Chronic Disease Management Market Report Scope & Overview:

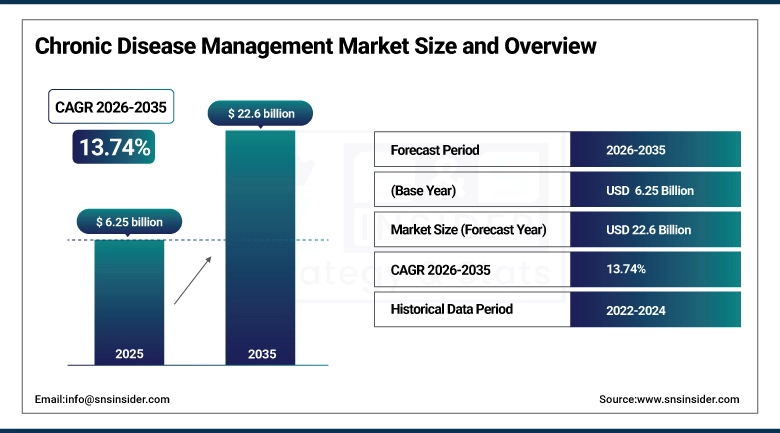

The Chronic Disease Management Market was valued at USD 6.25 billion in 2025 and is expected to reach USD 22.6 billion by 2035, growing at a CAGR of 13.74% from 2026–2035.

The Chronic Disease Management Market is expanding owing to an increase in the global prevalence of chronic illnesses, including diabetes, heart-related diseases, and lung diseases. The increasing use of technology in health care, such as digital health and telemedicine services, has contributed positively to better health care management and patient results. An increase in the health care infrastructure base, increased awareness about preventative health care practices, and government health care policies have fueled market growth.

Market Size and Forecast

-

Market Size in 2025: USD 6.25 Billion

-

Market Size by 2035: USD 22.6 Billion

-

CAGR: 13.74% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Chronic Disease Management Market - Request Free Sample Report

Chronic Disease Management Market Trends

-

Remote patient monitoring devices tracking vital signs, glucose levels, and other biomarkers continuously enabling proactive interventions.

-

AI-powered predictive analytics identifying high-risk patients before acute events occur, enabling targeted preventive outreach.

-

Telehealth integration making chronic care management accessible to patients in rural and underserved communities.

-

Behavioral health integration recognizing depression, anxiety, and stress as key factors in chronic disease outcomes.

-

Value-based care contracts incentivizing healthcare systems to invest in chronic disease management programs that reduce total cost of care.

-

Wearable device data integration with clinical electronic health records providing a continuous stream of patient health signals.

-

Population health management platforms identifying untreated or undertreated chronic patients across large insured populations.

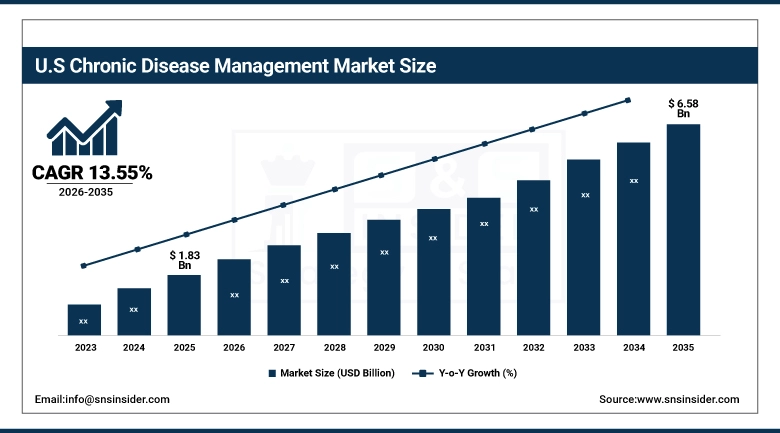

U.S. Chronic Disease Management Market was valued at USD 1.83 billion in 2025 and is expected to reach USD 6.58 billion by 2035, at a CAGR of 13.55% from 2026 to 2035.

