Performance Fabric Market Report Scope & Overview

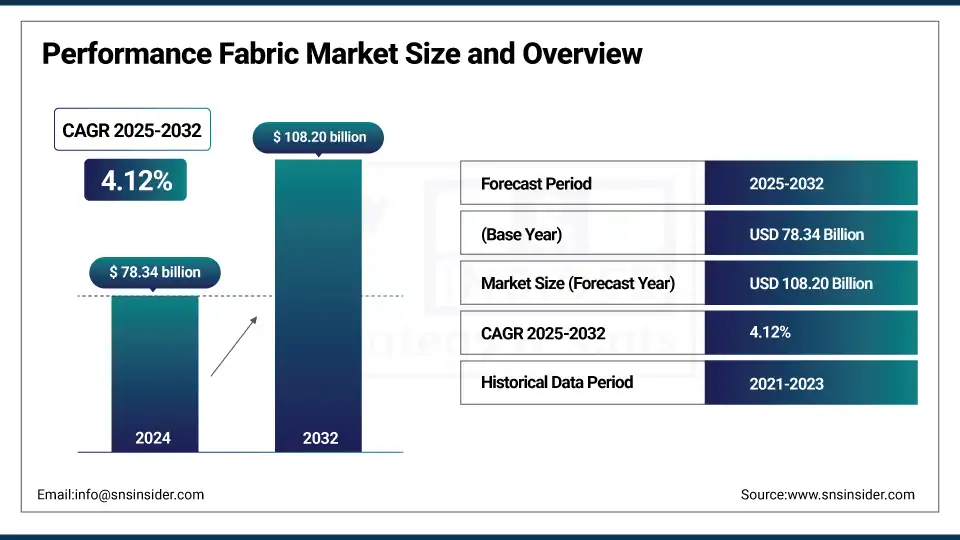

The Performance Fabric Market size was valued at USD 78.34 billion in 2024 and is expected to reach USD 108.20 billion by 2032, growing at a CAGR of 4.12% over the forecast period of 2025-2032.

Performance Fabric Market Analysis focuses on the growing need for sports and activewear among health-conscious consumers with fitness-oriented lifestyles. Rising awareness regarding workouts, including gym, running, yoga, and outdoor sports, has resulted in a greater need for fabrics that provide comfort, stretchability, breathability, and moisture management. Performance fabrics, which are sweat-wicking, stretchy, and durable, are being favored in athletic apparel production. The growth of the market is also steered on account of the increasing launch of athleisure fashion, owing to the high demand for multi-functional attire that satisfies consumer requirements of clothing that imparts both style and performance, which drives the performance fabric market growth.

To Get more information On Performance Fabric Market - Request Free Sample Report

In fact, 46.9% of U.S. adults aged 18 and older adhered to the aerobic guidelines in 2020 and 24.2% to the combined aerobic and muscle-strengthening recommendations, as per the CDC's National Center for Health Statistics.

