Motor Control Centers Market Report Scope & Overview:

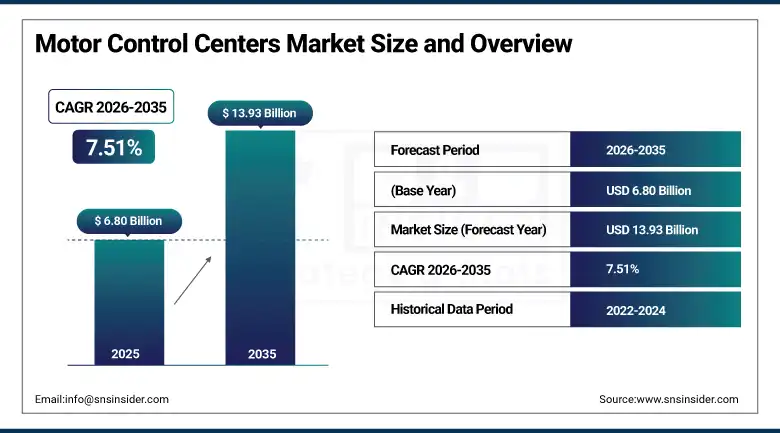

The Motor Control Centers Market size was valued at USD 6.80 Billion in 2025 and is expected to reach USD 13.93 Billion by 2035, growing at a CAGR of 7.51% from 2026–2035.

The global motor control centers market is advancing at an exceptional pace. Motor control centers are electrical distribution systems combining switchgear, motor starters, and control devices in a centralised enclosure that manages multiple motors from a single location. They are employed in manufacturing, oil and gas, utilities, mining, and water treatment facilities where multiple motors require coordinated control, protection, and monitoring. The market is experiencing significant growth driven by increased adoption of industrial automation, stringent energy efficiency regulations, and the rise of smart manufacturing.

In October 2024, Siemens launched the SIMOCODE M-CP, a compact and advanced motor management system designed for industrial switchboards specifically tailored for Motor Control Centers. It offers efficient motor control, Ethernet-based communication, and condition monitoring capability. The launch reflects the commercial direction of MCC product development toward IIoT-connected intelligent motor management whose real-time health monitoring and predictive maintenance capability reduces unplanned downtime costs that represent the primary financial motivation for intelligent MCC specification.

Market Size and Forecast

-

Market Size in 2026E: USD 7.31 Billion

-

Market Size by 2035: USD 13.93 Billion

-

CAGR: 7.51% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Motor Control Centers Market - Request Free Sample Report

Motor Control Centers Market Trends

-

Intelligent MCC adoption is increasing as Industry 4.0 initiatives require connected motor management systems. These systems provide real-time motor diagnostics, energy monitoring, and remote control capabilities for industrial operations.

-

Integration of variable frequency drives (VFDs) within MCCs is growing due to stricter energy efficiency regulations. VFD-based motor speed control helps reduce energy consumption and improve operational efficiency.

-

Modular MCC designs are gaining popularity because they simplify installation and support future capacity expansion. This flexibility reduces downtime and avoids the need for complete system replacement.

-

Data centre investments are driving demand for advanced MCC solutions to manage cooling systems, pumps, and backup power infrastructure. High reliability requirements are encouraging the adoption of intelligent MCC configurations.

-

Digital twin integration with MCC systems is enabling virtual commissioning and predictive maintenance capabilities. These technologies help optimize motor performance and lower lifecycle operating costs.

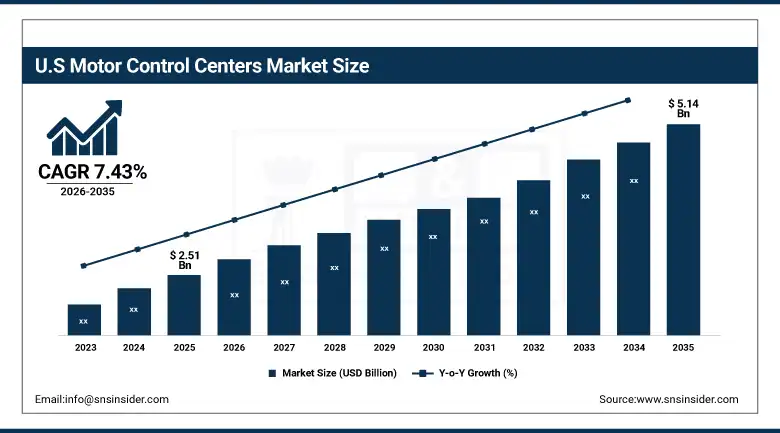

U.S. Motor Control Centers Market Size Outlook:

The U.S. Motor Control Centers Market was valued at approximately USD 2.51 Billion in 2025 and is expected to reach approximately USD 5.14 Billion by 2035, growing at a CAGR of approximately 7.43%. The U.S. is a significant motor control center market anchored by oil and gas processing, manufacturing, water utilities, and the rapidly growing data centre sector. Manufacturing contributed USD 2.3 trillion to U.S. GDP in 2023, creating substantial motor control procurement across production facility automation. The Bipartisan Infrastructure Law allocated USD 62 billion to DOE programmes modernising energy infrastructure whose grid investment creates utility sector MCC procurement. Rockwell Automation, Eaton, and ABB's U.S. operations define the domestic MCC market's commercial and technology standard whose intelligent MCC product leadership sustains above-average per-unit commercial value relative to commodity alternatives.

In April 2024, Rockwell Automation presented its new generation low voltage MCC called FLEXLINE 3500 at Hannover Messe, featuring modular design with Ethernet connectivity and integrated energy monitoring. The system enables operators to add, remove, or modify motor control units without interrupting power to the rest of the MCC, directly addressing the operational continuity requirement that prevents maintenance-window-dependent MCC modifications in continuous process industries.

Motor Control Centers Market Segment Analysis

-

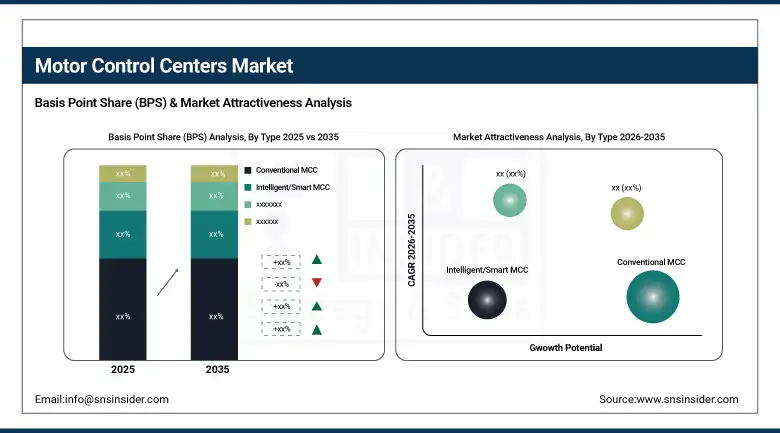

By Type, the Smart Motor/Conventional MCC segment dominated the Motor Control Centers Market with approximately 66% Smart Motor share in 2025, while the Intelligent/Smart MCC segment is the fastest growing with a CAGR of approximately 10.5%.

-

By Voltage, the Low Voltage segment dominated the Motor Control Centers Market with approximately 65% share in 2025, while the Medium Voltage segment is the fastest growing with a CAGR of approximately 9.2%.

-

By Component, the Motor Starters segment dominated the Motor Control Centers Market in 2025, while the Variable Frequency Drives segment is the fastest growing.

-

By End User, the Oil & Gas segment dominated the Motor Control Centers Market in 2025, while the Manufacturing segment is the fastest growing with a CAGR of approximately 9.8%.

By Type, smart motor dominates, intelligent MCC grows fastest

Smart motor and conventional MCC retained the dominant type position with approximately 66% of the motor control center market in 2025. The installed base of conventional MCCs across the global industrial sector creates replacement and upgrade procurement that sustains conventional MCC commercial leadership despite the intelligent MCC segment's faster growth rate. Each existing conventional MCC that reaches end of operational life creates a procurement decision whose replacement opportunity is contested between conventional replacement and intelligent upgrade.

Intelligent and smart MCCs are the fastest-growing type at approximately 10.5% CAGR because Industry 4.0's systematic deployment of IIoT monitoring infrastructure across industrial operations is creating structured demand for MCCs capable of integrating with plant-wide digital systems. Each new greenfield smart factory and each intelligent MCC upgrade in existing facilities creates a precedent whose operational benefit documentation sustains subsequent intelligent MCC specification decisions.

