Microservices in Healthcare Market Size Analysis:

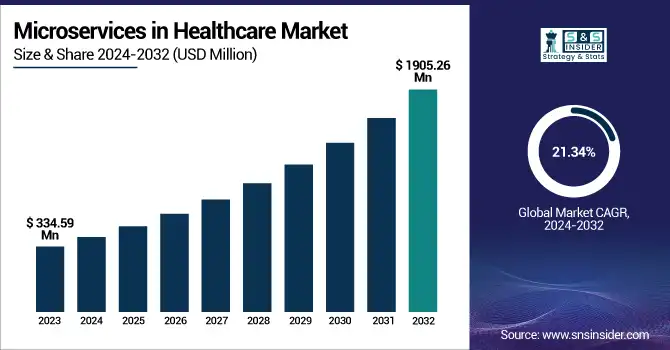

The Microservices in Healthcare Market size was valued at USD 334.59 million in 2023 and is expected to reach USD 1905.26 billion by 2032, growing at a CAGR of 21.34% over the forecast period 2024-2032.

The Microservices in Healthcare Market showcases its increasing adoption and significance. It details microservices adoption in healthcare organizations, underscoring performance and scalability improvements like downtime reduction and increased efficiency. The report also addresses the growing trend of healthcare APIs, which are enabling interoperability, and investment trends for microservices-based healthcare IT. It also covers regulatory implications with HIPAA, GDPR, FHIR and security implications. Legacy system integration insight with challenges and success rate details are also covered in the report. It provides an overview of the microservices revolution in healthcare IT, improving efficiency, security, and innovation.

Get more information on Microservices in Healthcare Market - Request Sample Report

The microservices in the healthcare market are fueled by the growing demand for effective and scalable healthcare solutions. With artificial intelligence, the healthcare spending of Americans is anticipated to be excessive, in alignment with digitalization and efficiency. The U.S. contributed the largest 36% to the global microservices market in 2023 due to its matured healthcare infrastructure and government initiatives that promote digital healthcare solutions.

Microservices in Healthcare Market Dynamics

Drivers

-

The increasing need for real-time data processing in healthcare is driving the adoption of microservices, enabling efficient management of vast amounts of patient data across various platforms.

The increasing need for real-time data processing in healthcare is significantly driving the adoption of microservices architecture, enabling efficient management of vast amounts of patient data across various platforms. Microservices handle modular, scalable, and agile IT solutions that are equally suited to cope with the ever-changing nature of healthcare data. This evolution is underscored by recent developments. One example of this would be the Patient Alerts Management Solution (PAMS) that was implemented in Royal Hobart Hospital, replacing paper-based charts with a digital form. For instance, the Royal Hobart Hospital implemented the Patient Alerts Management Solution (PAMS), transitioning from paper-based charts to a digital system. Since its launch in November, the average number of alerts recorded weekly has increased significantly, enhancing safety and reducing administrative work.

Similarly, TeleTracking's cloud-based software allows for tracking patients in real-time using electronic wristbands and the use of hospital control rooms to improve logistics, often leading to significant reductions in wait and turnaround times. Using TeleTracking’s system, for instance, the Maidstone and Tunbridge Wells NHS Trust has saved an estimated £2.1 million each year while substantially improving care standards. The Queensland Health Department set up a real-time data website that showed waiting lists, bed capacity, and emergency patient statuses in 25 major hospitals. The site refreshes every 30 minutes, facilitating patient flow and minimizing ambulance ramping. Such examples encompass the 360-degree view of real-time data processing in healthcare today, wherein microservices architecture plays a pivotal role in bolstering operational efficiency, patient safety, and health outcomes.

Restraint:

-

Data security and privacy concerns pose significant challenges to the implementation of microservices in healthcare, necessitating robust security measures to protect sensitive patient information.

Microservices adoption in healthcare is hindered by data security and privacy concerns. Microservices can be scaled and made more flexible but the same will create multiple points of entry, thereby increasing potential cyber-attacks. Each microservice communicates with APIs and may be exposed to unauthorized access or data breaches in the absence of strict security methods. Recent events highlight these weaknesses. Australian IVF clinic Genea was hit by a cyberattack in February 2025, resulting in the theft of nearly one terabyte of sensitive patient data, including medical records and personal information. The breach caused operational disruptions and underscored concerns about insufficient regulatory safeguards. In August 2024, virtual medical provider Confidant Health left an unsecured database that exposed over 120,000 files and 1.7 million activity logs leaving behind detailed medical histories and therapy session recordings in the wild. Microservices architectures became susceptible to such breaches, steering attention toward the criticality of robust security protocols. This may include also implementing comprehensive access control measures, encrypting data in transit and at rest, and undertaking regular security audits to protect sensitive health information. Also required to comply with regulatory frameworks, such as the Health Insurance Portability and Accountability Act (HIPAA), to maintain data security. Yet, these regulations can be difficult for healthcare organizations to comply with due to their complexity.

Opportunity:

-

Emerging markets present significant opportunities for the growth of microservices in healthcare, as these regions increasingly adopt digital healthcare solutions to modernize operations and improve patient care.

