PET Foam Market Report Scope & Overview:

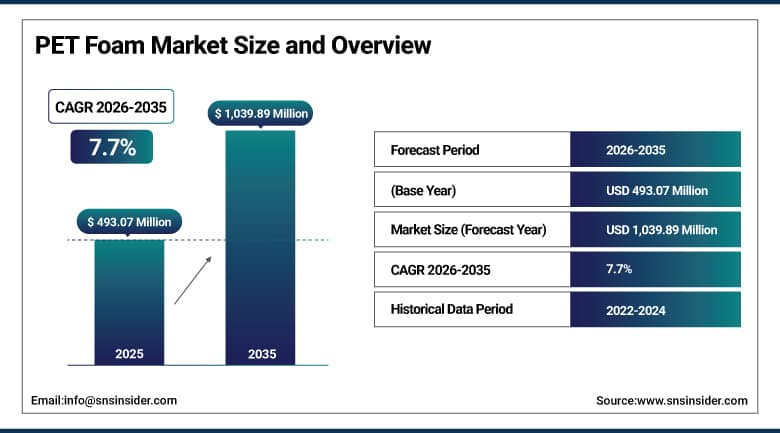

The PET Foam Market was valued at USD 493.07 Million in 2025 and is expected to reach USD 1,039.89 Million by 2035, growing at a CAGR of 7.7% from 2026 to 2035.

The PET Foam Market covers materials used in sandwich composites, like those made from polyethylene terephthalate. These foam materials must be both light and extremely sturdy, handling heat too. Manufacturers also recycle them and create them through processes such as extrusion and continuous foaming. We see these foams in all sorts of places - wind turbine blades, boats, cars, airplanes, trains, and even building components.

When making decisions, the market looks at supply chains, material costs, price swings, sustainability rules, and technology in lightweight composites. It also sees more use of PET foam in renewable energy, electric vehicles, and infrastructure. As a result, a big push for eco-friendly materials is now spreading through many industries.

In 2025, Armacell expanded its PET foam capacity in Europe to address the growing demand for blades in the wind energy sector, emphasizing the use of recyclable materials in lightweight composites, particularly for offshore wind. This is a component of green energy infrastructure and shows their dedication to renewable energy sources.

Market Size and Forecast:

-

Market Size in 2026E: USD 533.51 Million

-

Market Size by 2035: USD 1,039.89 Million

-

CAGR: 7.7 % from 2026 to 2035

-

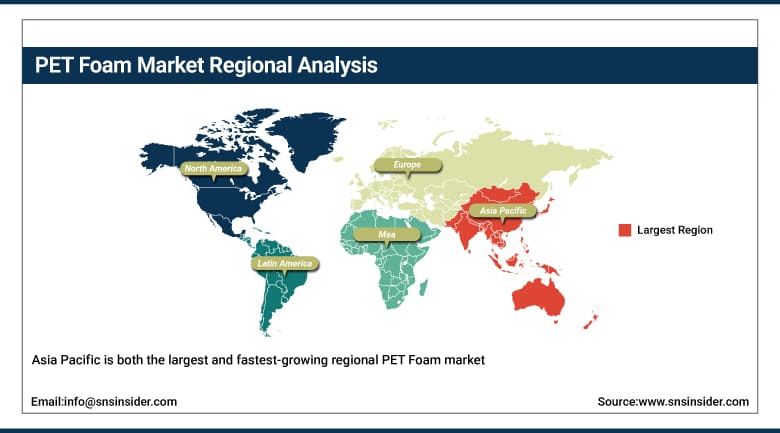

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On PET Foam Market - Request Free Sample Report

PET Foam Market Trends:

-

Rapid adoption in wind energy blades drives demand for lightweight, recyclable PET foam structural core materials globally.

-

Growing preference for sustainable composites accelerates replacement of PVC and PU foams in marine and automotive industries.

-

Increasing use in electric vehicle lightweighting improves energy efficiency, driving higher structural PET foam integration across components.

-

Advancements in recycled PET feedstock technologies enhance cost efficiency and strengthen circular economy-based foam production systems.

-

Expanding aerospace and rail applications boost demand for high-performance, fire-resistant PET foam sandwich panel structures.

