Processed & Frozen Vegetables Market Report Scope & Overview:

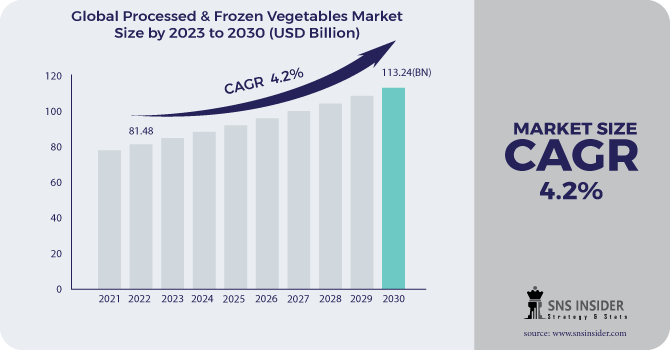

Processed & Frozen Vegetables Market Size was valued at USD 81.48 billion in 2022 and is expected to reach USD 113.24 billion by 2030, and grow at a CAGR of 4.2% over the forecast period 2023-2030.

Frozen vegetables will be vegetables protected under low temperatures and utilized over a significant stretch. These vegetables have their temperature kept up at a temperature that is beneath their edge of freezing over. This is done to make the transportation and capacity of frozen vegetables more straightforward. The strategy utilized in freezing vegetables incorporates diminishing the deterioration by transforming the additional dampness into ice, which hinders the development of microbes. Freezing helps save the essential supplements in vegetables, for example, carotenes, important to blend vitamin an in the body. Numerous economically accessible frozen vegetables are on the lookout, including prepared dinners, vegetables, and natural products, potatoes, meat and poultry, fish, and soup. They offer various benefits, which incorporate simple readiness, minimal expense, and accessibility during the slow time of year.

These kinds of vegetables are accessible in all general stores. Frozen prepared dinners further incorporate bundled prepared to-eat food varieties, pastry kitchen, bites, and treats. Also, to address the issues of the rising populace, stay away from food wastage, and keep the food organizations beneficial and serious, protection of food by freezing is taken on by different food makers. Business purchasers like inns, caterers, eateries, and cheap food chains are among significant clients of frozen food items that incorporate frozen vegetables and organic products, potatoes, and non-veg items.

Market Dynamics:

Driving Factors:

-

The rising wellbeing concerns and expanding mindfulness about the advantages of handled vegetables among purchasers across the globe.

-

The developing working-class populace, combined with expanding extra cash and urbanization across the globe.

Restraining Factors:

-

Upset transportation and suspended the inventory of vegetable items for a brief length.

Opportunities:

-

A few makers are putting resources into the combination of mechanization and advanced mechanics with handling gear, to work on the nature of the items and decrease the working expense.

Challenges:

-

A critical effect on the commodity and import of handled and frozen vegetables across the globe.

Impact of Covid-19:

The episode is antagonistically influencing economies and ventures in different nations because of lockdowns, travel boycotts, and business closures. The worldwide food handling industry is one of the significant businesses that are experiencing significant disturbances, for example, industrial facilities closure, inventory network breaks, innovation occasions scratch-offs, and office closures. The closing down of processing plants, and hardware, and the startling separation of production network or dispersion network is further affecting the development of the frozen vegetable market.

Market Estimation:

The disconnected channel contributed a portion of practically 78% of the worldwide handled and frozen vegetable market in 2021. Customers are favoring the disconnected channel for buying purchaser merchandise, food, as well as handling food items, where they can confirm the item quality. The web-based portion of the handled and frozen vegetable industry is expected to enlist the quickest from 2022 to 2028. The web entrance rate has seen rewarding development lately, which has prompted the huge development of the internet business area across the globe.

The canned item section added to the biggest income share in the worldwide market for handled and frozen vegetables in 2021. The rising notoriety of canned items is ready to drive development in the estimated period. The frozen portion is supposed to progress at the quickest development rate. Frozen vegetables are helpful, nutritious, and sound, and are made accessible to buyers through retail channels. Also, the developing fame and interest for frozen food, combined with the rising extra cash of the buyers, are huge variables of the market development.

Key Market Segmentation:

By Nature:

-

Organic

-

Conventional

By Product Type:

-

Beans

-

Peas

-

Corn and Baby Corn

-

Broccoli and Cauliflower

-

Potatoes

-

Onions

-

Tomatoes

-

Carrots

-

Spinach

-

Others

By Distribution Channel:

-

Business to Business (Foodservice)

-

Business to Consumer

-

Hypermarkets/Supermarkets

-

Convenience stores

-

Specialty Stores

-

Online Retail

.png)

Regional Analysis:

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

In light of geology, the worldwide Frozen vegetable market is bifurcated into North America, Europe, Asia Pacific, and the Rest of the world. The North American and European districts held the biggest portion of the overall industry of the frozen vegetable market. The presence of numerous general stores and a better foundation for the capacity of frozen items are set to drive market development. In any case, the Asia Pacific area is assessed to develop at a higher CAGR because of the rising populace, expanding dispensable salaries, and expanded inclination for frozen vegetables in everyday food among buyers in China and India.

Key Players:

The "Worldwide Frozen Vegetables Market" concentrate on the report will give significant knowledge stressing the worldwide market. The key part of the market is General Mills Inc., Nestle, Kellogg Co., B&G Foods, Inc., Aryzta AG, Flowers Foods, Iceland Foods Ltd., Amy’s Kitchen, Inc., Nature’s Garden, Foodnet Ltd., Cascadian Farm Organic, and The Kraft Heinz Company.

Foodnet Ltd-Company Financial Analysis

| Report Attributes | Details |

|---|---|

| Market Size in 2022 | US$ 81.48 Billion |

| Market Size by 2030 | US$ 113.24 Billion |

| CAGR | CAGR 4.2% From 2023 to 2030 |

| Base Year | 2022 |

| Forecast Period | 2023-2030 |

| Historical Data | 2020-2021 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Asparagus, Broccoli, Green Peas, Mushrooms, Spinach, Corn, Green Beans, and Others) • by End-User (Food Service Industry and Retail Customers) • by Distribution Channel (Discounters, Supermarkets/Hypermarkets, and Others) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, +D11UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | General Mills Inc., Nestle, Kellogg Co., B&G Foods, Inc., Aryzta AG, Flowers Foods, Iceland Foods Ltd., Amy’s Kitchen, Inc., Nature’s Garden, Foodnet Ltd., Cascadian Farm Organic, and The Kraft Heinz Company. |

| Key Drivers | •The developing working-class populace, combined with expanding extra cash and urbanization across the globe. |

| Market Challenges: | •A critical effect on the commodity and import of handled and frozen vegetables across the globe. |

Frequently Asked Questions

Ans: The Global Processed & Frozen Vegetables Market Size was valued at USD 78.2 billion in 2021

Ans: Manufacturers, Research Institutes, university libraries, suppliers, and distributors of the product.

Ans: Nature, Product Type, and Distribution Channel segments are covered in the Processed & Frozen Vegetables Market

Ans: The rising wellbeing concerns and expanding mindfulness about the advantages of handled vegetables among purchasers across the globe. A few makers are putting resources into the combination of mechanization are the elements driving and resulting in opportunities for the Processed & Frozen vegetable market.

Ans: Online retail segment is projected to make a foothold in the worldwide Processed & Frozen vegetable market.

Get in Touch