Sulfuric Acid Market Report Scope & Overview:

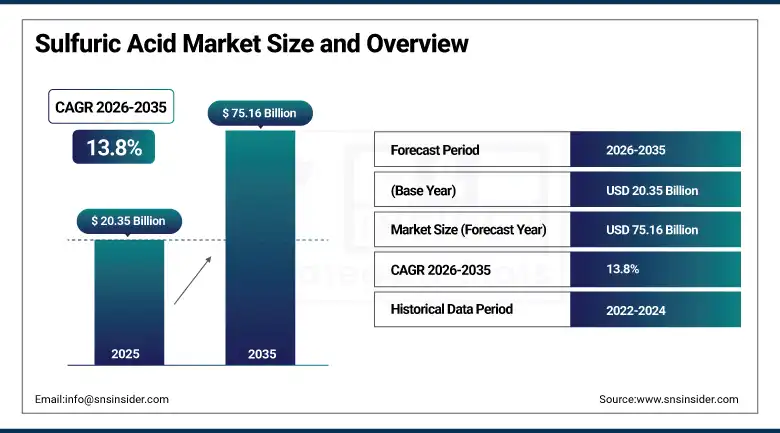

The Sulfuric Acid Market was valued at USD 20.35 Billion in 2025 and is expected to reach USD 75.16 Billion by 2035, growing at a CAGR of 13.8% from 2026–2035.

The global sulfuric acid market is growing at an exceptional pace. Sulfuric acid is the world’s most widely produced industrial chemical, often called the “king of chemicals” due to its foundational role across fertilisers, chemical manufacturing, metal processing, petroleum refining, and battery production. Fertiliser production consumes over 55% of global sulfuric acid output, creating direct commercial linkage to global food security investment and agricultural productivity programmes. The electric vehicle battery sector is creating a new high-growth demand category through lithium-ion battery manufacturing processes and next-generation battery chemistries. Growing population, expanding agricultural activity, and industrialisation in Asia Pacific and Africa are sustaining above-average demand growth across the forecast period.

In 2023, LG Chem expanded its sulfuric acid production capabilities with a focus on oleum production, targeting the increasing demand from the semiconductor electronics industry and EV battery manufacturing sectors. The expansion reflects the commercial diversification of sulfuric acid end-use demand beyond its traditional fertiliser and chemical manufacturing base into the high-growth battery and semiconductor industries whose per-unit acid consumption creates premium demand segments with above-average growth trajectories.

Market Size and Forecast

-

Market Size in 2026E: USD 23.16 Billion

-

Market Size by 2035: USD 75.16 Billion

-

CAGR: 13.8% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Sulfuric Acid Market - Request Free Sample Report

Sulfuric Acid Market Trends

-

EV battery manufacturing is creating a new above-average demand segment for high-purity sulfuric acid in lithium battery electrolyte preparation and battery recycling acid recovery processes whose combined procurement is growing proportionally with global EV production volume.

-

Electronic-grade sulfuric acid demand from semiconductor wafer cleaning and etching applications is growing rapidly with global semiconductor capacity expansion investment that is creating premium quality specification procurement beyond standard industrial acid grades.

-

Phosphate fertiliser production capacity expansion across Africa and Asia Pacific is creating growing sulfuric acid demand as new DAP and MAP facilities commission at scales requiring dedicated sulfuric acid supply infrastructure.

-

Sulfuric acid recovery and recycling from spent acid streams in metal processing, petroleum refining, and chemical manufacturing is improving industrial sustainability credentials while creating circular supply chains that partially offset primary production growth.

-

Wet sulfuric acid process technology development is enabling waste gas sulfur dioxide streams from smelters and refineries to be converted to commercial-grade sulfuric acid, improving facility economics and reducing SO2 emissions simultaneously.