By Voltage, low voltage dominates, medium voltage grows fastest

Low voltage MCCs retained the dominant voltage position with approximately 65% of the motor control center market in 2025. LV MCCs serving motors below 1 kV encompass the broadest range of industrial, commercial, and utility applications whose aggregate motor count and procurement volume substantially exceeds medium voltage alternatives. Manufacturing plants, commercial building HVAC systems, water treatment facilities, and data centre cooling infrastructure all deploy LV MCCs whose collective commercial scale defines the market's majority revenue. Each new manufacturing facility or commercial building installation creates LV MCC procurement that compounds with global industrial and commercial construction investment.

Medium voltage MCCs are the fastest-growing segment at approximately 9.2% CAGR because heavy industrial applications in oil and gas production, mining operations, large-scale water pumping, and petrochemical processing require the high-power motor control that MV MCCs provide at 2.4-15 kV voltage levels. Each new offshore oil platform, mine dewatering system, or large-scale water transfer pumping station creates MV MCC procurement whose per-installation commercial value substantially exceeds LV alternatives. The energy sector's capital investment in high-power process infrastructure is creating the most commercially premium MCC procurement growth of any application category.

By Component, motor starters dominate, VFDs grow fastest

Motor starters retained the dominant component position in the motor control center market in 2025. Motor starters are the fundamental control element present in every MCC regardless of voltage, application, or intelligence level. Each MCC installation requires motor starter units for every controlled motor circuit whose aggregate count across large industrial MCCs can number in the hundreds. The universal requirement creates commercial demand that compounds directly with MCC installation volume growth. Direct-on-line starters, soft starters, and star-delta starters collectively define the motor starter category whose product range serves the full spectrum of motor control applications from simple switching to controlled acceleration.

Variable frequency drives are the fastest-growing component because energy efficiency regulations in the EU, U.S. DOE, and Asian markets are creating systematic requirements for VFD-based motor speed control that eliminates the energy waste of throttle-valve flow control in pump and fan applications. The EU's Ecodesign Regulation for motor systems and the U.S. DOE's energy efficiency standards collectively create compliance-driven VFD procurement that is mandatory rather than discretionary in regulated motor applications. Each pump, fan, and compressor application that transitions from fixed-speed to VFD-controlled creates energy savings of 20-50% whose economic return justifies VFD investment with payback periods under three years.

By End User, oil & gas dominates, manufacturing grows fastest

Oil and gas retained the dominant end user position in the motor control center market in 2025. Upstream, midstream, and downstream oil and gas operations deploy the highest motor density of any industrial sector, with offshore platforms, refineries, and pipeline pumping stations each requiring dozens to hundreds of motor circuits whose centralised control through MCC infrastructure is operationally essential. The operational continuity requirement in hazardous area classified environments creates premium specification for explosion-proof, corrosion-resistant MCC enclosures whose specialised manufacturing commands above-average pricing that sustains oil and gas's commercial revenue dominance despite manufacturing's higher motor count.

Manufacturing is the fastest-growing end user at approximately 9.8% CAGR because smart factory investment is creating systematic MCC upgrade and new installation procurement across automotive, food and beverage, pharmaceutical, and electronics production whose Industry 4.0 transformation creates intelligent MCC demand that conventional factory automation did not generate. Each new EV manufacturing plant, semiconductor fab, and pharmaceutical GMP facility creates MCC procurement whose intelligent specification requirement sustains above-average per-installation commercial value that compounds with manufacturing sector investment growth.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

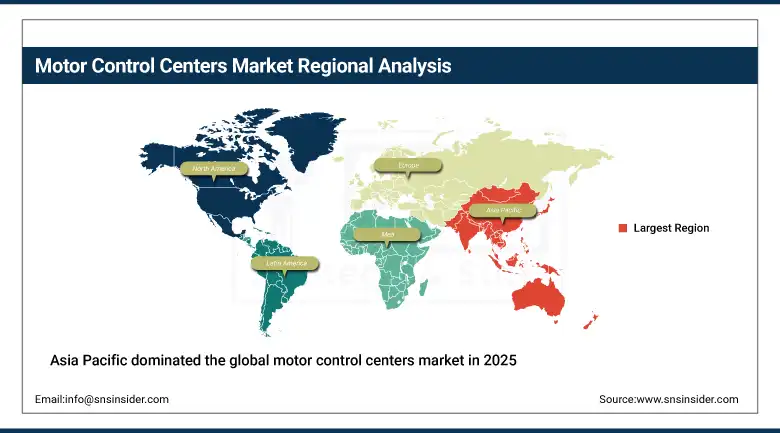

Asia Pacific Motor Control Centers Market Insights

Asia Pacific dominated the global motor control centers market in 2025, holding a share of over 35.3%. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary manufacturing sector's motor control investment, the power utility sector's electrical infrastructure, and the oil and gas processing industry's process automation. Rapid industrialisation across India, Vietnam, Indonesia, and Thailand is creating above-average first-time MCC installation demand whose greenfield opportunity represents the fastest-growing new procurement pool in the global market.

