Metal Casting Market Report Scope & Overview:

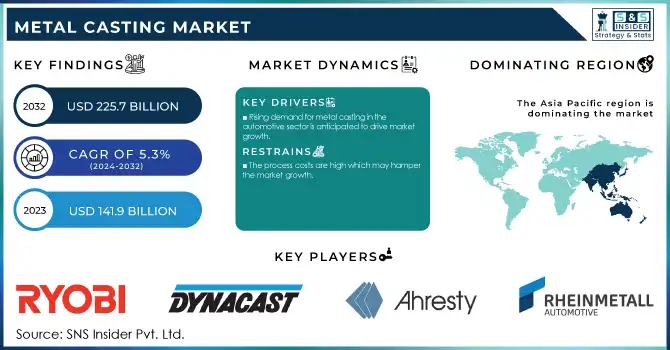

The Metal Casting Market Size was USD 141.9 billion in 2023 and is expected to reach USD 225.7 billion by 2032 and grow at a CAGR of 5.3% over the forecast period of 2024-2032.

Get more Information on Metal Casting Market - Request Sample Report

The expansion of the energy and power sector is significantly driving the demand for metal casting, particularly in renewable energy and power generation infrastructure. As nations transition to renewable energy, investment in wind, solar, and hydro projects is increasing quickly. High-quality cast parts including nacelles, hubs, and gearboxes are essential to wind turbines. Similarly, caster pieces are used in hydropower and thermal plants to ensure grant completion in incidental circumstances. Therefore, the need for improved casting techniques is growing along with the necessity for high-strength, custom-designed parts in these energy systems. The metal casting market is a major participant in the worldwide energy transition because the government supported this trend and its incentives for renewable energy.

The International Energy Agency (IEA) highlights that renewable power generation is set to overtake coal by 2025, with solar and wind dominating new installations. This evolution underscores the increasing demand for precision-engineered castings to ensure efficiency in renewable energy applications

The increasing use of aluminum and magnesium alloys is a transformative trend across various industries due to their lightweight, high-strength, and corrosion-resistant properties. Such materials are in particularly high demand within the automotive, aerospace, and electronics industries, were decreased component mass increases performance and fuel efficiency. For instance, the majority of automotive OEMs use cast aluminum engine blocks, cast aluminum cylinder heads, and cast aluminum transmission cases for reduced vehicle weight to comply with specific stringent emission norms and enforce fuel economy. Likewise, magnesium alloys became popular in aerospace as their excellent strength-to-weigh proportion offered a fantastic way to achieve decreased structural mass without compromising rigidity. Making matters worse, demand for electric vehicles (EVs) continues to climb, and these alloys are now at an even higher value, as lighter materials allow for an extended battery range and reduced energy consumption.

In 2023, the aluminum content in a typical U.S. vehicle was approximately 280 lbs, and the use of lightweight aluminum alloys continues to rise, driven by the need to meet stricter fuel economy standards and reduce carbon emissions.

Metal Casting Market Dynamics

Drivers

-

Rising demand for metal casting in the automotive sector is anticipated to drive market growth.

Increasing automotive industry requirements for cast components owing to performance, safety, and environmental standards is a major driving factor for metal casting market growth over the next eight years. As the automotive industry trends toward lightweight materials for better fuel economy and lower carbon emissions, aluminum, magnesium, and other alloy-cast metal parts are gaining further market momentum. Through these materials, high-strength and low-weight components can be produced such as engine blocks, cylinder heads, and suspension components. This demand is also due to the global getaway from fossil fuel vehicles towards electric vehicles (EVs) since automakers need cast components to improve battery performance and lighten vehicle weight.

Also, complex high-performance components for the automotive sector are produced using advanced casting processes in response to more stringent regulatory standards for combustion engine efficiency and safety. With increasing government regulations like the Corporate Average Fuel Economy (CAFE) standards in the U.S. and other similar frameworks in Europe and Asia pushing automakers to pursue lightweight casting solutions to meet fuel consumption and emissions target trends, the automotive manufacturing industry's requirement for metal casting is likely to grow, further fueling the metal casting market expansion.

