Epoxy Resins Market Report Scope & Overview:

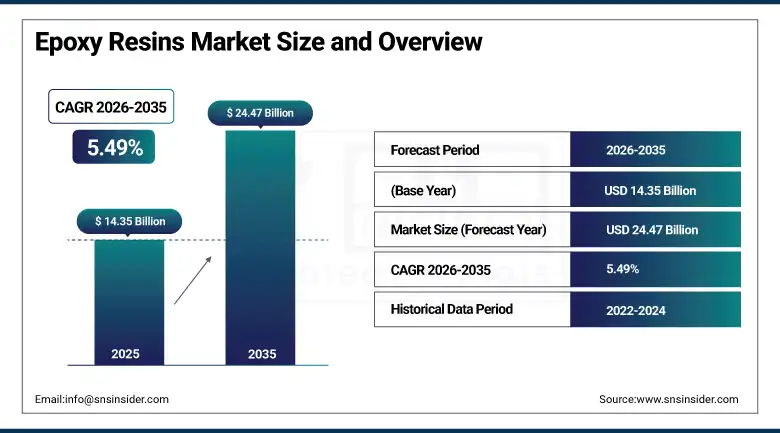

The Epoxy Resins Market was valued at USD 14.35 Billion in 2025 and is expected to reach USD 24.47 Billion by 2035, growing at a CAGR of 5.49% from 2026–2035.

The Epoxy Resins Market is growing steadily due to the rise in demand from various industry sectors including construction, automotive, aerospace, and wind energy. Epoxy resins are highly demanded in applications such as coatings, adhesives, sealants, and composite materials due to their high mechanical strength, excellent chemical resistance, and durability properties. The increasing need for infrastructure development and composite material utilization in vehicles has propelled market growth. Renewable energy projects that are rapidly growing have increased the use of epoxy resins for manufacturing composite materials.

According to the International Energy Agency (IEA), global renewable electricity capacity additions reached a record approximately 700 GW in 2024, with solar and wind accounting for the majority of new installations. Wind turbine blades extensively utilize epoxy resin-based composites due to their exceptional strength-to-weight ratio and durability. Furthermore, the United Nations Environment Programme (UNEP) reports that the buildings and construction sector accounts for around 34% of global energy demand, encouraging continued investments in infrastructure, protective coatings, adhesives, and flooring systems that rely on epoxy resins.

Epoxy Resins Market Size and Forecast

-

Market Size in 2026E: USD 15.14 Billion

-

Market Size by 2035: USD 24.47 Billion

-

CAGR: 5.49% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Epoxy Resins Market - Request Free Sample Report

Epoxy Resins Market Trends

-

Rising demand from construction and infrastructure sectors driving the use of epoxy resins in adhesives, coatings, flooring, and structural applications

-

Growing adoption in wind energy applications for manufacturing lightweight and high-strength composite components such as turbine blades

-

Increasing use in automotive and aerospace industries to support lightweighting initiatives and improve mechanical performance and durability

-

Expanding demand for protective coatings with superior corrosion resistance, chemical stability, and long service life across industrial environments

-

Continuous advancements in bio-based and low-VOC epoxy resin formulations supporting sustainability goals and environmental compliance requirements

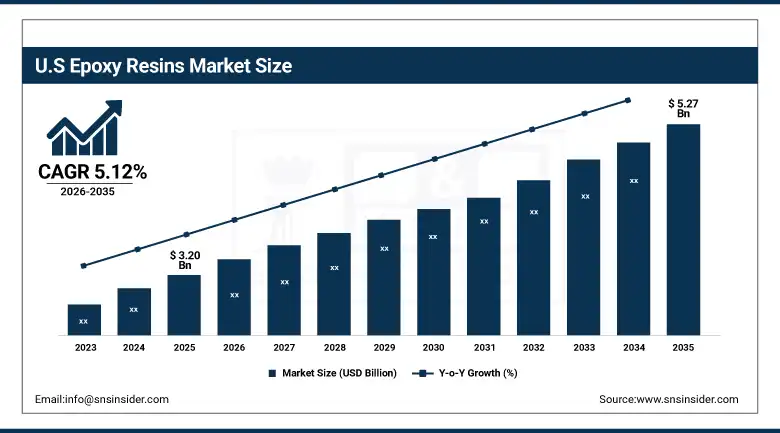

U.S. Epoxy Resins Market Outlook

The U.S. Epoxy Resins Market was valued at USD 3.20 Billion in 2025 and is expected to reach USD 5.27 Billion by 2035, growing at a CAGR of 5.12% from 2026–2035.

