Infectious Disease Diagnostics Market Report Scope & Overview:

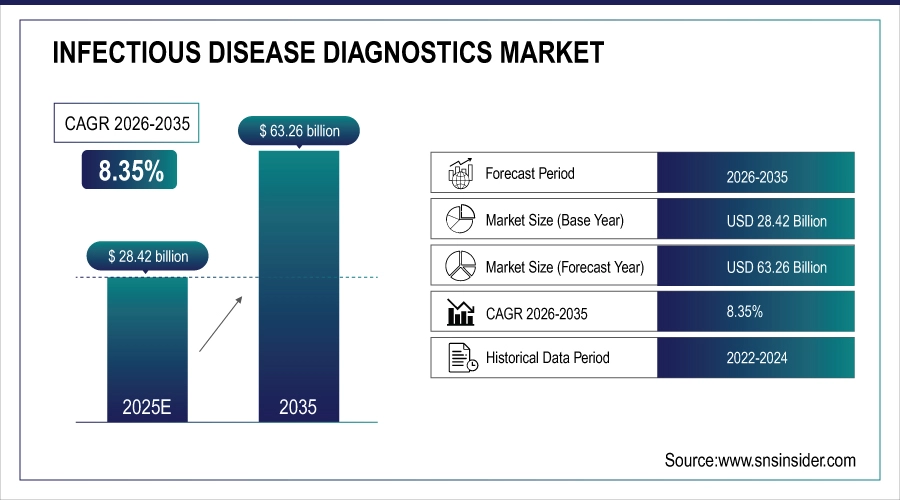

The Infectious Disease Diagnostics Market size is estimated at USD 28.42 Billion in 2025 and is expected to reach USD 63.26 Billion by 2035 and grow at a CAGR of 8.35% over the forecast period of 2026–2035.

The Infectious Disease Diagnostics Market analysis report provides comprehensive insights into market dynamics, technology adoption, and strategic initiatives. Rising prevalence of infectious diseases, increasing demand for rapid and accurate diagnostic solutions, and growing healthcare infrastructure are driving market growth during 2026–2035.

Infectious Disease Diagnostic tests exceeded 4.5 billion in 2025, driven by rising infections and growing adoption of rapid and accurate diagnostics.

Market Size and Forecast:

-

Market Size in 2025: USD 28.42 Billion

-

Market Size by 2035: USD 63.26 Billion

-

CAGR: 8.35% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Infectious Disease Diagnostics Market - Request Free Sample Report

Infectious Disease Diagnostics Market Trends:

-

Rising prevalence of bacterial, viral, fungal, and parasitic infections is driving demand for accurate diagnostic solutions.

-

Increasing adoption of rapid point-of-care and molecular testing is enhancing early detection and patient management.

-

Expansion of hospital, laboratory, and clinic networks is boosting testing capacity and accessibility.

-

Integration of AI, digital health platforms, and data analytics is improving diagnostic precision and workflow efficiency.

-

Technological advancements in immunoassays, microfluidics, and high-throughput testing are accelerating market scalability and accuracy.

-

Strategic collaborations between diagnostic companies, healthcare providers, and research institutes are fostering innovation and market expansion.

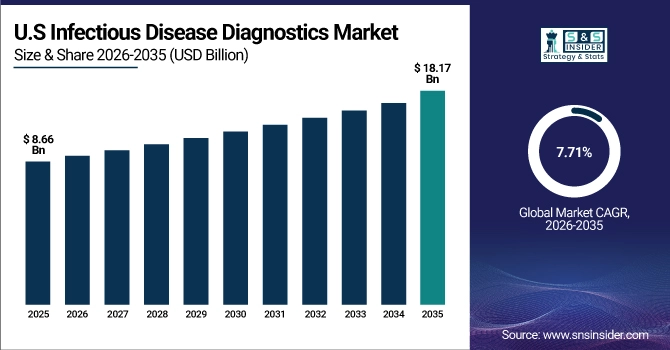

The U.S. Infectious Disease Diagnostics Market is projected to grow from USD 8.66 Billion in 2025E to USD 18.17 Billion by 2035, at a CAGR of 7.71%. Growth is driven by high disease burden, advanced healthcare infrastructure, widespread adoption of molecular and point-of-care diagnostics, and strong investments in laboratory automation and digital health solutions.

