Protective Coatings Market Report Scope & Overview:

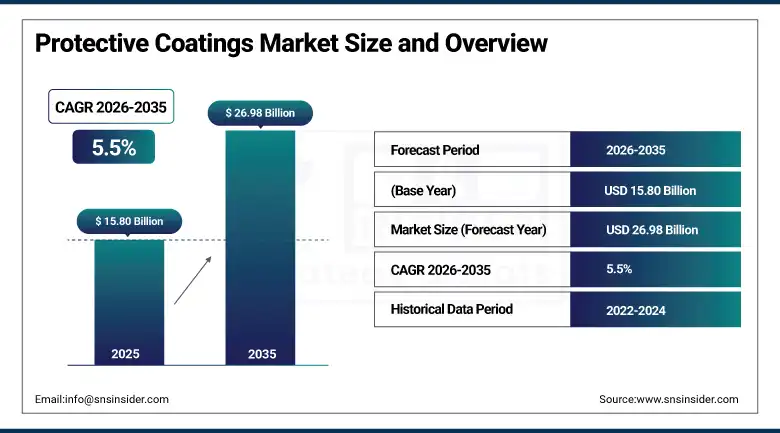

The Protective Coatings Market was valued at USD 15.80 Billion in 2025 and is expected to reach USD 26.98 Billion by 2035, growing at a CAGR of 5.5% from 2026–2035.

The Protective Coatings Market is witnessing steady growth because of the growing demand for corrosion resistance and durability from the construction industry, marine industry, oil and gas industry, and power generation industry. Fast-paced infrastructural developments and urbanization have resulted in increased demand for protective coatings. Moreover, there have been developments in offshore structures and petrochemical plants, which have augmented the demand for protective coatings. Besides, the stringent environmental laws have prompted the adoption of low VOC and water-borne coatings. Advances in high performance resin technologies have improved efficiency.

According to the World Bank, global infrastructure investment needs are estimated at trillions of dollars annually through 2030–2040, driven by urbanization and industrial expansion, which significantly supports demand for protective coatings in large-scale construction and industrial projects. According to the World Steel Association, global crude steel production exceeds 1.8 billion tonnes annually, and steel corrosion protection remains a major application driver, reinforcing strong demand for protective coating solutions across industrial and infrastructure sectors.

Protective Coatings Market Size and Forecast

-

Market Size in 2026E: USD 16.67 Billion

-

Market Size by 2035: USD 26.98 Billion

-

CAGR: 5.5% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Protective Coatings Market - Request Free Sample Report

Protective Coatings Market Trends

-

Nano-coating technology is providing ultra-thin, high-performance protective layers for aerospace, automotive, and industrial product applications.

-

Self-healing coatings filled with sol-gel microcapsules are autonomously repairing minor scratches, reducing service costs and downtime.

-

UV-cured coating adoption is accelerating due to low environmental impact and fast curing time meeting strict emission standards.

-

Waterborne and powder coating transition is responding to regulatory pressure for lower VOC emissions across major markets.

-

Heat-flex corrosion-under-insulation mitigation coatings are addressing critical infrastructure protection challenges in oil and gas applications.

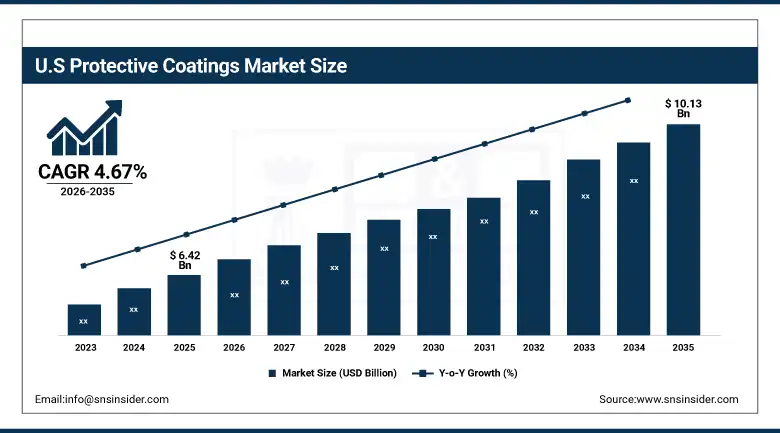

The U.S. Protective Coatings Market Outlook

The U.S. Protective Coatings Market was valued at USD 6.42 Billion in 2025 and is expected to reach USD 10.13 Billion by 2035, growing at a CAGR of 4.67% from 2026–2035.