The U.S. Epoxy Resins Market is one of the most commercially sophisticated national epoxy resin markets globally. Hexion, Olin Corporation, Huntsman Advanced Materials, Momentive Performance Materials, and DIC Corporation’s U.S. operations collectively define the domestic commercial landscape. The wind energy sector’s IRA-incentivised expansion creates above-average turbine blade composite epoxy demand, the automotive sector’s EV platform transition creates composite and adhesive epoxy procurement, and the construction sector’s infrastructure investment creates protective coating and flooring epoxy application demand that collectively sustain consistent above-average U.S. market engagement.

According to the U.S. Census Bureau, annual construction spending exceeded USD 2.1 trillion in 2025, supporting robust demand for epoxy coatings, flooring systems, adhesives, and structural composites used in commercial, residential, and infrastructure projects.

Epoxy Resins Market Segment Analysis

-

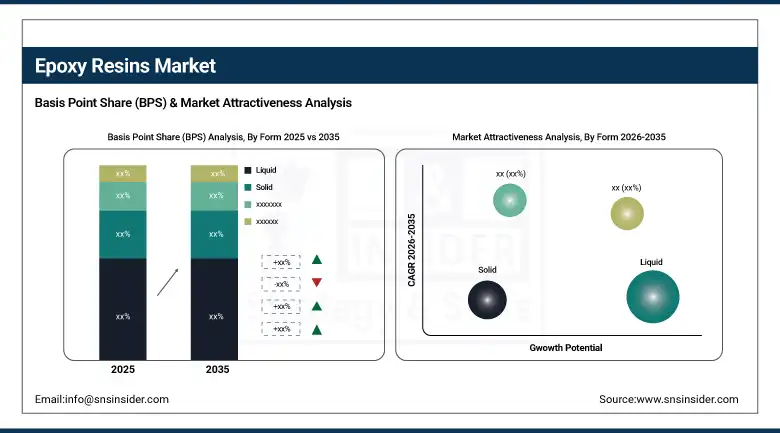

By Form, liquid segment dominated the Epoxy Resins Market in 2025 with 58% share; solution segment is the fastest growing segment.

-

By Raw Materials, DGBEA segment dominated the market in 2025 with 47% share; amine segment is the fastest growing segment.

-

By Application, paints & coatings segment dominated the market in 2025 with 39% share; composites segment is the fastest growing segment.

-

By End-User, building & construction segment dominated the market in 2025 with 31% share; wind energy segment is the fastest growing segment.

By Form, liquid segment dominates the epoxy resins market, while solution segment is the fastest-growing segment

The liquid segment dominated the Epoxy Resins Market in 2025 with 58% share due to their diverse applications in coatings, adhesives, composites, and electrical industry. The liquid epoxy resins segment has been favored by its superior ability in processing, good adhesion, great chemical resistance, and ease of formulating. The ability of liquid epoxy resins to combine with different types of curing agents and production methods makes the segment ideal for large-scale commercial uses. Demand for the segment from the construction, automotive, marine, and protective coatings industries is another factor that has favored its growth.

The solution segment is the fastest growing due to rising demand for advanced coatings and formulations in the coming years. The solution epoxy resins offer better properties such as improved formulation capability and surface coverage. Increasing expenditure in infrastructure development, industrial maintenance, and corrosion protection activities is one reason behind the segment's rapid growth. Preference for specialty coatings among manufacturers in the automotive, aerospace, and manufacturing industries will continue fueling its growth.

By Raw Materials, DGBEA segment dominates the epoxy resins market, while amine segment is the fastest-growing segment

The DGBEA segment dominated the Epoxy Resins Market in 2025 with 47% share because of its wide usage in the development of multi-purpose epoxy resins used in coating, adhesives, laminating, and composite manufacturing processes. These resins are known for their good mechanical strength, chemical resistance, durability, and adhesive properties. Due to their cost-effectiveness and established production system, these resins have achieved extensive market success. Continuous demand from construction, electronics, transportation, and industries further cemented its lead among the other segments.

The amine segment is the fastest growing as there is an increased demand for improved curing agents, which improves the properties of the epoxy resins. The amine curing agents not only improve the properties of the epoxy resin but can also improve the strength, thermal stability, and curing process. With increased application of such materials in the aerospace industry, wind energy sector, transportation, and coating industry, this growth has been propelled by rising demands.

