Automotive Industry Market Report Scope & Overview:

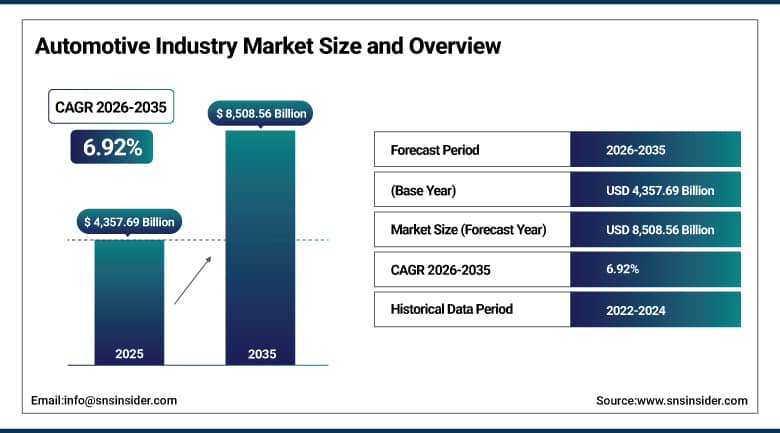

The Automotive Industry Market was valued at USD 4,357.69 Billion in 2025 and is expected to reach USD 8,508.56 Billion by 2035, growing at a CAGR of 6.92% from 2026 to 2035.

The Automotive Industry Market is growing at a rapid rate due to the increasing demand for vehicles in developing countries, increased electrification of vehicles, and the continuous incorporation of electronics, connectivity, and driverless vehicles into newly manufactured vehicles. The automotive industry includes manufacturing, selling, and servicing of passenger cars, commercial vehicles, electric vehicles, and two wheelers. The automotive industry is one of the most important industrial ecosystems around. In addition, the growth of the market is also being driven by increased software-based vehicle architecture, which increases the value of the vehicle, and urban congestion policies, which increase electric vehicle adoption in developed countries.

Toyota and BYD both expanded their electric vehicle platform production capacity in 2026, reflecting the automotive industry's continued structural shift toward electrification as automakers race to capture growing consumer demand for connected, software-defined vehicles.

Market Size and Forecast:

-

Market Size in 2026E: USD 4,659.00 Billion

-

Market Size by 2035: USD 8,508.56 Billion

-

CAGR: 6.92% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Automotive Industry Market - Request Free Sample Report

Automotive Industry Market Trends:

-

Rising electric vehicle adoption is driving automakers to expand dedicated EV platforms and battery manufacturing capacity across both mature and emerging automotive markets.

-

Growing integration of software-defined vehicle architecture is increasing the value and complexity of connected services, over-the-air updates, and advanced driver assistance systems.

-

Increasing urban congestion policies across Europe and parts of North America are accelerating electric vehicle penetration and reshaping automaker product portfolio strategies.

-

Expanding commercial fleet modernization investment across Asia Pacific is supporting infrastructure development and vehicle demand tied to growing logistics and e-commerce sectors.

-

Strategic partnerships among automakers, semiconductor suppliers, and battery manufacturers are supporting development of increasingly integrated, vertically coordinated vehicle supply chains.

U.S. Automotive Industry Market Outlook:

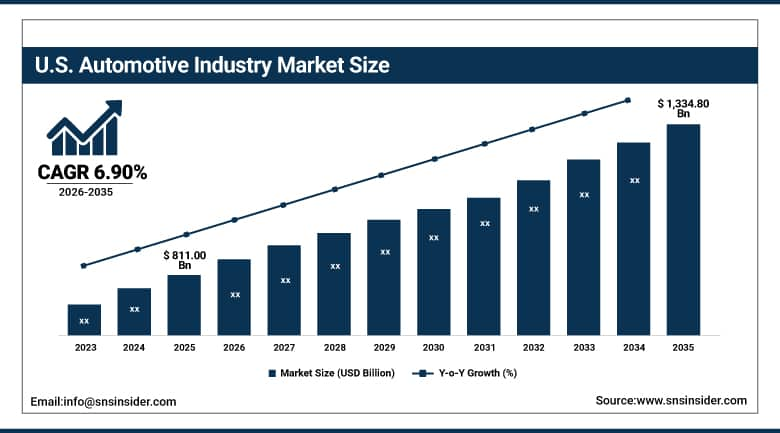

The U.S. Automotive Industry Market was valued at USD 811.00 Billion in 2025 and is projected to reach USD 1,334.80 Billion by 2035, growing at a CAGR of 6.90% during 2026–2035.