Infectious Disease Diagnostics Market Growth Drivers:

-

Rising prevalence of infectious diseases and demand for rapid, accurate diagnostics driving market expansion.

Rising prevalence of infectious diseases and increasing demand for rapid, accurate diagnostics are major drivers of the Infectious Disease Diagnostics Market growth. Hospitals, clinics, and laboratories are investing in advanced molecular, immunoassay, and point-of-care testing solutions to improve early detection, patient management, and outbreak control. Expansion of healthcare infrastructure and integration with digital health platforms further enhance testing efficiency. Continuous innovations in high-throughput testing, microfluidics, and AI-assisted diagnostics are accelerating market growth.

Over 62% of hospitals and diagnostic laboratories adopted rapid and molecular infectious disease tests in 2025 for early detection and improved patient care.

Infectious Disease Diagnostics Market Restraints:

-

High costs of advanced diagnostic tests and limited healthcare infrastructure are restricting market adoption.

High costs of advanced diagnostic tests and limited healthcare infrastructure are key restraints for the Infectious Disease Diagnostics Market. Small and mid-sized hospitals, clinics, and laboratories often face budgetary constraints, limiting adoption of molecular, immunoassay, and point-of-care testing solutions. Integrating advanced diagnostics with existing laboratory workflows and digital health platforms can be technically challenging. Additionally, ensuring test accuracy, regulatory compliance, and staff training requires significant investment and expertise. These factors collectively slow market penetration despite rising demand for infectious disease testing.

Infectious Disease Diagnostics Market Opportunities:

-

Growing demand for rapid, point-of-care diagnostics and digital health integration offers significant market expansion opportunities.

Growing demand for rapid, point-of-care diagnostics and integration with digital health platforms presents significant opportunities for the Infectious Disease Diagnostics Market. Hospitals, clinics, and laboratories are increasingly adopting advanced molecular, immunoassay, and high-throughput testing solutions to improve early detection and patient management. Companies offering scalable, accurate, and user-friendly diagnostic technologies can capitalize on this demand. Continuous innovation in AI-assisted diagnostics, microfluidics, and mobile health integration enables expanded adoption across healthcare and research sectors.

Over 35% of hospitals and clinics adopted rapid and point-of-care infectious disease diagnostics in 2025, driven by demand for early detection and digital health integration.

Infectious Disease Diagnostics Market Segmentation Analysis:

-

By Technology, Molecular Diagnostics held the largest market share of 42.75% in 2025, while Point-of-Care Tests are expected to grow at the fastest CAGR of 10.12% during 2026–2035.

-

By Disease Type, Viral diagnostics accounted for the highest market share of 38.60% in 2025, while Parasitic testing is projected to record the fastest CAGR of 11.05% through 2026–2035.

-

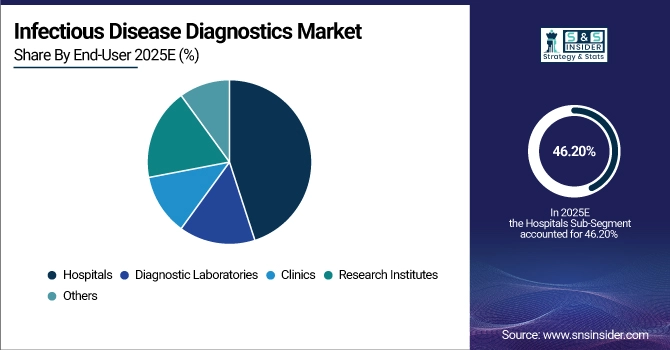

By End-User, Hospitals dominated with a 46.20% share in 2025, while Research Institutes are expected to expand at the fastest CAGR of 10.55% during the forecast period.