By Application, paints & coatings segment dominates the epoxy resins market with a 39% share, while composites segment is the fastest-growing segment.

The paints & coatings segment dominated the Epoxy Resins Market in 2025 with 39% share since these resins are extensively utilized in applications such as surface protection, increased durability, and improved surface characteristics. The good adhesion properties, chemical and moisture resistance, and mechanical strength of epoxy resins make them an ideal choice for industrial, marine, automotive, and infrastructural paints and coatings. Increasing investment in construction and industrial maintenance works continues to drive demand.

The composites segment is the fastest growing due to the increasing demand for lightweight and durable materials. Epoxy resins help in providing improved mechanical strength, durability, and environmental stress resistance to various products. They can be used in aerospace, automotive, marine, and renewable energy industries. The growing demand for lightweight and energy-efficient solutions is driving market growth. Growing demand for composites in next generation engineering projects is further propelling growth in the market.

By End-User, building & construction segment dominates the epoxy resins market with a 31% share, while wind energy segment is the fastest-growing segment

The building & construction segment dominated the Epoxy Resins Market in 2025 with 31% share due to increased applications in the field of coating, adhesives, floorings, sealing, and structural uses. The unique features of epoxy resins such as durability, chemical resistance, mechanical strength, and longevity make these products highly compatible for both commercial, residential, and industrial construction projects. Moreover, growing infrastructure development and building refurbishment trends fuel the demand further.

The wind energy segment is the fastest growing due to the increasing trend of investing in alternative power generation sources across the globe along with the installation of more wind turbines. Turbine blades consist of epoxy resins since these products offer high strength, lightness, and superior fatigue resistance. Demand for bigger and better wind turbines encourages higher utilization of advanced composites.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Epoxy Resins Market Insights

North America is a technically sophisticated epoxy resins market where Hexion, Olin Corporation, Huntsman Advanced Materials, and Momentive Performance Materials’ commercial operations define the domestic supply landscape. The United States accounts for approximately 87.4% of North American revenues through its wind energy expansion, automotive EV transition, aerospace composite production, and construction sector’s coating and adhesive demand.

U.S. Department of Energy (DOE) reported that national wind power capacity surpassed 150 GW, driving significant consumption of epoxy-based composite materials for wind turbine blades. Furthermore, the Federal Aviation Administration (FAA) highlights ongoing fleet modernization initiatives across the commercial aviation sector, increasing the adoption of lightweight composite materials in aircraft structures, where high-performance epoxy resins play a critical role in enhancing strength, durability, and fuel efficiency.

Canada contributes approximately 12.6% of North American revenues through its wind energy installation programme, the automotive manufacturing sector’s composite demand, and the construction industry’s epoxy coating application investment.

Europe Epoxy Resins Market Insights

Europe is a technically sophisticated epoxy resins market where the offshore wind energy expansion, aerospace composite manufacturing, and the automotive sector’s lightweight material specification create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive sector’s composite and adhesive procurement, the wind energy manufacturing sector’s turbine blade resin demand, and Hexion and Huntsman’s European commercial operations.

According to the European Commission, more than EUR 584 billion is being mobilized through REPowerEU and related energy-transition initiatives, supporting wind energy projects and industrial infrastructure developments that utilize epoxy composites and protective coatings. Furthermore, WindEurope reported that Europe installed approximately 16.4 GW of new wind power capacity in 2024, creating significant demand for epoxy resin-based composite materials used in turbine blade manufacturing.

In addition, Eurostat estimates that the European Union’s construction sector generates over EUR 1.5 trillion annually, making it a major consumer of epoxy flooring systems, coatings, adhesives, and structural materials. These large-scale investments and industrial activities continue to strengthen demand for epoxy resins across the region.

Denmark, the Netherlands, and the United Kingdom are significant secondary markets where the offshore wind energy industry’s turbine blade manufacturing creates above-average epoxy composite demand that compounds with Europe’s extraordinary North Sea offshore wind programme expansion.

