LEO Satellite Market Report Scope & Overview:

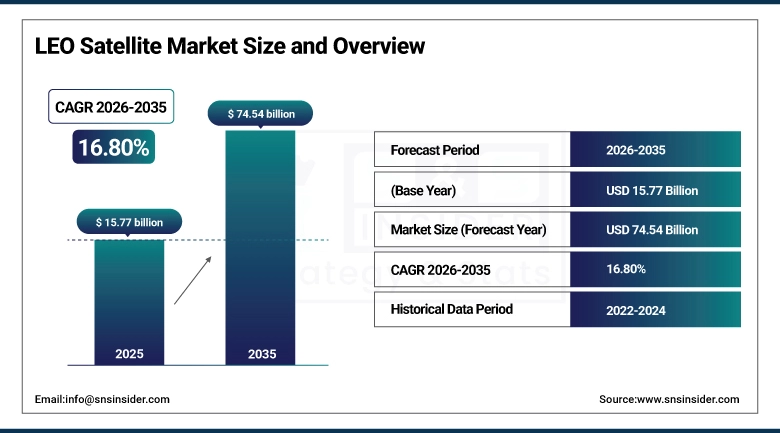

The LEO Satellite Market was valued at USD 15.77 billion in 2025 and is expected to reach USD 74.54 billion by 2035, growing at a CAGR of 16.80% from 2026–2035.

The LEO Satellite Market is expected to experience growth owing to the increasing need for high-speed internet connectivity worldwide, the increasing number of satellite constellations for communication and Earth observation purposes, and the increasing uses of satellites in military, navigation, and remote sensing applications. The development of reusable launch vehicles, miniaturization of satellites, and lower launch costs have made the market growth faster.

Market Size and Forecast

-

Market Size (2026E): USD 18.44 Billion

-

Market Size (2035): USD 74.54 Billion

-

CAGR (2026–2035): 16.80%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on LEO Satellite Market - Request Free Sample Report

LEO Satellite Market Trends

-

Accelerating deployment of mega-constellation broadband satellite networks, with SpaceX Starlink serving approximately 8 million subscribers across 150+ markets in 2025 and Amazon Project Kuiper initiating full constellation deployment with its first 27 operational satellites in April 2025, confirming that broadband internet LEO constellations represent the largest single growth driver for the LEO satellite market through 2035.

-

Growing adoption of electric propulsion systems across LEO satellite platforms, with Hall-effect and ion thruster technologies now powering approximately 58.3% of operational LEO satellites in 2025 due to their superior fuel efficiency, reduced propellant mass, and ability to support long-duration constellation station-keeping missions that chemical propulsion systems cannot achieve within the same mass budget.

-

Rapid expansion of Earth observation and remote sensing LEO constellations delivering daily global imagery and near-real-time geospatial intelligence to agricultural, environmental monitoring, urban planning, disaster response, and defense customers, with Planet Labs, Maxar, and Airbus Defense leading commercial EO constellation deployments that provide multi-spectral and synthetic aperture radar imagery across more than 150 million square kilometers of monitored land surface area.

-

Integration of edge AI processing capabilities into LEO satellite payloads enabling on-orbit data processing, anomaly detection, and selective downlink of actionable intelligence rather than raw sensor data, reducing ground station bandwidth requirements and latency for time-critical Earth observation and maritime surveillance applications, with satellite edge computing representing a key technology differentiator among constellation operators through 2035.

