Tissue Engineered Skin Substitutes Market Report Scope & Overview:

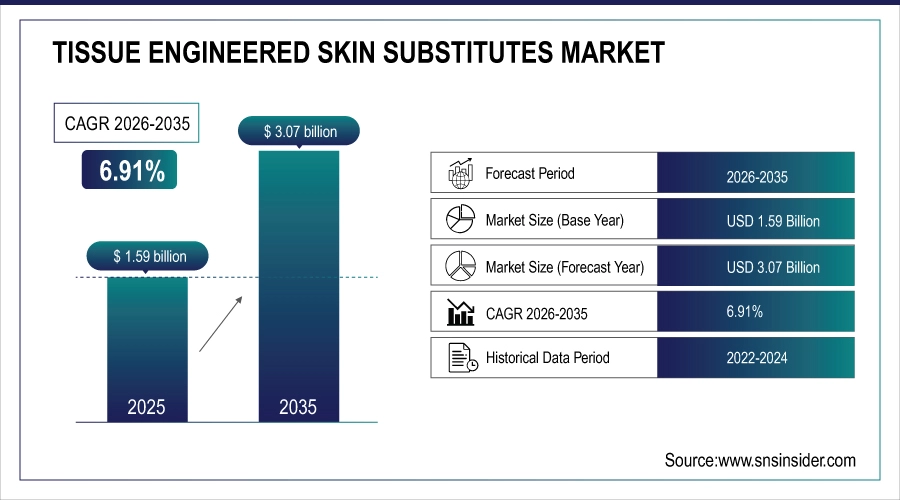

The Tissue Engineered Skin Substitutes Market size is estimated at USD 1.59 billion in 2025 and is expected to reach USD 3.07 billion by 2035 and grow at a CAGR of 6.91% over the forecast period of 2026-2035.

The Global Tissue Engineered Skin Substitutes Market is growing due to rising prevalence of chronic and acute wounds, including diabetic ulcers, burns, and surgical wounds. Increasing demand for advanced regenerative therapies, technological innovations in synthetic, biosynthetic, and biological skin substitutes, and growing adoption by hospitals and wound care centers drive market expansion. Supportive government initiatives, rising healthcare awareness, and investments in research further fuel global market growth.

87% of wound care providers globally adopted tissue-engineered skin substitutes propelled by surging chronic wound cases, regenerative medicine advances, and supportive health policies catalyzing market growth despite cost and accessibility challenges.

Market Size and Forecast

-

Market Size in 2025: USD 1.59 Billion

-

Market Size by 2035: USD 3.07 Billion

-

CAGR: 6.91% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Tissue Engineered Skin Substitutes Market - Request Free Sample Report

Tissue Engineered Skin Substitutes Market Trends

-

Rising prevalence of chronic wounds, burns, and diabetic ulcers is driving the tissue engineered skin substitutes market.

-

Growing adoption of bioengineered skin products in hospitals, wound care centers, and burn units is boosting market growth.

-

Expansion of advanced biomaterials, stem cell therapies, and regenerative medicine applications is fueling deployment.

-

Increasing focus on faster wound healing, reduced infection risk, and improved patient outcomes is shaping adoption trends.

-

Advancements in 3D bioprinting, scaffold technologies, and tissue regeneration techniques are enhancing product efficacy.

-

Rising healthcare expenditure and government support for regenerative therapies are supporting market expansion.

-

Collaborations between biotech firms, research institutions, and healthcare providers are accelerating innovation and global adoption.