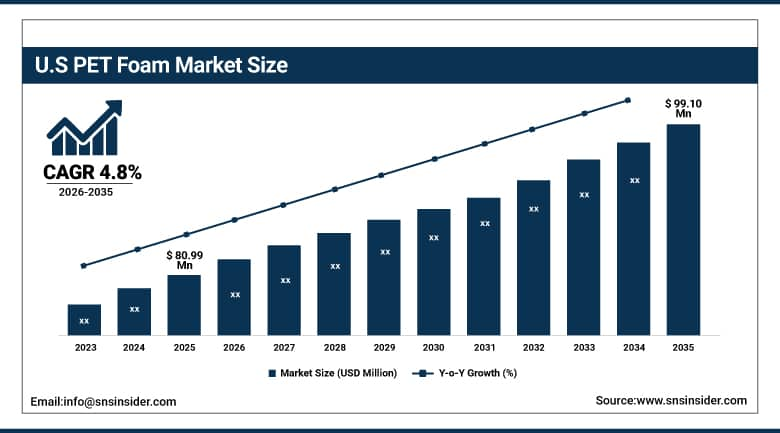

U.S. PET Foam Market Outlook

The United States continues to dominate the North America PET foam market in value terms, holding the largest share in the base year 2025 at USD 80.99 million out of the regional total of USD 99.10 million.

Their vast manufacturing infrastructure positions them strongly in the marine, wind energy, and transportation markets. Additionally, PET foam is gaining favor for its superior durability and improved recyclability over PVC foam, benefiting the structure and the environment.

From 2026 to 2035, the U.S. market should see its growth rate clock in at a steady 4.8% CAGR. This is thanks to a few key factors – expanding offshore and onshore wind projects, a strong need for composite parts in boats and vessels, and more use of lightweight composites in commercial vehicles and rail. Plus, it helps that there are major composite production centers in the Southeast and Gulf Coast areas. There's also a rising need for composites in aerospace and a push from regulators towards using more recyclable materials in industry supply chains.

PET Foam Market Segment Analysis:

-

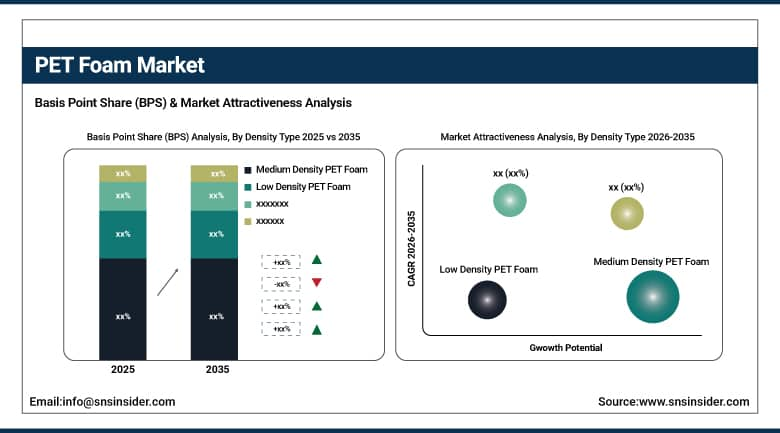

By Density Type, the medium density PET foam segment dominated the market with approximately 48.6% share in 2025, while the low-density PET foam is the fastest growing density type with a CAGR of approximately 9.74% during 2026 to 2035.

-

By Product Type, PET foam core dominated the market with approximately 35.9% share in 2025, while expanded PET (ePET) Foam / PET particle foam is the fastest growing type with a CAGR of approximately 12.7% during 2026 to 2035.

-

By Form, the rigid PET foam dominated the market with the 68.2% share in 2025, while the thermoformable PET Foam segment is growing rapidly with CAGR 12.33% during 2026 to 2035.

-

By Application, the sandwich core materials segment dominated the market with 56.0% share in 2025, while impact & vibration damping is the fastest growing application with a CAGR of approximately 11.97% during 2026 to 2035.

-

By End-Use Industry, wind energy (blades) segment dominated the market with 34.0% share in 2025, transportation (automotive, rail) is the fastest growing application with a CAGR of approximately 9.64% during 2026 to 2035.

-

By Manufacturing Process, extruded PET foam segment dominated the market with 59.5% share in 2025, thermoformed PET foam is the fastest growing application with a CAGR of approximately 11.52 % during 2026 to 2035.

By Density Type, medium density PET foam dominates, low density PET foam grows fastest

The PET foam market by density type reflects the fundamental material performance trade-offs between weight efficiency, structural rigidity, and processing versatility that govern foam core selection across composite manufacturing applications. Medium density PET foam commands the largest commercial share by virtue of its optimal balance of compressive strength, shear properties, and weight that positions it across the broadest range of structural sandwich composite applications, while low density variants are emerging as the fastest growing density category as lightweight and material cost efficiency priorities intensify across wind energy, transportation, and aerospace end-use markets.

Low density PET foam is booming in the global PET foam market because of big pushes for weight reduction in transport and aerospace. Companies in wind energy also want lighter materials to boost efficiency and ease supply chain costs. This foam fits the bill for many needs – it keeps structures light but strong. The segment grows at a solid 9.7% CAGR, showing how it's replacing heavier foam and balsa wood. Material scientists switch to it for newer designs in blades, vehicles, and planes. They aim to improve performance, save fuel, and cut weight where needed.