U.S. LEO Satellite Market Size Outlook

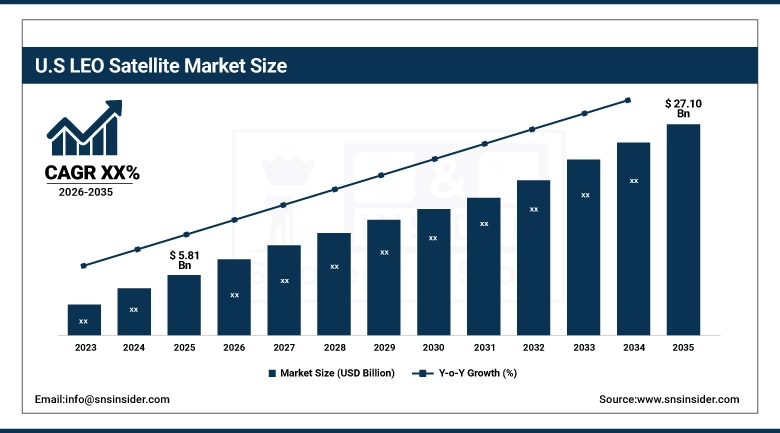

The U.S. LEO Satellite Market was valued at approximately USD 5.81 billion in 2025 and is expected to reach approximately USD 27.10 billion by 2035.

The U.S. LEO Satellites Market is growing owing to heavy investments made in satellite internet infrastructure, increase in defense and space modernization initiatives, and rising demand for real-time communication and earth observation services. The presence of leading space companies and efficient launch capabilities further drives market growth.

SpinLaunch's USD 12 million strategic investment from Kongsberg Defense & Aerospace in April 2025 for its Meridian Space LEO satellite broadband constellation, combined with Parsons and Globalstar's partnership to demonstrate the first software-defined satellite communication solutions in LEO announced in December 2024.

LEO Satellite Market Segment Analysis

-

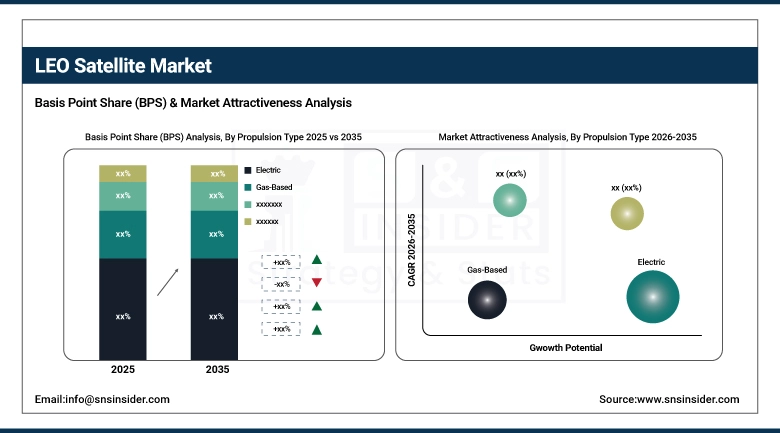

By Propulsion Type, electric propulsion dominated with approximately 58.30% market share in 2025; liquid fuel propulsion is the fastest-growing segment at a CAGR of approximately 17.85% from 2026 to 2035.

-

By Application, communication dominated with approximately 41.70% market share in 2025; earth observation & remote sensing is the fastest-growing application segment at approximately 18.35% CAGR from 2026 to 2035.

-

By End Use, commercial dominated with approximately 61.50% market share in 2025; government & defense is the fastest-growing end use at approximately 17.90% CAGR.

By Propulsion Type, electric dominates, liquid fuel grows fastest

Electric propulsion systems maintained their leadership in the LEO satellite market in 2025 with approximately 58.30% of market share, driven by the fundamental requirement of large-scale commercial constellations for fuel-efficient station-keeping technology that maximizes operational satellite lifetime within the propellant mass budget constraints of lightweight small satellite platforms.

Liquid fuel propulsion is the fastest-growing propulsion segment at approximately 17.85% CAGR through 2035, driven by the growing demand for high-thrust propulsion capabilities in LEO satellites requiring rapid orbital manoeuvrability, inclination change capability, and de-orbit compliance under evolving regulatory debris mitigation requirements, particularly for defense reconnaissance satellites, hosted payload platforms, and satellite servicing vehicles operating across multiple orbital planes within LEO altitude ranges.