-

By Distribution Channel, Direct Sales held the largest share of 40.50% in 2025, while Online Channels are anticipated to grow at the fastest CAGR of 11.20% through 2026–2035.

By End-User, Hospitals Dominate While Research Institutes Grow Rapidly:

Hospitals segment dominated the market due to high patient inflow, advanced laboratory infrastructure, and availability of skilled professionals. Hospitals conducted more than 2.1 billion infectious disease diagnostic tests in 2025, making them the primary end-user segment.

Research Institutes are the fastest-growing segment, supported by increased funding for infectious disease research and diagnostic innovation. Research-based testing activities crossed 180 million tests in 2025, driven by vaccine development and pathogen surveillance studies.

By Technology, Molecular Diagnostics Dominates While Point-of-Care Tests Grow Rapidly:

Molecular Diagnostics segment dominated the market due to its high sensitivity, accuracy, and ability to detect pathogens at early stages. These technologies are widely used in hospitals and reference laboratories for viral and bacterial infections. In 2025, molecular diagnostic testing volumes exceeded 1.8 billion tests, reflecting strong clinical adoption.

Point-of-Care Tests is the fastest-growing segment, driven by demand for rapid results and decentralized testing. Adoption accelerated across emergency care, rural clinics, and home-based diagnostics. POCT deployments surpassed 620 million tests in 2025, particularly in emergency care and outpatient settings.

By Disease Type, Viral Diagnostics Dominates While Parasitic Testing Expands Rapidly:

Viral segment dominated the market owing to high testing demand for influenza, HIV, hepatitis, and emerging viral outbreaks. Continuous surveillance programs and hospital-based testing significantly support this segment. In 2025, viral diagnostic tests accounted for over 1.6 billion procedures.

Parasitic is the fastest-growing segment, supported by rising incidence in tropical regions and improved detection technologies. Increasing government screening programs are further accelerating market adoption. Parasitic testing volumes grew to 290 million tests in 2025, driven by expanded screening programs and health initiatives.

By Distribution Channel, Direct Sales Dominate While Online Channels Expand Rapidly:

Direct Sales segment dominated the market as hospitals and laboratories prefer direct procurement for advanced diagnostic instruments and reagents. This channel ensures technical support, training, and long-term supply contracts. In 2025, direct sales accounted for over 2.2 billion diagnostic units distributed.

Online Channels are the fastest-growing segment, driven by smaller laboratories and clinics adopting digital procurement platforms. In 2025, online diagnostic product transactions exceeded 850 million units, reflecting increasing acceptance of e-commerce and remote supply solutions in healthcare.

Regional Insights:

North America Infectious Disease Diagnostics Market Insights:

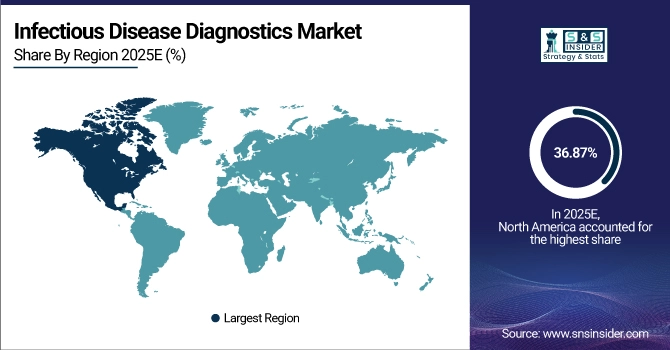

The North America Infectious Disease Diagnostics Market is dominated, holding a 36.87% share in 2025, driven by strong adoption across the U.S. and Canada. High prevalence of infectious diseases, advanced healthcare infrastructure, and widespread use of molecular and point-of-care diagnostics are fueling growth. Hospitals and diagnostic laboratories continue investing in rapid testing and digital health integration. Supportive regulatory frameworks, strong R&D activity, and early adoption of innovative diagnostic technologies further reinforce North America’s leadership in this mature market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Infectious Disease Diagnostics Market Insights:

The U.S. Infectious Disease Diagnostics Market is strongly influenced by high infectious disease prevalence, advanced healthcare infrastructure, and rapid adoption of molecular and point-of-care testing. Increasing investments in laboratory automation, digital health platforms, and outbreak surveillance programs are driving diagnostic innovation, early detection capabilities, and large-scale testing deployment, reinforcing the U.S. as the dominant market in North America.

