Climate Adaptation Market Report Scope & Overview:

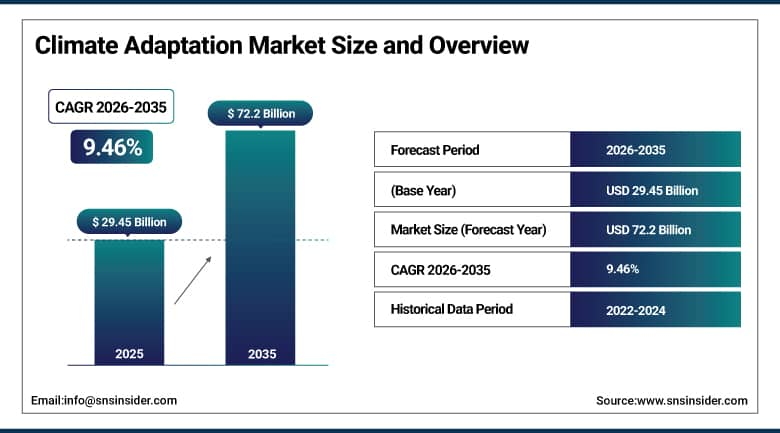

Climate Adaptation Market was valued at USD 29.45 billion in 2025 and is expected to reach USD 72.2 billion by 2035, growing at a CAGR of 9.46% from 2026-2035.

Climate change adaptation products have had great market prospects owing to the increasing frequency of extreme weather conditions, increased environmental concerns, and stricter regulations. Authorities and agencies have been constructing climate-proof infrastructures and implementing measures for water management and disaster control. There has been a demand for this since sustainability of the ecosystem is the primary concern.

The IPCC's Sixth Assessment Report estimates that limiting warming to 1.5°C requires adaptation investments of USD 127-357 billion annually by 2030 in developing countries alone. The U.S. National Climate Assessment (2023) documented economic losses from climate-related disasters exceeding USD 150 billion annually as a baseline, with projections suggesting acceleration without significant adaptation investment.

Climate Adaptation Market Size and Forecast

-

Market Size in 2025: USD 29.45 Billion

-

Market Size by 2035: USD 72.2 Billion

-

CAGR: 9.46% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Climate Adaptation Market - Request Free Sample Report

Climate Adaptation Market Trends

-

Nature-based climate adaptation solutions wetland restoration, urban tree canopy expansion, coastal mangrove rehabilitation are gaining institutional investment as their dual adaptation and biodiversity co-benefits attract blended public-private financing.

-

Climate risk disclosure mandates from the SEC, EU CSRD, and TCFD recommendations are driving corporate investment in climate vulnerability assessment and adaptation planning as compliance requirements rather than voluntary commitments.

-

Parametric climate insurance triggered by measurable weather events rather than assessed damages is expanding climate financial risk management to agricultural, infrastructure, and government clients that conventional insurance cannot serve effectively.

-

Urban heat island mitigation infrastructure cool roofs, permeable pavement, urban cooling centers is receiving municipal investment as extreme heat events increasingly exceed the thresholds at which public health impacts become acute.

-

Climate-resilient agriculture programs drought-tolerant crop varieties, precision irrigation systems, seasonal climate forecast integration are receiving government subsidy support as food system vulnerability to climate volatility grows.

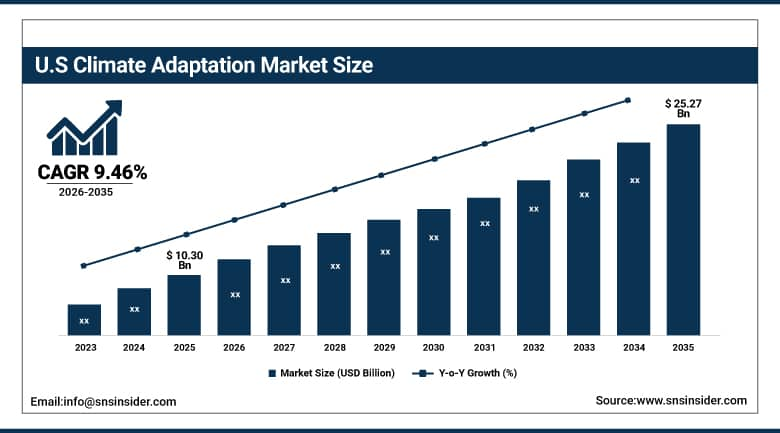

U.S. Climate Adaptation Market was valued at USD 10.30 billion in 2025 and is expected to reach USD 25.27 billion by 2035, growing at a CAGR of 9.46% from 2026-2035.