U.S. Sulfuric Acid Market Outlook

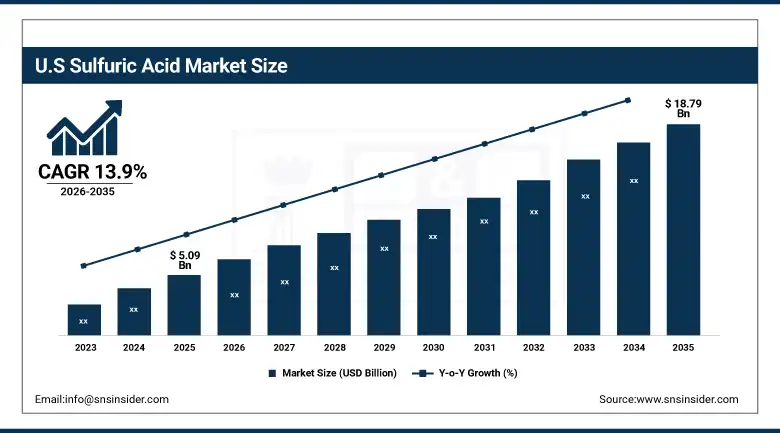

The U.S. Sulfuric Acid Market was valued at approximately USD 5.09 Billion in 2025 and is expected to reach approximately USD 18.79 Billion by 2035, growing at a CAGR of approximately 13.9%.

The U.S. is a significant sulfuric acid market whose demand is anchored by the phosphate fertiliser industry concentrated in Florida and Idaho, the petroleum refining sector’s alkylation acid requirements, and the mining industry’s heap leach copper extraction processes. PVS Chemicals and Chemtrade Logistics serve the domestic merchant market while Mosaic, Agrium, and integrated fertiliser producers consume captive production. The semiconductor industry’s domestic capacity expansion under the CHIPS Act is creating growing electronic-grade sulfuric acid demand whose purity specification requirements create premium procurement opportunities for specialised acid producers.

DuPont, in partnership with several companies, developed an advanced sulfuric acid catalyst technology in 2022 to improve the efficiency of sulfuric acid production and reduce emissions in the refining and petrochemical industries. The technology strengthens DuPont’s position in sulfuric acid-based catalyst systems and reflects the growing commercial investment in contact process efficiency improvement that reduces energy consumption and SO2 tail gas emissions per tonne of acid produced.

Sulfuric Acid Market Segment Analysis

-

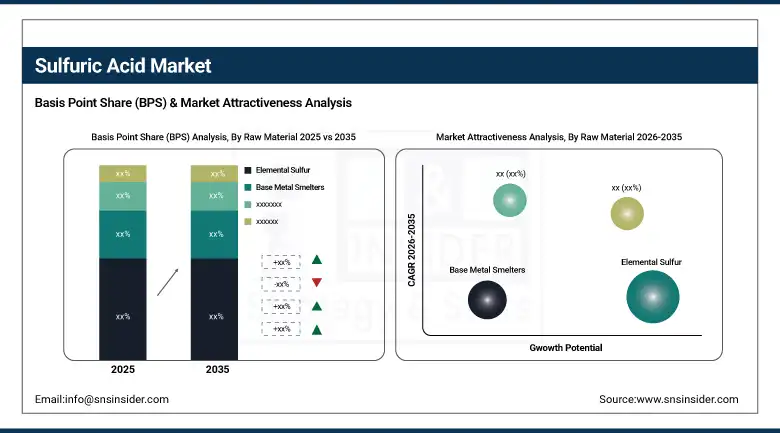

By Raw Material, the Elemental Sulfur segment dominated the Sulfuric Acid Market with approximately 52% share in 2025, while the Base Metal Smelters segment is the fastest growing.

-

By Application, the Fertilizers segment dominated the Sulfuric Acid Market with approximately 55% share in 2025, while the Battery/EV segment is the fastest growing.

-

By Concentration, the Concentrated Sulfuric Acid segment dominated the Sulfuric Acid Market in 2025, while the Oleum/Fuming Sulfuric Acid segment is the fastest growing.

-

By End User Industry, the Agriculture segment dominated the Sulfuric Acid Market in 2025, while the Electronics & Semiconductor segment is the fastest growing.