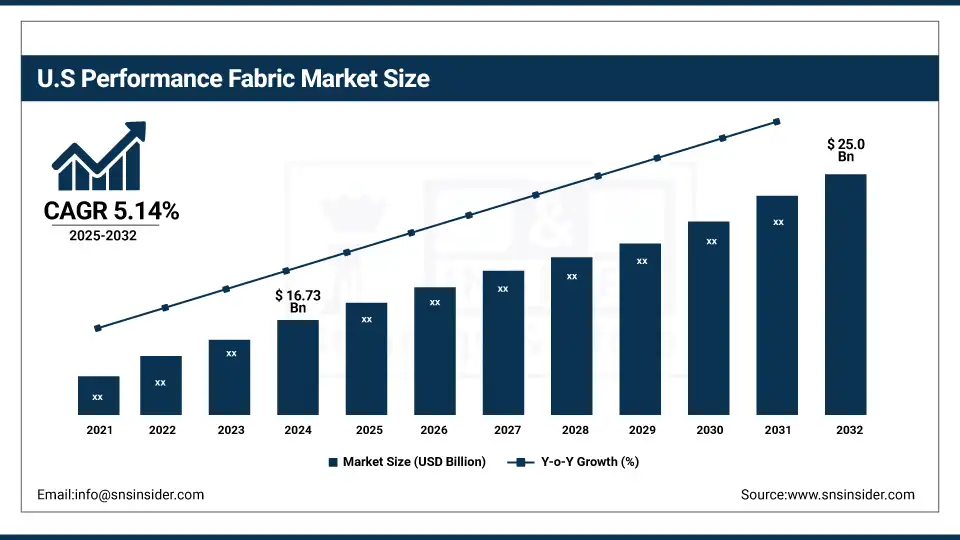

The U.S Performance Fabric market size was USD 16.73 billion in 2024 and is expected to reach USD 25.0 billion by 2032 and grow at a CAGR of 5.14% over the forecast period of 2025-2032. It is due to the presence of matured sportswear industry, high defense spending in US and demand for an innovative apparel for the consumers. Driven by American consumers who are more focused on comfort, performance, and sustainability, brands are doubling down on next-gen textile technologies. Aramid and flame-resistant textiles used in militarized fabrics for military uniforms and combat gear are the most significant application area for the defense sector in the country. Due to a strong established retail network, coupled with e-commerce penetration, performance fabrics influence a broad spectrum across end-user industries.

Market Dynamics

Drivers

-

Rising Demand for Functional Apparel in Sports and Fitness Drives the Market Growth

These performance fabrics are widely used in the manufacture of activewear and sportswear, and the growing trend of fitness is one of the factors creating a massive demand for this type of wear. Performance textiles have properties like stretch, moisture management, breathability, and odor control that consumers need in clothing. This trend is prevalent, especially in younger demographics and fitness-oriented professionals. The continuous market growth of gym activities, running, and yoga is due to increasing interest in these activities. Athleisure fashion clothing that can be both workout wear and casual wear contributes to that demand. With the comfort, performance equation having a heavier weight on the comfort side in the eyes of consumers, apparel brands are leaning into performance fabrics.

For Instance, in 2023, Nike put USD 125 million towards expanding its innovative, sustainable performance fabrics research and development division to align with increasing consumer demand.

Restrain

-

High Cost of Raw Materials and Production May Hamper the Market Growth

The performance fabrics utilize high-end materials like aramid, spandex, or specially treated polyester, and those materials are pricier than regular fabrics. Additionally, the required technological processes for finishing coating, lamination, and nanotechnology constitute a cost in the production price. As a result, the end-product price is higher, which limits their acceptance in price-sensitive markets. This creates a prohibitively high cost for smaller apparel brands and synthetic performance materials. Also, the ever-changing prices of petroleum-based synthetic fibers impact the cost structure negatively. The lack of funds may hence stifle the growth of performance fabric adoption in some regions.

Opportunities

-

Rising Adoption in Military and Public Safety Applications Creates an Opportunity in the Market

The increasing demand for performance fabrics is attributed to the needs in the military and public safety sectors, where high-protection, durability, and multi-functional performance are necessary during extreme and hazardous site conditions. These textiles are designed to provide flame protection, ballistic protection, chemical protection, and thermal shielding to people like soldiers, firefighters, and police officers.

More recent modern militaries in all locations are figuring out how to utilize light-weight and breathable materials, the ideal garment for protection from the environment, improved with materials that lessen movement limitations while still offering resistance to particular biological dangers driving the Performance Fabric market trends.

In 2024, the U.S. Department of Defense set aside USD 40 million for advanced fabric procurement 2024, focused on lightweight, flame-resistant, and weather-adaptive uniforms and gear for frontline troops.

Segmentation Analysis:

By Material Type

Polyester held the largest Performance Fabric market share, around 38.60%, in 2024. This dominance is attributed to the rising need for better protection concerning military personnel, government officials, and other high-profile individuals as geopolitical tensions, threats of terrorism, and civil unrest continue to rise. Performance Fabric is an essential aspect of armored vehicles; it provides ballistic protection while still allowing the vehicle to see outside and have its physiological structure like others. Several fleets are being upgraded with a massive investment boost to state and even private sectors that provide advanced glazing systems that comply with stringent international safety standards. The segment also continues to lead in the market, boosted by wearable technology developments in lightweight, multi-layered glass materials that have expanded their use in high-performing defense vehicles and even luxury low-profile vehicles.