The U.S. climate change adaptation market is expected to witness growth owing to the occurrence of climate change-induced disasters, rising vulnerability of infrastructure assets, and investments in federal and state resilience programs.

FEMA's Building Resilient Infrastructure and Communities (BRIC) program allocated USD 2.3 billion for pre-disaster mitigation in fiscal year 2024. The U.S. National Oceanic and Atmospheric Administration (NOAA) reports that the number of billion-dollar disaster events in the U.S. has increased from an average of 3 per year in the 1980s to 20+ per year in recent years, creating economic pressure for proactive adaptation investment.

Climate Adaptation Market Segment Analysis

-

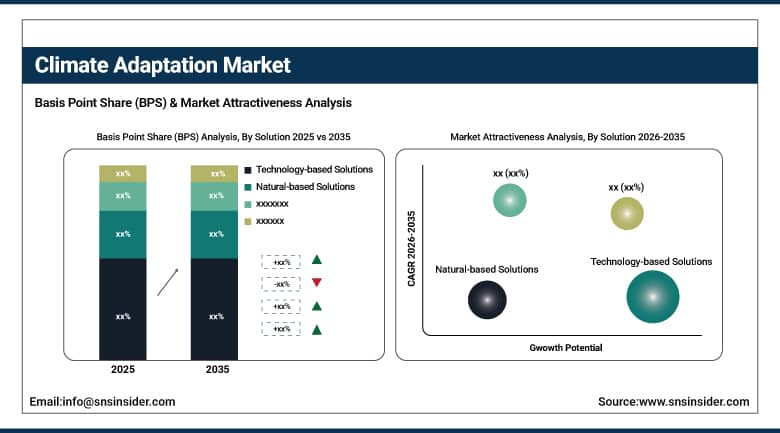

By Solution, Technology-based Solutions dominated the Climate Adaptation Market in 2025; Early Climate Warning & Environment Monitoring Solutions fastest growing.

-

By Industry, Government segment dominated the Climate Adaptation Market in 2025; Power Generation and Oil & Gas growing steadily.

By Solution, Technology-based Solutions dominate the Climate Adaptation Market, Early Warning growing fastest

Technology-based climate adaptation solutions held the dominant segment position in 2025, encompassing the broad range of engineered infrastructure seawalls and flood barriers, climate-resilient building materials, water recycling systems, drought-resistant irrigation, heat-resilient transportation infrastructure, and upgraded power grid designs that physically modifies assets and systems to reduce their vulnerability to climate impacts. These investments are the largest in absolute spending terms because they involve capital expenditure at infrastructure scale rather than services or monitoring subscriptions.

Early Climate Warning and Environment Monitoring Solutions are the fastest-growing segment, driven by the recognition that early warning capability delivers some of the highest returns of any climate adaptation investment documented studies show that USD 1 invested in multi-hazard early warning systems generates USD 4-10 in avoided disaster losses. Advanced weather forecasting using AI model ensembles, satellite-based flood and drought monitoring, real-time air quality surveillance networks, and wildfire detection systems using satellite and terrestrial sensor arrays are all expanding rapidly.

