Pruritus Therapeutics Market Report Scope & Overview:

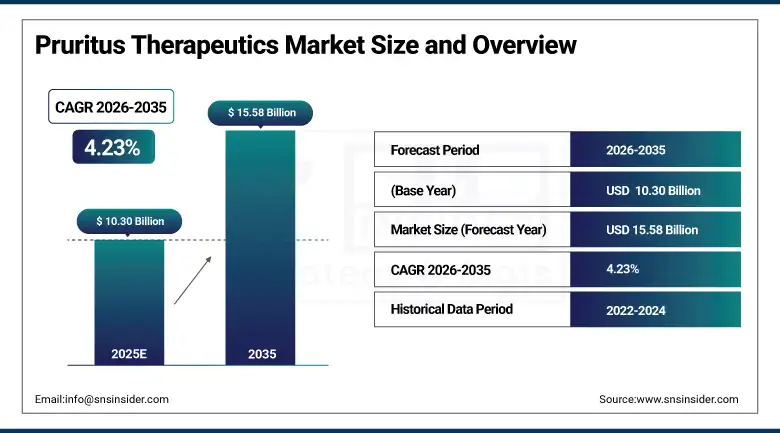

The Pruritus Therapeutics Market size was valued at USD 10.30 billion in 2025 and is expected to reach USD 15.58 billion by 2035, growing at a CAGR of 4.23% over the forecast period of 2026-2035.

The global pruritus therapeutics market is still growing steadily, primarily driven by increasing cases of chronic inflammatory skin diseases like atopic dermatitis, urticaria, and allergic contact dermatitis, along with a rapidly expanding pipeline of biologic and small molecule drugs. Another significant change is evident in the way this condition is now being viewed, i.e., it is now being treated as a medical condition rather than a symptom. Also, increased spending on healthcare, favorable reimbursement policies in developed countries, and the introduction of new IL-4, IL-13, and IL-31 receptor antagonists are all contributing to a gradual shift in the treatment of this condition. At the same time, pharmaceutical companies are also increasing their research and development activities for addressing the need for new treatments for both pediatric and elderly patients, which is also contributing to increased use of prescription medication as well as antihistamines for over-the-counter use.

For instance, in February 2024, the global prevalence of chronic pruritus was estimated to affect approximately 13.5% of the adult population worldwide, with atopic dermatitis alone responsible for over 223 million diagnosed cases globally, underscoring the substantial and expanding patient base driving demand for advanced pruritus therapeutics.

Pruritus Therapeutics Market Size and Forecast:

-

Market Size in 2025: USD 10.30 billion

-

Market Size by 2035: USD 15.58 billion

-

CAGR: 4.23% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Pruritus Therapeutics Market - Request Free Sample Report

Pruritus Therapeutics Market Trends:

-

Accelerated adoption of biologic agents, especially the IL-4/IL-13 antagonists like dupilumab, is changing the treatment landscape from immunosuppressive agents to targeted molecular therapies for the treatment of moderate-to-severe atopic dermatitis and chronic spontaneous urticaria.

-

Development and launch of JAK inhibitors-based oral therapies for the treatment of atopic dermatitis, including upadacitinib and abrocitinib, are providing physicians with a wide array of flexible options for the treatment of unresponsive cases to conventional corticosteroids and antihistamines.

-

Physicians' preference for calcineurin inhibitors and phosphodiesterase-4 inhibitors as steroid-sparing agents is increasing the adoption for the treatment of sensitive skin areas and long-term maintenance therapy for the treatment of atopic dermatitis.

-

Increased availability of internet pharmacies and digital health platforms is increasing the accessibility of over-the-counter antihistamines and prescription refills for the treatment of pruritus, thus increasing the treatment adherence rate for urban and semi-urban patient populations.

-

Increased use of real-world evidence, patient-reported outcome measures, and digital symptom tracking for the evaluation of pruritus therapeutics is reducing the drug approval timeline for the treatment of pruritus.

-

Increased prevalence of pruritus-related symptoms for the treatment of systemic diseases, including chronic kidney diseases, cholestatic liver diseases, and pruritus-related symptoms for the treatment of various types of cancers.

-

Increased competition for biologics from biosimilars under the FDA and EMA regulations and health technology assessment outcomes are changing the drug pricing landscape for the treatment of pruritus.