By Application, communication dominates, earth observation & remote sensing grows fastest

Communication maintained its position as the leading application of the LEO satellite market in 2025 with approximately 41.70% revenue share, driven by the large-scale commercial broadband constellation deployment programs anchored by SpaceX Starlink, Amazon Project Kuiper, and Eutelsat OneWeb that are deploying the largest satellite constellations in human history to deliver global broadband internet access to underserved and remote populations, enterprise users, maritime vessels, and commercial aviation platforms.

Earth Observation & Remote Sensing is the fastest-growing LEO satellite application at approximately 18.35% CAGR through 2035, driven by the rapid commercialization of daily global imaging data services by Planet Labs, Maxar, Airbus Defense, and emerging EO startups delivering multi-spectral, hyperspectral, and synthetic aperture radar imagery to agricultural, environmental, infrastructure monitoring, and national security customers at price points and data refresh rates that legacy geostationary and reconnaissance satellite systems cannot provide.

By End Use, commercial dominates, government & defense grows fastest

Commercial end users maintained their dominant position in the LEO Satellite market in 2025 with approximately 61.50% revenue share, led by the subscription broadband revenue model of Starlink and Project Kuiper that scales recurring constellation revenue with every additional subscriber terminal, vessel, aircraft, or enterprise customer connected, creating the most scalable revenue model in satellite industry history.

Government & Defense applications represent the fastest-growing LEO satellite end use segment through 2035, driven by the accelerating modernization of national defense satellite communication networks, the proliferation of Space Force and allied nation military LEO satellite programs for signals intelligence, communications, and missile warning, and the growing government procurement of commercial LEO broadband and Earth observation services as military customers recognize that commercially operated satellite constellations can deliver strategic intelligence and communication capabilities at lower cost than dedicated government systems.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

68% |

|

Europe |

United Kingdom / France |

32% |

|

Asia Pacific |

China / India |

38% |

|

Middle East & Africa |

UAE |

20% |

|

Latin America |

Brazil |

35% |

North America LEO Satellite Market Insights

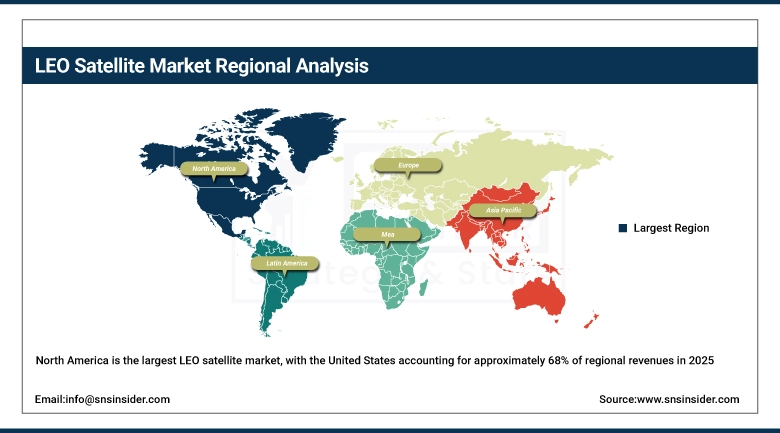

North America is the largest LEO satellite market, with the United States accounting for approximately 68% of regional revenues in 2025, driven by SpaceX's vertically integrated Starlink constellation and Falcon 9/Falcon Heavy launch dominance, Amazon's Project Kuiper deployment program, and U.S. government Space Force, NRO, and NASA procurement that collectively fund the world's most comprehensive LEO satellite industrial base. The United States hosts and funds the majority of global mega-constellation operator headquarters, satellite manufacturing capacity, and launch infrastructure, making North America the foundational region of LEO satellite market growth with a revenue base that sustains leadership through 2035 even as Asia Pacific and European market shares expand.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe LEO Satellite Market Insights