The U.S. Chronic Disease Management Market is expanding owing to the increasing incidence of diabetes, cardiovascular diseases, and respiratory conditions. Growing use of telemedicine, remote patient monitoring, and artificial intelligence in healthcare has led to better management of such chronic diseases. Efficient healthcare facilities, favorable reimbursement policies, and increased emphasis on preventive healthcare are other key factors contributing to market growth.

Chronic Disease Management Market Segment Analysis

-

By Service Type, Implementation Services segment dominated the Chronic Disease Management Market in 2025 with 46% share; Educational Services segment fastest growing (CAGR).

-

By Disease Type, Cardiovascular Diseases segment dominated the Chronic Disease Management Market in 2025 with 34% share; Diabetes segment fastest growing (CAGR).

-

By Delivery Mode, Cloud-based segment dominated the Chronic Disease Management Market in 2025 with 52% share; Web-based segment fastest growing (CAGR).

-

By End User, Providers segment dominated the Chronic Disease Management Market in 2025 with 61% share; Payers segment fastest growing (CAGR).

By Service Type, Implementation Services segment dominates the Chronic Disease Management Market, Educational Services segment expected to grow fastest

Implementation Services segment led the market for Chronic Disease Management Market in 2025 owing to the importance associated with implementation, integration, and customization of workflows in healthcare organizations. These implementation services are required by healthcare providers in order to integrate their chronic care management platform with other existing software such as electronic medical record system and hospital management system. Growing complexity of healthcare IT infrastructure and digital transformation of organizations have made the healthcare providers seek expertise in implementation services for successful adoption.

Educational Services segment is considered as the fastest-growing one as it focuses on educating patients about chronic diseases and training both the patient's caregiver as well as the healthcare professionals in managing chronic diseases. High prevalence rate and increasing number of patients suffering from chronic diseases are the major factors behind the high demand of structured educational courses that educate the patients to ensure medication adherence.

By Disease Type, Cardiovascular Diseases segment dominates the Chronic Disease Management Market, Diabetes segment expected to grow fastest

Cardiovascular Diseases segment dominated the Chronic Disease Management Market in 2025 owing to the rising incidence of heart diseases globally as a result of leading unhealthy lifestyle characterized by poor diets, stress, age, and lack of physical activity. The use of advanced technologies such as predictive analysis and monitoring systems has made it easier to manage such diseases. Moreover, the emphasis on early detection and management strategies in the healthcare industry has helped consolidate the lead of cardiovascular disease management solutions.

Diabetes segment will experience rapid growth owing to the increasing cases of diabetic patients attributed to obesity, genetics, and changes in lifestyle. Use of advanced devices, apps, and personalized treatment methods has made it much easier to manage the disease. Increasing awareness campaigns and initiatives aimed at detecting and diagnosing diabetes have further stimulated the demand for diabetes management solutions.

By Delivery Mode, Cloud-based segment dominates the Chronic Disease Management Market, Web-based segment expected to grow fastest

The Cloud-based segment led the Chronic Disease Management Market in 2025 due to its scalability, cost-effectiveness, and capability of providing real-time patient monitoring and data exchange. Cloud computing allows for easy integration with healthcare facilities, EHRs, and telehealth services. The increasing usage of telemedicine services, higher levels of digitalization in the field, and need for more flexible and centralized access to information contribute to the increased domination of cloud-based solutions in chronic care management.

The Web-based segment is currently growing at the fastest rate due to its easy access and compatibility with various devices. Health institutions and consumers increasingly opt for website solutions to engage in teleconsultations, book appointments, monitor their health, etc. Higher penetration rates of the Internet, increased popularity of telemedicine and need for user-friendly digital healthcare applications contribute to high growth rates in the web-based segment.

By End User, Providers segment dominates the Chronic Disease Management Market, Payers segment expected to grow fastest

Providers segment dominated the Chronic Disease Management Market in 2025 since it is involved in the provision of healthcare services to patients, conducting diagnoses, and chronic disease management. Hospitals, clinics, and other healthcare service providers depend on the chronic disease management system for coordination of healthcare service delivery, prevention of re-admissions, and improvement of treatment results. Growing uptake of digital health technologies and value-based healthcare practices have increased their dominance further.