Japan and South Korea represent technically sophisticated secondary markets whose manufacturing automation, utilities sector, and semiconductor facility MCC procurement create consistent intelligent MCC demand at above-average per-unit commercial value. Mitsubishi Electric and Fuji Electric's Japanese operations contribute both domestic market leadership and export-oriented product development whose global competitive position sustains Asia Pacific's MCC manufacturing leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Motor Control Centers Market Insights

North America is the fastest-growing regional motor control centers market, driven by U.S. infrastructure investment under the Bipartisan Infrastructure Law, onshoring manufacturing investment, and the rapidly expanding data centre sector's motor control requirements. The United States accounts for approximately 87.4% of North American revenues through Rockwell Automation, Eaton, and ABB's commercial dominance whose combined product portfolio defines the North American intelligent MCC standard.

Canada contributes approximately 12.6% of North American revenues through its oil sands and mining industries' MCC procurement, utilities sector investment, and the manufacturing sector's progressive automation whose combined demand creates consistent commercial engagement with major MCC suppliers.

Europe Motor Control Centers Market Insights

Europe is a technically sophisticated MCC market where EU energy efficiency directives, Industry 4.0 adoption across German and Nordic manufacturing, and the utilities sector's grid modernisation investment create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through Siemens' domestic market leadership, the automotive manufacturing sector's production automation, and the chemical industry's process control investment.

The United Kingdom, France, and Sweden are significant secondary markets where manufacturing automation, utility sector modernisation, and pharmaceutical production create consistent intelligent MCC procurement. ABB's Swiss headquarters and Schneider Electric's French operations sustain European MCC supply from established regional manufacturing presences.

MEA & Latin America Motor Control Centers Market Insights

The Middle East and Africa and Latin America are growing MCC markets where oil and gas infrastructure investment, industrial development, and utility sector modernisation create structured demand. Saudi Arabia leads MEA revenues at approximately 31.2% through ARAMCO's refinery and oil production facility MCC investment, SABIC's petrochemical plant control infrastructure, and Vision 2030's industrial development programme creating new manufacturing facility MCC procurement.

Brazil leads Latin American revenues at approximately 44.2% through its oil and gas sector's Petrobras offshore platform MCC, the manufacturing sector's production automation, and the utilities sector's water treatment and power distribution investment.

Market Dynamics

Growth Drivers: Industrial automation investment and energy efficiency mandates driving VFD-integrated intelligent MCC adoption

Industrial automation investment is the motor control centers market's most commercially certain growth driver. Each new automated production facility, mining operation expansion, or process plant upgrade creates MCC procurement whose intelligence specification is progressively migrating toward intelligent systems as the economic case for IIoT connectivity's operational benefit becomes commercially documented. The COVID-19 pandemic's acceleration of manufacturing automation investment, visible in robot installation records from 2021-2023, creates proportional MCC demand whose intelligent specification compound with automation investment growth.

Energy efficiency regulation is creating systematic VFD-integrated MCC procurement that is compliance-driven rather than discretionary. The EU's Ecodesign Regulation requirement for IE3 motor efficiency standards and VFD use in variable torque pump and fan applications creates mandatory MCC upgrade investment whose timeline and commercial scale are defined by regulatory implementation schedules. Each percentage point increase in industrial motor energy efficiency standard creates proportional VFD and intelligent MCC procurement that compounds with the global industrial motor installation base's scale.

Restraints: High initial capital cost of intelligent MCC systems and installation complexity in hazardous environments

Intelligent MCC systems command 30-50% pricing premium over conventional alternatives whose capital cost differential creates procurement resistance in cost-sensitive industrial environments where payback period analysis must demonstrate energy savings or downtime reduction ROI within acceptable investment timeframes. Large industrial facilities whose motor count creates substantial intelligent MCC investment requirements must justify the premium against demonstrable operational benefit whose documentation requires reference site performance data that new technology deployments initially lack.

