Electronic Health Records Market Report Scope & Overview:

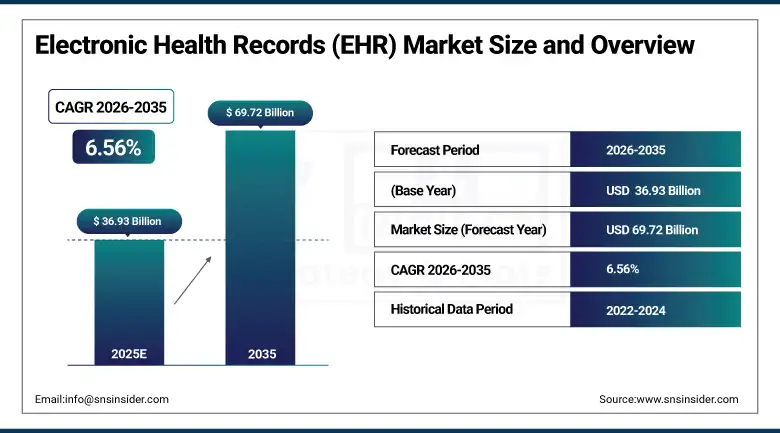

The Electronic Health Records Market size is valued at USD 36.93 Billion in 2025 and is expected to reach USD 69.72 Billion by 2035, growing at a CAGR of 6.56% over the forecast period of 2026-2035.

Global electronic health records market growth is fueled by the increasing digitalization of healthcare infrastructure, growing regulatory mandates for certified EHR adoption, and rising need for improved care coordination across hospital and ambulatory care settings. The growing volume of patient data, shortage of interoperable health IT systems, and increasing demand for better clinical outcomes are driving the adoption of EHR solutions across care settings worldwide. Massive funding from government as well as private health-care organization alongside the reimbursement structures supporting the use of certified EHRs are driving the global market. The COVID-19 pandemic has also been an inflection point for the digital transformation of healthcare delivery by demonstrating the importance of electronic health records in enabling telehealth, remote patient monitoring, and continuity of care in disrupted health systems.

In January 2025, the Office of the National Coordinator for Health Information Technology reported that over 88% of non-federal acute care hospitals in the U.S. had adopted a certified EHR system, reflecting the sustained momentum of government-backed EHR adoption programs across the country.

Electronic Health Records (EHR) Market Size and Forecast:

-

Market Size in 2025: USD 36.93 Billion

-

Market Size by 2035: USD 69.72 Billion

-

CAGR: 6.56% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Electronic Health Records (EHR) Market - Request Free Sample Report

Electronic Health Records Market Trends:

-

Wider shift toward web-based and cloud-hosted EHR platforms that reduce dependence on on-premise infrastructure, particularly among small and mid-size ambulatory practices.

-

Growing integration of AI-powered ambient documentation and clinical decision support tools within EHR platforms to reduce physician charting burden and improve documentation accuracy.

-

Increasing adoption of subscription-based EHR delivery models offering lower upfront costs and predictable pricing for healthcare organizations of varying sizes.

-

Expansion of FHIR-based interoperability frameworks driven by the 21st Century Cures Act, enabling more seamless exchange of patient data across care settings and health systems.

-

Rising demand for specialty-specific EHR configurations tailored to cardiology, oncology, behavioral health, and other clinically complex departments.

-

Growing integration of EHR platforms with remote patient monitoring devices, wearables, and telehealth portals to support chronic disease management and longitudinal care.

-

Increasing use of EHR-embedded population health analytics and quality reporting tools to support value-based care reimbursement and risk stratification at the provider level.