Asia-Pacific Infectious Disease Diagnostics Market Insights:

The Asia-Pacific Infectious Disease Diagnostics Market is the fastest-growing region, projected to expand at a CAGR of 9.87% during 2026–2035. Growth is driven by rising infectious disease burden, expanding healthcare infrastructure, and increasing adoption of rapid and molecular diagnostics across China, India, Japan, and Southeast Asia. Growing government screening programs, improving laboratory networks, and rising investments in public health surveillance and digital healthcare platforms are accelerating diagnostic adoption and strengthening Asia-Pacific’s dynamic market growth.

The China Infectious Disease Diagnostics Market is driven by a large patient population, rising infectious disease incidence, and expanding healthcare infrastructure. Increasing government-led screening programs, rapid adoption of molecular and point-of-care diagnostics, and growing investments in laboratory automation and public health surveillance are accelerating diagnostic adoption, positioning China as a major contributor to Asia-Pacific market growth.

Europe Infectious Disease Diagnostics Market Insights:

The Europe Infectious Disease Diagnostics Market is driven by rising investments in healthcare modernization, disease surveillance programs, and diagnostic innovation. Countries such as Germany, France, and the UK are shaping regional demand through widespread adoption of molecular diagnostics, immunoassays, and point-of-care testing. Expansion of hospital laboratory automation, cross-border public health initiatives, and strong regulatory support for early disease detection is boosting adoption. Continuous technological advancements and government-backed healthcare programs are reinforcing Europe’s significance in the infectious disease diagnostics market.

Germany is a key market in the European Infectious Disease Diagnostics landscape, driven by advanced healthcare infrastructure and strong public health systems. Growth is supported by widespread adoption of molecular diagnostics, laboratory automation, and point-of-care testing, alongside robust regulatory focus on disease surveillance, early detection, and healthcare digitalization.

Latin America Infectious Disease Diagnostics Market Insights:

The Latin America Infectious Disease Diagnostics Market is growing due to rising infectious disease prevalence and expanding healthcare investments. Adoption is supported by increasing deployment of diagnostic laboratories, rapid testing programs, and point-of-care solutions across Brazil, Mexico, and Argentina, with government-led public health initiatives and improving access to diagnostics driving regional market growth.

Middle East and Africa Infectious Disease Diagnostics Market Insights:

The Middle East & Africa Infectious Disease Diagnostics Market is expanding due to rising infectious disease burden and healthcare infrastructure development. Increasing adoption of rapid diagnostics, laboratory expansion, and public health screening programs is driving demand, with Saudi Arabia, the UAE, and South Africa emerging as key regional markets.

Infectious Disease Diagnostics Market Competitive Landscape:

Abbott Laboratories, headquartered in the U.S., is a leader in infectious disease diagnostics with a strong portfolio spanning molecular diagnostics, immunoassays, and rapid point-of-care testing. The company has established dominance through widely adopted platforms such as real-time PCR systems and rapid antigen tests used across hospitals, laboratories, and public health programs. Abbott’s extensive distribution network, large-scale manufacturing capabilities, and ability to rapidly scale testing during outbreaks have reinforced its market leadership. Continuous innovation, strong regulatory approvals, and strategic partnerships with healthcare providers further strengthen Abbott’s dominant position in the infectious disease diagnostics market.

-

In March 2025, Abbott expanded its Alinity molecular diagnostics portfolio, enhancing automated PCR testing for HIV, hepatitis, and respiratory viruses, improving lab efficiency and diagnostic accuracy while supporting large‑scale infectious disease detection across clinical and public health settings.