Restraint

-

The process costs are high which may hamper the market growth.

Metal casting processes are cost-intensive, which is a major restraint for metal casting market growth. Casting operations, especially for high-value materials such as aluminum, magnesium, and titanium alloys involve costly machinery, skilled labor, and considerable energy pay-offs. The cost-saving potential from casting technologies lies in the very high initial equipment investment needed for setting up casting systems (purchase of molds, furnaces, and other equipment) and in the significant costs of maintaining complex systems. Moreover, processes such as die casting or investment casting providing precision components for automotive and aerospace use entail even higher operational costs (due to the complexity of process methods and the use of duly alloyed materials).

Such high process costs can restrict the metal casting solutions for small-scale manufacturers, especially ones with less-developed industrial infrastructure. These extra cost responsibilities might also cause some trouble in new industries or startups (which are typically limited in their budget plans) that could benefit from the adoption of metal casting technologies.

Metal Casting Market Segmentation Analysis

By Material

Aluminum held the largest market share around 40% in 2023. It is owing to its lightweight and relatively lower cost along with its applicability in a diverse number of industries. Aluminum is a single example of material specially used in automotive, aerospace, and construction sectors due to a rising need for lightweight material with sturdiness and dependability. Add to this its sublime corrosion resistance, ease of molding, and high recyclability, and it's not hard to see why. Aluminum casting, for instance, is widely used within the auto business in hardware parts similar to engine blocks, transmission instances, and chassis components to cut back vehicle weight and enhance gas effectivity. In addition, its low price compared with titanium or magnesium, combined with its excellent mechanical properties, makes aluminum the material of choice for high-volume manufacturing and custom applications.

By Application

The automotive & transportation sector held the largest market around 55% in 2023. Metal casting plays an important role in the fabrication of many automotive components such as engine blocks, transmission parts, wheels, and suspension and body structures. Due to the ever-growing emphasis on weight reduction in the automotive industry to enhance fuel economy and minimize emissions, casting-friendly metals like aluminum and magnesium have taken center stage. Production of EVs has become one of the major drivers of automotive casting, largely owing to the wide adoption of lightweight cast components for higher battery efficiency and greater range in electric cars.

Metal Casting Market Regional Outlook

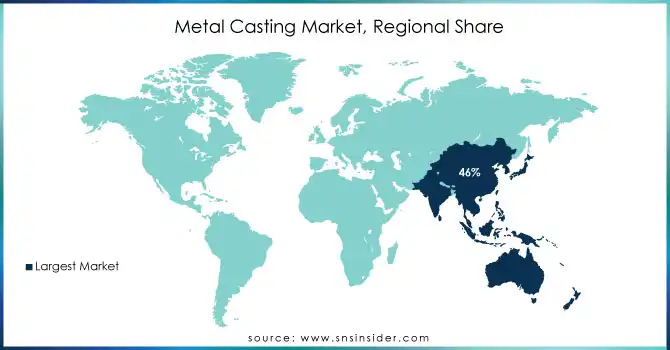

Asia Pacific held the highest market share around 46% in 2023 due to rapid industrialization, strong manufacturing capabilities, and demand in key sectors such as automotive, aerospace, and construction. Countries such as China, India, Japan, and South Korea are prominent consumers and producers of cast components due to the large-scale automotive manufacturing industries and infrastructure development projects in these countries. Automotive production is well established in the country, and his growing investment in electric vehicles EV boosts demand from the automotive sector for cast aluminum as a lightweight, high-strength material The competitive labor costs, productivity in engineering, and advanced manufacturing infrastructure coupled with government incentives for industrial development also enhance the growth of metal casting production in the region

In contrast, the growth of the automotive and transportation sectors in India has led to a rising demand for metal casting solutions. This industry is still one of the key consumers of metal cast parts in the region, as the automotive industry's mass production volume is still running at the top in the world. In addition, urbanization in Asia-Pacific countries is leading to increased infrastructure and construction projects, which is another factor supporting the demand for cast metal components in these industries.

