Medical Document Management Systems Market Report Scope & Overview:

Get more information on Medical Document Management Systems Market - Request Sample Report

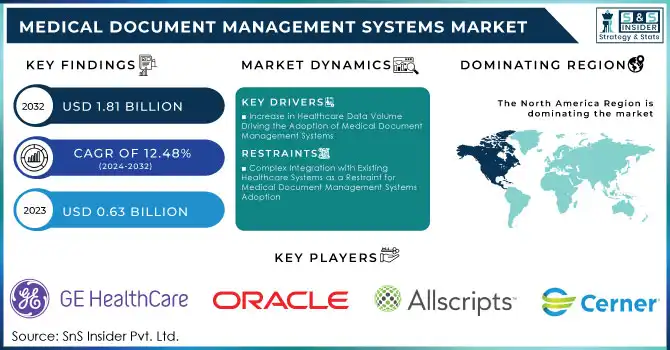

Medical Document Management Systems Market was valued at USD 0.63 billion in 2023 and is expected to reach USD 1.81 billion by 2032, growing at a CAGR of 12.48% from 2024-2032.

The Medical Document Management Systems market is growing due to increasing demand for seamless and secure management of healthcare data. The healthcare sector is producing large amounts of patient information, including electronic health records (EHRs) and diagnostic reports, which requires efficient systems for the organization and retrieval of this data. While Medical Document Management Systems overcome operational challenges, they have also been designed with stringently high regulatory standards in mind to improve the quality and safety of patient care. This aspect pertains to the rise in the trend of digital transformation within healthcare and the rising importance of advanced document management solutions.

The increasing uptake of Medical Document Management Systems responds to the growing need to beat inefficiencies and fragmentation in the management of data. Healthcare providers can access key information from various sources in an integrated platform, thus allowing speedy and secure access to such critical data. The increasing growth in telemedicine and digitized healthcare has further expanded the need for solutions that provide real-time access to documents to ensure that a patient gets uninterrupted and well-informed care. As of 2023, nearly half of the healthcare organizations in the United States have reported allowing the use of generative AI technology. This reflects the increasing adoption of advanced technologies in healthcare. The integration of AI improves the capabilities of MDMS by automating indexing, predictive analytics, and improved decision-making. Cloud-based technologies also strengthen data security and ensure seamless document management. rising importance of advanced document management solutions.

Looking ahead, the Medical Document Management Systems market is poised for sustained growth as healthcare systems continue to focus on patient-centric care and operational efficiency. Greater adoption of interoperability standards is fostering better data exchange and collaboration among healthcare entities, and innovations such as blockchain are redefining data security and trust in document management. As the emphasis on scalability and adaptability increases, MDMS will be key in transforming healthcare delivery as institutions can cope with the complexity of modern medical documentation while improving outcomes and quality of care for patients.

Medical Document Management Systems Market Dynamics

DRIVERS

-

Increase in Healthcare Data Volume Driving the Adoption of Medical Document Management Systems

With the increasing use of electronic health records, telemedicine, and chronic disease monitoring, unprecedented volumes of patient information are generated, and the efficient management of this data has now become crucial for smooth healthcare operations. Medical Document Management Systems solutions make available secure storage, fast retrieval, and streamlined workflows, allowing healthcare providers to manage large datasets effectively. They help ensure stringent regulatory standards while simultaneously improving accessibility and reducing the burden of administrative tasks. With a move towards paperless systems and value-based care, Medical Document Management Systems have come to be one of the essential tools in modern medicine.

-

Improved Patient Care and Operational Efficiency through Medical Document Management Systems Adoption

Medical Document Management Systems ensure that patient care is improved substantially through the rapid access and sharing of medical professional information with healthcare organizations. More effectively, this smooth flow allows fast decision-making, giving improved patient outcomes. Such a system of document management streamlines the process of retrieving records, thereby reducing more use of paper records since most of the time get used in searching for details. This leads to better resource use, allowing healthcare providers to focus on core tasks. Moreover, automation of the storage and retrieval of documents helps reduce paperwork, optimizing the administrative processes and making hospital and clinic operations more efficient. Medical Document Management Systems helps healthcare institutions provide better care while enhancing their internal workflows and productivity.