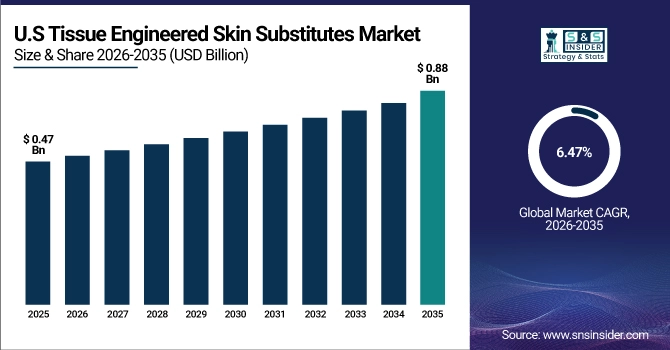

U.S. Tissue Engineered Skin Substitutes Market was valued at USD 0.47 billion in 2025 and is expected to reach USD 0.88 billion by 2035, growing at a CAGR of 6.47% from 2026-2035.

The U.S. Tissue Engineered Skin Substitutes Market is growing due to high prevalence of chronic wounds, advanced healthcare infrastructure, strong adoption of regenerative therapies, technological innovations in skin substitutes, and increasing demand from hospitals and wound care centers.

Tissue Engineered Skin Substitutes Market Growth Drivers:

-

Increasing prevalence of chronic and acute wounds driving demand for advanced tissue engineered skin substitute therapies globally

Rising prevalence of chronic wounds such as diabetic ulcers, burns, and pressure ulcers is driving demand for tissue engineered skin substitutes. Aging populations and lifestyle-related health conditions increase the incidence of non-healing wounds, creating a need for advanced regenerative therapies. Tissue engineered skin substitutes provide faster healing, reduced infection risk, and improved functional and cosmetic outcomes. Hospitals, wound care centers, and clinics are adopting these substitutes to reduce patient recovery time and overall healthcare costs. Continuous innovation in bioengineered skin products and supportive government healthcare initiatives further amplify adoption, driving market growth globally.

86% of wound care centers globally expanded use of tissue-engineered skin substitutes driven by rising chronic and acute wound prevalence to accelerate healing, reduce complications, and address unmet clinical needs.

Tissue Engineered Skin Substitutes Market Restraints:

-

High cost of tissue engineered skin substitutes limiting accessibility and widespread adoption across healthcare facilities

High cost of tissue engineered skin substitutes is a significant restraint limiting accessibility and adoption, particularly in emerging markets. Production involves advanced biotechnology, skilled labor, and rigorous quality control, resulting in expensive products. Insurance coverage and reimbursement policies are often limited, making treatment unaffordable for many patients. Small clinics and healthcare providers may struggle to procure these substitutes due to budget constraints. Cost-sensitive patients may prefer traditional grafting methods or conventional wound care therapies. Price barriers reduce market penetration, slow adoption rates, and restrict growth potential despite the increasing demand for advanced regenerative wound care solutions globally.

78% of healthcare facilities particularly in cost-sensitive regions limited use of tissue-engineered skin substitutes due to high costs, restricting patient access and slowing broad clinical adoption despite proven therapeutic benefits.

Tissue Engineered Skin Substitutes Market Opportunities:

-

Rising investments in research and development creating innovative tissue engineered skin substitutes with enhanced healing properties

Increasing investments in research and development provide significant opportunities for the tissue engineered skin substitutes market. Biotech firms and healthcare institutions are developing advanced substitutes using stem cells, growth factors, and 3D bioprinting technologies. Innovations focus on improving wound closure rates, reducing scarring, and enhancing tissue regeneration. Collaborations between companies, universities, and research organizations accelerate product development and commercialization. Growing funding from government initiatives and private investors supports innovation and scaling of production. These developments open opportunities for new product launches, expansion into emerging markets, and improved patient outcomes, driving long-term market growth globally.

83% of regenerative medicine developers advanced tissue-engineered skin substitutes driven by R&D investments delivering enhanced healing, reduced scarring, and improved integration for chronic wounds and burns.

