Mulch Film Market Report Scope and Overview:

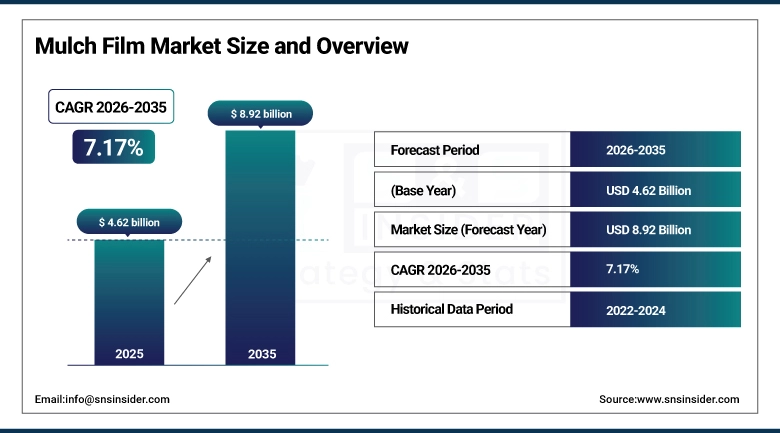

The Mulch Film Market was valued at USD 4.62 billion in 2025 and is expected to reach USD 8.92 billion by 2035, growing at a CAGR of 7.17% from 2026-2035.

The mulch film market is witnessing an enormous growth within due to the growing awareness concerning sustainable agriculture and enhancing agricultural productivity on a global level. Mulch films are widely applied within commercial agriculture, horticulture, greenhouse farming, as well as fruits and vegetables planting in order to improve soil heat management, conserve moisture, eliminate weeds' emergence, and enhance fertilizers use. An increased demand for advanced agricultural technologies that can improve the performance of farms is associated with increased pressure concerning agricultural productivity due to the fast-growing population and the lack of available farmland.

There are various governmental incentives promoting mulch films' use in the form of agricultural modernization projects, water saving projects, and even sustainable farming subsidies. Growing concerns over soil degradation, water shortage, and climate change are stimulating the demand for more efficient irrigation systems and protection for crops. Finally, mulch films' growing popularity in the industry is related to a shift towards recyclable mulch films due to increasingly stringent regulations within the agricultural plastic waste management industry.

Mulch Film Market Size and Forecast

-

Market Size in 2025: USD 4.62 Billion

-

Market Size by 2035: USD 8.92 Billion

-

CAGR: 7.17% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Mulch Film Market - Request Free Sample Report

Mulch Film Market Trends

-

Growing application of biodegradable mulch films due to environmental sustainability trends.

-

Growing application of precision farming along with drip irrigation and mulch film technology.

-

Growing need for UV-resistant and multi-layered agricultural films.

-

Increasing trend of growing vegetables under the greenhouses around the globe.

-

Growing application of photo-selective and colored mulch films.

-

Growing governmental assistance for water conservation and sustainable agriculture practices.

-

Growing developments in recycle polymers and bio-degradable agricultural films.

-

Growing trend of using less pesticides and herbicides owing to mulch film applications.

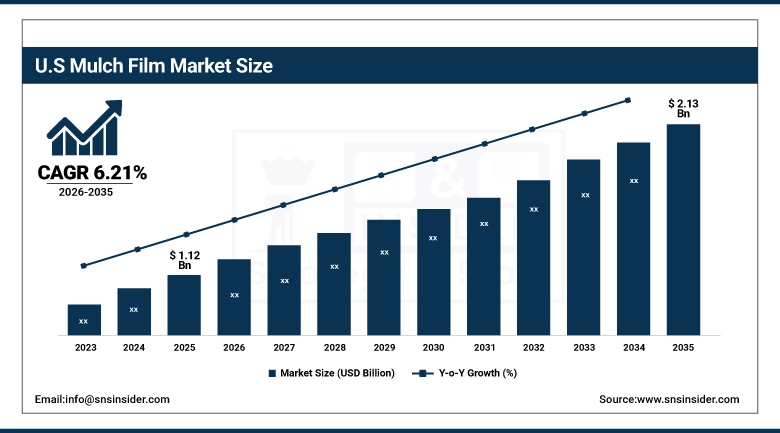

U.S. Mulch Film Market was valued at USD 1.12 billion in 2025 and is expected to reach USD 2.13 billion by 2035, growing at a CAGR of 6.21%.