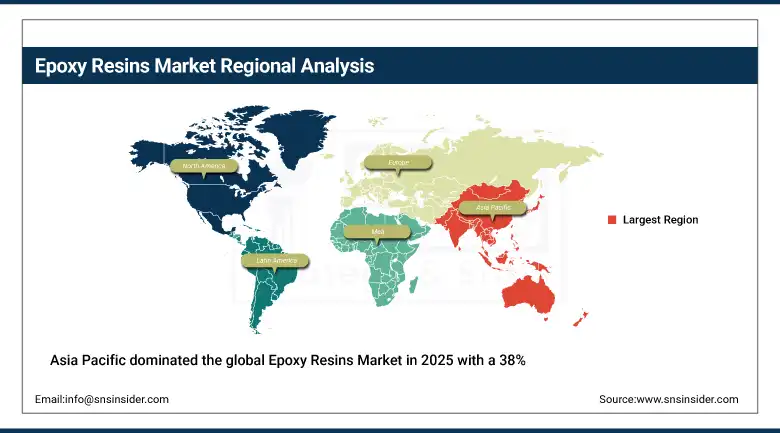

Asia Pacific Epoxy Resins Market Insights

Asia Pacific dominated the global Epoxy Resins Market in 2025 with a 38% market share, driven by China’s extraordinary manufacturing scale across electronics, construction, and wind energy, Japan’s specialty epoxy chemical leadership, South Korea’s electronics and EV manufacturing demand, and Southeast Asia’s growing industrial base. China accounts for approximately 44.8% of Asia Pacific revenues through its position as both the largest epoxy resin producer and consumer, supported by extensive wind turbine blade manufacturing and strong demand for coatings and adhesives from the construction sector.

According to the National Bureau of Statistics of China, the country’s construction industry generates output exceeding CNY 31 trillion annually, making it one of the world’s largest consumers of epoxy coatings, adhesives, flooring systems, and structural materials. Additionally, the Global Wind Energy Council (GWEC) reported that China installed approximately 80 GW of new wind power capacity in 2024, the highest globally, creating substantial demand for epoxy resin-based composites used in wind turbine blades.

Furthermore, India’s Ministry of New and Renewable Energy (MNRE) reported renewable energy capacity exceeding 220 GW, supporting increased utilization of epoxy-based components in wind energy infrastructure.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Epoxy Resins Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its petrochemical complex’s industrial protective coating demand, SABIC’s specialty chemical manufacturing, and the Vision 2030 construction sector’s growing epoxy flooring and adhesive application. Brazil leads Latin American revenues at approximately 44.2% through its growing onshore wind energy turbine blade composite demand, the construction sector’s coating and adhesive procurement, and the automotive manufacturing sector’s epoxy composite investment. UAE’s extraordinary construction sector and South Africa’s industrial maintenance coating demand collectively sustain growing regional market development through 2035.

Market Dynamics

Growth Drivers: Wind energy expansion and EV composite adoption creating above-average structural demand

Global wind energy capacity expansion is the epoxy resins market’s most commercially transformative near-term growth driver. The IEA’s Net Zero 2050 scenario’s requirement for 7,300 GW of cumulative wind capacity by 2030 creates epoxy composite demand at commercial scale whose per-turbine resin consumption growth with rotor diameter creates a demand trajectory that compounds both with installation volume and turbine size progression. Each new offshore wind farm commissioning whose turbine count creates tens of thousands of tonnes of epoxy blade resin procurement sustains wind energy’s fastest-growing end-user status.

Electric vehicle structural composite adoption creates growing automotive epoxy demand as battery enclosure, underbody reinforcement, and crash structure composite specification create per-vehicle epoxy content that substantially exceeds ICE vehicle equivalents. Each EV platform that specifies structural composite creates epoxy procurement whose aggregate across global EV production volume growth creates above-average automotive sector demand that compounds with EV market penetration.

Restraints: BPA regulatory pressure and raw material price volatility

Bisphenol-A regulatory pressure across EU REACH, California Proposition 65, and emerging Asian chemical safety frameworks creates specification migration concern for DGEBA epoxy resins whose BPA-derived chemistry creates endocrine disruption regulatory classification risk. Each regulatory action restricting BPA in consumer-contact applications creates reformulation investment motivation whose commercial impact sustains bio-based and BPA-free epoxy development investment.

Epichlorohydrin raw material price volatility, whose propylene feedstock dependence creates price cycles that directly impact epoxy resin production economics, creates margin uncertainty that limits producer investment pace during high-feedstock-cost periods.