Climate Adaptation Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Europe |

Germany |

25% |

|

Asia Pacific |

China |

45% |

|

Middle East & Africa |

Saudi Arabia |

35% |

|

Latin America |

Brazil |

48% |

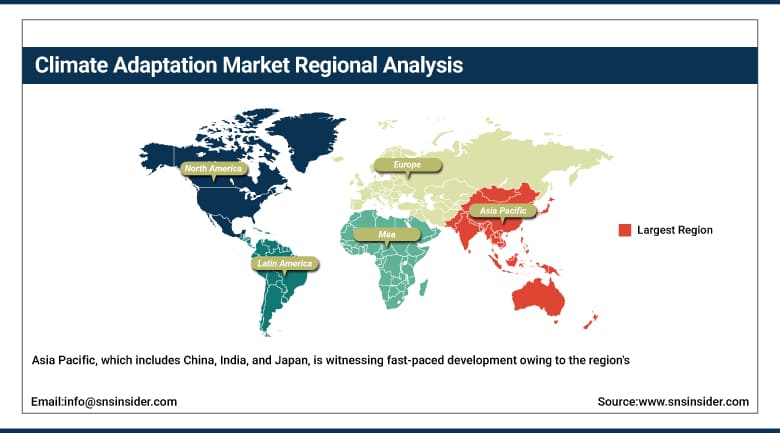

Asia Pacific Climate Adaptation Market Insights

Asia Pacific, which includes China, India, and Japan, is witnessing fast-paced development owing to the region's high vulnerability to climate change and high population density. Climate change is leading to rising sea levels, increasing temperatures, and variations in the monsoon system, and thus, governments are investing heavily in infrastructure for adaptation and agricultural practices that build resilience against climate change. Developing countries are increasingly resorting to water resource management and disaster management technologies to ensure sustainability. Funding from international agencies and public-private partnerships are important drivers for market development.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Climate Adaptation Market Insights

North America, especially comprising the US and Canada, is an example of a developed market for climate adaptation strategies that involves significant investments. This development is attributed to growing cases of wildfires, hurricanes, and floods, thus the need to invest more in infrastructure for effective management of natural disasters. Effective policies, funding from government bodies, and technology contribute to the deployment of climate adaptation methods. Private organizations and insurance companies interested in risk reduction also contribute to the growth of this sector. Smart cities, climate modeling, early warning system, and water management are some of the sectors receiving considerable attention.

Europe Climate Adaptation Market Insights

The continent of Europe, with Germany, France, and United Kingdom leading the way, demonstrates high levels of growth fueled by strict environmental laws and measures. Sustainable urban development and flood mitigation systems along with energy-efficient buildings are some of the priorities in the European Union. The measures adopted by the EU for climate change, including funding methods, have made it easier for investors to adopt adaptation technologies. There is increased understanding of climate change issues in the region, making carbon neutrality an important aspect for many companies.

Middle East & Africa and Latin America Climate Adaptation Market Insights

The Middle East and Africa, as well as Latin America, have been recognized as potential emerging markets in climate adaptation. The reasons for such growth in these two regions include higher exposure to droughts, water scarcity, and extreme weather conditions. Governments in these regions are focusing on making investments in order to better manage their water resources, prevent the further expansion of deserts, and develop adaptive agriculture. International assistance, climate funding, and NGOs have a considerable impact on projects being initiated. In Latin America, forests and land are major issues that need addressing.

Climate Adaptation Market Growth Drivers:

-

Escalating extreme weather events and mandatory climate risk disclosure requirements driving global climate adaptation investment

The increase in the climate adaptation industry has been facilitated by the hurricane seasons of 2024, the historic heatwaves in Europe, and the wildfires burning across Australia, whereby climate change is felt rather than read in scientific papers, reports, and literature. The refusal of insurance firms in Florida and California to underwrite properties that are seen to be too risky as it is no longer economically feasible to do so sends a subliminal message to property owners and potential investors that it is time to engage in climate adaptation practices. Mandatory climate risk reporting, including the SEC climate risk reporting regulation, CSRD in Europe, and climate risk disclosures for pension schemes mandated by the TCFD globally, have turned a voluntary process into corporate law, whereby companies engaging in certain businesses must assess their material climate risks, which translates into climate adaptation investments.

Swiss Re's Economic Research Institute estimates insured climate-related losses reached USD 109 billion in 2023, the fourth-highest annual total on record, contributing to insurance market withdrawal from climate-exposed regions. The Bank for International Settlements (BIS) has identified physical climate risk as a systemic financial stability concern, prompting central bank stress testing that is driving financial sector climate adaptation investment.

Climate Adaptation Market Restraints:

-

Fragmented regulatory frameworks and monitoring complexity limiting coordinated climate adaptation strategy implementation globally

There exist some real coordination challenges that may hinder the effectiveness of the climate adaptation investment process. The difference between laws and institutions at national, sub-national, and local levels can give rise to contradictory standards for climate adaptation, incentives, and reporting processes, thus making it hard for funding and technology transfers among different regions. Investments in climate adaptation take a very long time to generate any benefits, as is the case with the construction of a seawall designed to protect a city against the effects of climate change and with a lifespan of fifty years, posing a challenge against the budgetary process that favors short-term investments with budgetary implications.