The US continues to be among the key consumers of mulch films owing to high adoption of modern farming equipment and methods such as precision agriculture and irrigation techniques. In the US, farmers are increasingly applying mulch films in the production of vegetables, in greenhouses, horticulture, and fruit growing as a means of improving agricultural output and conserving water.

Growing interest in organic farming and eco-friendly agricultural practices is helping propel market growth. Favorable government policies towards soil management, water conservation, and environment-friendly agricultural products are further driving the adoption of biodegradable and recyclable mulch films. Growth in greenhouse farming in states like California, Texas, and Florida is playing a vital role in market growth.

Mulch Film Market Segment Analysis

-

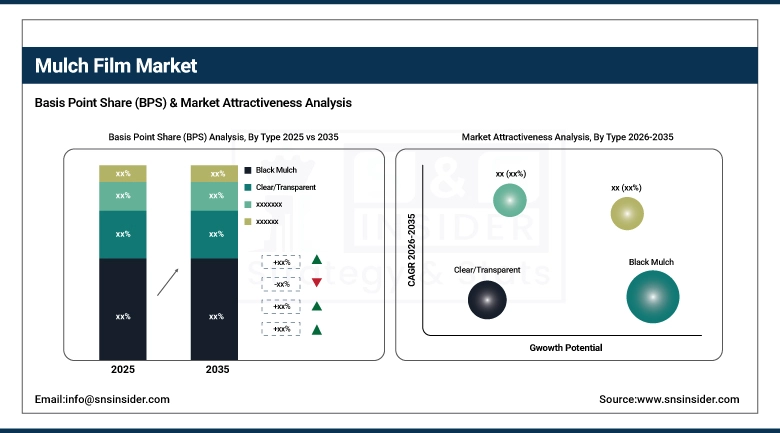

Based on Type, Black Mulch Films dominated the market in 2025 with approximately 52.1% revenue share.

-

Based on Raw Material, Conventional Polyethylene Films accounted for nearly 69.2% market share in 2025.

-

Based on Application, Agricultural farms dominated the market with around 76.2% revenue share.

By Type, Black Mulch Films dominated while Biodegradable Films expected to grow fastest.

The black mulch films dominated the market, owing to its effectiveness in weed management, water conservation, and soil temperature management. The black mulch films are widely adopted in vegetables growing and horticulture due to the efficiency and economic viability.

The biodegradable mulch films are expected to show highest CAGR, mainly driven by increasing environmental issues with respect to plastic used in agriculture. With the increasing government guidelines towards sustainability, farmers are encouraged to use sustainable products.

By Raw Material Conventional Polyethylene Films accounted for Largest Share

The conventional mulch films held the majority share in the mulch film market, which was 69.2%, in 2025. It is the use of low-density polyethylene (LDPE) films that constitutes the main driving force behind such figures. The preference for LDPE films stems from their resilience, cost efficiency, and superior ability to manage weed growth, soil moisture, and regulate soil temperatures. LDPE films are popular due to their flexibility and easy applicability, especially when it comes to large-scale agricultural activities. In this case, it is worth mentioning the work conducted by the National Agricultural Plastics Recycling Program in the USA, which acknowledges the extensive usage of polyethylene films in agriculture. Although biodegradable mulch films become increasingly more popular in some regions due to environmental reasons, the low price and reliability of conventional films ensure their domination, especially considering the widespread popularity of LDPE. According to the American Chemistry Council, about 60% of all agricultural plastic waste in the USA comprises polyethylene films.

By Application, High School Segment Dominates STEM Education Market, Middle School Segment Shows Fastest Growth

The market was dominated by agricultural farms in 2025 with a market share of ~76%. Agricultural farms represent the biggest end-users of mulch films due to the vast amount of land used in farming and the high degree of activity of operations on those lands. The application of mulch films by these players is mostly seen when trying to maximize yield in terms of row crops such as cotton, maize, soybean, and vegetables. There have been numerous instances where the United States Department of Agriculture (USDA) included mulch films in their programs under initiatives like Environmental Quality Incentives Programs (EQIP). The purpose of doing this is to help farmers preserve water in arid zones, such as in Arizona and California, by helping to decrease labor costs due to weed removal, increase efficiency of nutrition and water, and extend the planting season. Numerous research papers from institutions like Texas A&M University and Purdue University have highlighted the benefits of applying mulch films on farms through cases where farmers have had increased yield and saved water.