RESTRAINTS

-

Complex Integration with Existing Healthcare Systems as a Restraint for Medical Document Management Systems Adoption

Many of the healthcare organizations already deploy a wide variety of legacy systems such as Electronic Health Records (EHR), Laboratory Information Systems (LIS), and Radiology Information Systems (RIS). Since these legacy systems usually don't support newer MDMS platforms, integration can prove to be complex and expensive. The integration process of MDMS with these legacy systems is time-consuming, expensive, and requires technical expertise. Customizations may be necessary to ensure smooth data flow and interoperability, which would increase the overall cost and delay the adoption of Medical Document Management Systems. This challenge may deter smaller healthcare providers or those with outdated infrastructure from transitioning to MDMS.

Medical Document Management Systems Market Segment Analysis

BY PRODUCT

Solution segment led the medical document management systems market, capturing around 60% of the revenue share in 2023. This is attributed to the increasing demand for holistic platforms that integrate document management, data security, and workflow automation. Healthcare organizations are increasingly adopting these solutions to improve operational efficiency, ensure compliance, and streamline access to critical patient data.

The Service segment is expected to grow at the highest CAGR of around 13.54% during the period 2024-2032. This is due to rising demand for consulting, implementation, and support services. Health care organizations' increasing adoption of MDMS will make expertise services even more crucial, as they are required to guarantee smooth integration, customization, and after-sales system support.

BY END USE

The Hospitals & Clinics segment accounted for the largest revenue share of around 51% in 2023. This is due to growing need for efficient document management systems within healthcare settings that handle huge amounts of patient data. Increasingly, hospitals and clinics are adopting MDMS to make patient records more streamlined, enhance care coordination, and comply with regulations, hence making them the largest users of these solutions.

The Insurance Providers segment is expected to grow at the fastest CAGR of about 13.75% from 2024 to 2032. The rapid growth is due to the need for insurance companies to manage vast amounts of medical claims and patient data efficiently. In this context, the digitized health care landscape makes it imperative for insurance companies to opt for MDMS to streamline claim processing, secure data, and rule out any discrepancies regarding regulatory standards.

BY DELIVERY MODE

The Cloud-Based & Web-Based segment dominated the market of Medical Document Management Systems, with about 67% share of revenue in 2023 and is expected to grow at the fastest CAGR of 13.14% from 2024-2032. This is because there has been an increased adoption of cloud technology, which would be providing healthcare organizations scalable, cost-effective, and secure solutions for managing their patients' data. Cloud-based platforms provide easy access to medical documents from any location, promoting collaboration and improving operational efficiency. The growing preference for remote healthcare services and the need for data security further drive the rapid growth of this segment, as organizations seek flexible, reliable solutions that can adapt to evolving healthcare needs and regulatory requirements.

Medical Document Management Systems Market Regional Outlook

In 2023, North America dominated the Medical Document Management Systems market, holding the largest revenue share of about 44%. This is attributed to advanced health care infrastructure, widespread use of electronic health records, and stringent regulatory frameworks such as HIPAA, which promote the usage of secure and efficient systems for managing documents. MDMS solutions are being invested into in the region's healthcare by those companies for better patient care and easy operation and compliance with highly tightened data protection laws.

The Asia Pacific region is expected to grow at the fastest CAGR of about 13.75% from 2024 to 2032 due to rapid digitalization in the healthcare system, rise in healthcare investments, and growing demand for efficient management of documents in developing nations. Such countries as China and India, which are concentrating their effort on better access and infrastructure for healthcare, are driving the growth of the market in the region by requiring scalable and economical MDMS solutions to handle growing patient data.

