Medical Foods Market Report Scope & Overview:

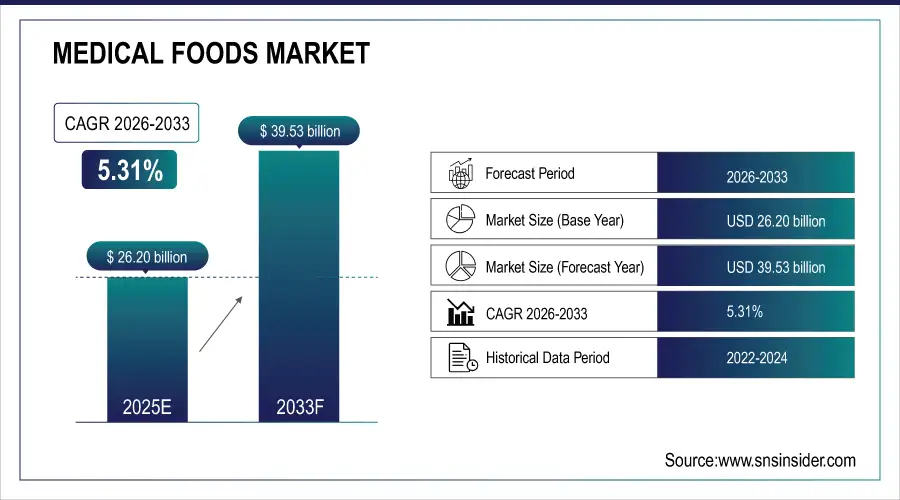

The Medical Foods Market Size is valued at USD 26.20 Billion in 2025E and is projected to reach USD 39.53 Billion by 2033, growing at a CAGR of 5.31% during the forecast period 2026–2033.

The Medical Foods Market analysis report offers an elaborate summary of market performance, focusing on product innovation and clinical nutrition advances and therapeutic application. Growing burden of chronic and metabolic disease and aspirations for disease-specific nutrition will drive sales through the rest of the forecast period.

Medical food consumption reached 1.8 million metric tons in 2025, driven by rising chronic diseases and increased use of therapeutic nutrition.

Market Size and Forecast:

-

Market Size in 2025: USD 26.20 Billion

-

Market Size by 2033: USD 39.53 Billion

-

CAGR: 5.31% from 2026 to 2033

-

Base Year: 2025

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information on Medical Foods Market - Request Free Sample Report

Medical Foods Market Trends:

-

There is a growing need for personalized and disease-specific nutrition, leading to advancements in the design of medical food formulations for chronic diseases.

-

Growing emphasis on clinical validation and regulatory clears is establishing credibility and driving healthcare integration.

-

Increasing adoption in hospitals and homecare settings is driving market growth.

-

Functional ingredients and bioavailability technologies are improving therapeutic effectiveness and patient outcomes.

-

Rising population of geriatrics and metabolic disorders is driving demand for disease specific nutrition solutions.

-

The development of plant-based, clean label medical foods is on the rise as we move toward natural and sustainable health products.

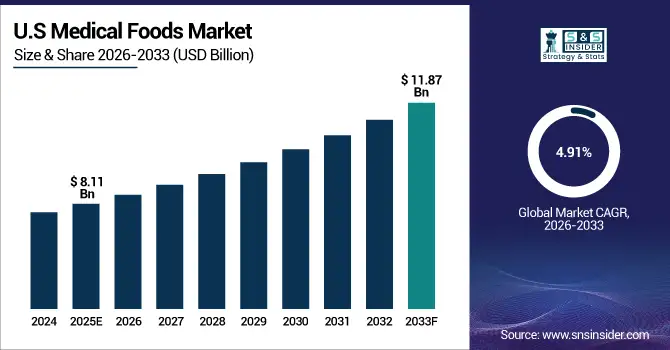

U.S. Medical Foods Market Insights:

The U.S. Medical Foods Market is projected to grow from USD 8.11 Billion in 2025E to USD 11.87 Billion by 2033, at a CAGR of 4.91%. Growth is being propelled by the increasing incidence of chronic diseases, growing clinical nutrition programs and an overall increase in personalized disease-specific dietary management solutions.

Medical Foods Market Growth Drivers:

-

Growing prevalence of chronic and metabolic disorders driving demand for disease-specific, clinically validated medical nutrition solutions.

The growing prevalence of chronic and metabolic disorders is a key driver of Medical Foods Market growth. As the prevalence of conditions such as diabetes, cancer and neurological disorders continues to grow on a scale, so creates the market for clinically validated, disease-specific nutritional solutions. Medical foods offer directed nutritional management to help meet therapeutic goals, minimize complications and support overall treatment. This movement toward personalized nutrition has the potential to change the way we approach how we manage chronic disease and rehabilitate patients.