By Raw Material, elemental sulfur dominates, base metal smelters grow fastest

Elemental sulfur retained the dominant raw material position with approximately 52% of the sulfuric acid market in 2025. Its commercial primacy reflects the economics of the contact process, where elemental sulfur’s high sulfur content, consistent purity, and global supply availability from hydrocarbon processing desulfurisation create the most commercially efficient feedstock for large-scale sulfuric acid production. Petroleum refineries and natural gas processing plants generate elemental sulfur as a mandatory by-product of hydrocarbon desulfurisation whose continued production creates a structurally available feedstock supply that sustains elemental sulfur’s dominant position independently of mining sulfur demand cycles.

Base metal smelters are the fastest-growing raw material source because the global copper, zinc, and nickel mining sector’s capacity expansion in Chile, Peru, the Democratic Republic of Congo, and Indonesia is generating growing by-product sulfur dioxide streams whose conversion to commercial sulfuric acid through on-site wet sulfuric acid process plants creates both environmental compliance and commercial revenue for mine operators. Each new major copper smelter commissioned creates a defined sulfuric acid production capacity addition whose commercial output serves domestic fertiliser and chemical markets in proximity to the smelting region.

By Application, fertilizers dominate, battery/EV grows fastest

Fertilisers retained the dominant application position with approximately 55% of the sulfuric acid market in 2025. Sulfuric acid’s foundational role in phosphoric acid production for DAP, MAP, and superphosphate fertilisers creates a commercial linkage between agricultural productivity investment and acid demand that is structurally stable across commodity price cycles. The global population’s continued growth toward 10 billion by 2050 creates sustained food production requirement whose fertiliser input demand sustains sulfuric acid procurement independent of individual crop price cycles. Africa’s agricultural development programmes and Asia Pacific’s continued fertiliser consumption growth create the most commercially significant above-average demand pool.

Battery and EV applications are the fastest-growing end use because the global EV production ramp is creating new sulfuric acid demand in electrolyte preparation, formation cycling, and battery recycling processes that are growing proportionally with EV manufacturing scale. Lead-acid batteries for start-stop vehicle systems and uninterruptible power supplies create the existing substantial battery sector acid demand. Lithium-ion battery manufacturing’s sulfuric acid requirements in electrode processing and cathode material production create an above-average growth demand overlay. Battery recycling’s sulfuric acid recovery loops create circular demand that compounds with battery fleet growth.

By Concentration, concentrated sulfuric acid dominates, oleum grows fastest

Concentrated sulfuric acid retained the dominant concentration position in the sulfuric acid market in 2025. The 93-98% concentration range used in fertiliser production, metal pickling, petroleum alkylation, and general chemical manufacturing encompasses the majority of global acid consumption whose commercial standardisation around concentrated grades creates the most developed production infrastructure, distribution logistics, and customer specification framework. The contact process’s standard output is concentrated sulfuric acid whose absorption and dilution to specific application concentrations defines the downstream processing that most industrial consumers perform.

Oleum and fuming sulfuric acid are the fastest-growing concentration category because the semiconductor industry’s electronic-grade acid requirement and specialty organic chemical sulfonation processes require the highest-purity, highest-reactivity acid formulations whose production requires additional absorption and purification steps beyond standard concentrated acid manufacture. BASF’s electronic-grade sulfuric acid expansion in China and global semiconductor fab capacity additions are creating structured oleum demand whose premium pricing and above-average specification requirements create commercially attractive margin opportunities for qualified producers.

By End User Industry, agriculture dominates, electronics grows fastest

Agriculture retained the dominant end user industry position in the sulfuric acid market in 2025. The foundational role of phosphate fertiliser in global crop production creates a structural commercial relationship between agricultural activity scale and sulfuric acid demand whose annual procurement cycle follows the global fertiliser production calendar. The Mosaic Company, Nutrien, and OCP Group’s combined phosphate fertiliser production capacity represents the single largest institutional sulfuric acid procurement concentration in the global market, whose combined consumption defines the market’s commercial character and sustains above-average volumes that create logistics and supply chain infrastructure investment around major fertiliser-producing regions.

