Monosodium Glutamate Market Report Scope & Overview:

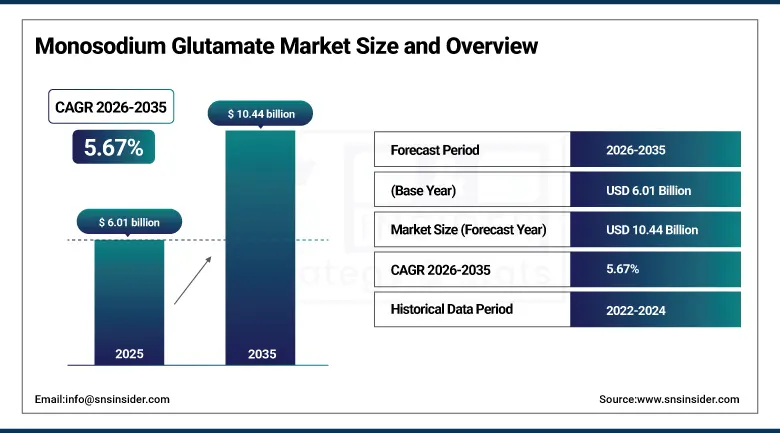

The Monosodium Glutamate Market was valued at USD 6.01 billion in 2025 and is expected to reach USD 10.44 billion by 2035, growing at a CAGR of 5.67% from 2026-2035.

The expansion of the Monosodium Glutamate Market is fueled by the growing preference for processed foods, ready-to-eat foods, salty snacks, and convenience food products around the world. Rising urbanization, hectic lifestyles of consumers, and high intake of restaurant foods and fast foods are propelling higher use of MSG in food preparations. The growing preference for Asian cuisines and umami-taste products is boosting the market demand. Moreover, rising growth of the food processing industry, surging sale of packaged foods, and the economic advantages provided by MSG are fueling market growth in the coming years.

In Northern Nigeria, unbranded and adulterated MSG is widely sold in markets despite health warnings, driven by low cost and local food preferences. A Sokoto warehouse was recently sealed by NAFDAC for stocking over 5,000 bags of unregistered MSG, highlighting regulatory and health concerns.

Monosodium Glutamate Market Size and Forecast

-

Market Size in 2025: USD 6.01 Billion

-

Market Size by 2035: USD 10.44 Billion

-

CAGR: 5.67% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Monosodium Glutamate Market - Request Free Sample Report

Monosodium Glutamate Market Trends

-

Rising demand for flavor enhancement in processed and packaged foods is driving the monosodium glutamate (MSG) market.

-

Growing adoption across snacks, soups, sauces, ready-to-eat meals, and foodservice applications is boosting market growth.

-

Expansion of convenience food consumption and changing dietary lifestyles is fueling product demand.

-

Increasing focus on improving taste profiles and reducing sodium content in food products is shaping adoption trends.

-

Advancements in fermentation technologies and clean-label production methods are enhancing manufacturing efficiency and product quality.

-

Rising demand from the food processing and restaurant industries is supporting market expansion.

-

Collaborations between food ingredient manufacturers, packaged food companies, and restaurant chains are accelerating innovation and global adoption.

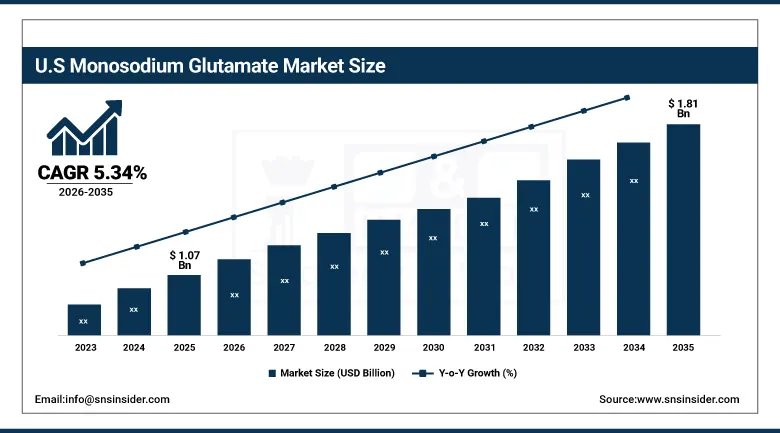

U.S. Monosodium Glutamate Market was valued at USD 1.07 billion in 2025 and is expected to reach USD 1.81 billion by 2035, growing at a CAGR of 5.34% from 2026-2035.