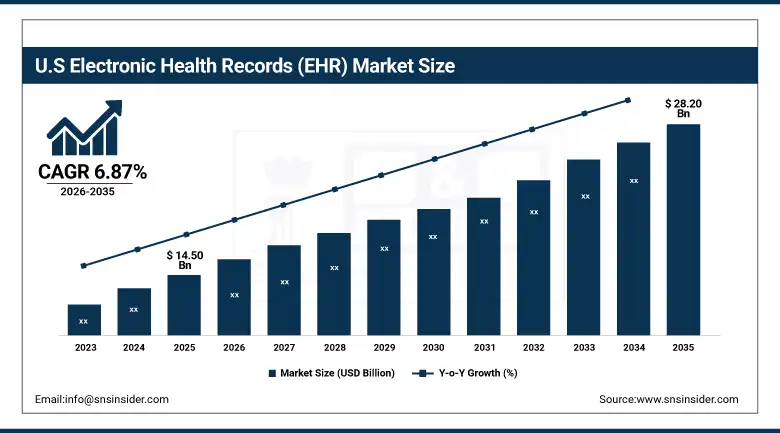

The U.S. Electronic Health Records Market is estimated at USD 14.50 billion in 2025 and is expected to reach USD 28.20 billion by 2035, growing at a CAGR of 6.87% from 2026-2035. The U.S. holds the largest market share as the U.S. electronic health records market is strongly supported by near-universal certified EHR adoption among hospitals, high healthcare IT spending, and the presence of leading EHR vendors such as Epic Systems and Oracle Health. Rising federal investment in health data interoperability, continued ONC rulemaking on information blocking, and the accelerating adoption of AI-assisted clinical documentation tools are further boosting market growth across the country.

Electronic Health Records (EHR) Market Growth Drivers:

-

Government Mandates and Regulatory Incentives for EHR Adoption Driving Market Growth

Well and truly driving the global electronic health records market are the government-backed regulatory mandates and financial incentive programs. In the U.S., the HITECH Act set up Medicare and Medicaid EHR incentive programs that increased the share of certified EHR adoption in hospitals from 46 percent in 2009 to over 88 percent by 2025, evolving through Meaningful Use to Promoting Interoperability to the ONC interoperability rules. The Hospital Future Act containing over EUR 4.3 billion in funding for hospital digital modernisation has come out of Germany, and India has registered over 340 million Health Ids so far as part of the Ayushman Bharat Digital Mission – creating a massive and structured demand pipeline for EHR rollouts. The sustained public sector commitments in key regions (US and EU) are creating a long-term momentum for electronic health records market growth till 2035, with national level policy induced adoption cycles adding to the vendor investments in platform development and interoperability potential.

For example, in March 2025, Te Whatu Ora Health New Zealand launched the Shared Digital Health Records project to consolidate patient data from across the country into a unified national platform, reinforcing the continued momentum of government-driven EHR infrastructure investment globally.

Electronic Health Records (EHR) Market Restraints:

-

High Implementation Costs and Interoperability Gaps Restricting Market Expansion

Critical factors hampering the electronic health records market growth includes high initial implementation cost and reducing interoperability issues[–]. While the deployment of enterprise EHR for large health systems can approach hundreds of millions of dollars, this represents a significant barrier to entry for smaller practices and hospitals in less affluent geographies. Inconsistent and divergent standards in the data, diverse implementation of the data formats through the API by different entrants in the eco-system, and the rights of patient data under the policies and protocols for security of health data in HIPAA & GDPR are creating barriers to free-flowing clinical data exchange across the care continuum. This ineffectiveness is propagated by physician pushback against EHR workflow modifications and also the high prevalence of clinician burnout ascribed to documentation burden, impeding wide-scale adoption, specifically with independent methods and specialized service providers, where switching costs stay an ongoing barrier.

Electronic Health Records (EHR) Market Opportunities:

-

AI Integration and Cloud-Based EHR Adoption Creating Significant Market Opportunities

The increased association of artificial intelligence with EHR platforms provides a huge market opportunity for the global electronic health records market. AI-enabled ambient documentation, automated coding, clinical decision support, and risk stratification are progressing out of pilot projects and becoming part of the workflow in leading EHR products. Cloud-based EHR delivery models have been able to expand the market to smaller practices and under-resourced health systems that simply have not had the infrastructure to support on premise deployment. Improving possibilities of precision medicine, chronic disease management of patients with multimorbidity and population health analytics predicated on their access to longitudinal and structured clinical records are also being opened when integrated EHR data with genomics platforms, wearable device feeds and remote monitoring systems becomes increasingly integrated.

For example, in July 2025, Experity launched Care Agent, an AI-driven patient assistant for urgent care designed to streamline patient communication, share discharge notes and lab results via secure SMS, and reduce administrative follow-up workload—offered free of charge to its existing EHR customer base, demonstrating the shift toward AI-native EHR feature delivery.