Get Customized Report as per your Business Requirement - Request For Customized Report

Key Players

-

Ryobi Limited (Die-cast aluminum components, Engine parts)

-

Dynacast (Zinc die-cast components, Aluminum die-cast parts)

-

MINO Industry USA, Inc. (Die-casting machines, Precision die-cast parts)

-

Ahresty Corporation (Aluminum die-casting, Engine components)

-

GIBBS (Automotive castings, Die-cast aluminum products)

-

Rheinmetall Automotive AG (Aluminum castings, Engine parts)

-

Endurance Technologies Limited (Automotive components, Aluminum die-casting)

-

Aisin Automotive Casting, LLC. (Aluminum castings, Transmission components)

-

Nemak (Engine blocks, Transmission components)

-

Georg Fischer Ltd (Automotive components, Precision casting)

-

Castrol (Lubricants for casting, Industrial casting oils)

-

BASF (Casting resins, Chemical products for casting processes)

-

Alcoa Corporation (Aluminum castings, Automotive structural components)

-

Magna International (Aluminum die-casting, Automotive parts)

-

KSM Castings Group (Aluminum castings, Cylinder heads)

-

ZOLLERN GmbH & Co. KG (Steel castings, Gear components)

-

Eagle Aluminum Cast Products (Aluminum castings, Pressure die-cast products)

-

Precision Castparts Corp. (Aerospace components, Industrial castings)

-

Duncan Industries, Inc. (Sand castings, Engine parts)

-

Bühler Group (Die-casting machines, Precision parts)

Recent Development:

-

In 2024, Ryobi Aluminium Casting UK has significantly advanced its manufacturing capabilities, integrating cutting-edge processes into its operations. This includes the continued use of their patented Ryobi Shut Valve (RSV), a vacuum-assisted die-casting process.

-

In 2022, POSCO announced that its Pohang and Gwangyang steel plants received certification for their outstanding efforts in advancing sustainability within the steel industry. This achievement highlights the plants' strong dedication to environmental, social, and corporate governance (ESG) goals.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 141.9 Billion |

| Market Size by 2032 | US$ 225.7 Billion |

| CAGR | CAGR of 5.3% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Cast Iron, Aluminium, Stainless Steel, Zinc, Magnesium, Carbon Steel, High Steel Alloy, Others) • By Process Type (Sand Casting, Die Casting, Shell Mold Casting, Gravity Casting, Vacuum Casting, Investment Casting, Others) • By End-use (Automotive & Transportation, Building & Construction, Mining, Equipment & Machine, Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Ryobi Limited, Dynacast, MINO Industry USA, Inc., Ahresty Corporation, GIBBS, Rheinmetall Automotive AG, Endurance Technologies Limited, Aisin Automotive Casting, LLC., Nemak, Georg Fischer Ltd, and other players. |

| DRIVERS | • Emission and fuel efficiency rules that are strict • Lack of a different way to make things • More and more people are buying hybrid and electric cars. |

| Restraints | • The process costs a lot of money because it needs a lot of tools, dies, and energy. |

Frequently Asked Questions

The Metal Casting Market Size was USD 141.9 billion in 2023 and is expected to reach USD 225.7 billion by 2032 and grow at a CAGR of 5.3% over the forecast period of 2024-2032.

The process costs a lot of money because it needs a lot of tools, dies, and energy are the restraints for Global Metal Casting Market.

Ryobi Limited, Dynacast, MINO Industry USA, Inc., Ahresty Corporation, GIBBS, Rheinmetall Automotive AG, Endurance Technologies Limited, Aisin Automotive Casting, LLC., Nemak and Georg Fischer Ltd.

Manufacturers, Consultant, aftermarket players, association, Research institute, private and universities libraries, suppliers and distributors of the product.

Primary or secondary type of research done by this reports.

Get in Touch