The Growth of the US Monosodium Glutamate Market is fueled by an increase in the consumption of processed food products, rising popularity of Asian cuisine, and growth of the fast food industry chain. Manufacturers are resorting to MSG in their food products in order to improve taste and decrease sodium content.

Monosodium Glutamate Market Segment Highlights

-

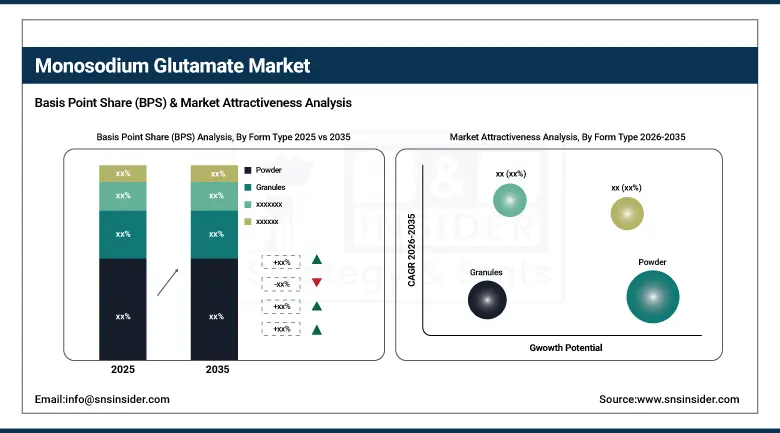

By Form Type, Powder segment dominated the Monosodium Glutamate Market in 2025 with ~68% share; Granules segment fastest growing during 2026–2035.

-

By Application, Noodles, Soups, and Broths segment dominated the Monosodium Glutamate Market in 2025 with ~36% share; Seasonings & Dressings segment fastest growing during 2026–2035.

-

By Distribution Channel, B2B segment dominated the Monosodium Glutamate Market in 2025 with ~72% share; B2C segment fastest growing during 2026–2035.

Monosodium Glutamate Market Segment Analysis

By Form Type, Powder segment dominates the Monosodium Glutamate Market, Granules segment expected to grow fastest

Powdered form leads the MSG market owing to its greater solubility, blendability properties, and usage in processed and packaged foods. The powdered form of MSG is preferred by food producers since it allows an even spread of taste while preparing soups, snacks, instant noodles, and seasoning blends. Increased shelf life, storage convenience, and cost savings on transportation make the product more viable for mass production. Furthermore, powdered form has great compatibility with automatic food production systems across the globe.

Granules is experiencing rapid expansion driven by growing demand for premium-seasoning products that provide efficient dispensing and good texture preservation. Caterers and households favor granular MSG because of its easy handling and lower dust generation upon usage. Increasing consumption trends of gourmet meals, flavored seasonings, and ready-to-eat foods have further fueled demand. Moreover, MSG producers are developing sophisticated granular formulas for improved stability and consistency in flavors.

By Application, Noodles, Soups & Broths segment dominates the Monosodium Glutamate Market, Seasonings & Dressings segment expected to grow fastest

Noodles, soups, and broths dominate the monosodium glutamate market owing to the high usage of MSG as a flavor enhancer in these applications. Demand for convenience and quick-to-make meals continues to remain strong around the world. In addition, MSG helps manufacturers to improve the taste of such food products at an affordable cost. Urbanization and changing lifestyles have also fueled the popularity of such applications.

Seasonings and dressings are expected to register rapid growth in the years ahead because of the growing preference for flavorful seasoning products and spice blends. As consumers become more interested in the cuisines of other countries as well as fusion foods, they look for ways to make their cooking taste better. The availability of packaged seasoning and gourmet food products will be driving the growth of the segment.

By Distribution Channel, B2B segment dominates the Monosodium Glutamate Market, B2C segment expected to grow fastest

The B2B market segment leads due to the fact that monosodium glutamate is mainly distributed in bulk form to food processing companies, restaurants, snack makers, and food processing companies. Industrial consumption in large volumes within the packaged foods, frozen foods, and foodservice markets strongly contributes to the leading position in the market. The manufacturers' preference for purchasing the commodity directly in bulk helps sustain the leading position of this market segment.

The B2C segment is experiencing rapid growth due to the growing use of flavoring products by consumers while preparing food items in their households. Growing awareness among consumers about umami seasoning and experimenting with foods like that prepared in restaurants is also driving demand from the consumer side. Expansion in supermarkets, e-commerce websites, and online grocery delivery services is making the product easily accessible to the consumers.