The United States leads North American protective coatings revenues through the Inflation Reduction Act’s USD 369 billion funding over ten years promoting clean energy and emission reduction, significantly boosting infrastructure for renewable energy production and transmission requiring corrosion protection. PPG Industries, The Sherwin-Williams Company, and Dow sustain U.S. market leadership through their comprehensive protective coating portfolios serving construction, marine, and industrial end markets.

According to the U.S. Department of Transportation, the United States has over 600,000 bridges, many requiring corrosion protection and maintenance coatings, significantly supporting demand for protective coating solutions in infrastructure maintenance.

Protective Coatings Market Segment Analysis

-

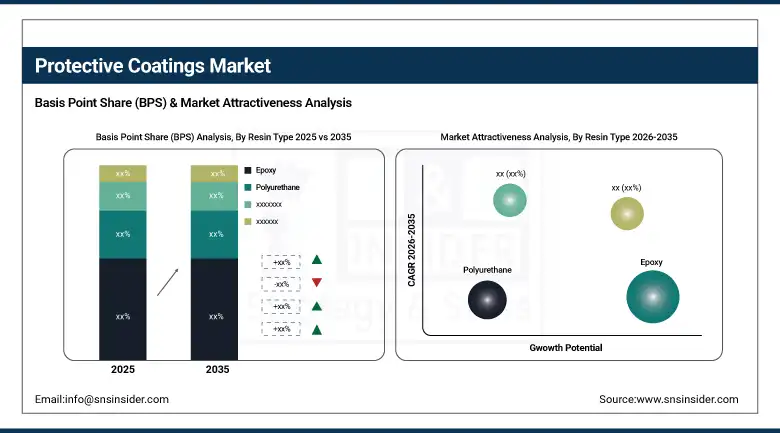

By Resin Type, Epoxy segment dominated the Protective Coatings Market in 2025 with 38% share; Polyurethane segment is the fastest growing segment.

-

By Technology, Solvent Based segment dominated the market in 2025 with 48% share; Water Based segment is the fastest growing segment.

-

By Application, Construction segment dominated the market in 2025 with 40% share; Oil & Gas segment is the fastest growing segment.

-

By End-Use Industry, Civil Building & Infrastructure segment dominated the market in 2025 with 42% share; Offshore Structures segment is the fastest growing segment.

By Resin Type, epoxy resin segment dominates the protective coatings market, while polyurethane segment is the fastest-growing segment

Epoxy resin dominated the Protective Coatings Market in 2025 because of the better property of adhesion and corrosion resistance, besides being durable under severe conditions. It has been extensively used in construction, marine, and industrial applications, where there is a need for long-term protection of the surface area. Chemical resistance, coupled with resistance to moisture, temperature, and physical stress, makes epoxy resin highly reliable. The extensive application of epoxy resin in infrastructure and industrial maintenance projects helps it dominate the global protective coating applications.

Polyurethane is the fastest growing segment due to their flexible nature, UV-resistance characteristics, and protective properties that last for a long time. They are gaining popularity in applications in the automotive, oil & gas, and infrastructure sectors owing to high-performing coating needs in these industries. Increasing demands for protective coating materials that are weather resistant and energy efficient are adding momentum to the growth of polyurethane coatings in the global protective coatings market.

By Technology, solvent-based coatings segment dominates the protective coatings market, while water-based coatings segment is the fastest-growing segment

Solvent-based coatings dominated the market in 2025 due to their excellent adhesion, drying capacity, and high-performance abilities in adverse conditions. These coatings are extensively used in the construction and heavy-duty industries. The ability of solvent-based coatings to withstand harsh weather conditions and chemical resistance makes them suitable for long-term use. Existing and widespread usage in industries has been aiding its dominance in the protective coatings market.