Electronics and semiconductors are the fastest-growing end user industry because the extraordinary capital investment in new semiconductor fabrication capacity under the CHIPS Act in the U.S., the European Chips Act, and equivalent programmes in Japan, South Korea, and Taiwan is creating growing demand for ultra-high-purity electronic-grade sulfuric acid whose specifications exceed industrial acid purity by several orders of magnitude. Semiconductor wafer cleaning, etching, and oxide stripping processes consume electronic-grade acid at volumes that scale with wafer starts per month, creating a structurally growing premium acid demand category whose commercial value per tonne substantially exceeds industrial grade acid pricing.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Sulfuric Acid Market Insights

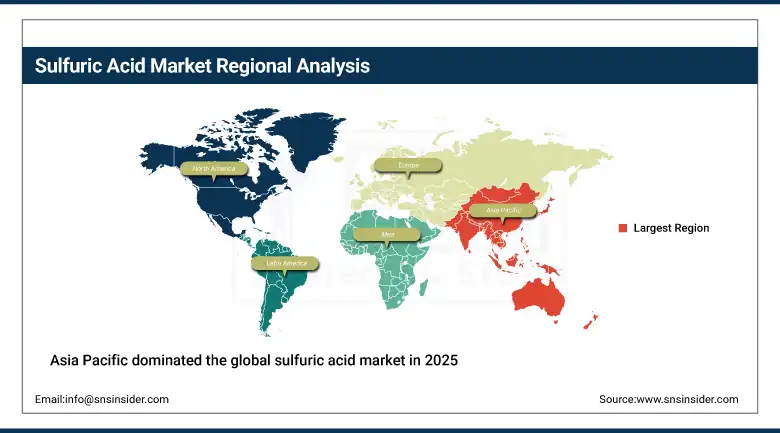

Asia Pacific dominated the global sulfuric acid market in 2025 as the world’s largest production and consumption region, driven by China’s extraordinary phosphate fertiliser production scale, India’s growing fertiliser and chemical manufacturing demand, and the region’s rapidly expanding semiconductor and battery manufacturing investment. China accounts for approximately 54.6% of Asia Pacific revenues through its position as the world’s largest sulfuric acid producer and consumer, whose integrated phosphoric acid and fertiliser manufacturing complex consumes the majority of domestic acid production while also generating significant export volume.

India and Southeast Asia represent the most commercially dynamic emerging markets within Asia Pacific, where agricultural expansion, industrial development, and the progressive localisation of battery and electronic manufacturing are creating above-average acid demand growth. India’s fertiliser self-sufficiency programme investment and the Make in India initiative’s chemical manufacturing development are creating structured domestic sulfuric acid demand whose scale is progressively reducing import dependence.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Sulfuric Acid Market Insights

North America is a significant sulfuric acid market anchored by the U.S. phosphate fertiliser industry’s concentrated production in Florida and Idaho, petroleum refining’s alkylation acid demand, and the growing semiconductor and battery manufacturing sectors. The United States accounts for approximately 82.5% of North American revenues through its integrated fertiliser producer captive acid consumption and merchant market supplied by PVS Chemicals and Chemtrade Logistics. The CHIPS Act’s semiconductor manufacturing investment is creating a new growing electronic-grade acid procurement category whose volume will compound with each new fab commissioned.

Canada contributes approximately 17.5% of North American revenues through its base metal smelting sector’s by-product acid production, potash fertiliser industry’s sulfuric acid consumption, and the mining industry’s heap leach copper operations whose acid demand sustains consistent base-metal-linked procurement across commodity price cycles.

Europe Sulfuric Acid Market Insights

Europe is a technically sophisticated sulfuric acid market where environmental regulation drives efficient production technology adoption, chemical manufacturing creates consistent speciality acid demand, and the region’s battery gigafactory investment programme is creating above-average battery-grade acid demand growth. Germany accounts for approximately 22.3% of European revenues through BASF’s sulfuric acid production and catalyst system operations, the chemical and pharmaceutical industries’ specialty acid consumption, and the country’s position as Europe’s largest chemical manufacturing hub.