F. Hoffmann-La Roche Ltd, based in Switzerland, is a leading player in the infectious disease diagnostics market, driven by its strong expertise in molecular diagnostics and laboratory automation. Roche’s COBAS molecular testing platforms are extensively deployed in centralized laboratories, supporting high-throughput and highly accurate pathogen detection. The company’s dominance is reinforced by deep integration of diagnostics with digital laboratory workflows, strong clinical validation, and long-term relationships with hospitals and reference laboratories. Continuous investments in R&D, companion diagnostics, and disease surveillance initiatives have enabled Roche to maintain a strong and influential market position.

-

In December 2025, Roche launched the cobas BV/CV PCR assay, enabling rapid, accurate detection of bacterial vaginosis and candida vaginitis from a single sample, improving diagnosis and patient management. The assay supports high-throughput laboratory workflows efficiently.

Thermo Fisher Scientific Inc., headquartered in the U.S., holds a dominant position in the infectious disease diagnostics market through its comprehensive portfolio of molecular testing kits, PCR instruments, reagents, and laboratory consumables. The company supports a wide range of infectious disease testing applications across clinical diagnostics, research, and public health laboratories. Thermo Fisher’s strength lies in its supply chain, broad customer base, and ability to deliver scalable, high-throughput diagnostic solutions. Strategic acquisitions, strong R&D investments, and integration of advanced technologies have positioned Thermo Fisher as a key driver of innovation and market dominance.

-

In June 2025, Thermo Fisher and Mylab Discovery Solutions introduced Applied Biosystems TaqPath RT‑PCR kits for tuberculosis, hepatitis B/C, and HIV, enhancing molecular diagnostic access and infection monitoring in India and globally. Kits ensure rapid, reliable testing.

Infectious Disease Diagnostics Market Key Players:

-

Abbott Laboratories

-

F. Hoffmann-La Roche Ltd

-

Thermo Fisher Scientific Inc.

-

Danaher Corporation

-

bioMérieux SA

-

Siemens Healthineers AG

-

Becton, Dickinson and Company

-

QIAGEN N.V.

-

Hologic Inc.

-

Bio-Rad Laboratories, Inc.

-

QuidelOrtho Corporation

-

Grifols S.A.

-

DiaSorin S.p.A.

-

SD Biosensor, Inc.

-

PerkinElmer Inc.

-

Sysmex Corporation

-

OraSure Technologies, Inc.

-

Co-Diagnostics, Inc.

-

Trinity Biotech plc

-

Genetic Signatures Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 28.42 Billion |

| Market Size by 2035 | USD 63.26 Billion |

| CAGR | CAGR of 8.35% From 2026 to 2035 |

| Base Year | 2025E |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Molecular Diagnostics, Immunoassays, Microbiological Culture, Point-of-Care Tests, Others) • By Disease Type (Bacterial, Viral, Fungal, Parasitic, Others) • By End-User (Hospitals, Diagnostic Laboratories, Clinics, Research Institutes, Others) • By Distribution Channel (Direct Sales, Online Channels, Distributors, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories, F. Hoffmann-La Roche Ltd, Thermo Fisher Scientific Inc., Danaher Corporation, bioMérieux SA, Siemens Healthineers AG, Becton, Dickinson and Company, QIAGEN N.V., Hologic Inc., Bio-Rad Laboratories, Inc., QuidelOrtho Corporation, Grifols S.A., DiaSorin S.p.A., SD Biosensor, Inc., PerkinElmer Inc., Sysmex Corporation, OraSure Technologies, Inc., Co-Diagnostics, Inc., Trinity Biotech plc, Genetic Signatures Ltd. |

Frequently Asked Questions

North America dominated with a 36.87% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 9.87% during 2026–2035.

Molecular Diagnostics dominated with a 42.75% share in 2025, while Point-of-Care Tests are projected to grow at the fastest CAGR of 10.12% during 2026–2035.

Growth is driven by rising infections, demand for rapid diagnostics, and expanded healthcare infrastructure.

The market is valued at USD 28.42 Billion in 2025E and is projected to reach USD 63.26 Billion by 2035.

The Infectious Disease Diagnostics Market is expected to grow at a CAGR of 8.35% during 2026–2035.

Get in Touch