Mulch Film Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~81% |

|

Europe |

United Kingdom |

~26% |

|

Asia Pacific |

China |

~44% |

|

Middle East and Africa |

UAE |

~34% |

|

Latin America |

Brazil |

~52% |

North America Mulch Film Market Insights

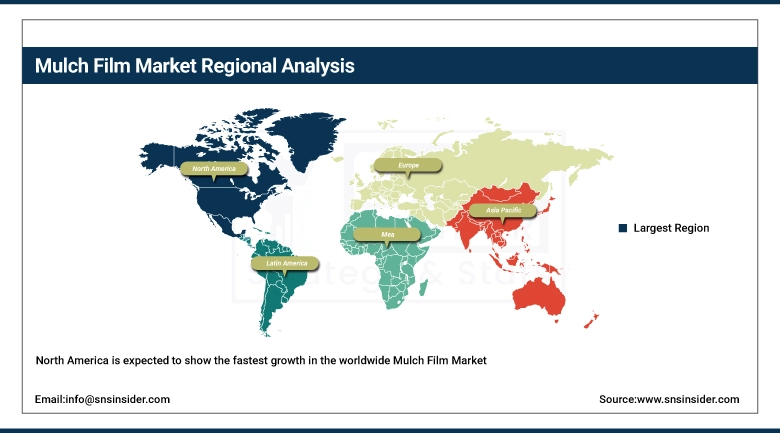

North America is expected to show the fastest growth in the worldwide Mulch Film Market during the forecast period owing to the increasing use of precision agriculture, rising need for sustainable agricultural solutions, and growing usage of biodegradable mulch films in the USA and Canada. In the region, farmers are increasingly using mulch films as it helps them conserve water, reduce their dependence on herbicides, manage soil temperatures better, and boost crop production from valuable fruit and vegetable crops. Growing trends in greenhouse farming and organic farming along with initiatives for climate smart farming are rapidly increasing the demand in the region. Rising trend towards environmentally safe products in the form of biodegradable and recyclable agricultural films is adding momentum to the market growth. Investment in mechanized farming and improved irrigation infrastructure continues to provide excellent future prospects to mulch film companies in North America.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Mulch Film Market Insights

The Asia-Pacific region held the maximum share of the global Mulch Films Market in 2025 owing to its extensive usage in agriculture, use of plasticulture techniques, and growing preference for higher yields across nations such as China, India, Japan, and Southeast Asia. The leading position is held by the Chinese market owing to the increasing application of mulch films in horticulture, protected crop cultivation, and efficient water management techniques. India too is experiencing a steady increase in demand on account of increased investment in drip irrigation techniques and protected cultivation systems. The growing need to boost agricultural output, coupled with food safety issues and rising population levels, has led to the increasing use of mulch films in horticultural and commercial farming.

Europe Mulch Film Market Insights

Europe is an important region in the Global Mulch Films Market because of the growth in sustainable agriculture techniques, development of greenhouse cultivation, and the emphasis laid by governments in Germany, the UK, France, Italy, and Spain on the use of eco-friendly inputs in agriculture. There is growing usage of bio-degradable mulch films among European farmers owing to the regulations imposed by governments on the use of plastics in agriculture. Europe is a major market for advanced mulch films on account of its growing horticultural sector and use of protective cultivation methods. Initiatives for sustainability from the EU along with advancements in precision agriculture technology have led to more recycling and bio-based agriculture films.

Latin America Mulch Film Market Insights

The Mulch Film Market in Latin America is experiencing consistent growth driven by increased commercial farming operations, growing exports of fruits and vegetables, and the widespread use of protected cultivation practices in Brazil, Mexico, Argentina, and Chile. Increasing applications of mulch films are being made by farmers for improving the quality of produce, enhancing irrigation efficiency, and lowering weed management expenses. Brazil continues to lead as the key market in the region owing to its significant presence of agricultural production and emphasis on advanced farming techniques. The growing importance of greenhouse farming, export-oriented horticulture, and water conservation practices is driving the demand for the region’s mulch films market.