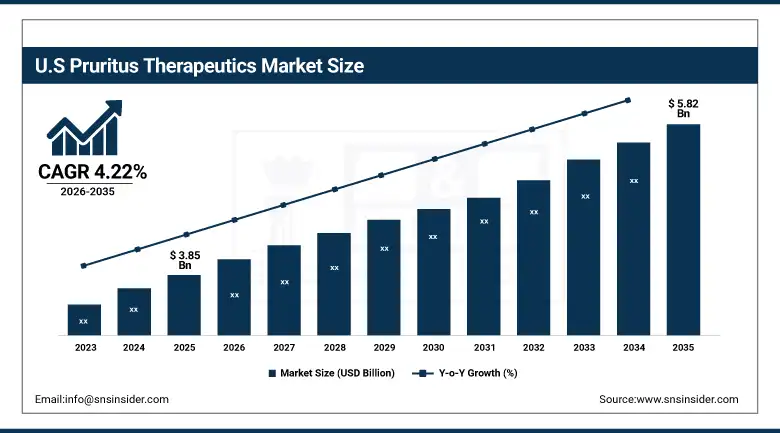

The U.S. Pruritus Therapeutics Market was valued at USD 3.85 billion in 2025 and is expected to reach USD 5.82 billion by 2035, growing at a CAGR of 4.22% from 2026-2035. The global pruritus therapeutics market is dominated by the US, which is attributed to the extremely high prevalence of atopic dermatitis and other conditions causing pruritus (31.6 million in total) among the American population, established reimbursement system for dermatological drugs, availability and reimbursement of novel and advanced FDA-approved treatment such as biologics and JAK inhibitors, better insurance coverage for prescription pruritus treatments, a better environment for clinical trials, and an established specialty pharmacy network for pruritus treatments distribution in the US. In addition, higher awareness campaigns conducted by the National Eczema Association and other dermatological advocacy organizations are also boosting the numbers of early diagnosis and treatment initiation in the market.

Pruritus Therapeutics Market Growth Drivers:

-

Rising Global Prevalence of Atopic Dermatitis and Chronic Urticaria is Driving the Pruritus Therapeutics Market Growth

The escalating global burden of atopic dermatitis, chronic spontaneous urticaria, and allergic contact dermatitis represents the most significant structural growth driver for the pruritus therapeutics market. With chronic pruritus affecting approximately 1 in 7 adults globally and atopic dermatitis impacting up to 20% of children in high-income countries, the patient population eligible for therapeutic intervention is vast and growing. Increasing urbanization, environmental allergen exposure, and rising incidence of immune dysregulation disorders are amplifying disease prevalence across both developed and emerging economies, directly expanding prescription volumes for corticosteroids, biologics, and antihistamines. Growing recognition of pruritus as a debilitating quality-of-life condition, rather than merely a symptom, is further driving physician prescribing behavior and market revenue generation.

For instance, in May 2024, the American Academy of Dermatology reported that annual healthcare costs associated with atopic dermatitis in the U.S. exceeded USD 5.3 billion, of which therapeutics accounted for approximately 67%, reflecting the substantial commercial opportunity within the pruritus treatment segment.

Pruritus Therapeutics Market Restraints:

-

High Treatment Costs of Biologic Therapies and Limited Access in Emerging Markets are Hampering Pruritus Therapeutics Market Growth

Despite their good clinical efficacy profiles, the high cost of acquisition for biologics and targeted therapy agents, with annual treatment costs for dupilumab and JAK inhibitors running upwards of $30,000 per patient in the United States, poses a major challenge for the widespread acceptance of these drugs in the global market, especially in developing and underdeveloped markets in the world. In the Asian Pacific and Latin American markets, where out-of-pocket expenditure on healthcare is high, the majority of patients still use affordable generic antihistamines and corticosteroids for their allergic diseases, thereby limiting the scope for premium products and suppressing their overall market value realization.

Pruritus Therapeutics Market Opportunities:

-

Expanding Biologic Pipeline and Novel Mechanism-of-Action Therapies Create Significant Growth Opportunities for the Pruritus Therapeutics Market

The strong clinical pipeline of novel itch pathways such as IL-31 Receptor Antagonists, TSLP Inhibitors, Substance P Modulators, and Kappa Opioid Receptor Agonists is an unprecedented growth opportunity in the Pruritus Therapeutics industry. In fact, promising drugs such as Nemolizumab (IL-31RA Antagonist) and Tradipitant (NK1 Receptor Antagonist) are in late-stage clinical development, indicating that future approval of these drugs is likely to open up completely new treatment algorithms in diseases such as chronic prurigo, uremic pruritus, cholestatic itch, among others. Additionally, investment in topical PDE-4 inhibitors and microbiome formulations is likely to diversify the existing product portfolios in the Pruritus Therapeutics industry in the next decade, offering multi-billion-dollar commercial opportunities in developed as well as developing markets.