The Netherlands, Belgium, and Spain are significant secondary European markets where petrochemical refining’s alkylation acid demand, fertiliser production, and the growing battery manufacturing sector create consistent commercial procurement. European sulfuric acid production from base metal smelting operations at Aurubis and Boliden provides merchant market supply that sustains domestic industry’s acid access independent of elemental sulfur import logistics.

MEA & Latin America Sulfuric Acid Market Insights

The Middle East and Africa and Latin America are growing sulfuric acid markets where phosphate fertiliser development, mining sector expansion, and industrial growth are creating structured demand. Saudi Arabia leads MEA revenues at approximately 31.2% through SABIC’s chemical complex sulfuric acid consumption, Saudi Arabia’s fertiliser industry investment, and the refining sector’s alkylation requirements. Morocco’s OCP Group phosphate complex represents the most commercially significant single sulfuric acid consumption infrastructure in the MEA region.

Brazil leads Latin American revenues at approximately 44.2% through its agricultural sector’s fertiliser consumption, mining industry’s copper and gold extraction acid demand, and the growing automotive battery sector. Chile’s copper mining industry’s heap leach operations are one of the largest single national sulfuric acid demand concentrations globally, whose procurement volume sustains significant dedicated production capacity in proximity to the Atacama copper production region.

Market Dynamics

Growth Drivers: Global food production requiring fertiliser phosphate demand and battery/semiconductor manufacturing creating premium new demand

Global food production requirement is the sulfuric acid market’s most structurally certain commercial growth driver. The World Bank projects global food demand will increase 50% by 2050 as population grows toward 10 billion and dietary protein consumption rises with income levels in developing economies. Phosphate fertiliser’s foundational role in achieving this food production target creates a non-discretionary agricultural input whose demand grows proportionally with cropland expansion and yield intensity improvement programmes. Each percentage point increase in global fertiliser consumption creates proportional sulfuric acid demand whose scale reflects the >55% application share that fertilisers represent in global acid consumption.

Battery manufacturing and semiconductor fabrication are simultaneously creating the most commercially dynamic new demand segments in the sulfuric acid market. The global EV production ramp’s acid requirements for electrolyte preparation, formation cycling, and battery recycling, combined with the extraordinary semiconductor capacity investment under CHIPS Act and equivalent programmes, are creating structured new demand categories whose above-average purity specifications create premium acid procurement opportunities that standard industrial acid markets cannot serve. Each new battery gigafactory or semiconductor fab commissioned creates a defined acid procurement relationship whose volume compounds with facility ramp-up.

Restraints: Sulfuric acid transport hazard creating logistics complexity and environmental compliance cost of SO2 tail gas management

Sulfuric acid’s highly corrosive nature and transport hazard classification create logistics complexity and cost that limits merchant market distribution radius. The requirement for specialised stainless steel or lined railcars and tankers, dedicated handling infrastructure, and emergency response planning creates logistics investment that sustains regional production near consumption centres rather than efficient long-distance supply chains. This logistics constraint creates multiple regional market structures whose economics are determined by local production capacity relative to local demand rather than global arbitrage.

Environmental compliance cost for SO2 tail gas management in sulfuric acid plants creates above-average capital and operating expense whose regulatory stringency varies significantly across national jurisdictions. EPA and EU air quality standards require near-complete SO2 conversion efficiency from double-absorption contact process configurations whose capital cost exceeds simpler single-absorption plant designs. Developing market producers operating under less stringent environmental frameworks can produce acid at lower compliance cost, creating competitive advantage that distorts global trade economics.

Opportunities: Electronic-grade acid for semiconductor expansion, battery acid recycling circular economy, and African fertiliser infrastructure investment

Electronic-grade sulfuric acid for semiconductor manufacturing represents the most commercially value-accretive near-term market development opportunity. Ultra-high-purity acid graded at parts-per-trillion metallic contaminant levels whose production requires dedicated ion-exchange purification, semiconductor-grade packaging, and cleanroom-compatible logistics commands pricing premiums of 10-20 times standard industrial grade acid. BASF’s electronic-grade capacity expansion in China and the CHIPS Act’s semiconductor fab investment are creating growing demand for this premium grade whose qualified producer community is small relative to demand growth potential.