Monosodium Glutamate Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

81.5% |

|

Europe |

United Kingdom |

16.8% |

|

Asia Pacific |

Australia |

6.9% |

|

Middle East & Africa |

UAE |

18.4% |

|

Latin America |

Brazil |

46.7% |

Asia Pacific Monosodium Glutamate Market Insights

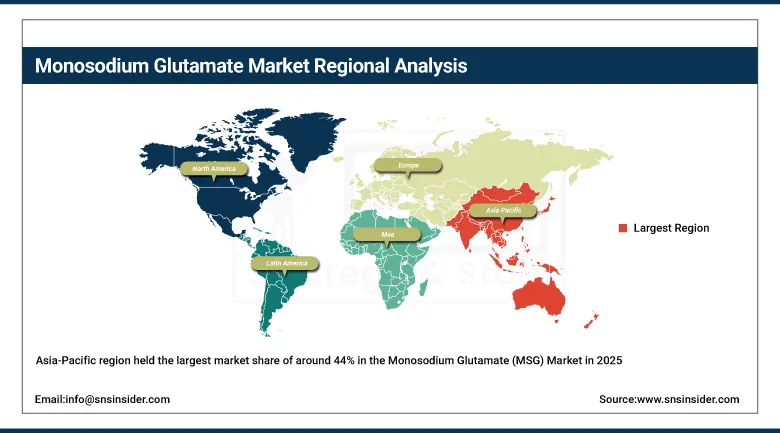

The Asia-Pacific region held the largest market share of around 44% in the Monosodium Glutamate (MSG) Market in 2025. The high consumption of processed foods, instant noodles, soups, and savory snacks among Asian nations such as China, Japan, South Korea, Indonesia, and India drives the dominance of the Asia-Pacific region. Other factors fueling the growth of the market include the presence of major players in MSG manufacturing, sufficient availability of raw materials, and growth in the food processing industry.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Monosodium Glutamate Market Insights

The North American Monosodium Glutamate Market is experiencing consistent growth owing to the growing demand for processed foods, frozen foods, snack foods, and cuisines served in restaurants. The increasing trend of eating Asian foods and umami seasonings is fueling the market growth within the U.S. and Canada. The use of MSG by food producers in their food products is rising to boost flavors while lowering sodium content in such products. The rise in the number of quick-service restaurants and online food deliveries is boosting demand. Nevertheless, clean-labeling trends are still affecting the formulations of products in regional food businesses.

Europe Monosodium Glutamate Market Insights

The growth of the Europe Monosodium Glutamate Market can be attributed to the rising demand for savory food products, ready-to-eat meals, soups, sauces, and processed snack products. The rise in the consumption of multicultural foods and the growing prevalence of Asian cuisines is driving the widespread use of MSG among the foodservice segment. Food producers are incorporating MSG into their products in order to increase the taste and consistency of their products without raising the cost of production. In countries such as Germany, France, Italy, and the UK, there has been an increase in the demand for convenient foods due to hectic lifestyles and urbanization.

Middle East & Africa and Latin America Monosodium Glutamate Market Insights

Middle East & Africa and Latin America are witnessing steady growth in the MSG market owing to increased consumption of packaged foods, seasonings, processed meat products, and ready-to-eat food items. Urbanization, improved retailing facilities, and growth in fast-food restaurants have helped boost the regional demand for MSG. Penetration of global food chains, coupled with changes in consumer food preferences, is also driving MSG usage in commercial food production operations. Notable contribution to market expansion comes from countries like Brazil, Mexico, South Africa, Saudi Arabia, and UAE. Increased investment in the food processing industry provides opportunities for growth in the coming years.

Monosodium Glutamate Market Growth Drivers:

-

Rising Demand for Processed and Convenience Foods Across Urban Populations Accelerates Monosodium Glutamate Consumption Globally

The growing consumption of packaged and processed foods is driving the demand for monosodium glutamate. Monosodium glutamate is extensively used by food processors in snacks, ready-to-eat meals, instant noodles, soups, and sauces. Urbanization and changes in lifestyle have led consumers to look for easy-to-consume and longer-lasting foods with rich flavors. The use of MSG is increasingly observed by fast-food restaurants and other food service providers to ensure consistency in the taste of their products. In addition, increasing disposable income and processed foods in emerging markets provide support to monosodium glutamate consumption on a large scale.

Monosodium Glutamate Market Restraints:

-

Stringent Food Safety Regulations and Labeling Requirements Increasing Compliance Challenges for Global Monosodium Glutamate Manufacturers and Exporters

Government regulations related to the use of additives, ingredients, and labeling processes are posing problems for MSG manufacturing companies. The regulations of government agencies of various countries involve the need to disclose the names of flavors present in food products, adding to the expense of complying with such regulations. There are differences in the amount of MSG that can be added to foods in various countries, posing additional problems for trade and exports. Food manufacturing companies have to modify their practices according to changes in regulations and consumer demands. On the other hand, health groups are exerting pressure on food manufacturers to cut down on additives.