Nylon held a significant Performance Fabric market share. It is due to the performance, and it continues to offer advantages over competing materials in high-demand applications like sportswear, outdoor apparel, swimsuits, and military uniforms. Its durability and quick-drying, along with its lightweight nature, make it particularly appropriate for rough environments and performance-heavy ecosystems. Additionally, the ability of nylon to blend seamlessly with other fibers for added stretch and durability gives greater design freedom for fabric development. In both consumer and industrial markets, increasing demand for durable, high-performance fabrics continues to propel nylon relevance and a robust share of the performance fabric space.

By End Use

The textile & apparel segment held the largest market share, around 40.21%, in 2024. It is owing to the increasing inclination towards high-performance clothing among consumers, not just as everyday wear but also as technical performance apparel. Because of their enhanced properties (like moisture-wicking, stretchability, durability, breathability, etc.), performance fabrics are getting fresher uses in every category of casual wear, workwear, and fashion apparel. One major driver of this trend has been the rise of athleisure: Consumers want that perfect cross between stylish and functional apparel. In addition, textile manufacturers and brands are putting money into cutting-edge fabric technologies to satisfy growing standards for comfort, performance, and sustainability.

Defense & public safety hold a significant market share in the Performance Fabric market. This segment comprises high-performance fabrics market that provide flame, cut, ballistic & chemical resistance, crucial to the field of military personnel, firefighters, law enforcement officers, and emergency responders. Due to increasing global security issues and investment in the modernization of defense infrastructure, high-performance textiles are gaining prominence for use in uniforms and protective equipment of the defense sector worldwide. In addition to its function and comfort attributes, these fabrics also allow for greater movement and endurance in a harsh environment.

Regional Analysis:

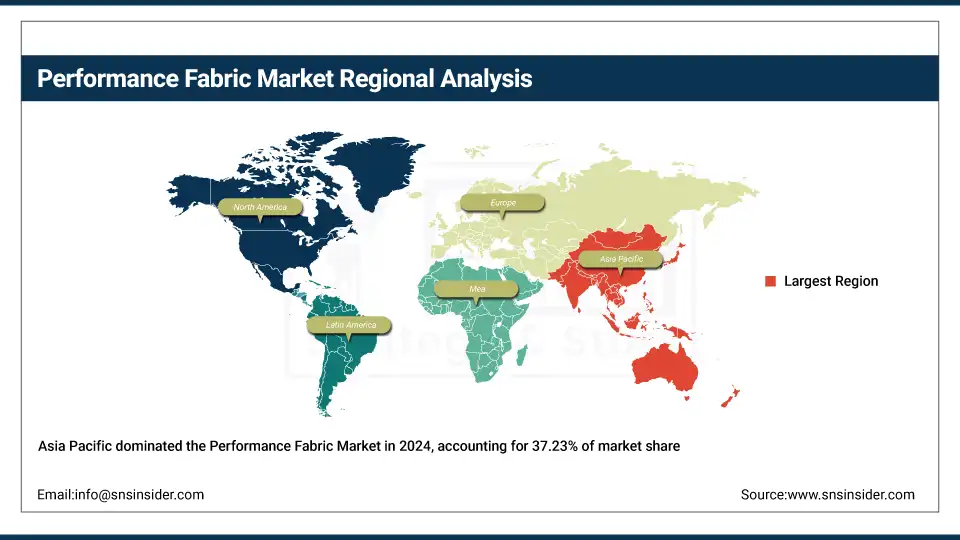

Asia Pacific Performance Fabric market held the largest market share, around 37.23%, in 2024. It is due to the rapid urbanization, rising fitness trends, and availability of large-scale textile manufacturing hubs are a few of the significant aspects behind the growth in the Performance Fabric Market over the forecast period. The growing middle-class populations, rising health awareness, and higher disposable income of people in countries like China, India, Japan, and South Korea are propping up the demand for economical activewear that caters to functional and regular wearing needs. In addition, the region has emerged as the leading region in the global textile export market, leveraging low-cost labor, high manufacturing infrastructure, and material science innovation. Such demand has transformed Asia-Pacific into a strategic center for global brands seeking to source and sustain high-performance fabrics.