EHR Market Segment Analysis:

-

By product, the web-based EHR segment accounted for the largest share of 83.68% in 2025, and the client server-based EHR segment continues to hold relevance in large enterprise and government hospital settings.

-

By type, the acute care segment has registered the highest market share of about 45.57% in 2025, followed by the ambulatory care segment, which is anticipated to register the highest CAGR over the forecast period.

-

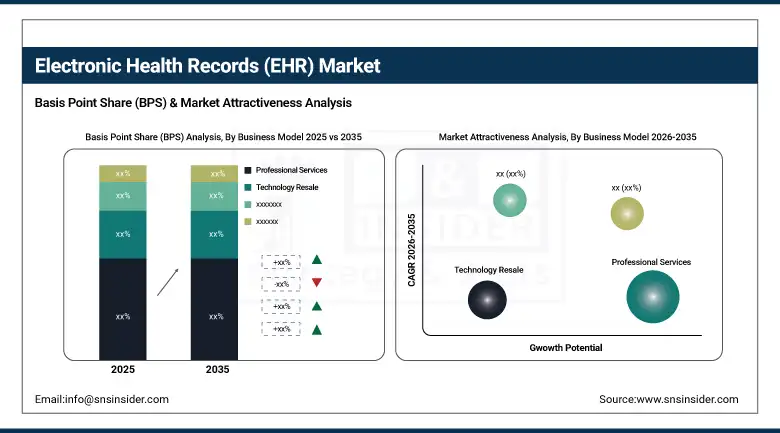

By business model, professional services held the dominant share of 32.60% in 2025, while the subscriptions segment is projected to grow at the fastest rate through 2035.

-

By end use, hospital use led the market with a share of nearly 58.29% in 2025, while the ambulatory use segment is expected to be the fastest-growing segment over the forecast period of 2026–2035.

By Product, Web-Based EHR Dominates, While Client Server-Based EHR Retains Enterprise Relevance

The web-based EHR segment held the largest revenue share of around 83.68% in 2025 as web-based platforms have seen very high acceptance among healthcare providers across both hospital and ambulatory settings. The growth of this segment is mainly attributed to the elimination of in-house server infrastructure requirements, lower total cost of ownership, and the ability to deliver rapid platform updates without hardware dependency. From 2026 to 2035, the web-based segment is anticipated to maintain dominance, specifically driven by the accelerating shift to cloud-hosted delivery models, growing FHIR-based interoperability mandates, and the increasing preference of smaller and independent practices for software-as-a-service EHR pricing structures. The client server-based segment retains relevance in government healthcare facilities and large hospital networks where offline operational capability and institutional data control remain important considerations for deployment decisions.

By Type, Acute EHR Leads the Market, While Ambulatory Registers Fastest Growth

The acute care segment contributed the largest share of about 45.57% of the electronic health records market revenue in 2025, owing to the high complexity of inpatient documentation requirements, large volume of clinical workflows across hospital admissions, and significant capital investments by hospital systems in comprehensive inpatient EHR platforms. The acute segment is mainly driven by regulatory compliance requirements, medication management needs, and the demand for real-time clinical decision support within hospital environments. On the other hand, the ambulatory EHR segment is anticipated to witness the highest CAGR over the forecast period of 2026–2035, driven by growing outpatient volumes, increasing preference for lightweight cloud-based platforms among physician practices, and heightened government focus on primary care digitalization across both developed and emerging markets. The post-acute segment, covering rehabilitation, long-term care, and home care settings, is also gaining momentum as care delivery continues to shift downstream from high-cost acute environments.

By Business Model, Professional Services Leads, While Subscriptions Registers Fastest Growth

The professional services segment contributed more than 32.60% revenue share in 2025 owing to the substantial deployment, customization, training, and ongoing support requirements involved in EHR implementation across hospital and health system environments. Large-scale EHR rollouts require extensive consulting, change management, and technical integration work, sustaining high demand for vendor-led and third-party implementation services. On the other hand, the subscriptions segment, which is driven by the shift to cloud-hosted platforms, predictable per-provider pricing, and lower capital expenditure requirements, is expected to record the highest CAGR over the forecast period of 2026 and 2035. This expansion is driven by the growing preference of ambulatory and mid-market healthcare organizations for operating expenditure-based EHR procurement and the proliferation of software-as-a-service delivery models across the health IT industry. The licensed software and technology resale segments continue to sustain incremental revenue among enterprise buyers and channel distribution partners.