Medical food grew 7.2% in 2025, driven by rising cases of chronic diseases and increasing adoption of disease-specific nutritional therapies across clinical and homecare settings.

Medical Foods Market Restraints:

-

Stringent regulatory classifications, high clinical validation costs, and limited reimbursement policies are constraining large-scale growth of the Medical Foods Market.

Stringent regulatory classifications, high clinical validation costs, and limited reimbursement policies are major restraints for the Medical Foods Market. Producers are subjected to complex approval systems under stringent medical and dietary rules, delaying product launches and driving up compliance costs. Requirement for large scale clinical evidence adds to development cost, when limited insurance coverage restricts patient access. Together, these factors present serious limitations to market accessibility, especially for new entrants focused on niche therapeutic nutrition categories.

Medical Foods Market Opportunities:

-

Growing focus on personalized nutrition and biotech innovation offers opportunities for advanced condition-specific medical food development.

Growing focus on personalized nutrition and biotech innovation presents a major opportunity for the Medical Foods Market. Progress in biotechnology allows for the production of individualized products matching the metabolic profiles or disease situations. Companies are developing bioactive ingredients, enhanced nutrient delivery options and clinical substantiation to bolster the efficacy of formulations. This move toward personalized, evidence-based nutrition builds brand trust, ensures patient compliance, and supports sustained growth in healthcare and wellness.

Personalized and condition-specific medical foods accounted for 27% of new product launches in 2025, driven by advancements in biotechnology and precision nutrition.

Medical Foods Market Segmentation Analysis:

-

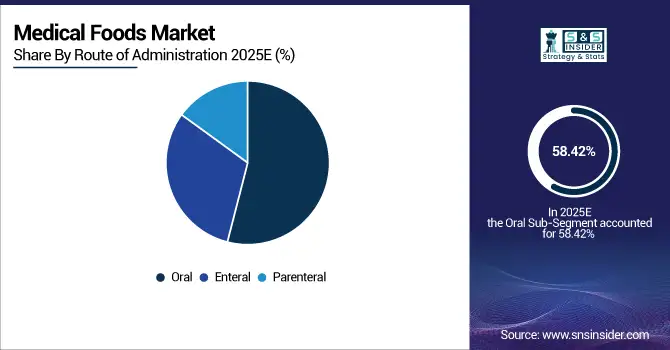

By Route of Administration, Oral held the largest market share of 58.42% in 2025, while Enteral is expected to grow at the fastest CAGR of 6.24% during 2026–2033.

-

By Product Type, Liquids accounted for the highest market share of 46.78% in 2025, while Powders are projected to expand at the fastest CAGR of 6.11% during the forecast period.

-

By Application, Diabetes dominated with a 33.69% share in 2025, while Neurological Disorders are anticipated to record the fastest CAGR of 6.43% through 2026–2033.

-

By Ingredient, Proteins held the largest share of 39.72% in 2025, while Omega-3 is expected to grow at the fastest CAGR of 6.32% during 2026–2033.

-

By End-Use, Hospitals accounted for the largest share of 48.15% in 2025, while Homecare is forecasted to register the fastest CAGR of 6.09% during 2026–2033.

By Route of Administration, Oral Dominates While Enteral Expands Rapidly:

Oral segment dominated the Market as it is convenient, improved patient compliance and are applicable for various chronic diseases including diabetes and cancer. Market available forms of oral medical foods are varied and commonly used both in hospitals and homecare. Enteral is the fastest growing segment to be growing rapidly owing to growing adoption of tube-fed nutrition in critical care and geriatric patients. In 2025, enteral feeding accounted for nearly 30% of clinical nutrition therapies globally.

By Product Type, Liquids Dominate While Powders Expand Rapidly:

Liquid segment dominated the market as they are easily absorbable, digestible and can be used for oral and enteral feeds. For critically ill patients who require accurate dosing and are in acute need of nutrition, they are the choice in many hospitals. Powder is the fastest growing segment, due to long shelf life and an opportunity to be customized to a specific recipe that fits homecare and outpatient nutrition. In 2025, powdered medical food products represented about 22% of new therapeutic nutrition launches.

By Application, Diabetes Dominates While Neurological Disorders Expand Rapidly:

Diabetes segment dominated the market with increase in number of diabetic patients requiring diet management for control over blood sugar levels and metabolic balance. Today, hospitals and clinics are ‘prescribing’ food specifically meant for people with diabetes to be used alongside traditional treatments. Neurological Disorders is the fastest growing segment, driven by upsurge in innovations for Brain-health formulations and nutrition awareness toward cognitive. In 2025, neurological-targeted medical foods accounted for 19% of R&D investments in clinical nutrition.