Water-based coatings are the fastest growing segment due to stringent environmental regulations and preference for VOC-free options. Water-based coatings exhibit better safety and performance than solvent-based coatings. Increased awareness regarding green buildings and sustainability in the construction industry is boosting the application of water-based coatings. Advancements in the field of technology are enhancing performance characteristics and durability of water-based coatings.

By Application, construction segment dominates the protective coatings market, while oil & gas segment is the fastest-growing segment

The Construction segment dominated the Protective Coatings Market in 2025 owing to extensive use of protective coatings for corrosion resistance, waterproofing, and durability in construction projects. Protective coatings play an integral part in protecting bridges, roadways, commercial buildings, and residential structures. Rapid urbanization and developments in infrastructure along with maintenance of existing constructions are some of the major factors that have contributed to the leading position of this application.

The Oil & Gas segment is the fastest growing because of rising investments in exploration, drilling, and pipelining efforts. Protective coatings play an important role in avoiding corrosion as well as ensuring safety in challenging offshore and onshore conditions. Higher energy consumption and the development of deep-water projects have led to their increased use. The effectiveness of protective coatings in extending asset life and reducing maintenance expenses has boosted growth in this sector.

By End-Use Industry, civil building & infrastructure segment dominates the protective coatings market, while offshore structures segment is the fastest-growing segment

Civil building and infrastructure dominated the Protective Coatings Market in 2025 due to extensive constructions and maintenance of infrastructural buildings. Protective coatings are used extensively on bridges, tunnels, buildings, and utilities in order to increase their lifespan and provide protection against environmental wear and tear. The need for urban development coupled with heavy investment by governments in constructing infrastructure is the primary growth driver.

Offshore structures are the fastest growing segment due to rapid developments in marine oil and gas operations. Protective coatings have an extremely important role in protecting the structures from salt corrosion, and this is expected to lead to growth opportunities for protective coatings market players. The increasing number of offshore wind energy and offshore drilling projects is driving the demand further.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

48.6% |

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Middle East & Africa |

Saudi Arabia |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Protective Coatings Market Insights

North America is a significant protective coatings market where the Inflation Reduction Act’s substantial clean energy infrastructure funding and the broader oil and gas, marine, and construction sectors’ corrosion protection requirements sustain regional demand. The United States accounts for approximately 82.5% of North American revenues through PPG Industries, The Sherwin-Williams Company, and Dow’s comprehensive protective coating manufacturing and distribution infrastructure.

According to the U.S. Energy Information Administration, the U.S. operates one of the largest oil refining capacities globally, requiring extensive protective coatings for pipelines, storage tanks, and refinery infrastructure, further driving market growth in the energy and industrial sectors.

Canada contributes supplementary North American revenues through its oil and gas sector’s pipeline and infrastructure protection requirements, the growing renewable energy infrastructure investment creating corrosion protection demand, and its construction sector’s consistent protective coating specification across residential and commercial building projects.

Europe Protective Coatings Market Insights

Europe is a significant protective coatings market where rigorous emission standards driving waterborne and powder coating adoption, the established petrochemical and marine industries’ corrosion protection requirements, and growing renewable energy infrastructure investment collectively sustain regional demand. Germany accounts for approximately 22.4% of European revenues through its large industrial and construction sectors and Wacker Chemie’s domestic coating manufacturing presence.

According to the European Environment Agency, industrial emissions reduction policies are accelerating the adoption of low-VOC and sustainable coating technologies across Europe, supporting the shift toward environmentally compliant protective coating solutions.

According to Eurostat, manufacturing contributes approximately 15–16% of EU GDP, reinforcing steady demand for industrial coatings across production facilities, infrastructure, and heavy industries.

Offshore energy development in the North Sea exceeds 35 GW of installed wind capacity, requiring long-term corrosion protection for subsea structures, turbines, and offshore platforms exposed to harsh marine environments.

The United Kingdom’s infrastructure investment programmes and France’s industrial and marine sectors collectively sustain European protective coatings market development despite these energy cost headwinds.