By End Use, Hospital Use Leads, While Ambulatory Use Grows the Fastest

The hospital use category held the largest revenue share of 58.29% in the electronic health records market in 2025, on account of the scale and complexity of inpatient documentation, billing, and care coordination requirements within hospital environments. This is driven by the continued push by large health systems and academic medical centers toward fully integrated care platforms that consolidate inpatient, emergency, surgical, and ancillary department records within a single enterprise EHR system. However, the ambulatory use segment is anticipated to observe the highest CAGR over the forecasted period of 2026-2035, owing to the growing volume of outpatient visits globally, expansion of independent physician practices and multi-specialty group practices, and the accelerating adoption of affordable cloud-native EHR platforms among primary care, specialty, and urgent care settings. The increasing patient preference for outpatient and telehealth-based care models is further broadening the addressable market for ambulatory EHR solutions across all major geographies.

Electronic Health Records (EHR) Market Regional Highlights:

Asia Pacific Electronic Health Records Market Insights:

The Asia Pacific market is the fastest-growing regional market, with a strong CAGR over the forecast period, due to large-scale national digital health programs, rapidly expanding hospital infrastructure, and increasing government investment in health IT modernization. The key factors include the massive patient populations in China and India that generate a large volume of healthcare data, the rising prevalence of chronic diseases requiring longitudinal care records, and the proactive regulatory frameworks supporting health system digitalization. The region also benefits from a rapidly growing private hospital sector across Southeast Asia, substantial venture capital investments in health-tech startups, and joint efforts between academic institutions and healthcare organizations to develop region-specific EHR solutions suited to the diverse healthcare needs of the population.

North America Electronic Health Records Market Insights:

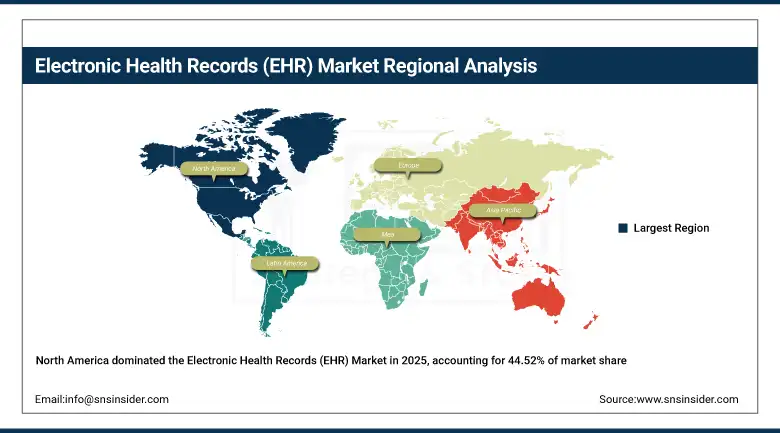

The electronic health records market in North America has showed the highest revenue share of 44.52% in 2025 owing to the presence of a mature healthcare IT infrastructure, high healthcare spending, and near-universal certified EHR adoption among hospitals. The key enablers are the existence of world-leading EHR vendors such as Epic Systems and Oracle Health, a highly developed health information exchange ecosystem, and favorable reimbursement and regulatory frameworks for certified EHR use. It is also supported by significant venture capital investment in health IT startups, ongoing federal interoperability rulemaking under the ONC, and accelerating adoption of AI-assisted clinical documentation tools across hospital and ambulatory care settings throughout the U.S. and Canada.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Electronic Health Records Market Insights:

European region accounts for the second most dominant market for electronic health records after North America. Solid government backing for digital health, the availability of rich longitudinal patient data through universal healthcare systems, and globally recognized research institutions in clinical informatics are all driving forces behind market growth in the region. Reasons for the growth of the electronic health records market in Europe are the coordinated European Health Data Space initiative enabling cross-border patient data exchange, Germany's Hospital Future Act mobilizing over €4.3 billion for hospital digital infrastructure, and the UK NHS target of 90% of trusts using comprehensive EHR platforms, all creating a structured and sustained demand environment for EHR adoption and upgrade investment across the region.

