority of smartphone, wearable, and tablet charging applications worldwide.

The Resonant segment is projected to grow at the fastest CAGR during the forecast period, offering meaningfully greater spatial freedom and charging distance than inductive technology can achieve, advantages that matter considerably for automotive, industrial, and multi-device charging applications. Rising demand for charging solutions that do not require precise device-to-pad alignment continues pushing resonant technology adoption ahead of the broader technology segmentation.

By Application, Consumer Electronics led the market, Automotive grew fastest

The Consumer Electronics segment held the largest application share in 2025, at approximately 46.00%, anchored by smartphones, tablets, smartwatches, and earbuds that remain the primary users of wireless charging technology. That broad-based, sustained consumer device demand keeps this application category firmly at the center of overall wireless charging consumption across nearly every major regional market.

The Automotive segment is projected to grow at the fastest CAGR during the forecast period, driven by increasing adoption of electric vehicles that continues heightening demand for convenient, cable-free charging solutions integrated directly into vehicle design. Rising integration of wireless charging technology into both vehicle interiors for portable devices and EV charging infrastructure itself continues pushing automotive application demand ahead of the broader application segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

38.30% |

|

North America |

United States |

85.90% |

|

Europe |

Germany |

27.70% |

|

Middle East & Africa |

UAE |

26.60% |

|

Latin America |

Mexico |

38.90% |

Asia Pacific Wireless Charging Market Insights

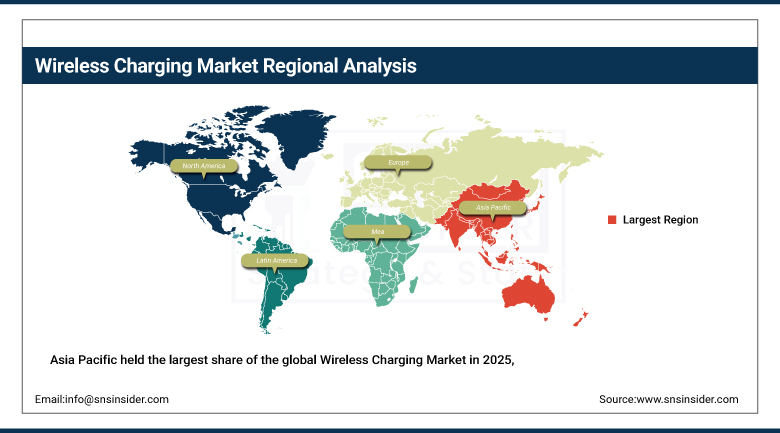

Asia Pacific held the largest share of the global Wireless Charging Market in 2025, at approximately 41.35%, anchored by dense fabrication capacity, early Qi2 certification pipelines, and Japan-led automotive integration programs across the region. Rapid adoption of smartphones and other wireless-enabled devices continued driving regional demand at a scale few other regions could match.

China accounted for roughly 38.30% of regional revenue, supported by its massive consumer electronics manufacturing base and expanding domestic wireless charging component production. Japan and South Korea contributed significant additional regional demand through their own advanced automotive integration and consumer electronics industries, reinforcing Asia Pacific's position as the clear global leader in wireless charging adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Wireless Charging Market Insights

North America was the fastest-growing region in the global Wireless Charging Market, driven by high electric vehicle adoption and strong emphasis on sustainability among consumers and regional governments. High penetration of advanced consumer electronic devices, combined with the shift toward integrating wireless charging into personal devices, continued reinforcing this leadership position throughout the year.

The United States accounted for roughly 85.90% of regional revenue, reflecting its concentration of leading consumer electronics brands and automotive manufacturers integrating wireless charging technology. Canada contributed a smaller but steadily growing share of regional revenue, supported by its own expanding electric vehicle and consumer electronics adoption, keeping North America's growth rate ahead of every other region tracked in this report.

Europe Wireless Charging Market Insights

Europe occupied a significant market share of the Wireless Charging Market globally in 2025, owing to its strong automobile production base and increasing use of consumer electronics in the region. Germany had a 27.70% market share driven by its presence of automobile makers adopting wireless charging in their new generation electric vehicles.

France, United Kingdom, and Italy were also following the same pattern, as the region's largest economies witnessed continued adoption of automobiles in the form of electric vehicles, along with consumer electronics. Europe's increasing focus on sustainability and investment in infrastructure of electric vehicles is likely to sustain its demand throughout the forecast period.

MEA & Latin America Wireless Charging Market Insights

Middle East & Africa witnessed consistent growth in the adoption rate of wireless charging technology in 2025, owing to increasing consumer electronic devices penetration and increasing investments made by enterprises in intelligent infrastructure in the Gulf countries. The UAE was responsible for around 26.60% of the total revenues earned in the region, aided by increasing consumer preference for high-end consumer electronics and connected devices.

Latin America witnessed consistent growth at a similar rate to that seen in MEA, where Mexico will record the highest CAGR at around 38.90% of the total revenues in the global market. Brazil and Argentina followed suit with a similar growth pattern due to the increasing adoption of consumer electronics and automotive manufacturing in the region.