For instance, in July 2024, the FDA granted Breakthrough Therapy Designation to a novel IL-31 receptor antagonist for the treatment of prurigo nodularis, underscoring the strong regulatory tailwind supporting next-generation pruritus therapeutics and the significant unmet medical need in niche itch-associated conditions.

Pruritus Therapeutics Market Segment Analysis

-

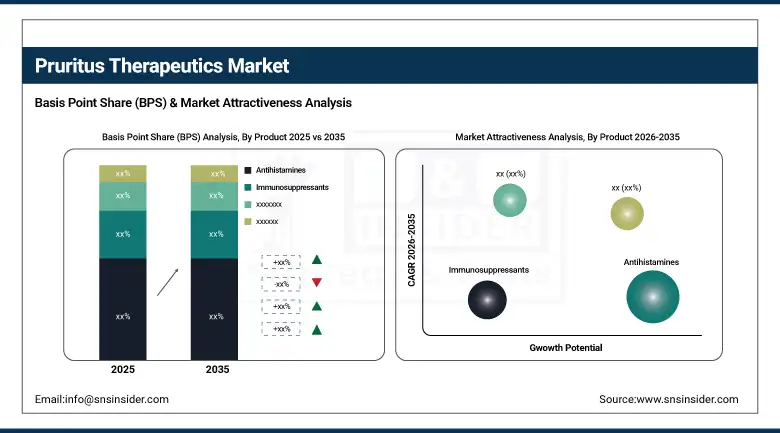

By product, antihistamines held the largest share of approximately 31.84% in 2025, while the immunosuppressant segment is expected to register the highest CAGR of 6.18% through 2035.

-

By disease, atopic dermatitis dominated with a share of approximately 37.92% in 2025, and the urticaria segment is expected to register the highest CAGR of 5.12% over the forecast period.

-

By distribution channel, hospital pharmacies accounted for the leading share of approximately 42.33% in 2025, while online pharmacies are expected to register the highest CAGR of 7.46% through 2035.

By Product, Antihistamines Lead the Market, While Immunosuppressants Register Fastest Growth

Antihistamines showed the highest share in revenues with approximately 31.84% in 2025, due to its widespread availability in both prescription and over-the-counter formulations, its clinical use in all forms of urticaria and allergic pruritus, and its high penetration through all channels of distribution in hospitals, retail pharmacies, and online pharmacies. On the other hand, the immunosuppressant segment is predicted to show the highest CAGR of approximately 6.18% during the forecast period of 2026-2035, because of the rapidly increasing use of biologic immunomodulators, expanding approvals for JAK inhibitors, and clinical need for maintenance therapy with steroids in moderate to severe forms of atopic dermatitis and chronic prurigo. Corticosteroids showed the second highest share in products with approximately 28.16% in 2025, because of sustained clinical use in all forms of acute flares of pruritic diseases.

By Disease, Atopic Dermatitis Leads, While Urticaria Registers Fastest Growth

The atopic dermatitis segment held the highest revenue share of approximately 37.92% in 2025 due to high disease prevalence rates globally, an exceptionally active pharmaceutical pipeline, and high commercial success rates for dupilumab and tralokinumab. This segment is also driven by increasing pediatric approvals for biologics, increasing disease management awareness, and rising specialist engagement in academic and community dermatology. The urticaria segment is also growing and is estimated to have the highest CAGR of approximately 5.12% in the forecast period from 2026 to 2035. This is due to increasing diagnosis rates for chronic spontaneous urticaria, increasing indications for anti-IgE therapies like omalizumab, and a rising pipeline for anti-Siglec-8 and anti-KIT biologics for treatment-refractory chronic inducible urticaria. Allergic contact dermatitis held a constant share of approximately 17.86% in 2025.

By Distribution Channel, Hospital Pharmacies Lead, While Online Pharmacies Register Fastest Growth

Hospital pharmacies maintained the largest share of approximately 42.33% in 2025, indicating the concentration of biologic infusion services, specialty drug dispensing, and inpatient dermatology treatment protocols in hospital-based healthcare delivery. High-value biologic prescriptions for dupilumab, omalizumab, and JAK inhibitors are predominantly delivered through hospital-based pharmacy networks, thereby maintaining the revenue growth of this channel. Online pharmacy is anticipated to experience the highest CAGR of approximately 7.46% between 2026 and 2035, led by the increasing consumer acceptance of the convenience of prescription refill services, the development of e-pharmacy regulations in the U.S. and the European Union, and the increasing penetration of telehealth-based digital prescription platforms. Retail pharmacies maintained approximately 29.74% of the market share in 2025, led by the high volume of OTC antihistamine prescriptions and the widespread availability of these pharmacy types.