Payers Segment is expected to be the fastest-growing since there will be an emphasis on lowering healthcare spending, enhancing healthcare outcomes for patients, and encouraging prevention of chronic diseases. Insurance companies and other healthcare payers are embracing chronic disease management software to ensure that the reimbursements are optimized while minimizing the costs of treatment in the future. Growth in the value-based healthcare approach and rising prevalence of chronic diseases will drive this trend worldwide.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

78% |

|

Europe |

United Kingdom |

30% |

|

Asia Pacific |

India |

38% |

|

Middle East & Africa |

UAE |

36% |

|

Latin America |

Brazil |

52% |

North America Chronic Disease Management Market Insights

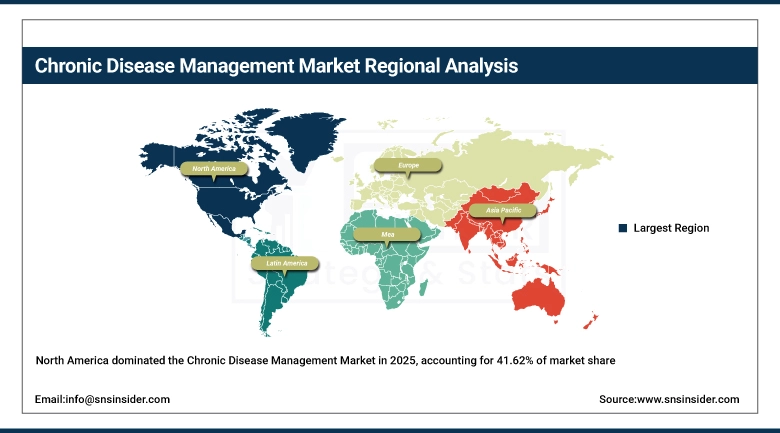

North America emerged as the leading region for the Chronic Disease Management Market in 2025, accounting for 41.62% of revenue. The region is characterized by its well-developed healthcare system, high adoption of health tech innovations, and telemedicine and remote patient monitoring solutions. North America has a significant incidence rate of chronic diseases, including diabetes, heart diseases, and respiratory problems. The region also has favorable reimbursement practices, developed healthcare IT infrastructure, and active participation of major market players.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Chronic Disease Management Market Insights

The Asia Pacific region is anticipated to experience the highest CAGR of 14.51% in the Chronic Disease Management Market owing to the increasing prevalence of chronic illnesses like diabetes, heart disease, and respiratory problems. The factors contributing to the growth of this market include growing digitization of the healthcare sector, increased adoption of telemedicine and remote patient monitoring, and improved infrastructure in the healthcare industry. Increased awareness about preventive healthcare, high healthcare spending, and government efforts towards adopting digital health solutions are other factors propelling market growth.

Europe Chronic Disease Management Market Insights

Europe Chronic Disease Management Market is witnessing steady growth owing to the rising incidence of cardiovascular disorders, diabetes, and respiratory ailments within the European countries. Improved healthcare facilities, increased usage of digital health solutions, and the growing trend towards telemedicine services are boosting the provision of chronic care in the region. The support from government policies encouraging preventive healthcare services and early detection programs is also aiding the market growth. Besides, the use of AI analytics and electronic health records is enhancing the disease management capabilities.

Middle East & Africa and Latin America Chronic Disease Management Market Insights

The Middle East & Africa and Latin America Chronic Disease Management Market is experiencing consistent growth due to an increasing number of people suffering from diabetes, cardiovascular disease, and obesity. The increasing use of technology and digital platforms in chronic care management has made it easier for more people to receive these services. Growing healthcare infrastructure, preventive healthcare programs by governments, and increased awareness regarding chronic disease management are contributing factors towards market growth. However, lack of healthcare facilities in rural areas and budget constraints remain barriers.