African fertiliser infrastructure investment represents the most commercially significant emerging market development opportunity in the sulfuric acid market. Africa’s underdeveloped phosphate fertiliser manufacturing capacity, juxtaposed with Morocco’s OCP Group’s extraordinary phosphate rock resource position and the continent’s agricultural intensification investment, creates a structured demand growth pathway whose commercial realisation through new fertiliser complex development will require dedicated sulfuric acid production infrastructure investment at scale.

Recent Developments:

-

2023: LG Chem expanded its sulfuric acid production capabilities in 2023, focusing on oleum production to support increasing demand from the semiconductor electronics industry and EV battery manufacturing sectors, reflecting the commercial diversification of sulfuric acid demand into high-purity, high-growth industrial applications.

-

2023: The Mosaic Company ramped up sulfuric acid production for phosphoric acid manufacturing in 2023 in response to rising global fertiliser demand, demonstrating the direct commercial linkage between global agricultural productivity investment and sulfuric acid procurement volume at integrated fertiliser producer scale.

-

2022: DuPont, in partnership with several companies, developed an advanced sulfuric acid catalyst technology in 2022 to improve contact process production efficiency and reduce SO2 emissions in refining and petrochemical applications, strengthening DuPont’s position in high-performance sulfuric acid catalyst systems.

Sulfuric Acid Market Key Players

-

BASF SE

-

Chemtrade Logistics Inc.

-

PVS Chemicals Inc.

-

The Mosaic Company

-

Solvay S.A.

-

AkzoNobel N.V.

-

Vale Fertilizantes S.A.

-

Nutrien Ltd.

-

DuPont de Nemours

-

Aurubis AG

-

LG Chem

-

Sumitomo Chemical

-

Honeywell International

-

Ineos Group

-

Hubei Xingfa Chemicals

-

OCP Group

-

EuroChem Group

-

ICL Group

-

Eco Services Operations

-

Southern States Chemical

Sulfuric Acid Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.35 Billion |

| Market Size by 2035 | USD 75.16 Billion |

| CAGR | CAGR of 13.8% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Raw Material (Elemental Sulfur, Base Metal Smelters, Pyrite Ores) • by Application (Fertilizers, Chemical Manufacturing, Metal Processing, Petroleum Refining, Battery/EV, Others) • by Concentration (Concentrated Sulfuric Acid, Dilute Sulfuric Acid, Oleum/Fuming Sulfuric Acid) • by End User Industry (Agriculture, Automotive, Electronics & Semiconductor, Mining, Pharmaceuticals, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | BASF SE, Chemtrade Logistics Inc., PVS Chemicals Inc., The Mosaic Company, Solvay S.A., AkzoNobel N.V, Vale Fertilizantes S.A., Nutrien Ltd., DuPont de Nemours, Aurubis AG, LG Chem, Sumitomo Chemical, Honeywell International, Ineos Group, Hubei Xingfa Chemicals, OCP Group, EuroChem Group, ICL Group, Eco Services Operations, Southern States Chemical |

Frequently Asked Questions

The Sulfuric Acid Market is expected to grow at a CAGR of 13.8% from 2026 to 2035.

The Sulfuric Acid Market was valued at USD 20.35 Billion in 2025.

Global food production requirement sustaining non-discretionary phosphate fertiliser demand that consumes over 55% of sulfuric acid output, and EV battery manufacturing and semiconductor fabrication capacity expansion creating premium new acid demand segments with above-average purity specifications and growth trajectories.

Fertilizers dominated the Sulfuric Acid Market with approximately 55% share in 2023, while the Battery/EV segment is the fastest growing.

Asia Pacific dominated the Sulfuric Acid Market in 2025 as the world’s largest production and consumption region, with China accounting for approximately 54.6% of Asia Pacific revenues.

Get in Touch