The country’s top automakers are increasing production of vehicles that use electricity, hybrid power, and innovative vehicle platforms with enhanced software, in response to high consumer demand for connectivity and increased government encouragement to produce batteries and semiconductors in-country. Increased research into self-driving vehicles and enhanced safety technologies, coupled with ongoing improvements in the dealerships’ sales process, are helping to increase domestic demand for advanced automotive technology.

In 2026, General Motors expanded its U.S. electric vehicle battery manufacturing capacity to support growing domestic production of its next-generation EV platform lineup amid rising consumer demand for connected, software-defined vehicles.

Automotive Industry Market Segment Analysis:

-

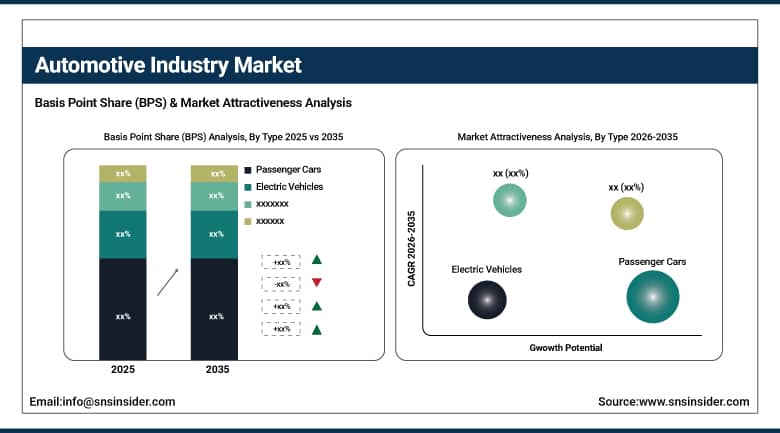

By Type, Passenger Cars dominated the Automotive Industry Market with a 54.60% share in 2025, while Electric Vehicles is the fastest-growing type segment with a CAGR of 14.80% from 2026–2035.

-

By Fuel Type, Internal Combustion Engine dominated the Automotive Industry Market with a 57.00% share in 2025, while Electric is the fastest-growing fuel type segment with a CAGR of 15.60% from 2026–2035.

-

By Sales Channel, Dealerships dominated the Automotive Industry Market with a 61.40% share in 2025, while Online Retail is the fastest-growing sales channel segment with a CAGR of 12.90% from 2026–2035.

-

By Vehicle Size, Mid-Size dominated the Automotive Industry Market with a 38.70% share in 2025, while Luxury is the fastest-growing vehicle size segment with a CAGR of 8.60% from 2026–2035.

By Type, Passenger Cars dominated the Automotive Industry Market, while Electric Vehicles is the fastest-growing segment.

Passenger Cars accounted for the maximum revenue market share of 54.60% in the Automotive Industry Market during 2025. Passenger cars continue to account for the highest vehicle category owing to the large number of private vehicles in matured as well as developing automotive sectors, in which passenger cars are still the primary mode of personal transportation around the world.

Electric Vehicles are estimated to grow at the highest CAGR of 14.80% during the forecast period of 2026-2035. Fast adoption of battery-powered and plug-in hybrid electric cars, due to stricter environmental norms, declining cost of batteries, and increase in charging stations, is driving the growth of this segment.

By Fuel Type, Internal Combustion Engine dominated the Automotive Industry Market, while Electric is the fastest-growing segment.

The Internal Combustion Engine segment ruled the Automotive Industry Market by contributing to 57.00% of the market's revenue share in 2025. The internal combustion engine cars continue to be the most popular among all the fuel types due to existing fueling infrastructure, lower capital costs, and consumer familiarity, especially in the developing economies, where electric cars charging infrastructure remains underdeveloped.

The Electric segment is projected to grow at the fastest CAGR of 15.60% from 2026 to 2035. The rising number of government incentives, stricter regulations regarding emissions, and fast falling costs of manufacturing batteries is fuelling the rising popularity of electric vehicles, whose sales volumes are expected to increase sharply in the coming years.

By Sales Channel, Dealerships dominated the Automotive Industry Market, while Online Retail is the fastest-growing segment.

Dealerships Segment had the highest share in the Automotive Industry Market of 61.40% in 2025. Dealerships segment continues to be the primary mode of selling vehicles due to their existing capabilities in vehicle financing, trade-ins, and after-sales services, making dealerships essential components of the buying process for most vehicle buyers all around the world.

Online Retail Segment is anticipated to have the highest growth rate or highest CAGR of 12.90% during the forecast period 2026-2035. The growing comfort of the customers with configuring, financing, and buying directly from the manufacturer using online retail channels through innovative methods of electric vehicle manufacturers will boost the adoption rate of online retail channels.