By Ingredient, Proteins Dominate While Omega-3 Expands Rapidly:

Proteins segment dominated the market due to its function in muscle recovery, immune system support and clinical treatment. They’re an important part of medical foods for metabolic stress and post-surgical patients. Omega-3 is the fastest growing segment, driven by robust science for cardiovascular and neuro benefits. Manufacturers are also developing new nutraceutical products that include omega-3s to treat chronic inflammation and brain health. In 2025, omega-3-based medical foods featured in over 28% of new product approvals.

By End-Use, Hospitals Dominate While Homecare Expands Rapidly:

Hospitals segment dominated the market due to being the main site for clinical nutrition therapy and dietary supervision. Their dosing and patient monitoring are tightly controlled. The homecare is the largest and fastest-growing market due to rise of personalized nutrition and telehealth services. Homecare is the fastest growing segment favored by patients for reasons of convenience and economy. In 2025, home-based medical nutrition usage increased by nearly 18% compared to the previous year.

Medical Foods Market Regional Analysis:

North America Medical Foods Market Insights:

North America dominated the Medical Foods Market, accounting for a 37.46% market share in 2025. Leadership of the region is attributed to organized healthcare set-ups, high incidence of chronic and metabolic diseases, and high adoption by clinics for disease-based nutrition. Strong R&D investment, favorable reimbursement policies and high awareness about therapeutic benefits of the medical nutrition intensify its leadership with North America at its heart for innovation and commercialization in economic landscape for medical foods market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Medical Foods Market Insights:

U.S. Medical Foods Market is predominantly driven by increasing chronic and metabolic diseases prevalence, increase in clinical nutrition awareness and growing physician-prescribed dietary treatment. Invention of bioactive ingredients, personalized nutrition and disease-targeted formulations will improve therapeutic results as significant R&D spending further reinforces the country’s role as a leading player in medical nutrition.

Asia-Pacific Medical Foods Market Insights:

The Asia-Pacific Medical Foods Market is the fastest-growing region, projected to expand at a CAGR of 6.41% during 2026–2033. Growth is mainly driven by growing awareness of clinical nutrition for improving patient care, increasing prevalence of lifestyle-related diseases, and rising geriatric population in China, India, Japan, and South Korea. Robust investments in biotechnology, personalized nutrition and hospital-based dietary programs also reinforce the role of Asia pacific as being the most dynamic region for medical foods industry.

China Medical Foods Market Insights:

China’s Medical Foods Market is driven by the rising prevalence of chronic diseases, growing awareness of clinical nutrition, and expansion of hospital-based dietary programs. Rising focus on biotechnology, locally manufactured therapeutic nutrition and personalized dietary solutions will position China as a primary growth contributor in the APAC medical foods market.

Europe Medical Foods Market Insights:

The Europe Medical Foods Market is flourishing due to the increasing prevalence of chronic & metabolic disorders and strong focus on clinical nutrition & preventive healthcare. Growing preference for condition-specific nutritional treatment and rising aging population contribute to the market growth. Major contributions are coming from Germany, the UK, France and Italy, thanks to well-established health care infrastructure, tough nutritional regulations and rising patient-specific and evidence-based medical nutrition solutions in hospitals and homecare.

Germany Medical Foods Market Insights:

Germany is a major Medical Foods market given its sophisticated healthcare ecosystem and robust clinical nourishment and patient care focus. Rising incidence of metabolic and neurological diseases fuels the demand for disease targeted formulations. In addition, personalized nutrition innovation, hospital-led dietary programs and stringent regulations all helped to maintain Germany’s dominance in the European medical nutrition market.

Latin America Medical Foods Market Insights:

The Latin America Medical Foods Market is anticipated to be rising due to increased awareness about clinical nutrition, increasing incidence of chronic and metabolic diseases and growing healthcare expenditure in Brazil, Mexico and Argentina. High demand for condition-specific formulas and a greater access to specialist nutritional therapies are driving growth in the region, improving patient outcomes.

Middle East and Africa Medical Foods Market Insights:

The Middle East & Africa Medical Foods Market is growing due to rising health care infrastructure, prevalence of chronic and metabolic diseases and awareness about clinical nutrition. Investments made in advanced hospitals, personalized diets and regulatory backup are increasing the demand in pivotal countries such as Saudi Arabia, UAE and South Africa that augments regional health.