By Product Type, PET foam core dominates, expanded PET (ePET) foam / PET particle foam grows fastest

PET foam core owns a huge chunk of the global PET foam market, mainly due to its widespread use in wind energy blades, boat building, and reducing vehicle weight. It's super popular because of its awesome compressive strength, shear modulus, and ability to handle heat and chemicals without sweating. This stuff is what engineers turn to when they need something both strong and reliable. Because it does so well in harsh conditions compared to other foams, it remains the top pick for those building stuff that needs to be super durable.

Expanded PET foam and PET particle foam represent the fastest growing product type segment in the global PET foam market, driven by increasing interest in bead foam processing technologies, recyclability advantages, and the material's compatibility with molded three-dimensional component geometries that are difficult to achieve with conventional sheet or block foam formats. The segment's exceptional 12.7% CAGR reflects rising demand from automotive interior components, technical packaging, and specialty molded applications where geometric complexity, surface finish quality, and end-of-life recyclability are prioritized alongside core structural performance.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

81.72 % |

|

Europe |

Germany |

21.91% |

|

Asia Pacific |

China |

40.24% |

|

Middle East & Africa |

UAE |

26.14% |

|

Latin America |

Brazil |

37.20 % |

Asia Pacific PET Foam Market Insights

Asia Pacific is both the largest and fastest-growing regional PET Foam market. This is due to massive wind energy capacity expansion programs across China, India, and ASEAN markets are driving sustained high-volume growth in PET foam core demand for turbine blade sandwich composite manufacturing at both established and newly commissioned blade production facilities. The Indian PET foam market is projected to experience exceptional expansion driven by India's rapidly accelerating wind energy installation program targeting 500 GW of renewable energy capacity by 2030, strong government support for composite material adoption in transportation, and growing domestic composite manufacturing investment across wind blade, marine, and industrial sectors.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America PET Foam Market Insights

In 2025, North America took a big chunk of the global PET Foam revenues, with the US accounting for about 81.72%. The country's solid lead is thanks to its strong composite manufacturing setup in areas like marine, wind energy, and transport. Plus, more folks are turning to PET foam because it’s robust and fits better with recycling efforts compared to PVC foam in composite materials.

Canada's long coastline and tons of waterways are super important. They help a crucial marine composites industry thrive – think boat building with PET foam cores. The country's clever tech policies and move towards electric vehicles and composite rail parts are huge too. There's also a major effort into recycling materials and making stuff that can be reused, which is awesome. All this boosts the need for PET foam core materials, making the future look promising.

Europe PET Foam Market Insights

Europe held a significant share of global PET Foam revenues in 2025. Germany leads the European PET foam market in value terms, accounting for the largest share in the base year 2025 with USD 28.13 million out of the regional total of USD 128.36 million. This dominance is underpinned by Germany's position as Europe's largest composite manufacturing economy, its advanced wind energy technology development ecosystem, and its structurally significant marine, automotive, and rail composite manufacturing industries.

Poland's government has established ambitious renewable energy targets underpinning substantial onshore wind development pipeline, with Baltic offshore wind projects representing a major emerging demand driver for PET foam core materials in blade manufacturing.

MEA & Latin America PET Foam Market Insights

Saudi Arabia dominates the Middle East and Africa PET foam market in value terms, leading with $8.58 million in the base year 2025. That's a big chunk out of the region's total $27.04 million. The country's huge ongoing construction projects, which include composite cladding and panel systems, drive this. They're also building up offshore and onshore renewable energy sites, needing tons of composite parts. Plus, there's a surge in marine infrastructure spending along the Red Sea and Arabian Gulf coasts.

Brazil dominates the Latin America PET foam market in value terms, holding the largest share in the base year 2025 with USD 12.45 million out of the regional total of USD 33.46 million. Brazil's leadership is supported by its relatively developed composite manufacturing sector, significant marine boat building industry serving both recreational and commercial markets, and growing wind energy installation program that represents one of the most active renewable energy development pipelines in Latin America.

Market Dynamics:

Growth Drivers: Expansion of wind energy & composite blade manufacturing

The wind energy sector is the single most powerful structural demand engine in the global PET foam market, accounting for approximately 30-40% of total global PET foam consumption by volume. PET foam is selected as a structural core in sandwich composite wind blades for a combination of performance attributes that no competing material fully replicates: a high stiffness-to-weight ratio that reduces blade mass without compromising structural integrity; superior fatigue resistance across the 20-25-year operational life of a commercial wind turbine; compatibility with both infusion and prepreg composite manufacturing processes; and increasingly the decisive differentiating criterion.