Middle East & Africa Mulch Film Market Insights

The Middle East and Africa region is witnessing the rise in the Mulch Film Market due to rising investments in efficient agriculture, growing greenhouses, and food security measures in the UAE, Saudi Arabia, South Africa, and Egypt. Mulch films are being used widely by countries in the region for better soil moisture retention and cultivation of crops amid arid climates. The countries including Saudi Arabia and the UAE are at the forefront of adopting mulch films via government-driven greenhouse cultivation and sustainable agriculture initiatives. An increasing emphasis on reducing water usage, enhancing productivity, and developing agriculture in controlled environments is contributing positively to the growth in the market. The adoption of modernized irrigation methods is set to drive the growth of mulch films in the region.Bottom of Form

Market Growth Drivers:

-

Rising adoption of protected agriculture and water-efficient farming practices

The need for increased agricultural efficiency, proper water management, and superior crop quality is becoming one of the major factors responsible for the growing popularity of agricultural mulch films among farmers around the world. Agricultural mulch films are highly useful for managing soil moisture, soil temperature, weed control, and ensuring consistent crop production, and their importance cannot be overstated when growing fruits, vegetables, and ornamental plants. Increasing food chain pressures owing to expanding populations and decreasing availability of cultivable land are prompting farmers to resort to the use of advanced plasticulture techniques. The growth of greenhouse farms, irrigation facilities, and precision agriculture practices in the Asia-Pacific, North America, and Europe regions is boosting market demand.

Market Restraints:

-

Environmental concerns regarding plastic waste and disposal challenges

Traditional mulch films made from polyethylene are environmentally harmful as far as soil pollution, accumulation of plastic waste, and agricultural waste management are concerned. The improper disposal and recycling of agricultural films is one of the biggest obstacles facing several developing countries owing to the lack of waste management facilities. Moreover, rising regulation on single-use plastics and increasing environmental consciousness amongst consumers and governments are hindering the usage of non-degradable mulch films. Besides, the higher prices associated with biodegradable films vis-a-vis regular plastic mulch films are posing obstacles to its widespread adoption.

Market Opportunities:

-

Growing development of biodegradable and bio-based mulch film technologies

Growing focus on sustainable farming techniques and circular economy models is leading to many business opportunities in the development of biodegradable and compostable mulch film products. Producers are now focusing their efforts on developing bio-based polymers and environmentally safe agricultural films that degrade naturally without causing any harmful chemicals to remain in the soil. New developments in the area of durability, UV protection, and moisture management capabilities of biodegradable mulch films are resulting in higher commercial success rates in greenhouse farming and high-yield crops production. Growth prospects in the biodegradable mulch film market are likely to be bolstered by the growing support from governments for sustainable agricultural technology.

Recent Developments:

-

2026: BASF introduced a new range of biodegradable films for agriculture through innovative soil degradable mulch films that would help conserve water and minimize plastic waste post-harvesting in commercial farms.

-

2025: Berry Global launched sustainable mulch films with recycled polymer technology and improved UV protection for precision agriculture and greenhouse farming around the world.

Mulch Film Market Key Players

Some of the Mulch Film Market Companies

• AB Rani Plast OY

• Al-Pack Enterprises Ltd.

• Armando Alvarez Group

• BASF SE

• Berry Global Inc.

• BioBag International AS

• Coveris

• Dubois Agrinovation Inc.

• Group Barbier

• Iris Polymers Industries Private Limited

• Kingfa Sci & Tech Co Ltd

• Kuraray Europe GmbH

• Novamont S.p.A.

• Napco National

• Plastika Kritis S.A.

• Polystar Plastics Ltd

• RKW SE

• Shalimar Group

• Tilak Polypack

• Yibiyuan Water-Saving Equipment Technology Co., Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.62 Billion |

| Market Size by 2035 | USD 8.92 Billion |

| CAGR | CAGR of 7.17% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Clear/Transparent, Black Mulch, Colored Mulch, Photoselective Mulch, Degradable Mulch) • By Raw Material (Conventional, Biodegradable) • By Application (Agricultural Farms, Horticulture) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AB Rani Plast OY, Al-Pack Enterprises Ltd., Armando Alvarez Group, BASF SE, Berry Global Inc., BioBag International AS, Coveris, Dubois Agrinovation Inc., Group Barbier, Iris Polymers Industries Private Limited, Kingfa Sci & Tech Co Ltd, Kuraray Europe GmbH, Novamont S.p.A., Napco National, Plastika Kritis S.A., Polystar Plastics Ltd, RKW SE, Shalimar Group, Tilak Polypack, and Yibiyuan Water-Saving Equipment Technology Co., Ltd. |

Frequently Asked Questions

Ans: North America is expected to grow at the fastest CAGR of 6.4% in the Mulch Film Market.

Ans: Agricultural farms dominated with approximately 76.8% share in 2025.

Ans: Black Mulch Films held approximately 52.1% share in 2025.

Ans: The Mulch Film Market was valued at USD 4.62 Billion in 2025.

Ans: The Mulch Film Market is expected to grow at a CAGR of 7.17% from 2026 to 2035.

Get in Touch