Mammography Workstations Market Report Scope & Overview:

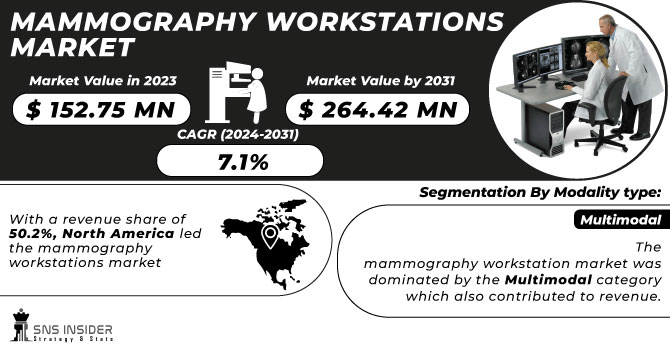

The Mammography Workstations Market Size was valued at USD 152.75 million in 2023, and is expected to reach USD 264.42 million by 2031, and grow at a CAGR of 7.1% over the forecast period 2024-2031.

A type of specialised system used for breast imaging is referred to as mammography. Low-dose x-ray imaging is used to find cancer before the patient notices any symptoms. It is well known to be a kind of non-invasive medical test that doctors frequently employ to diagnose and treat health disorders. Breast ultrasound, MR, and CR mammography, among other common radiography modalities, are just a few examples of the pictures that can be viewed, operated, evaluated, and stored by doctors using a mammography workstation.

Get more information on Mammography Workstations Market - Request Sample Report

One of the key factors propelling the expansion of the mammography workstation market is the rising incidence of breast cancer among people worldwide.

Consumer preference for less painful minimally invasive treatments is rising, and the industry is expanding as a result of more innovative product launches and swift FDA approvals. The modernisation of breast cancer screening to give patients more control and aid in decision-making, as well as the increase in research spending to create new technology for early breast cancer diagnosis, have a further impact on the market. Additionally, the market for mammography workstations is positively impacted by rising healthcare spending, high disposable income, a growth in the preference for long-term surgical fixes, improvements in healthcare infrastructure, and government initiatives to enhance medical technology.

MARKET DYNAMICS

DRIVERS

-

Breast cancer incidence is rising, and the elderly population is expanding.

-

Market Accessibility of Multimodality Diagnostic Platforms Has Increased

-

Raising awareness among patients of the clinical advantages of early disease detection

RESTRAINTS

-

Workstation and procedure costs for mammography are very high.

OPPORTUNITIES

-

Workflows for medical imaging that combine artificial intelligence and cloud technologies

CHALLENGES

-

Prohibitive Regulatory Requirements for Product Commercialization

-

Concerns with Breast Screening Programs

IMPACT OF COVID-19

Due to mandatory lockdowns and other restrictions set by the relevant governing bodies in response to the recent COVID-19 outbreak, the activities of several industries have either temporarily ceased or are operating with small personnel. The worldwide mammography workstation market is no exception, and this factor is anticipated to have a detrimental effect on this market's revenue growth in the years to come.

By Modality type

The mammography workstation market was dominated by the multimodal category, which also contributed to revenue. The extensive usage of these devices in hospitals and breast care facilities is primarily responsible for the segment's high market share. The multimodality workstation offers a high-resolution display and the capacity to contrast two-dimensional display and tomo synthesis images. These workstations also offer flexibility for reading specific settings and protocols.

During the projected period, the standalone workstation market is anticipated to grow at a profitable pace. The strong adoption of these gadgets is mostly to blame for the segment's high growth rate. Images and integration from several vendors and multimodality are made possible by the standalone workstation. These stand-alone workstations streamline complicated procedures to streamline practitioners' efforts. Images of breast tissue are automatically aligned by the gadgets, which combine data from many modalities in one place. Additionally, these gadgets offer patient history via a graphic patient record timeline and display computed and digital radiography on the screen.

By Application

The diagnosis screening category, which accounted for the biggest revenue share, led the market for mammography workstations. Mammography workstation utilisation in diagnostic screening accounts for a large portion of this segment's high market share. To detect breast cancer in its earliest, treatable stage, diagnostic screening is done on asymptomatic women. In addition, the expansion of the industry is being aided by an increase in breast screening programmes. A free mammogram is offered to women above 50 every two years as part of the national breast cancer screening program Breast Screen Australia.

During the projected period, it is anticipated that the advance imaging segment will expand at a profitable rate. The widespread use of these gadgets and the introduction of cutting-edge products are the main causes of the segment's strong growth rate. The system supports 3D breast ultrasound images, and Hitachi, GE Invenia ABUS, Siemens Acuson ABVS, and iVu Sophia have purchased it together with a diagnostic tool for interpretation and reading.