Europe added approximately 18-20 GW of wind capacity in 2024, maintaining its position as the world's most active offshore wind development region and sustaining demand for high-specification composite core materials across blade OEM supply chains anchored in Denmark, Germany, Spain, and the UK.

Restraints: High raw material cost and petroleum price volatility.

PET foam production is structurally exposed to feedstock cost volatility in a way that most competing structural foam materials are not, because PET resin - the primary raw material - is derived from purified terephthalic acid (PTA) and monoethylene glycol (MEG), both of which are petrochemical derivatives whose pricing follows crude oil, paraxylene, and ethylene market cycles. During the 2022-2023 supply chain disruption cycle, PET resin prices spiked by 15-20% across multiple regions, forcing wind blade manufacturers' procurement teams to accelerate evaluation of alternative core materials.

Opportunities: Massive expansion of offshore wind energy and large-scale turbine manufacturing.

The global offshore wind boom represents the most structurally significant and commercially visible long-term growth opportunity in the entire PET foam market. Unlike onshore wind - a mature technology where incremental capacity additions are constrained by land availability, visual impact planning restrictions, and grid connection infrastructure - offshore wind is in an early-growth phase of deployment that is simultaneously expanding its geographic footprint and its per-turbine scale.

OEMs are standardizing high-performance PET foam in offshore structural specifications due to its fatigue resistance over 25-year offshore cycles, its chemical resistance to the saline, UV-exposed offshore environment, and its compliance with emerging blade recyclability requirements.

Recent Developments:

-

2025: Gurit launched RIMA PET wind blade core foam material manufactured exclusively from chemically recycled post-consumer PET, with an independently certified lifecycle carbon intensity of 1.2 kg CO₂/kg foam versus 2.6-3.1 kg CO₂/kg for virgin-grade PET foam.

-

2025: Armacell launched ArmaPET Eco range that uses up to 100% recycled PET in structural foam cores, achieving a reduction in lifecycle emissions of 35-50% depending on the application, and has achieved commercial-scale supply qualification with wind energy OEM procurement programmes across multiple European markets.

-

2025: 3A Composites expanded its AIREX PET foam product line with enhanced recycled content variants, targeting wind energy blade manufacturers focusing on circular material adoption.

PET Foam Market Key Players are:

-

ARMACELL

-

3A COMPOSITES

-

SEKISUI KASEI CO., LTD.

-

DIAB GROUP

-

GURIT HOLDING AG

-

QINGDAO REGAL NEW MATER

-

3D CORE GMBH & CO. KG

-

SKY COMPOSITES AG

-

TOPOLO NEW MATERIALS

-

4A MANUFACTURING GMBH

-

CORELITE

-

VISIGHT

-

CARLIER PLASTIQUES

-

TONGXIANG SELVA COMPOSI

-

CEL COMPONENTS S.R.L

-

CHANGZHOU JLON COMPOSIT

-

COMPOSITE ESSENTIAL MATER

-

CHANGZHOU UTEK COMPOSIT

-

CARBON-CORE CORP.

PET Foam Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 493.07 Million |

| Market Size by 2035 | USD 1,039.89 Million |

| CAGR | CAGR of 7.7% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Expanded PET (ePET) Foam / PET Particle Foam, Virgin PET Foam, Recycled PET Foam (rPET/ePET), PET Foam Core, PET Foam Sheets & Blocks) • By Density Type (Low Density Pet foam, Medium Density Pet foam, High Density Pet Foam) • By Form (Rigid Pet Foam, Flexible / Semi Rigid Pet Foam, Thermoformable Pet Foam) • By Application (Sandwich Core Materials, Thermal Insulation, Structural Reinforcement, Buoyancy Materials, Impact & Vibration Damping) • By End-Use Industry (Wind Energy (blades), Marine, Transportation (Automotive, Rail), Aerospace, Construction, Industrial Equipment) • By Manufacturing process (Extruded PET Foam, Molded PET Foam, Thermoformed PET Foam) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Armacell, 3a Composites, Sekisui Kasei Co., Ltd., Diab Group, Gurit Holding Ag, Qingdao Regal New Materials, 3d Core Gmbh & Co. Kg, Sky Composites Ag, Topolo New Materials, 4a Manufacturing Gmbh, Corelite, Visight, Carlier Plastiques, Tongxiang Selva Composites, Cel Components S.R.L, Changzhou Jlon Composites, Composite Essential Materials, Changzhou Utek Composites, Carbon-Core Corp. |

Frequently Asked Questions

The PET Foam Market is expected to grow at a CAGR of 7.7% from 2026 to 2035.

The PET Foam Market was valued at USD 493.07 Million in 2025.

Expansion of wind energy & composite blade manufacturing.

PET Foam Core dominated the PET Foam Market in 2025.

Asia Pacific dominated the PET Foam Market in 2025.

Get in Touch