By Vehicle Size, Mid-Size dominated the Automotive Industry Market, while Luxury is the fastest-growing segment.

Mid-Size was the most dominant segment within the Automotive Industry Market, accounting for 38.70% of revenue share in 2025. Mid-sized cars continue to be the largest category of cars due to their good combination of space, efficiency, and cost-efficiency, which makes them the most suitable option for the largest number of user categories around the world.

The Luxury segment is projected to grow at the highest CAGR of 8.60% during the forecast period from 2026-2035. Increasing disposable income along with the middle class in developing countries, along with preference for high-end features and technology packs, has been boosting the sales of luxury cars.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.00% |

|

Europe |

Germany |

27.60% |

|

Asia Pacific |

China |

46.30% |

|

Middle East & Africa |

UAE |

25.70% |

|

Latin America |

Brazil |

37.90% |

North America Automotive Industry Market Insights

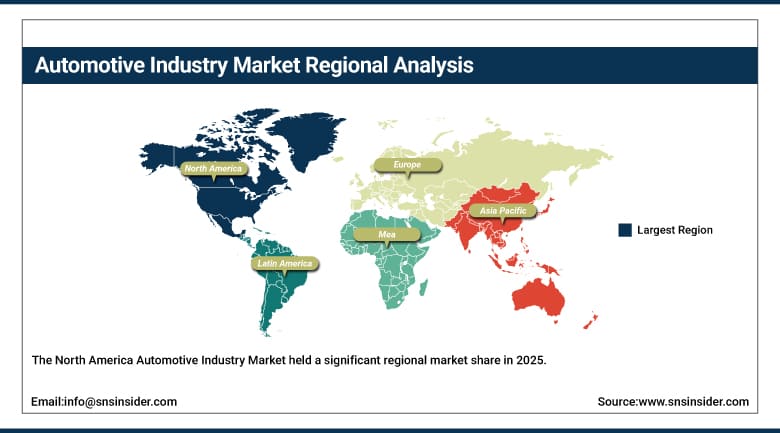

The North America Automotive Industry Market held a significant regional market share in 2025 owing to strong consumer demand for electric vehicles and advanced safety systems, robust domestic manufacturing base, and continued innovation in connected and autonomous vehicle technology.

The US was the leading country within the North America Automotive Industry Market in 2025 with a market share of 85.00% of the regional market, driven by extensive domestic vehicle manufacturing infrastructure, growing electric vehicle production investment, and strong consumer demand for advanced automotive technology. Canada is contributing to regional growth through its expanding automotive component manufacturing base.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Automotive Industry Market Insights

The Europe region was a major contributor to the Automotive Industry Market in 2025. This is attributed to stringent emissions regulations accelerating electric vehicle adoption, strong presence of leading premium automotive brands, and urban congestion policies reshaping vehicle purchasing patterns across member states.

Germany is one of the major markets in Europe owing to its dominant automotive manufacturing base and strong presence of leading automakers investing in electrification and software-defined vehicle technology. Other countries such as France, Italy, and Spain are also contributing to market growth through expanding vehicle production and rising electric vehicle adoption.

Asia Pacific Automotive Industry Market Insights

The Asia Pacific Automotive Industry Market is expected to witness the fastest growth rate during the forecast period 2026-2035. The market growth is driven by robust manufacturing potential, great consumer demand, high urbanization, and huge spending on electric vehicles and supporting infrastructure across the region's major economies.

China is one of the main growth drivers in the Asia Pacific Automotive Industry Market, owing to its dominant vehicle production base, rapidly growing domestic electric vehicle manufacturing ecosystem, and supportive government policies. India, Japan, and South Korea are also contributing to regional growth through expanding vehicle production and rising consumer demand for advanced automotive technology.

Middle East & Africa and Latin America Automotive Industry Market Insights

Middle East & Africa and Latin American regions are gradually expanding automotive industry participation as vehicle demand grows and domestic assembly investment increases across both regions. Growing regional infrastructure investment is opening meaningful avenues for market growth across these regions.

Brazil is set to be a prominent Latin American market fueled by growing domestic vehicle production and rising consumer demand for personal and commercial vehicles. The Middle East & Africa region has UAE and Saudi Arabia investing in automotive assembly and electric vehicle infrastructure as part of broader economic diversification strategies.

Growth Drivers: Rising vehicle demand and electrification driving market growth

Increasing demands for vehicles across the emerging markets, increasing usage of electric vehicles, and integration of latest technology such as electronics and connectivity technology are some of the key factors driving the market for Automotive Industry Market. The automotive industry is positioned as a highly systemically important asset class that has a pivotal role to play in the ecosystem of manufacturing and mobility.