By End-use

The market for mammography workstations was controlled by the hospital sector, which also contributed the biggest revenue share. This is due to an increase in breast screenings and developments in mammography workstation technology. Furthermore, the segment is expanding due to rising healthcare spending as well as different government reforms. Using devices like mammography workstations, many OECD nations have implemented breast cancer screening programmes. As a result, the aforementioned elements support category expansion.

During the projected period, the breast care centre segment is anticipated to develop at the fastest rate. The increasing network of breast centres and increased awareness of breast care centres are the segment's main drivers. Complete diagnostic and preventative healthcare treatments are offered by these facilities.

KEY MARKET SEGMENTS:

By Modality type

-

Multimodal

-

Standalone

By Application

-

Diagnostic screening

-

Advance imaging

-

Clinical review

By End-use

-

Hospitals

-

Breast care centers

-

Academia

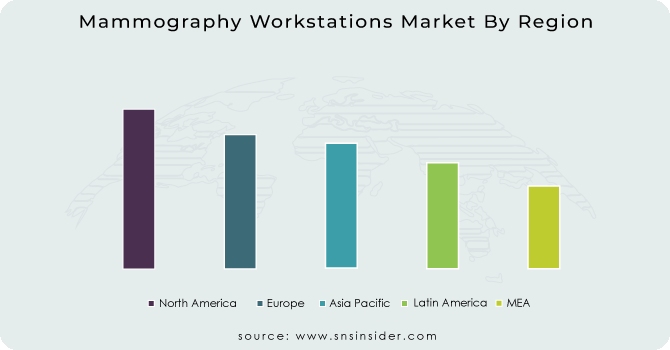

REGIONAL ANALYSIS

With a revenue share of 50.2%, North America led the mammography workstations market and is anticipated to continue to do so during the projected period. North America, Europe, Latin America, Asia Pacific, the Middle East, and Africa are the regional divisions of the mammography workstation market. The North American market for mammography workstations is growing as a result of an ageing population and an increase in new introductions. Rapid FDA approvals and ongoing technological development in the field of mammography are further factors fostering the region's expansion. Additionally, the existence of significant competitors in the sector is accelerating the market's expansion in the area.

The market is predicted to experience the quickest growth rate in Asia Pacific during the forecast period. The main drivers of market expansion are the growing elderly population and expanding public awareness of breast cancer early detection. The prevalence of breast cancer is lower in the Asia-Pacific region than it is in the West. The frequency has, nevertheless, significantly increased among Asian people. The area is home to about 27.0%of all breast cancer cases, the majority of which are in China and Japan. The market is expanding as a result of rising government financing for mammography programmes as well as ongoing technological advancements.

Need any customization research on Mammography Workstations Market - Enquiry Now

REGIONAL COVERAGE

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

KEY PLAYERS:

Some of the major key players are as follows: Analogic Corporation, Canon, Inc., General Electric (GE) Co., Hologic, Inc., Fujifilm Holdings Corporation, Mindray Medical International Limited, Koninklijke Philips N.V., Allengers Medical Systems Ltd., Siemens AG (Siemens Healthineers), Metaltronica S.p.A. and Other Players.

Fujifilm Holdings Corporation-Company Financial Analysis

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 152.75 Million |

| Market Size by 2031 | US$ 264.42 Million |

| CAGR | CAGR of 7.1% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Modality type (Multimodal, Standalone) • By Application (Diagnostic screening, Advance imaging, Clinical review) • By End-use (Hospitals, Breast care centers, Academia) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Canon, Inc., General Electric (GE) Co., Hologic, Inc., Fujifilm Holdings Corporation, Mindray Medical International Limited, Koninklijke Philips N.V., Allengers Medical Systems Ltd., Siemens AG (Siemens Healthineers), Metaltronica S.p.A. |

| DRIVERS | • Breast cancer incidence is rising, and the elderly population is expanding. • Market Accessibility of Multimodality Diagnostic Platforms Has Increased • Raising awareness among patients of the clinical advantages of early disease detection |

| RESTRAINTS | • Workstation and procedure costs for mammography are very high. |

Frequently Asked Questions

Manufacturer and service provider, research institutes, university and private libraries, suppliers, and distributors.

The report is divided into three segments: By Modality Type, By Application, and By End User.

Some of the main drivers are Market Accessibility of Multimodality Diagnostic Platforms Has Increased, and Raising awareness among patients of the clinical advantages of early disease detection.

Ans: The Mammography Workstations Market size is growing at a CAGR of 7.1% over the forecast period 2024-2031.

Ans: The Mammography Workstations Market siz e was valued at US$ 152.75 million in 2023.

Get in Touch