Tissue Engineered Skin Substitutes Market Segment Highlights

-

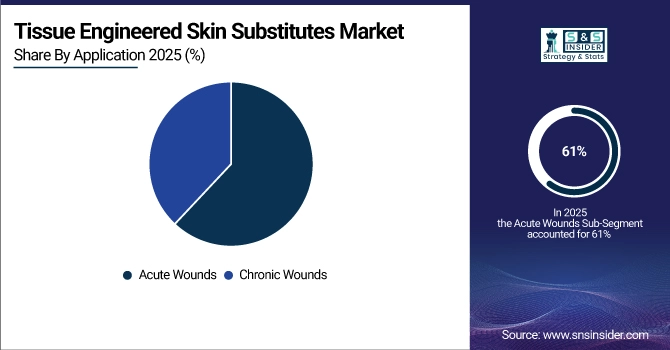

By Application, Acute Wounds dominated the Market with 61% share in 2025; Chronic Wounds fastest growing (CAGR).

-

By Product, Biological dominated the Market with 38% share in 2025; Biosynthetic fastest growing (CAGR).

-

By End-Use, Hospitals dominated the Market with 51% share in 2025; Wound Care Centers fastest growing (CAGR).

Tissue Engineered Skin Substitutes Market Segment Analysis

By Application, Acute Wounds segment dominates the Market, Chronic Wounds segment expected to grow fastest

Acute Wounds segment dominated the Tissue Engineered Skin Substitutes Market in 2025 due to the high incidence of burns, surgical wounds, and trauma cases requiring immediate and effective wound care. Hospitals and clinics prefer advanced skin substitutes for faster healing, reduced infection risk, and improved cosmetic outcomes, driving market dominance.

Chronic Wounds segment is expected to grow at the fastest CAGR from 2026-2035 due to increasing prevalence of diabetic ulcers, pressure ulcers, and non-healing wounds. Rising aging populations, lifestyle-related diseases, and demand for advanced regenerative therapies are fueling adoption. Tissue engineered substitutes provide improved healing, reduced complications, and better patient quality of life, accelerating market growth.

By Product, Biological segment dominates the Market, Biosynthetic segment expected to grow fastest

Biological segment dominated the Tissue Engineered Skin Substitutes Market in 2025 because it offers superior biocompatibility, integration with host tissue, and faster wound closure. Products derived from human or animal tissues are widely preferred in hospitals and wound care centers. High clinical efficacy, reduced rejection risk, and favorable outcomes drive widespread adoption globally.

Biosynthetic segment is expected to grow at the fastest CAGR from 2026-2035 due to increasing technological innovations combining natural and synthetic materials. These substitutes provide customizable healing properties, reduced immune response, and cost-effective solutions. Rising adoption in chronic wound management, burns, and reconstructive surgeries is expected to propel biosynthetic substitutes’ growth across global markets.

By End-Use, Hospitals segment dominates the Market, Wound Care Centers segment expected to grow fastest

Hospitals segment dominated the Tissue Engineered Skin Substitutes Market in 2025 due to large patient volumes, advanced infrastructure, and availability of skilled healthcare professionals. Hospitals prefer engineered skin substitutes for acute and complex wounds, offering better healing, infection control, and patient outcomes. High adoption and procurement make hospitals the leading end-use segment globally.

Wound Care Centers segment is expected to grow at the fastest CAGR from 2026-2035 as specialized centers focus on chronic wound management and regenerative therapies. Increasing prevalence of diabetes, pressure ulcers, and post-surgical wounds drives demand. These centers adopt innovative skin substitutes, provide expert care, and offer follow-up treatments, fueling rapid market expansion.