Microservices in Healthcare should have huge opportunities in the Emerging markets. Emerging markets have been adopting digital healthcare solutions rapidly to transform their operations and provide better patient-care. As an example, India’s Apollo Hospitals is hoping to invest in artificial intelligence (AI) to help reduce staff workload through processes such as automating medical documentation. This will free up two to three hours a day for front-line healthcare professionals enabling them to care for patients more effectively. Moreover, through public-private partnerships, the Edison Alliance's "1 Billion Lives Challenge" has connected more than 1 billion people to digital services including healthcare around the world. By harnessing digital connectivity, such as telemedicine, this initiative has not only improved access to medical services in underserved areas, but also proved transformative in the way healthcare is delivered. In addition, virtual hospitals, like Saudi Arabia's Seha Virtual Hospital, are setting the stage for further electronic integration. Seha, the world’s largest virtual hospital, collaborates with 224 hospitals and 44 specialized services, allowing it to provide remote medical assistance to patients via video consultations and monitoring devices. This model overcomes geo-logistical and resource availability challenges, further improving patient outcomes in emerging economies.

Challenge:

-

Integrating microservices with legacy healthcare systems remains a significant challenge, often due to the complexity and cost associated with migrating from outdated, monolithic architectures.

There are several major challenges that healthcare as an industry faces in integrating microservices into legacy systems that can affect the efficiency and effectiveness of healthcare delivery. According to a 2024 survey, 85% of healthcare IT initiatives face delays related to integration challenges, leading to negative impacts on patient care in 49% of those cases. One primary obstacle is the fragmentation of systems; as of 2024, only 55% of hospitals could electronically find, send, receive, and integrate patient information from external providers. Such fragmentation prevents interchangeable information from flowing smoothly, often resulting in incomplete patient files and human mistakes. Interoperability is hampered by the absence of standardized data formats and protocols. Organizations use different electronic health record (EHR) systems that utilize various data standards, complicating the goal of seamless data exchange.

Integration hurdles are compounded by security and compliance issues. More than 33 million healthcare records were breached in 2023, which underscores the necessity for strong cybersecurity practices in the integration of systems. Protecting patients' data while adopting additional technologies is essential for patients' confidence and to comply with regulations. Furthermore, higher implementation costs are also one of the major barriers, particularly for smaller providers. Many organizations want to migrate to microservices architectures, but system upgrades, new technology acquisition, and staff retraining corridors are expensive, and organizations continue to run legacy systems rather than move to the architecture.

Microservices in Healthcare Market Segmentation Analysis

By Component

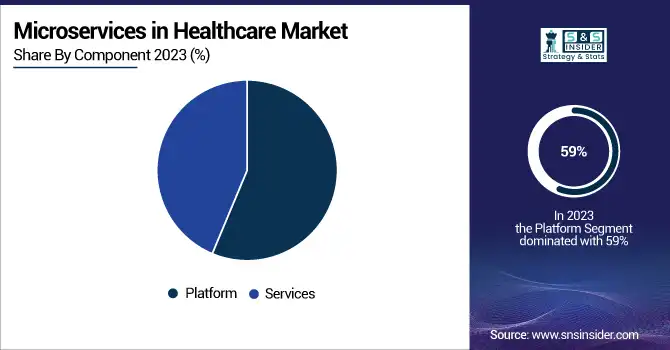

The platform segment accounted for the largest share 59% of the microservices in healthcare market in 2023. This dominance can be attributed to the platform's ability to provide a robust foundation for developing and deploying microservices, which are crucial for enhancing operational efficiency and scalability in healthcare. Government efforts, like promoting electronic health record (EHR) implementation, spurred demand for end-to-end integration of health services. This has been the case for the U.S. government as well, where regulations such as the 21st Century Cures Act to create standards for interoperability have been taking congratulations to be achieved if HealthCare is running on microservice platforms allowing to manage data easily and integrate the data. The platform segment also benefits from the ability to quickly develop and deploy applications–critical for healthcare organizations, which must respond swiftly to regulatory shifts and changing patient needs. Moreover, platforms create a framework within which to weave consulting, integration, training, support, and maintenance services into an integral solution, which makes it an absolute must-have for healthcare providers that aim to bolster their IT landscape. Microservice platforms are highly scalable and adaptable, which will help propel their usage in more and more healthcare applications.

By Deployment Model

The cloud-based models segment held the largest share of the microservices in the healthcare market in 2023. This is because cloud-based solutions are cost-effective, scalable, and flexible. Cloud technology has emerged as a go-to solution for healthcare providers seeking to improve data management while maintaining security. Microservices based in the cloud help organizations spend less on infrastructure and improve data storage and processing, vital for managing complex healthcare data. Moreover, cloud services offer access to maintenance and technical support that is less favourable in the case of on-premise data centers, and this is an added benefit for healthcare providers embracing flexibility without making heavy investments. Government initiatives to strengthen healthcare IT infrastructure support the rise of cloud-based microservices. North American governments, for example, have been advocating for the adoption of data-cloud computing in healthcare to drive data sharing and interoperability, critical to improving patient care. Healthcare applications will find this feature of the cloud quite useful because the healthcare sector requires agile and responsive IT systems that can support rapid deployment and scalability.