Opportunities: Bio-based epoxy development and offshore wind turbine blade composite

Bio-based epoxy resin development from plant-derived cardanol, furfuryl alcohol, and bio-epichlorohydrin represents the most commercially premium sustainability opportunity whose reduced fossil feedstock dependence creates specification preference in green building certification, sustainable procurement, and renewable energy supply chain applications whose corporate sustainability commitment creates above-commodity procurement motivation.

Offshore wind turbine blade composite represents the most commercially certain near-term volume growth opportunity whose per-blade resin consumption exceeding 20 tonnes creates extraordinary aggregate demand from each offshore wind farm’s turbine count whose commercial procurement compounds with offshore wind installation acceleration.

Recent Developments:

-

2024: Hexion launched its next-generation EPON Resin series for wind turbine blade composite applications in 2024 with enhanced toughness, improved elongation-at-break, and faster glass fibre wet-out for vacuum-assisted resin infusion manufacturing of increasingly large rotor blade structures.

-

2024: Huntsman Advanced Materials launched its new Araldite LY 3585/Aradur 3487 epoxy system in 2024 targeting fast-cure offshore wind blade manufacturing processes enabling cycle time reduction from conventional 8-hour cure to below 4-hour demould in optimised production cell conditions.

-

2024: Olin Corporation expanded its epoxy resin production capacity at its Freeport, Texas facility in 2024 through debottlenecking investment that increased liquid epoxy resin output capacity targeting the growing wind energy composite and construction sector demand in North America.

-

2023: Olin Corporation launched its D.E.R. 383 liquid epoxy resin with reduced viscosity for wind energy composite infusion applications in 2023, targeting vacuum-assisted resin infusion manufacturing of large wind turbine blades whose lower viscosity improves glass fabric wet-out at processing temperature.

-

2023: SABIC launched its new bio-based epoxy resin pilot programme in 2023 using bio-derived epichlorohydrin from renewable glycerol feedstock, targeting the growing demand for sustainable chemistry alternatives in construction coating and composite applications with green building certification procurement requirements.

Epoxy Resins Market Key Players

-

3M

-

Aditya Birla Chemicals

-

BASF SE

-

Dow Chemical Company

-

DIC Corporation

-

Huntsman Corporation

-

Kukdo Chemical Co., Ltd.

-

Macro Polymers

-

Mitsubishi Chemical Group Corporation

-

Nan Ya Plastics Corporation

-

Olin Corporation

-

Sinopec Corporation

-

Westlake Epoxy

-

Hexion Inc.

-

Cytec Solvay Group

-

Shin-Etsu Chemical Co., Ltd.

-

Eternal Chemical Co., Ltd.

-

Sika AG

-

Scott Bader Company Ltd.

-

Momentive Performance Materials Inc.

Epoxy Resins Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 14.35 Billion |

| Market Size by 2035 | USD 24.47 Billion |

| CAGR | CAGR of 5.49% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Form (Liquid, Solid, Solution) • By Raw Materials (DGBEA, Novolac, Aliphatic, Glycidyl, Amine, Others) • By Application (Paints & Coatings, Composites, Adhesives & Sealants, Others) • By End-User (Building & Construction, Automotive, General Industrial, Consumer Goods, Wind Energy, Aerospace/Aircraft, Marine, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3M, Aditya Birla Chemicals, BASF SE, Dow Chemical Company, DIC Corporation, Huntsman Corporation, Kukdo Chemical Co., Ltd., Macro Polymers, Mitsubishi Chemical Group Corporation, Nan Ya Plastics Corporation, Olin Corporation, Sinopec Corporation, Westlake Epoxy, Hexion Inc., Cytec Solvay Group, Shin-Etsu Chemical Co., Ltd., Eternal Chemical Co., Ltd., Sika AG, Scott Bader Company Ltd., Momentive Performance Materials Inc. |

Frequently Asked Questions

The Epoxy Resins Market is expected to grow at a CAGR of 5.49% from 2026 to 2035.

The Epoxy Resins Market was valued at USD 14.35 Billion in 2025.

Wind turbine blade composite epoxy resin demand from global offshore and onshore wind capacity expansion, and EV structural composite adoption creating above-average automotive epoxy demand from battery enclosure and lightweight structural applications.

Paints & Coatings dominated the Epoxy Resins Market in 2025, while Composites is the fastest growing segment.

Asia Pacific dominated the Epoxy Resins Market in 2025, with China accounting for approximately 44.8% of Asia Pacific revenues.

Get in Touch