Significant technological innovations in batteries, software-driven vehicles, and autonomous driving are major reasons for the increasing complexity and value addition in vehicles. Increasing urban congestion policies that are leading to increasing adoption of electric vehicles, increasing investments in infrastructure that lead to modernization of commercial fleets, and increasing consumer preference towards connected mobility solutions are other driving factors for the forecast period.

Restraints: Supply chain fragility and high capital requirements limiting market expansion

One of the main barriers to market growth is persistent supply chain fragility affecting semiconductor and critical mineral sourcing, which continues to expose automakers to production disruption risk despite ongoing efforts to diversify supply away from single-region dependencies.

Additionally, the enormous capital requirements associated with transitioning to electric and software-defined vehicle platforms are straining automaker balance sheets, driving industry-wide platform consolidation to fund technology roadmaps. Geopolitical uncertainty affecting trade policy and critical mineral access further introduces cost and planning uncertainty for automotive manufacturers.

Opportunities: Expansion of software-defined vehicles and emerging market demand creating new growth avenues

The significant proliferation in the software-defined vehicle architecture, the emergence of connected services and subscription-based business models, along with rising vehicle demand in the emerging economies, is projected to result in significant growth opportunities in the Automotive Industry Market. An increase in the demand for high-tech, luxury vehicles is set to aid future demand for advanced automotive platforms.

There is a significant opportunity for growth in the development of self-driving technology as well as connected mobility solutions, which lead to the creation of additional revenue streams through subscription services other than selling vehicles. The rise in vehicle demand as well as manufacturing capacity in emerging economies of Asia Pacific and Latin America can bring about significant demand during the forecast period.

Recent Developments:

-

2025: Toyota expanded its bZ series electric vehicle platform lineup, introducing additional body styles and battery configurations to broaden its electrification strategy across markets.

-

2025: BYD advanced its next-generation Blade Battery platform, offering improved energy density and safety performance for its expanding electric vehicle lineup.

-

2026: Tesla launched an updated Model Y refresh featuring enhanced range, updated interior technology, and improved manufacturing efficiency across its production facilities.

-

2026: Volkswagen introduced its new MEB+ electric vehicle platform for the compact segment, targeting improved affordability and range for mass-market electric vehicle customers.

Automotive Industry Market key players are:

-

Toyota Motor Corporation

-

Volkswagen AG

-

Stellantis N.V.

-

General Motors Company

-

Ford Motor Company

-

Hyundai Motor Company

-

Honda Motor Co., Ltd.

-

Nissan Motor Co., Ltd.

-

BMW Group

-

Mercedes-Benz Group AG

-

Tesla, Inc.

-

SAIC Motor Corporation Limited

-

BYD Company Limited

-

Suzuki Motor Corporation

-

Kia Corporation

-

Renault Group

-

Tata Motors Limited

-

Mazda Motor Corporation

-

Subaru Corporation

-

Geely Automobile Holdings Limited

Automotive Industry Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4,357.69 Billion |

| Market Size by 2035 | USD 8,508.56 Billion |

| CAGR | CAGR of 6.92% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Passenger Cars, Commercial Vehicles, Electric Vehicles, Two Wheelers) • by Fuel Type (Internal Combustion Engine, Electric, Hybrid, Hydrogen) • by Sales Channel (Dealerships, Direct Sales, Online Retail) • by Vehicle Size (Compact, Mid-Size, Full-Size, Luxury) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Toyota Motor Corporation, Volkswagen AG, Stellantis N.V., General Motors Company, Ford Motor Company, Hyundai Motor Company, Honda Motor Co., Ltd., Nissan Motor Co., Ltd., BMW Group, Mercedes-Benz Group AG, Tesla, Inc., SAIC Motor Corporation Limited, BYD Company Limited, Suzuki Motor Corporation, Kia Corporation, Renault Group, Tata Motors Limited, Mazda Motor Corporation, Subaru Corporation, Geely Automobile Holdings Limited |

Frequently Asked Questions

The Automotive Industry Market is expected to grow at a CAGR of 6.92% from 2026 to 2035.

The Automotive Industry Market was valued at USD 4,357.69 Billion in 2025.

The market is driven by rising vehicle demand across emerging economies, accelerating electric vehicle adoption, and continued integration of advanced electronics and connectivity technology.

The Internal Combustion Engine segment dominated the Automotive Industry Market in 2025, accounting for approximately 57.00% market share.

The North America region dominated the Automotive Industry Market in 2025, driven by strong consumer demand for electric vehicles and advanced safety systems.

Get in Touch