Climate Adaptation Market Opportunities:

-

Carbon removal technology investment and climate resilience infrastructure finance creating significant climate adaptation growth opportunities

The climate adaptation market is seeing growth in two different types of opportunity sectors which are opening up new frontiers commercially for the climate adaptation market sector. This includes carbon removal, which uses direct air capture, enhanced weathering, biochar, and ocean alkalinity techniques to remove carbon from the environment as it has been established that emissions reduction alone will not result in climate stabilization. Firms such as Climeworks, Carbon Engineering, and many start-ups are establishing themselves in carbon removal with investments exceeding US$3 billion since 2020. Resilience infrastructure financing, which includes resilience bonds, climate risk insurance, and resilience loans, where interest rates are tied to climate adaptation outcomes, have established themselves as innovative funding mechanisms which will leverage private funds towards adaptation investment.

Recent Developments:

-

2026: World Bank launched its Climate Resilience and Adaptation Finance Toolkit (CRAFT), a USD 5 billion blended finance facility designed to mobilize private sector co-investment in climate adaptation infrastructure across developing nations, providing concessional lending and risk guarantees that improve project economics for adaptation investments in low-income countries facing the highest climate vulnerability.

-

2025: Google DeepMind released its GraphCast weather forecasting model for operational climate hazard prediction, achieving 10-day weather forecast accuracy comparable to the European Centre for Medium-Range Weather Forecasts (ECMWF) ensemble model at 1,000x lower computational cost, enabling more organizations to run high-resolution climate hazard forecasting for adaptation planning.

-

2025: Climeworks achieved 40,000 tonnes of annual CO2 direct air capture capacity at its Mammoth facility in Iceland the world's largest operational direct air capture plant establishing a commercial milestone for the carbon removal industry and demonstrating that gigaton-scale removal capacity is technically achievable with continuous scale-up investment.

Climate Adaptation Market Key Players

Some of the Climate Adaptation Market Companies

-

Siemens AG

-

Schneider Electric SE

-

Honeywell International Inc.

-

IBM Corporation

-

Microsoft Corporation

-

Amazon Web Services (AWS)

-

Xylem Inc.

-

Veolia Environnement S.A.

-

CH2M Hill (Jacobs Engineering)

-

AECOM Technology Corporation

-

WSP Global Inc.

-

Arcadis N.V.

-

Tetra Tech Inc.

-

Mott MacDonald Group

-

Black & Veatch Holding Co.

-

ICF International Inc.

-

Ramboll Group A/S

-

Wood PLC

-

Climeworks AG

-

Carbon Engineering Ltd.

Climate Adaptation Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 29.45 Billion |

| Market Size by 2035 | USD 72.2 Billion |

| CAGR | CAGR of 9.46% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution (Natural-based Solutions, Technology-based Solutions, Early Climate Warning & Environment Monitoring Solutions) • By Industry (Oil & Gas, Power Generation, Chemical & Petrochemical, Government, Education, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens AG, Schneider Electric SE, Honeywell International Inc., IBM Corporation, Microsoft Corporation, Amazon Web Services (AWS), Xylem Inc., Veolia Environnement S.A., CH2M Hill (Jacobs Engineering), AECOM Technology Corporation, WSP Global Inc., Arcadis N.V., Tetra Tech Inc., Mott MacDonald Group, Black & Veatch Holding Co., ICF International Inc., Ramboll Group A/S, Wood PLC, Climeworks AG, Carbon Engineering Ltd. |

Frequently Asked Questions

Ans: North America dominated the Climate Adaptation Market in 2025.

Ans: Early Climate Warning & Environment Monitoring Solutions is expected to register the fastest CAGR through 2035.

Ans: Technology-based Solutions dominated the Climate Adaptation Market in 2025.

Ans: The Climate Adaptation Market was valued at USD 29.45 billion in 2025.

Ans: The Climate Adaptation Market is expected to grow at a CAGR of 9.46% from 2026 to 2035.

Get in Touch