Monosodium Glutamate Market Opportunities:

-

Rising Demand for Plant-Based Foods and Vegan Seasoning Products Creating New Application Areas for Monosodium Glutamate Manufacturers Worldwide

Growth in demand for vegetarian diets and vegan foods has presented significant growth potential for MSG producers across the world. The use of MSG has gained popularity in meat substitutes, vegan snack foods, instant soup products, and vegetarian sauce bases as an additive that increases the umami flavor in these products. Food companies have found a way to incorporate MSG in their formulation of foods with less fat content as well as plant-based foods without incurring high manufacturing costs. Increasing consumer interest in sustainable food products has driven companies to innovate in flavors. More growth potential is expected in the vegan restaurant sector and other health food segments.

Recent Developments:

-

2026: Ajinomoto Co., Inc. gained strong market attention in 2026 as investors highlighted the company’s advanced fermentation expertise used in monosodium glutamate production and semiconductor materials, strengthening its industrial growth outlook and global business diversification strategy.

-

2025: Ajinomoto Co., Inc. continued expanding global awareness campaigns in 2025 supporting the safety and sodium-reduction benefits of monosodium glutamate, promoting wider use of MSG in processed foods, restaurant applications, and low-sodium seasoning solutions worldwide.

-

2024: CJ CheilJedang Corporation strengthened its sustainable monosodium glutamate business during 2024 by promoting microbial fermentation technology under its MIPOONG brand, supporting environmentally responsible production and increasing global adoption of umami-based food ingredients.

-

2023: Ajinomoto Co., Inc. and CJ Group resolved longstanding patent litigation related to amino-acid and monosodium glutamate technologies in Germany during 2023, improving operational stability and reducing legal uncertainty across the global MSG manufacturing industry.

Key Players

Some of the Monosodium Glutamate Market Companies

-

Ajinomoto Co., Inc.

-

Fufeng Group

-

Meihua Holdings Group Co., Ltd.

-

Ningxia Eppen Biotech Co., Ltd.

-

COFCO Biochemical (Anhui) Co., Ltd.

-

Vedan International (Holdings) Limited

-

Cargill Incorporated

-

Gremount International Company Limited

-

Shandong Qilu Biotechnology Group Co., Ltd.

-

Henan Lotus Flower Gourmet Powder Co., Ltd.

-

Shandong Xinle Monosodium Glutamate Limited Company

-

Linghua Group Limited

-

Star Lake Bioscience Co., Inc.

-

CJ CheilJedang Corporation

-

Daesang Corporation

-

Foodchem International Corporation

-

Arshine Food Additives

-

Great American Spice Company

-

Prinova Group LLC

-

McCormick & Company, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.01 Billion |

| Market Size by 2035 | USD 10.44 Billion |

| CAGR | CAGR of 5.67% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Form Type(Powder, Granules) • By Application(Noodles, soups, and broths, Meat products, Seasonings & dressings, Others) • By Distribution channel (B2B,B2C[Supermarkets and hypermarkets, Convenience stores, Specialty stores, Online retail, Others]) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Ajinomoto Co., Inc., Fufeng Group, Meihua Holdings Group Co., Ltd., Ningxia Eppen Biotech Co., Ltd., COFCO Biochemical (Anhui) Co., Ltd., Vedan International (Holdings) Limited, Cargill Incorporated, Gremount International Company Limited, Shandong Qilu Biotechnology Group Co., Ltd., Henan Lotus Flower Gourmet Powder Co., Ltd., Shandong Xinle Monosodium Glutamate Limited Company, Linghua Group Limited, Star Lake Bioscience Co., Inc., CJ CheilJedang Corporation, Daesang Corporation, Foodchem International Corporation, Arshine Food Additives, Great American Spice Company, Prinova Group LLC, McCormick & Company, Inc. |

Frequently Asked Questions

Ans: Asia-Pacific dominated the Monosodium Glutamate Market in 2025.

Ans: The Powder segment dominated the Monosodium Glutamate Market in 2025.

Ans: Rising Demand for Processed and Convenience Foods Across Urban Populations Accelerates Monosodium Glutamate Consumption Globally.

Ans: The Monosodium Glutamate Market was valued at USD 6.01 billion in 2025.

Ans: The Monosodium Glutamate Market is expected to grow at a CAGR of 5.67% from 2026 to 2035.

Get in Touch