Need any customization research on Medical Document Management Systems Market - Enquiry Now

Latest News -

-

In September 2024, Oracle introduced new electronic health record (EHR) innovations aimed at improving clinician productivity and patient care.

-

On November 26, 2024, Veradigm launched the Veradigm Ambient Scribe, an AI-powered solution that captures and transcribes real-time patient-provider interactions into structured medical notes, reducing clinician documentation time and enhancing patient care.

Key Players

-

3M (3M Health Information Systems, 3M ChartNet)

-

Kofax (Kofax PaperPort, Kofax TotalAgility)

-

GE Healthcare (GE Centricity, GE Healthcare Imaging Solutions)

-

Oracle (Oracle Healthcare Cloud, Oracle Health Information Management)

-

athenahealth, Inc. (athenaClinicals, athenaOne)

-

Veradigm LLC (Veradigm EHR, Veradigm Payer Solutions)

-

Allscripts Healthcare, LLC (Allscripts Sunrise, Allscripts TouchWorks)

-

Cerner Corporation (Cerner PowerChart, Cerner Millennium)

-

Hyland Software, Inc. (OnBase by Hyland, Hyland Healthcare Solutions)

-

McKesson Corporation (McKesson Enterprise Document Management, McKesson Paragon)

-

NXGN Management, LLC (NextGen Healthcare EHR, NextGen Healthcare PM)

-

ThoughtTrace, Inc. (ThoughtTrace Document Management, ThoughtTrace AI)

-

Laserfiche (Laserfiche Document Management, Laserfiche Workflow)

-

Midmark Corporation (Midmark Digital Radiography, Midmark Medical Record Management)

-

Agaram Technologies Pvt Ltd (MedNeo, MediSpire)

-

Nextgen Healthcare Information Systems, LLC (NextGen Ambulatory EHR, NextGen Practice Management)

-

Toshiba Corporation (Toshiba Medical Imaging Systems, Toshiba Medical Information Systems)

-

Siemens Healthcare GmbH (Siemens Healthineers, Siemens Soarian Health Information Management)

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 0.63 Billion |

| Market Size by 2032 | USD 1.81 Billion |

| CAGR | CAGR of 12.48% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Solution, Service) • By Delivery Mode (On-premise, Cloud Based & Web Based) • By Application (Patient Medical Record Management, Admission & Registration Document Management, Patient Billing Document Management) • By End Use (Hospitals & Clinics, Insurance Providers, Other Healthcare Institutions) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | 3M, Kofax, GE Healthcare, Oracle, athenahealth, Inc., Veradigm LLC, Allscripts Healthcare, LLC, Cerner Corporation, Hyland Software, Inc., McKesson Corporation, NXGN Management, LLC, ThoughtTrace, Inc., Laserfiche, Midmark Corporation, Agaram Technologies Pvt Ltd, Nextgen Healthcare Information Systems, LLC, Toshiba Corporation, Siemens Healthcare GmbH. |

| Key Drivers | • Surge in Healthcare Data Volume Driving the Adoption of Medical Document Management Systems. • Improved Patient Care and Operational Efficiency through MDMS Adoption. |

| Restraints | • Complex Integration with Existing Healthcare Systems as a Restraint for MDMS Adoption. |

Frequently Asked Questions

The Asia Pacific region is expected to grow at the fastest CAGR of 13.75% from 2024 to 2032.

North America dominated with a 44% revenue share in 2023 due to advanced healthcare infrastructure and widespread EHR adoption.

The Cloud-Based & Web-Based segment dominated with about 67% of the market share in 2023 and is expected to grow at the fastest CAGR of 13.14% from 2024 to 2032.

The Hospitals & Clinics segment led the market, accounting for 51% of the revenue share in 2023.

Medical Document Management Systems Market was valued at USD 0.63 billion in 2023 and is expected to reach USD 1.81 billion by 2032, growing at a CAGR of 12.48% from 2024-2032.

Get in Touch