Pruritus Therapeutics Market Regional Highlights:

North America Pruritus Therapeutics Market Insights:

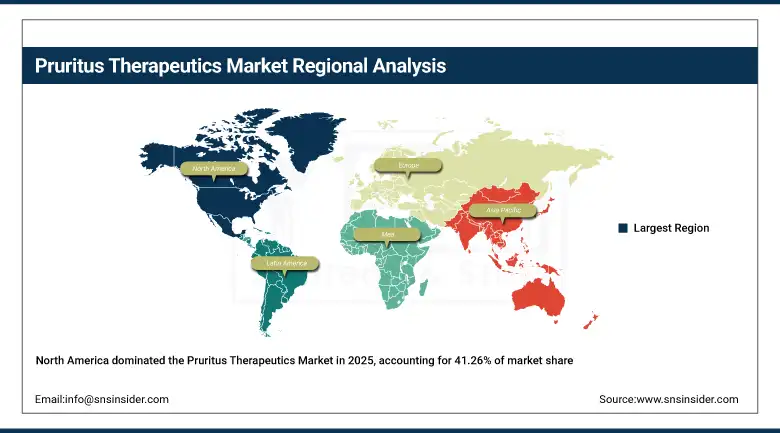

North America held the largest revenue share of approximately 41.26% in 2025 of the pruritus therapeutics market, underpinned by the highest per-capita consumption of prescription dermatology therapeutics, extensive FDA-approved biologic and JAK inhibitor portfolios, and a highly developed specialty pharmacy infrastructure. The U.S. market benefits from active clinical guideline updates from the American Academy of Dermatology, strong patient advocacy driving early and sustained therapy adoption, and commercial payer willingness to cover premium pruritus biologics under prior authorization protocols. Canada contributes incrementally to regional growth through government-funded provincial drug plans that include dupilumab and select JAK inhibitors on formulary for moderate-to-severe atopic dermatitis.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Pruritus Therapeutics Market Insights:

Asia Pacific is the fastest-growing segment of the pruritus therapeutics market, growing at a CAGR of 5.94%, due to the increasing rate of the dermatology patient pool, healthcare expenditure, and pharmaceutical manufacturing capabilities in the region, covering China, India, Japan, and South Korea. The increasing incidence of atopic dermatitis and urticaria among the pediatric population in urban centers, improving health insurance cover, and increasing access to generic corticosteroids and antihistamines are major drivers for the pruritus therapeutics market in the region. The increasing rate of skin health awareness among the population, entry of global biologic manufacturers in emerging markets in the Asia Pacific region, and increasing access to hospital-based dermatology specialty care services are the major drivers for the pruritus therapeutics market in the region. India and China are the major untapped markets for the pruritus therapeutics industry in the region, as pharmaceutical companies in the region are increasingly developing affordable biosimilars for the treatment of pruritic diseases.

Europe Pruritus Therapeutics Market Insights:

Europe represents the second-largest pruritus therapeutics market, with an approximate revenue share of 27.43% in 2025, due to the presence of established national health service structures, EMA-approved biologic portfolios, and robust pharmacovigilance infrastructure for ensuring the safety and efficacy of the therapeutics. The UK, Germany, and France account for the three largest pruritus therapeutics markets in Europe, with an established national dermatology guideline for dupilumab and JAK inhibitors for the treatment of moderate-to-severe atopic dermatitis. The market also benefits from the increasing trend of introducing biosimilars for the treatment of pruritus with monoclonal antibody-based therapeutics, which is improving the affordability of the therapeutics in the Central and Eastern European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Pruritus Therapeutics Market Insights:

In Latin America and the Middle East & Africa, rising dermatology disease burden, improving healthcare infrastructure, and growing pharmaceutical market liberalization are generating incremental demand for pruritus therapeutics. Brazil and Mexico lead the LATAM segment, supported by expanding public health insurance coverage for dermatological conditions and growing private hospital dermatology capacity. In the MEA region, the Gulf Cooperation Council countries, particularly Saudi Arabia and the UAE, are experiencing accelerated adoption of biologic pruritus therapies driven by rising disposable incomes, advanced private healthcare ecosystems, and increasing physician awareness of targeted treatment options. Affordable generic antihistamines and corticosteroids remain the dominant therapeutic choices across both LATAM and Sub-Saharan African markets.