Asia Pacific Protective Coatings Market Insights

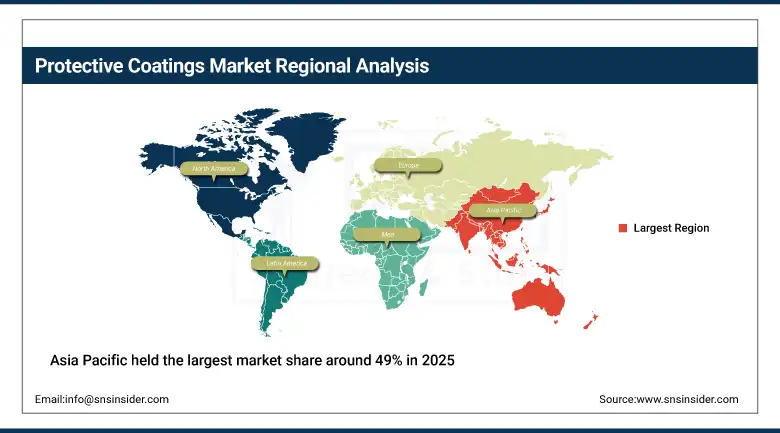

Asia Pacific held the largest market share around 49% in 2025. Asia Pacific, with its rapid industrialisation, infrastructure development, and expanding high-performance coatings demand across industries, drives market growth, primarily driven by large-scale construction projects, manufacturing activities, and automotive production in countries such as China, India, Japan, and South Korea. China accounts for approximately 48.6% of Asia Pacific revenues through its massive infrastructure construction programme and growing middle-class population increasing demand for residential, commercial, and industrial construction.

According to the World Bank, Asia accounts for over 50% of global construction activity, driving large-scale demand for protective coatings used in infrastructure, commercial buildings, and industrial projects.

According to the United Nations Industrial Development Organization, Asia produces over 50% of global manufacturing output, requiring extensive corrosion protection systems across industrial equipment, plants, and heavy machinery.

In Japan and South Korea, automotive and electronics are significant end-use industries driving these coatings due to requirements for durable, weather-resistant, and environmentally-resistant products. Government programmes including India’s Smart Cities Mission to develop modernised urban infrastructure and China’s focus on industrial development have been supportive of protective coating introduction, with increasing adoption of sustainable and green coating solutions as environmental regulations become stringent propelling investment in advanced coating technologies.

The shipbuilding industry is highly concentrated, with China, South Korea, and Japan collectively accounting for over 85% of global shipbuilding output, significantly increasing demand for marine protective coatings used in vessels and offshore structures.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Protective Coatings Market Insights

Saudi Arabia leads MEA revenues at approximately 22.8% through its large petrochemical and oil and gas infrastructure requiring extensive corrosion protection, alongside growing construction sector investment under Vision 2030 diversification initiatives. The UAE’s construction boom and growing marine infrastructure create expanding regional demand for protective coating applications.

Brazil leads Latin American revenues at approximately 43.8% through its large construction sector’s infrastructure protection requirements and growing oil and gas sector’s pipeline and offshore structure coating demand. Mexico and Argentina contribute growing secondary regional demand through their expanding construction and industrial sectors.

Market Dynamics

Growth Drivers: Infrastructure investment and coating longevity emphasis sustaining structural protective coating demand growth

Increasing demand for protective coatings from the infrastructure and construction industry across the globe is a major factor contributing to market growth, with growing urbanisation and rising demand for concrete structures to be tough and long-lasting increasing demand for high-performance coatings. A major factor driving the protective coatings market is the rising emphasis on extending the durability and stability of coatings, with today’s protective coatings designed to resist the most severe environmental conditions including extreme temperatures, humidity, and UV exposure, thereby improving structure or equipment durability.

Technological advancements, including cutting-edge epoxy coatings, have been basic components in growing the life expectancy of key assets, especially important in industries such as oil and gas where equipment faces heavy environmental stresses. Long-lasting materials imply less maintenance and repairs, translating into cost savings for construction, automotive, and marine industries, with regulatory readiness in line with ASTM International and ISO standards on durability and performance supporting adoption of advanced formulations.

Restraints: High raw material and energy costs creating margin pressure on protective coating manufacturers

High prices of raw materials and energy sources are major restraints to the growth of the protective coatings market. Prices of crucial raw materials, including resins, pigments, and additives, have increased owing to supply chain disruptions, geopolitical conflicts, and rising demand for these materials in other industrial processes, with the cost of epoxy resins and titanium dioxide, two base raw materials used in protective coatings, having skyrocketed and applied margin pressure on manufacturers.