Latin America (LATAM) and Middle East & Africa (MEA) Electronic Health Records Market Insights:

Electronic Health Records Market in Latin America & Middle East & Africa would be driven by increasing public investment in healthcare infrastructure digitalization, growing smartphone and mobile internet penetration enabling cloud-based EHR deployment, and government initiatives to improve access to quality healthcare. The major factors for growth include national digital health programs in Brazil and Mexico supporting public hospital EHR adoption, Vision-led smart healthcare initiatives in UAE and Saudi Arabia driving regional health IT investment, and emphasis on affordable cloud-based EHR delivery suited to the infrastructure realities of emerging markets. There is an increasing number of health-tech startups across both regions developing EHR-adjacent solutions relevant to regional disease epidemiology and healthcare delivery constraints.

EHR Market Competitive Landscape:

Epic Systems (founded 1979) is the enterprise EHR leader in the U.S. acute care hospital market, with a 42.3% inpatient market share and over 280 million patients served globally on their integrated inpatient, ambulatory, and specialty care platform using a single unified database.

-

In August 2025, Epic Systems introduced a new suite of AI-powered tools for healthcare professionals and patients, including expanded collaboration with health insurance companies to improve care coordination and reduce administrative friction across integrated delivery networks.

Oracle Health: The second-largest U.S. hospital EHR vendor with enterprise EHR, data exchange and population health management solutions increasingly intertwined with Oracle Cloud Infrastructure and Oracle's wider enterprise tech stack. (Formerly Cerner, acquired by Oracle Corporation in 2022 for USD 28.3 billion)

-

In October 2024, Oracle unveiled its next-generation EHR platform built on Oracle Cloud Infrastructure at the Oracle Health Summit, embedding clinical AI agents, ambient documentation capabilities, and automated appointment preparation tools designed to modernize workflows for its legacy Cerner customer base.

Founded in 1999 eClinicalWorks is among the largest ambulatory EHR providers in the U.S. with a unified platform that includes EHR, practice management, revenue cycle management and patient engagement tools serving over 850,000 physicians, and strong growth momentum in AI-supported clinical documentation and automated care coordination across practices.

-

In March 2025, Contentnea Health selected eClinicalWorks' cloud-based EHR to manage integrated medical, dental, and behavioral health services across its facilities, leveraging the platform's unified care management capabilities to improve care quality and operational performance at scale.

Electronic Health Records Market Key Players:

-

Epic Systems Corporation

-

Oracle Health (Cerner)

-

eClinicalWorks

-

athenahealth

-

MEDITECH

-

NextGen Healthcare

-

Veradigm (Allscripts)

-

GE Healthcare

-

McKesson Corporation

-

Greenway Health

-

TruBridge

-

AdvancedMD

-

CureMD Healthcare

-

Netsmart Technologies

-

Practice Fusion

-

ModMed

-

CompuGroup Medical

-

DrChrono

-

CareCloud

-

Experity

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 36.93 Billion |

| Market Size by 2035 | USD 69.72 Billion |

| CAGR | CAGR of 6.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | By Product (Client Server-Based EHR, Web-Based HER) By Type (Acute, Ambulatory, Post-Acute) By Business Models (Licensed Software, Technology Resale, Subscriptions, Professional Services, Others) By End Use(Hospital Use, Ambulatory Use) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Epic Systems Corporation, Oracle Health, eClinicalWorks, athenahealth, MEDITECH, NextGen Healthcare, Veradigm, GE Healthcare, McKesson Corporation, Greenway Health, TruBridge, AdvancedMD, CureMD Healthcare, Netsmart Technologies, Practice Fusion, ModMed, CompuGroup Medical, DrChrono, CareCloud, Experity. |

Frequently Asked Questions

Ans: Government mandates and regulatory incentives for certified EHR adoption are a key factor driving the market growth.

Ans: The Electronic Health Records Market size is valued at USD 36.93 billion in 2025 and is expected to reach USD 69.72 billion by 2035.

Ans: The Electronic Health Records Market is expected to grow at a CAGR of 6.56% over the forecast period.

Ans: The web-based EHR segment dominated the market with a share of about 83.68% in 2025.

Ans: North America dominated the market, holding the highest revenue share of 44.52% in 2025.

Get in Touch