By End-use

In 2023, healthcare service providers accounted for the largest share of microservices in the healthcare market. This is primarily because of government push and mandates for providers to deploy digital solutions EHRs, telemedicine platforms, etc. As an example, the U.S. government's promotion of Meaningful Use has motivated healthcare providers to adopt EHR systems, which commonly have been implemented as microservices to interconnect and interoperate. Microservices are vital for healthcare providers to improve patient care with real-time data access and operational efficiency. Healthcare will require a dozen or so microservices to serve such functions as patient portals, appointment scheduling, EHRs, telemedicine platforms, and billing systems. They can construct and release these functionalities quickly and autonomously because of the microservices approach. Such flexibility is especially valuable in the health care sector, where providers must respond quickly to evolving patient needs and regulatory requirements.

Regional Insights

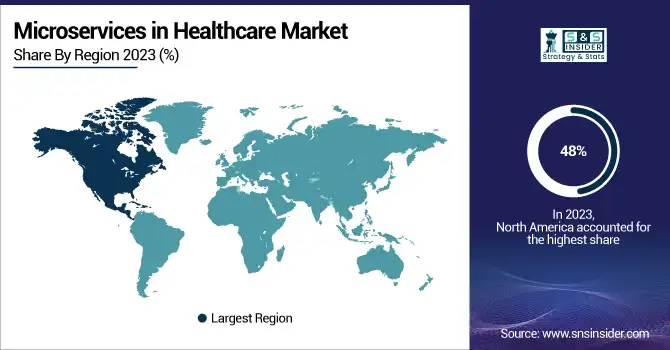

The North American region held a 48% revenue share in the microservices in the healthcare market during 2023 owing to developed healthcare infrastructure, and as well government support for digital health initiatives. It was also driven by high healthcare spending in the region and the presence of some of the biggest healthcare technology players. North America accounted for a designable market share in 2023, owing to the advanced healthcare system and the strong reform of the U.S. in healthcare innovation. North America is expected to lead the Service Management Software market owing to continuous technological advancements, rapid adoption of new technologies, and increasing inclination towards automation of services. Microservices have been further encouraged by the U.S. government's efforts to establish electronic health records and improve data sharing.

On the other hand, Asia-Pacific is growing with the fastest CAGR owing to increasing investment in healthcare technology and government initiatives to improve healthcare services. Rising per capita healthcare spending, substantial investment in healthcare technology, and a burgeoning healthcare infrastructure in developing countries all drive the growth of the Asia-Pacific region. This growth has mostly been driven by several countries, including China, Japan, and India, which require automation and digitalization of healthcare systems.

Need any customization research on Microservices in Healthcare Market - Enquiry Now

Microservices in Healthcare Market Key Players

Key Service Providers/Manufacturers

-

Epic Systems

-

Oracle Health

-

HealthHero

-

Abridge

-

CodaMetrix

-

Cohere Health

-

Neko Health

-

Lumeris

-

Grove AI

-

Infinitus Systems

-

Femmi

-

Locumate

-

BiVACOR

-

Pending AI

-

Lumos Diagnostics

-

Sicona Battery Technologies

-

Aquila

-

Pfizer

-

Eli Lilly

Recent Development in the Microservices in Healthcare Market

-

In February 24, 2024 Philips released an article about how the patient care transformation, healing patients through healthcare interoperability, with microservices.

-

AWS HealthScribe was launched in 2024, and it applies generative AI to automate clinical documentation.

-

In 2024, Microsoft launched Azure Health Data Services, which consolidates transactional and analytical healthcare data workflows onto the same platform.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 334.59 Million |

| Market Size by 2032 | USD 1905.26 Million |

| CAGR | CAGR of 21.34% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Delivery Model (On-premise Models, Cloud-based Models) • By Component (Platforms, Services) • By End user (Healthcare Providers, Healthcare Payers, Lifesciences Industry, Research Organizations) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | InterSystems, Epic Systems, Oracle Health, HealthHero, Abridge, CodaMetrix, Cohere Health, Neko Health, Lumeris, Grove AI, Infinitus Systems, Femmi, Locumate, BiVACOR, Pending AI, Lumos Diagnostics, Sicona Battery Technologies, Aquila, Pfizer, Eli Lilly |

Frequently Asked Questions

Ans: The Platforms Services segment dominated the Microservices in Healthcare Market.

Ans: The increasing need for real-time data processing in healthcare is driving the adoption of microservices, enabling efficient management of vast amounts of patient data across various platforms.

Ans. The CAGR of the Microservices in Healthcare Market is 21.34% during the forecast period of 2024-2032.

Ans: The North America region dominated the Microservices in Healthcare Market in 2023.

Ans. The projected market size for the Microservices in Healthcare Market is USD 1905.26 billion by 2032.

Get in Touch