The production processes for coatings are very energy-hungry, with production costs driven higher still by increasing energy costs especially in heavy fossil fuel-dependent locations. This challenge is exacerbated in Europe, with increased energy prices resulting from lower gas imports as well as the energy transition, creating regional cost disadvantages that European coating manufacturers must navigate relative to producers in lower-energy-cost markets.

Opportunities: Advanced coating technology adoption and emerging market infrastructure investment creating premium growth categories

The adoption of advanced coating technologies is a key trend fuelling expansion of the protective coatings market, with novel technologies like nano-coatings, self-healing coatings, and UV-cured coatings disrupting the sector by providing unprecedented levels of protection and performance. Nano-coatings offer ultra-thin, high-performance superimposed layers projected particularly in the fields of aerospace, automotive, and consumer products, while self-repairing paints filled with microcapsules of sol-gel material autonomously heal small scratches, reducing service costs and downtime.

The growing global trend of strict environmental regulation has increased the adoption of UV-cured coatings due to their low environmental impact and fast curing time, with these technologies being adopted more quickly than ever in part due to growing emphasis on sustainability and energy efficiency. Government infrastructure programmes including China’s Belt and Road Initiative and India’s Smart Cities Mission create substantial new construction activity whose protective coating specification requirements sustain above-baseline market growth in rapidly developing economies.

Recent Developments:

-

2025: Evonik launched a new leveling agent under the name TEGO Flow 380 designed especially for high-grade automotive clear coats, characterised by better anti-pop characteristics and wider compatibility for automotive and general industrial coating applications.

-

2025: Akzo Nobel announced a new super-durable Interpon D powder coating giving aluminium surfaces the natural look and feel of stone without the challenges and costs of the actual material, with the launch focused on the Indian market for designers and architects.

-

2025: The Sherwin-Williams Company released heat-flex corrosion-under-insulation mitigation coatings, described by the company as the most effective formulation currently offered on the market for combating corrosion below insulation in industrial settings.

Protective Coatings Market Key Players are:

-

AkzoNobel N.V.

-

PPG Industries, Inc.

-

The Sherwin-Williams Company

-

Jotun Group

-

Hempel A/S

-

RPM International Inc.

-

Axalta Coating Systems

-

BASF Coatings GmbH

-

Kansai Paint Co., Ltd.

-

Nippon Paint Holdings Co., Ltd.

-

Asian Paints Limited

-

Berger Paints India Limited

-

Teknos Group

-

Tikkurila Oyj

-

Sika AG

-

3M Coatings Division

-

Carboline Company

-

Chugoku Marine Paints, Ltd.

-

DAW SE (Caparol)

-

Wacker Chemie AG

Protective Coatings Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.80 Billion |

| Market Size by 2035 | USD 26.98 Billion |

| CAGR | CAGR of 5.5% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Resin Type (Epoxy, Polyurethane, Acrylic, Alkyd, Zinc, Others) • By Technology (Solvent Based, Water Based, Powder Coatings, Others) • By Application (Construction, Marine, Oil & Gas, Power Generation, Others) • By End-Use Industry (Offshore Structures, Petrochemical, Civil Building & Infrastructure, Water & Wastewater Treatment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AkzoNobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Jotun Group, Hempel A/S, RPM International Inc., Axalta Coating Systems, BASF Coatings GmbH, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, Berger Paints India Limited, Teknos Group, Tikkurila Oyj, Sika AG, 3M Coatings Division, Carboline Company, Chugoku Marine Paints, Ltd., DAW SE (Caparol), Wacker Chemie AG |

Frequently Asked Questions

The Protective Coatings Market is expected to grow at a CAGR of 5.5% from 2026 to 2035.

The Protective Coatings Market was valued at USD 15.80 Billion in 2025.

Infrastructure growth, coating durability demand, advanced technologies, and government infrastructure programs drive Protective Coatings Market expansion globally.

Epoxy resin held the largest market in 2025.

Asia Pacific held the largest market share around 49% in 2025.

Get in Touch