Pruritus Therapeutics Market Competitive Landscape:

AbbVie Inc. (est. 1888, spin-off 2013) is a global research-driven biopharmaceutical company with a strong presence in immunology and dermatology. AbbVie's RINVOQ (upadacitinib), a selective JAK1 inhibitor, has achieved broad label approvals across atopic dermatitis and is under clinical evaluation for additional pruritic indications, supported by the company's extensive dermatology medical affairs and commercial infrastructure.

-

In January 2025, AbbVie announced positive Phase III results for upadacitinib in pediatric atopic dermatitis patients aged 6 months to 11 years, with plans to submit supplemental regulatory filings to the FDA and EMA, further broadening the addressable pruritus therapeutics patient population.

Regeneron Pharmaceuticals, Inc. (est. 1988) is a leading biotechnology company renowned for its monoclonal antibody discovery platform. Regeneron, in collaboration with Sanofi, markets Dupixent (dupilumab), the first biologic approved specifically for moderate-to-severe atopic dermatitis and subsequently for prurigo nodularis and chronic spontaneous urticaria, representing the highest-revenue single agent in the global pruritus therapeutics market.

-

In March 2024, Regeneron and Sanofi received FDA approval for Dupixent as an add-on maintenance therapy for chronic spontaneous urticaria in adults and adolescents 12 years and older, significantly expanding the drug's addressable commercial opportunity within the pruritus therapeutics segment.

Pfizer Inc. (est. 1849) is a multinational biopharmaceutical corporation with a diversified immunology and inflammation portfolio. Pfizer's Cibinqo (abrocitinib), a once-daily oral JAK1 inhibitor approved for moderate-to-severe atopic dermatitis, has been commercially launched in over 40 markets globally and is supported by a robust phase IV real-world evidence program to solidify long-term safety and efficacy data in chronic pruritic conditions.

-

In September 2024, Pfizer published long-term safety data from the JADE EXTEND study demonstrating sustained efficacy of abrocitinib over 96 weeks in adults with moderate-to-severe atopic dermatitis, reinforcing physician confidence and supporting formulary expansion discussions with payers across North America and Europe.

Pruritus Therapeutics Market Key Players:

-

AbbVie Inc.

-

Regeneron Pharmaceuticals, Inc.

-

Pfizer Inc.

-

Sanofi S.A.

-

Novartis AG

-

Johnson & Johnson (Janssen Pharmaceuticals)

-

Eli Lilly and Company

-

LEO Pharma A/S

-

Galderma S.A.

-

Astellas Pharma Inc.

-

Incyte Corporation

-

Cara Therapeutics, Inc.

-

Kiniksa Pharmaceuticals, Ltd.

-

Escient Pharmaceuticals

-

Dermira, Inc. (an Eli Lilly Company)

-

GlaxoSmithKline plc

-

Bayer AG

-

Viatris Inc.

-

Noven Pharmaceuticals LLC

-

Torii Pharmaceutical Co., Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.30 Billion |

| Market Size by 2035 | USD 15.58 Billion |

| CAGR | CAGR of 4.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Corticosteroids, Calcineurin Inhibitors, Local Anesthetics, Counterirritants, Antihistamines, Immunosuppressant, Others) • By Disease (Urticaria, Atopic Dermatitis, Allergic Contact Dermatitis, Others) • By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | AbbVie Inc., Regeneron Pharmaceuticals, Inc., Pfizer Inc., Sanofi S.A., Novartis AG, Johnson & Johnson (Janssen Pharmaceuticals), Eli Lilly and Company, LEO Pharma A/S, Galderma S.A., Astellas Pharma Inc., Incyte Corporation, Cara Therapeutics, Inc., Kiniksa Pharmaceuticals, Ltd., Escient Pharmaceuticals, Dermira, Inc. (an Eli Lilly Company), GlaxoSmithKline plc, Bayer AG, Viatris Inc., Noven Pharmaceuticals LLC, Torii Pharmaceutical Co., Ltd. |

Frequently Asked Questions

The Pruritus Therapeutics Market was valued at USD 10.30 billion in 2025 and is projected to grow steadily over the forecast period.

The Pruritus Therapeutics Market is expected to reach USD 15.58 billion by 2035, reflecting sustained demand for advanced itch management therapies.

The Pruritus Therapeutics Market is anticipated to grow at a CAGR of 4.23% from 2026 to 2035.

Growth of the Pruritus Therapeutics Market is driven by rising prevalence of atopic dermatitis, increasing biologics adoption, and expanding R&D pipelines, along with improved awareness and diagnosis rates.

In the Pruritus Therapeutics Market, antihistamines dominate with a 31.84% share in 2025, while immunosuppressants are the fastest-growing segment with a CAGR of 6.18%.

Get in Touch