Get Customized Report as per Your Business Requirement - Enquiry Now

In 2024, the Ministry of Textiles, India, announced the scheme on “PM MITRA Parks” to enhance the Manufacturing of performance fabrics through Integrated Textile Parks, themed on Technical and Green Textiles.

North America Performance Fabric market held a significant market share and is the fastest-growing segment in the forecast period. It is due to the region having several top garment manufacturers and industries, high consumer expenditure on premium activewear, and early adoption of advanced textile technologies. The U.S. and Canada possess a relatively mature sports and outdoor culture, contributing to steady demand for performance fabrics in the sportswear, athleisure, and outdoor gear categories. The sales of fabric consumption for protective clothing also remain steady with government procurement for defense and public safety. The advanced textile R&D ecosystem and the presence of leading brands in the region, such as Nike, Under Armour, and Lululemon, is fueling the market dominance.

In 2023, Under Armour expanded its Baltimore innovation hub to include advanced performance textile research focused on sustainable and smart fabrics.

Europe held a significant market share in the forecast period. It is due to high product approval due to sustainable fashion demand, strong regulatory standards, and innovation in technical textiles. Germany, Italy, and France are the most effective at textile engineering and exports of high-quality performance fabrics (sportswear, fashion, protective wear). Green manufacturing to generates eco-textiles, gaining advantages over recycling and multi-purpose textiles, as per consumers demand of European consumers are primarily selecting recycled, multi-functional textiles. Similarly, R&D for performance materials is also driven by interest in developing sustainable textile systems supported by the government.

In 2023, Polartec (a Milliken brand) launched a new line of biodegradable performance fabrics in Europe, catering to the growing demand for circular textile solutions.

Key Players:

The major performance fabrics companies are DuPont, Toray Industries, Invista, Hyosung Corporation, Lenzing AG, Polartec, Schoeller Textil AG, Milliken & Company, Teijin Limited, HeiQ Materials AG

Recent Development:

-

In 2025, Polartec expanded the Power Shield Pro line for Spring/Summer 2026 with ~50% carbon footprint reduction via plant-based Biolon nylon and maintaining 20k/20k waterproof/breathability.

-

In July 2024, Under Armour launched its first products featuring Neolast, a proprietary recyclable elastomer fiber developed in partnership with Celanese, significantly improving sustainability by aiming to reduce spandex use by 75% by 2030

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 78.34 Billion |

| Market Size by 2032 | USD 108.20 Billion |

| CAGR | CAGR of4.12% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Material Type (Polyester, Nylon, Spandex, Aramid, and Others) • By End Use (Textile & Apparel, Sports & Outdoor, Defense & Public Safety, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | DuPont, Toray Industries, Invista, Hyosung Corporation, Lenzing AG, Polartec, Schoeller Textil AG, Milliken & Company, Teijin Limited, HeiQ Materials AG |

Frequently Asked Questions

Ans: Sustainability is significantly reshaping the Performance Fabric Market as consumers and brands increasingly prioritize eco-friendly materials and processes. This shift is driving demand for recycled fibers, bio-based fabrics, and low-impact manufacturing.

Ans: Smart textiles enhance the Performance Fabric Market by integrating sensors and responsive technologies into fabrics. They enable features like temperature control, moisture detection, and biometric monitoring. This innovation supports advanced applications in sportswear, healthcare, and defense sectors.

Ans: Asia Pacific currently dominates the Performance Fabric market.

Ans: Rising demand for functional apparel in sports and fitness drives the market growth.

Ans: The Performance Fabric Market was valued at USD 78.34 billion in 2024.

Get in Touch