Market Dynamics

Growth Drivers: IoT manufacturing integration and electric vehicle adoption

Manufacturing sector players integrating operations with the Internet of Things and selecting automation as a business strategy globally continue driving demand for wireless chargers that offer flexible, energy-efficient, and convenient power solutions for IoT-enabled devices. Many devices and technology manufacturers requiring constant, reliable power supply sources continue finding wireless chargers an increasingly viable alternative to traditional wired power solutions.

The increasing adoption of electric vehicles continues heightening demand for convenient charging solutions, driving integration of wireless charging technologies deeper into the automotive sector. The Qi2 evolution folding Apple's Magnetic Power Profile into the open standard continues raising ceiling power while tightening charging efficiency, reinforcing structural demand growth across nearly every major wireless charging application category worldwide.

Restraints: Charging efficiency limitations and heat generation concerns

Wireless charging systems continue facing efficiency limitations relative to wired alternatives, as electromagnetic energy transfer inherently loses some power as heat during the charging process. That efficiency gap can meaningfully affect charging speed and device temperature management, particularly for higher-power applications where heat dissipation becomes a genuine engineering challenge.

The precise alignment requirements that inductive charging technology demands continue limiting user convenience relative to the promise of truly cable-free power delivery, since misaligned devices may charge slowly or not at all. That alignment sensitivity continues driving interest in resonant alternatives, even though resonant technology itself carries higher component costs that can restrict adoption in price-sensitive product categories.

Opportunities: Furniture integration and industrial IoT expansion

Growing integration of wireless charging transmitters into furniture, countertops, and air conditioning units presents substantial opportunity for component manufacturers positioned to serve this expanding embedded infrastructure category. Manufacturers capable of delivering discreet, furniture-integrated charging solutions stand to capture a growing share of demand as this application category continues widening beyond dedicated charging pads and docks.

Rising manufacturing sector adoption of wireless charging for industrial IoT devices presents a further significant growth avenue, as automation-focused manufacturers increasingly favor wireless power delivery over wired connections that can complicate equipment mobility and maintenance. Component manufacturers capable of delivering ruggedized, industrial-grade wireless charging solutions stand to capture meaningful new revenue streams as this application category continues maturing through 2035.

Recent Developments:

-

2025: Samsung Semiconductor unveiled its S2MIW06 power management integrated circuit in February, spotlighting tighter component integration designed for upcoming Qi2-compatible smartphone handsets.

-

2025: FORVIA HELLA selected Infineon's 1200 volt CoolSiC metal-oxide-semiconductor field-effect transistors in January for its 800 volt direct current wireless charging equipment, advancing high-voltage automotive charging capability.

-

2025: Mophie launched new Qi2 wireless chargers in September capable of delivering faster charging speeds up to fifteen watts for iPhones and other Qi2-compatible Android devices, emphasizing efficiency and broad device compatibility.

-

2025: AUKEY launched the MagFusion Ark in September, a modular true wireless charging system integrating multiple transmitters that supports simultaneous charging of up to six devices.

-

2023: Resonant Link announced a strategic partnership with Lura Health in July, developing two wireless charging systems for Lura Health's oral sensor device that meet United States Food and Drug Administration requirements.

Wireless Charging Companies are:

-

Texas Instruments Incorporated

-

Qualcomm Incorporated

-

STMicroelectronics N.V.

-

Infineon Technologies AG

-

NXP Semiconductors N.V.

-

Samsung Electronics Co., Ltd.

-

Apple Inc.

-

Anker Innovations Limited

-

ZAGG Inc.

-

AUKEY

-

ConvenientPower HK Ltd.

-

Powermat Technologies Ltd.

-

Energous Corporation

-

Onsemi

-

Renesas Electronics Corporation

-

Resonant Link, Inc.

-

FORVIA HELLA

-

Ossia Inc.

Wireless Charging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.57 Billion |

| Market Size by 2035 | USD 79.60 Billion |

| CAGR | CAGR of 22.37% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Transmitters, Receivers) • by Technology (Inductive, Resonant, Radio Frequency) • by Application (Consumer Electronics, Automotive, Industrial, Healthcare) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | WiTricity Corporation, Texas Instruments Incorporated, Qualcomm Incorporated, STMicroelectronics N.V., Infineon Technologies AG, NXP Semiconductors N.V., Samsung Electronics Co., Ltd., Apple Inc., Belkin International, Inc., Anker Innovations Limited, ZAGG Inc., AUKEY, ConvenientPower HK Ltd., Powermat Technologies Ltd., Energous Corporation, Onsemi, Renesas Electronics Corporation, Resonant Link, Inc., FORVIA HELLA, Ossia Inc. |

Frequently Asked Questions

The Wireless Charging Market is expected to grow at a CAGR of 22.37% from 2026 to 2035.

The Wireless Charging Market was valued at USD 10.57 Billion in 2025.

IoT manufacturing integration combined with rising electric vehicle adoption and the Qi2 charging standard evolution is the major growth factor.

The Transmitters segment held approximately 66.00% share in 2025 and was also the fastest-growing component segment.

Asia Pacific held the largest share of the Wireless Charging Market in 2025, at approximately 41.35%, while North America was the fastest-growing region.

Get in Touch