Europe represents a highly strategic LEO satellite market that features such initiatives as the OneWeb satellite constellation operated by Eutelsat delivering broadband connectivity services to corporate and governmental clients, satellite production capabilities of Airbus Defense and Space and Thales Alenia Space for both commercial and ESA programs, as well as the ESA investments in scientific, Earth observation, and navigation LEO demonstration projects. The cooperation between Orange and Telesat on integrating Telesat Lightspeed LEO satellite capacity into the European terrestrial network and the December 2024 purchase of 100 additional OneWeb satellites by Eutelsat from Airbus Defense and Space demonstrate the high momentum of LEO investments in Europe up until 2035.

Asia Pacific LEO Satellite Market Insights

Asia Pacific is the fastest-growing regional LEO satellite market with a projected CAGR of around 18.34% owing to China's increasing national LEO satellite constellation programs such as the Guowang 13,000-satellite broadband constellation and Honghu-3 commercial constellation, India's expanding commercial space industry due to the opening up of the satellite launch and manufacturing industries for private organizations, Japan's growing Earth observation and defense satellite investments, and South Korea's emerging satellite manufacturing and launching capabilities. It is the presence of both the national strategic satellite constellations and commercial satellite constellations in countries such as China, India, Japan, and South Korea that makes Asia Pacific the fastest-growing LEO satellite market.

Latin America and MEA LEO Satellite Market Insights

Latin America and MEA represent LEO satellite opportunities on account of the increasing use of LEO broadband services for rural and remote areas by private companies, procurement of government Earth observation satellites for agriculture, environment, and security purposes, as well as LEO satellite connectivity services for the maritime and aviation industries. Brazil represents the largest portion of Latin American revenues, around 35%, due to government satellite programs, large agricultural demand for Earth observation services, and Starlink broadband services in rural areas. MEA's LEO satellite adoption has been spurred by the investments made by the UAE in their space program and Vision 2030 in Saudi Arabia involving satellite technology.

Market Dynamics

Growth Drivers: Surging demand for global high-speed connectivity, declining launch costs, and expanding commercial earth observation applications driving broad-based LEO satellite constellation investment globally

Key factors driving the development of the LEO satellite market are the need for high-speed internet connectivity in underserved regions such as rural, remote, maritime, and aviation sectors where terrestrial infrastructure would not be economically feasible, the sharp reduction in cost per kilogram to launch a satellite to LEO from USD 10,000 in 2020 to below USD 3,000 in 2025 owing to the cost-effectiveness of SpaceX's Falcon 9 reusable rockets, making it economically feasible to deploy a constellation of satellites in orbit, and the increasing market for high-frequency Earth observation data that is attracting investments into deploying imaging constellations.

Orange's partnership with Telesat to integrate Lightspeed LEO satellite capacity into European terrestrial infrastructure, combined with MEASAT's MOU with Shanghai Spacesail Technologies for joint development and marketing of LEO satellite services signed in February 2025.

Restraints: Orbital congestion and space debris accumulation, complex regulatory spectrum coordination, and high upfront constellation capital requirements

One of the main limitations facing the LEO satellite market is the rapid growth of space debris and orbital congestion in the LEO altitude regions that are most valuable commercially, where the 14,000 debris objects in orbit moving at very high speeds pose collision hazards for the operational satellites requiring expensive active avoidance measures. The complexity of obtaining orbital spectrum coordination approval under international regulatory jurisdiction and spectrum filing at the International Telecommunication Union takes years and limits new constellation operator participation in the market and launches their commercial operations. The large amount of money required for the launch of constellations comprising hundreds to thousands of satellites prior to providing any commercial services prevents other operators from entering the market.