Hazardous area MCC installation in oil and gas, chemical, and mining environments requires explosion-proof enclosure design, certified component specification, and installation engineering whose complexity adds cost and timeline to MCC projects. Each zone classification change or process expansion in hazardous environments requires regulatory re-certification that creates implementation barriers limiting the pace of intelligent MCC upgrade adoption in safety-critical installations.

Opportunities: Data centre MCC market expansion and emerging market industrial development

Data centre MCC expansion represents a rapidly growing commercial opportunity whose scale compounds with hyperscale facility construction investment. Each new data centre campus's cooling infrastructure, UPS systems, and electrical distribution require intelligent MCC systems whose critical facility reliability requirements justify premium intelligent specification. The AI infrastructure investment wave's extraordinary data centre construction pace is creating above-average data centre MCC procurement growth that sustains the market's overall above-average CAGR.

Emerging market industrial development in India, Southeast Asia, and Africa is creating first-time MCC installation demand whose greenfield opportunity allows modern intelligent MCC specification without the retrofit complexity that existing industrial facilities impose. Each new industrial zone development, manufacturing facility, or utility infrastructure project in emerging markets creates MCC procurement that represents net addition to the global market rather than replacement of existing capacity.

Recent Developments:

-

2024: Siemens launched the SIMOCODE M-CP motor management system in October 2024, designed specifically for Motor Control Centers with Ethernet-based communication, condition monitoring, and compact integration for industrial switchboards.

-

2024: Rockwell Automation presented the FLEXLINE 3500 low voltage MCC in April 2024 at Hannover Messe, featuring modular hot-swap design with Ethernet connectivity and integrated energy monitoring enabling MCC unit replacement without power interruption.

-

2024: In November 2024, Fuji Electric launched the MICREX-SX Series SPH3300/2200 programmable controllers with 6.5x higher control speed and enhanced logging functions aimed at improving productivity and digital transformation on manufacturing shop floors integrated with MCC systems.

Motor Control Centers Companies are:

-

ABB Ltd.

-

Siemens AG

-

Rockwell Automation Inc.

-

Schneider Electric

-

Mitsubishi Electric Corporation

-

General Electric

-

Fuji Electric Co., Ltd.

-

Legrand S.A.

-

Larsen & Toubro

-

Powell Industries Inc.

-

WEG S.A.

-

Leroy-Somer (Nidec)

-

CHINT Group

-

Havells India

-

Bosch Rexroth

-

Danfoss A/S

-

Yaskawa Electric

-

Emerson Electric Co.

Motor Control Centers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.80 Billion |

| Market Size by 2035 | USD 13.93 Billion |

| CAGR | CAGR of 7.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Conventional MCC, Intelligent/Smart MCC) • by Voltage (Low Voltage, Medium Voltage, High Voltage) • by Component (Motor Starters, Variable Frequency Drives, PLCs, Switchgear, Others) • by End User (Oil & Gas, Manufacturing, Mining, Water & Wastewater, Utilities, Data Centres, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ABB Ltd., Siemens AG, Eaton Corporation, Rockwell Automation Inc., Schneider Electric, Mitsubishi Electric Corporation, General Electric, Fuji Electric Co., Ltd., Legrand S.A., Nidec Corporation, Larsen & Toubro, Powell Industries Inc., WEG S.A., Leroy-Somer (Nidec), CHINT Group, Havells India, Bosch Rexroth, Danfoss A/S, Yaskawa Electric, Emerson Electric Co. |

Frequently Asked Questions

The Motor Control Centers Market is expected to grow at a CAGR of 7.51% from 2026 to 2035.

The Motor Control Centers Market was valued at USD 6.80 Billion in 2025.

Industrial automation investment creating systematic MCC procurement across new smart factory installations and energy efficiency regulatory mandates driving VFD-integrated intelligent MCC adoption that replaces conventional fixed-speed motor control systems.

Smart Motor/Conventional MCC dominated with approximately 66% share in 2025, while Intelligent/Smart MCC is the fastest growing with a CAGR of approximately 10.5%.

Asia Pacific dominated the Motor Control Centers Market in 2025 with over 35.3% market share, while North America is the fastest-growing region.

Get in Touch