Regional Insights

North America Tissue Engineered Skin Substitutes Market Insights

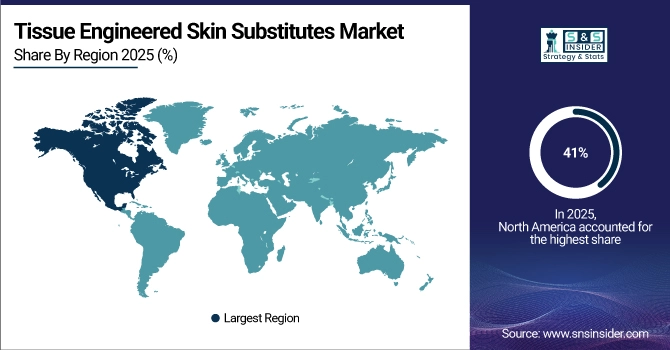

North America dominated the Tissue Engineered Skin Substitutes Market with the highest revenue share of about 41% in 2025 due to the presence of leading biotechnology and medical device companies, high healthcare spending, and advanced hospital infrastructure. Strong adoption of innovative skin substitutes for acute and chronic wound care, combined with favorable reimbursement policies, extensive research and development, and high awareness among healthcare professionals, supports rapid market penetration. The region’s mature healthcare ecosystem drives consistent demand for advanced wound management solutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Tissue Engineered Skin Substitutes Market Insights

Asia Pacific segment is expected to grow at the fastest CAGR of about 8.50% from 2026-2035 due to rising prevalence of chronic wounds, increasing diabetes and burn cases, and improving healthcare infrastructure. Growing awareness about advanced wound care solutions, government initiatives promoting healthcare modernization, and expanding hospital and wound care centers encourage adoption. Rapid urbanization, rising disposable income, and expanding presence of multinational companies offering tissue engineered skin substitutes further accelerate market growth in the region over the forecast period.

Europe Tissue Engineered Skin Substitutes Market Insights

Europe in the Tissue Engineered Skin Substitutes Market is experiencing steady growth due to advanced healthcare infrastructure, high awareness of regenerative therapies, and strong presence of leading biotech companies. Hospitals and wound care centers increasingly adopt synthetic, biosynthetic, and biological skin substitutes for acute and chronic wounds. Supportive government policies, favorable reimbursement systems, and rising R&D investments further drive market expansion, making Europe a significant contributor to global tissue engineered skin substitutes demand.

Middle East & Africa and Latin America Tissue Engineered Skin Substitutes Market Insights

Middle East & Africa and Latin America in the Tissue Engineered Skin Substitutes Market are witnessing moderate growth due to improving healthcare infrastructure, rising awareness of advanced wound care, and increasing prevalence of chronic wounds and burns. Hospitals and wound care centers are gradually adopting synthetic, biosynthetic, and biological substitutes. Supportive government initiatives, growing medical tourism, and expanding presence of international companies further drive market adoption and growth in these regions.

Competitive Landscape:

MiMedx Group, Inc.

MiMedx Group develops regenerative biomaterials and tissue-based products for wound care, surgical, and orthopedic applications. Its portfolio includes amniotic membrane-derived products and skin substitutes designed to accelerate healing and reduce complications in chronic and acute wounds. MiMedx emphasizes clinical research, reimbursement strategies, and regulatory compliance to support product adoption. The company targets hospitals, clinics, and specialty practices, focusing on innovative therapies that improve patient outcomes in tissue repair and regenerative medicine.

-

2024: MiMedx announced continued LCD coverage for EPIFIX and EPICORD skin substitutes, supporting diabetic foot and venous leg ulcer treatment under updated 2025 reimbursement policies.

Smith & Nephew is a global medical technology company specializing in advanced wound care, orthopedics, and sports medicine. The company develops innovative therapies including skin substitutes, surgical devices, and biologics to enhance tissue repair and patient recovery. Smith & Nephew focuses on chronic wound management, hospital partnerships, and regenerative medicine, leveraging clinical research and technology integration to deliver improved outcomes for patients with complex wounds, ulcers, and surgical reconstruction needs.

-

2025: Smith & Nephew launched cellularized skin substitutes with integrated growth factors for chronic ulcer care, enabling faster tissue repair and improved clinical outcomes in pilot programs.