Opportunities: Direct-to-device satellite connectivity, LEO-enabled 5G backhaul, and expanding defense LEO constellation programs

Direct-to-device LEO satellite connectivity that allows regular smartphones to receive satellite broadband signals without specialized terminal equipment is a disruptive market opportunity, as AST SpaceMobile’s BlueBird constellation and SpaceX’s direct-to-cell Starlink offer will address the multibillion subscriber base that does not have terrestrial coverage, thus creating a new addressable market for LEO satellites that goes well beyond the existing user terminal-equipped subscribers. The use of LEO satellites for 5G backhaul at remote and rural mobile base stations is an emerging infrastructure market where the cost-prohibitive fiber and microwave backhaul links can be replaced by LEO broadband satellites, allowing mobile carriers to deploy 5G coverage in sparse areas at a fraction of the cost. The rising demand for defense LEO satellite communication and surveillance missions from NATO countries, Five Eyes countries, and Indo-Pacific allies creates a long-term premium government procurement opportunity for LEO communication and signal intelligence satellites.

Recent Developments:

-

April 2025: Amazon launched the first 27 operational Project Kuiper satellites on an Atlas V rocket, marking the initiation of full commercial LEO broadband constellation deployment as Amazon advances toward its committed deployment of over 3,200 satellites to deliver global high-speed internet services from low Earth orbit.

-

February 2025: MEASAT signed a memorandum of understanding with Shanghai Spacesail Technologies to jointly develop and market LEO satellite services, combining MEASAT's extensive satellite infrastructure with Spacesail's innovative LEO technologies to accelerate delivery of resilient global connectivity through expanded LEO capabilities across Asian and Pacific markets.

LEO Satellite Market Key Players are:

-

SpaceX (Starlink)

-

Amazon (Project Kuiper)

-

Eutelsat / OneWeb

-

Telesat (Lightspeed)

-

Planet Labs PBC

-

Airbus Defense and Space

-

Thales Alenia Space

-

Boeing

-

Lockheed Martin Corporation

-

Northrop Grumman

-

Iridium Communications Inc.

-

Globalstar, Inc.

-

AST SpaceMobile

-

Maxar Technologies Inc.

-

Kepler Communications

-

NanoAvionics

-

Kongsberg NanoAvionics

-

Spire Global

-

Satellogic

-

Tyvak Nano-Satellite Systems

LEO Satellite Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.77 Billion |

| Market Size by 2035 | USD 74.54 Billion |

| CAGR | CAGR of 16.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Propulsion Type (Electric, Gas-Based, Liquid Fuel) • By Application (Communication, Earth Observation & Remote Sensing, Scientific Research, Navigation, Technology Demonstration, Others) • By End Use (Commercial, Government & Defense, Others) • By Frequency Band (L-Band, S-Band, C-Band, X-Band, Ku-Band, Ka-Band, Q/V-Band, Laser/Optical) • By Satellite Mass (Small Satellites, CubeSats, Medium Satellites (180–1,000 Kg), Large Satellites (Above 1,000 Kg)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SpaceX (Starlink), Amazon (Project Kuiper), Eutelsat / OneWeb, Telesat (Lightspeed), Planet Labs PBC, Airbus Defense and Space, Thales Alenia Space, Boeing, Lockheed Martin Corporation, Northrop Grumman, Iridium Communications Inc., Globalstar, Inc., AST SpaceMobile, Maxar Technologies Inc., Kepler Communications, NanoAvionics, Kongsberg NanoAvionics, Spire Global, Satellogic, and Tyvak Nano-Satellite Systems. |

Frequently Asked Questions

Ans: Earth Observation & Remote Sensing is the fastest-growing application segment at approximately 18.35% CAGR through 2035.

Ans: Electric propulsion dominated with approximately 58.30% of revenues in 2025.

Ans: Rising demand for global connectivity, real-time data transmission, and rapid deployment of satellite constellations are driving LEO Satellite Market growth.

Ans: The LEO Satellite Market was valued at USD 15.77 billion in 2025.

Ans: The LEO Satellite Market is expected to grow at a CAGR of 16.80% from 2026 to 2035.

Get in Touch