Medical Foods Market Competitive Landscape:

Abbott, headquartered in the U.S., is a leader in the medical foods market, driven by its strong nutrition division and advanced clinical research. The company’s broad product portfolio also serves consumers with a variety of nutritional needs to help improve health and wellness, including products for people with diabetes. By leveraging its strong R&D, clinical validation and healthcare partners, Abbott further consumes the market with evidence-based formulations, patient-focused innovation and capability to mass produce for trust worthy availability.

-

In April 2025, Abbott launched “Glucerna Select,” a new medical nutrition formula for diabetes management. It features a low-glycemic carbohydrate blend, quality protein, and key micronutrients to support stable blood sugar and metabolic health, reinforcing Abbott’s leadership in diabetic nutrition innovation.

Nestlé Health Science, a subsidiary of Nestlé S.A. headquartered in Switzerland, leads the medical foods sector with an emphasis on personalized nutrition and therapeutic innovation. Its collection of products for chronic conditions and metabolic disorders, which includes Optifast, Peptamen and Modulen is based on nutrition science. Its operations, supported by extensive research staff and strict cooperative relations with medical institutions, also enable the company to incorporate nutrition into healthcare. They maintained this lead due to its ongoing innovation, clinical effectiveness and its ability to meet increasingly restrictive patient and regulatory demands.

-

In February 2025 the company launched a comprehensive GLP-1 Nutrition Support Platform in the U.S. addressing nutrition needs of individuals on GLP-1 therapies (weight-loss/diabetes drugs), covering muscle preservation, gut health, hydration and micronutrient support.

Danone’s Nutricia division, based in the Netherlands, is a major force in the medical foods industry, specializing in advanced clinical nutrition for infants, adults, and elderly patients. The company’s good name has been formed over decades of balanced expertise in metabolic and therapeutic nutrition, including Fortisip and Neocate. The company’s leadership is underpinned by its commitment to clinical research, sustainability and an integrated approach to health that connects science, nutrition and patient outcomes which support its medical nutrition offering.

-

In June 2025, Danone launched its “Iron Up!” programme to fight iron deficiency anaemia in children and women, combining science-based nutritional solutions, awareness campaigns, healthcare collaborations, and public–private partnerships to scale impact.

Medical Foods Market Key Players:

Some of the Medical Foods Market Companies are:

-

Abbott

-

Nestlé Health Science

-

Danone (Nutricia)

-

Fresenius Kabi

-

Baxter International

-

B. Braun Melsungen

-

Mead Johnson/Reckitt

-

Glanbia Performance Nutrition

-

Arla Foods

-

Otsuka Pharmaceutical

-

Alfasigma

-

Amerifit Brands

-

Stryker Corporation

-

Fonterra Co-operative Group

-

Royal DSM

-

Ingredion Incorporated

-

Kerry Group

-

Vitaflo International

-

Sterling Nutraceuticals

-

Cambrooke Therapeutics

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 26.20 Billion |

| Market Size by 2033 | USD 39.53 Billion |

| CAGR | CAGR of 5.31% From 2026 to 2033 |

| Base Year | 2025E |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Route of Administration (Oral, Enteral, Parenteral) • By Product Type (Pills, Powders, Liquids, Semi-Solid, Others) • By Application (Diabetes, Cancer, Metabolic Disorders, Neurological Disorders, Gastrointestinal Disorders, Others) • By Ingredient (Proteins, Vitamins, Minerals, Omega-3, Others) • By End-Use (Hospitals, Homecare, Clinics, Long-Term Care Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott, Nestlé Health Science, Danone (Nutricia), Fresenius Kabi, Baxter International, B. Braun Melsungen, Mead Johnson/Reckitt, Glanbia Performance Nutrition, Arla Foods, Otsuka Pharmaceutical, Alfasigma, Amerifit Brands, Stryker Corporation, Fonterra Co-operative Group, Royal DSM, Ingredion Incorporated, Kerry Group, Vitaflo International, Sterling Nutraceuticals, Cambrooke Therapeutics. |

Frequently Asked Questions

North America dominated the market with a 37.46% share in 2025, while Asia-Pacific is the fastest-growing region with a CAGR of 6.41% during 2026–2033.

Liquids dominated with a 46.78% share in 2025, while Powders are projected to grow at the fastest CAGR of 6.11% during 2026–2033.

Growth is driven by rising chronic disease prevalence, growing demand for personalized nutrition, and advancements in clinical nutrition science.

The market is valued at USD 26.20 Billion in 2025E and is projected to reach USD 28.53 Billion by 2033.

The Medical Foods Market is expected to grow at a CAGR of 5.31% during the forecast period 2026–2033.

Get in Touch