Acelity L.P. Inc. (3M)

Acelity, now part of 3M, develops advanced wound care and surgical solutions including bioengineered skin substitutes, negative pressure wound therapy, and dermal matrices. Its focus is on accelerating tissue regeneration, improving graft adherence, and enhancing patient outcomes in acute, chronic, and surgical wounds. Leveraging innovation, clinical trials, and hospital partnerships, Acelity addresses complex wound care challenges and supports surgeons and healthcare providers with integrated, regenerative, and evidence-based treatment solutions.

-

2025: Acelity (3M) introduced a bioengineered dermal matrix for complex wound management, improving graft adherence and accelerating tissue regeneration for surgical and trauma care applications.

Medline Industries is a healthcare supply and medical products company providing advanced wound care, surgical solutions, and hospital consumables. Its tissue-engineered skin substitutes and regenerative therapies target acute and chronic wounds while integrating with hospital protocols. Medline emphasizes clinical efficacy, workflow efficiency, and broad product accessibility to support healthcare providers. The company invests in innovation, partnerships, and education to improve wound care outcomes and adoption of advanced regenerative solutions globally.

-

2025: Medline expanded its tissue-engineered skin substitute portfolio for acute and chronic wounds, reinforcing hospital adoption and integration with advanced wound care protocols.

LifeNet Health is a non-profit tissue bank specializing in allograft and biologically derived regenerative products, including skin, bone, and soft tissue. Its skin substitutes support wound healing, surgical reconstruction, and chronic wound care, with enhanced regenerative properties. LifeNet Health prioritizes safety, clinical research, and innovation to optimize patient outcomes. The organization collaborates with hospitals, surgeons, and tissue engineering partners to provide high-quality, bioactive solutions for complex wound and reconstructive care.

-

2025: LifeNet Health promoted biologically derived allograft skin substitutes with enhanced regenerative properties, supporting improved healing and clinical outcomes in chronic wounds and surgical reconstruction.

Tissue Engineered Skin Substitutes Market Key Players

-

Organogenesis Inc.

-

Integra LifeSciences

-

Smith & Nephew plc

-

Acelity L.P. Inc. (3M)

-

Mölnlycke Health Care

-

MiMedx Group, Inc.

-

Medline Industries Inc.

-

Allergan plc

-

Kerecis

-

LifeNet Health

-

Vericel Corporation

-

Avita Medical

-

Amnio Technology, LLC

-

Regenicin, Inc.

-

PolarityTE, Inc.

-

Stratatech Corporation

-

Stryker Corporation

-

ConvaTec Group PLC

-

LifeCell International

-

PolyNovo Limited

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.59 Billion |

| Market Size by 2035 | USD 3.07 Billion |

| CAGR | CAGR of 6.91% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Synthetic, Biosynthetic, Biological) • By Application (Acute Wounds, Chronic Wounds) • By End-Use (Hospitals, Wound Care Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Organogenesis Inc., Integra LifeSciences, Smith & Nephew plc, Acelity L.P. Inc. (3M), Mölnlycke Health Care, MiMedx Group, Inc., Medline Industries Inc., Allergan plc, Kerecis, LifeNet Health, Vericel Corporation, Avita Medical, Amnio Technology, LLC, Regenicin, Inc., PolarityTE, Inc., Stratatech Corporation, Stryker Corporation, ConvaTec Group PLC, LifeCell International, PolyNovo Limited |

Frequently Asked Questions

North America dominated the Tissue Engineered Skin Substitutes Market in 2025.

The Biological segment dominated the Tissue Engineered Skin Substitutes Market in 2025.

Increasing prevalence of chronic and acute wounds driving demand for advanced tissue engineered skin substitute therapies globally.

The Tissue Engineered Skin Substitutes Market was valued at USD 1.59 billion in 2025.

The Tissue Engineered Skin Substitutes Market is expected to grow at a CAGR of 6.91% from 2026 to 2035.

Get in Touch