Chronic Disease Management Market Growth Drivers

-

Expanding adoption of digital health technologies including telemedicine, remote patient monitoring, and AI-based healthcare platforms improving disease control efficiency

The widespread implementation of digital health tools is changing the way chronic conditions are managed through real-time patient monitoring and informed decision making in clinical settings. Telehealth services make it possible to conduct virtual appointments, thus avoiding unnecessary trips to hospitals. Remote patient monitors are capable of continuously tracking important biological data like blood sugar levels, blood pressure, and heart rate, which allows for timely action. Data analysis and artificial intelligence support medical professionals in forecasting the course of diseases and developing treatment strategies tailored to patients. The incorporation of mobile health apps contributes to higher patient involvement and adherence to prescribed medications.

Chronic Disease Management Market Restraints

-

Data privacy concerns and lack of interoperability between healthcare systems limiting seamless integration of chronic disease management platforms

The rising fears concerning the confidentiality of patients' information, security threats, and unapproved access hinder the use of digital tools for managing chronic diseases. Health institutions deal with personal health information that makes them susceptible to cyber attacks and other related issues. Moreover, the non-uniformity of the legal frameworks regulating data protection across different parts of the world is a major obstacle in implementing global health platforms. The failure to have an interoperable system for different healthcare IT solutions makes it difficult to transmit data from one healthcare institution to another.

Chronic Disease Management Market Opportunities

-

Rising demand for home-based healthcare and remote patient monitoring solutions driving expansion of chronic disease management platforms globally

There has been an increasing demand for home-based health care and remote patient monitoring, which presents promising opportunities for chronic disease management programs. Many patients would rather undergo treatment at home than go to hospitals to avoid unnecessary visits and feel more comfortable. Remote monitoring allows for constant health condition tracking of diabetes, hypertension, heart diseases, and many other chronic diseases. Telemedicine and mobile health applications have also expanded their reach and have increased patient access and participation. Health care service providers are now investing in technology solutions that facilitate virtual visits and real-time communication.

Recent Developments

-

2025: Teladoc Health launched its AI-powered chronic care platform integrating real-time remote monitoring data from wearables and connected devices with predictive AI models, enabling care teams to prioritize patients showing early signs of decompensation before acute events occur.

-

2024 (August): WellnessWits collaborated with IBM's Watsonx Assistant to launch an AI-powered virtual chronic care companion that facilitates patient-provider communication, medication adherence support, and personalized self-management guidance for patients with multiple chronic conditions.

-

2023: Omada Health received FDA breakthrough device designation for its digital diabetes prevention program, representing recognition of the clinical evidence base for digital chronic disease management and potentially unlocking Medicare coverage for the program serving the highest-risk diabetic population.

Chronic Disease Management Market Key Players

-

Siemens Healthineers

-

GE Healthcare

-

Allscripts Healthcare Solutions

-

Cerner Corporation

-

Epic Systems Corporation

-

McKesson Corporation

-

Oracle Corporation

-

Teladoc Health, Inc.

-

Medtronic plc

-

Omada Health

-

Health Catalyst

-

Cognizant Technology Solutions

-

WellDoc, Inc.

-

eClinicalWorks

-

CareCloud, Inc.

-

Lumeon Inc.

-

NextGen Healthcare

-

Virgin Pulse

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.35 Billion |

| Market Size by 2035 | USD 22.6 Billion |

| CAGR | CAGR of 13.74% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Consulting Services, Implementation Services, Educational Services, Other) • By Disease Type (Cardiovascular Diseases, Diabetes, Respiratory Diseases, Cancer, Chronic Kidney Disease, Others [Arthritis, etc.]) • By Delivery Mode (On-premise, Web-based, Cloud-based) • By End User (Providers, Payers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Philips Healthcare, IBM Corporation, Siemens Healthineers, GE Healthcare, Allscripts Healthcare Solutions, Cerner Corporation, Epic Systems Corporation, McKesson Corporation, Oracle Corporation, Teladoc Health, Inc., Medtronic plc, Omada Health, Health Catalyst, Cognizant Technology Solutions, WellDoc, Inc., eClinicalWorks, CareCloud, Inc., Lumeon Inc., NextGen Healthcare, Virgin Pulse, and other players. |

Frequently Asked Questions

Rising global chronic disease burden, the healthcare system shift to value-based care, and AI-powered digital health tools enabling continuous patient engagement and early intervention.

North America dominates with 41.62% revenue share; Asia Pacific is expected to grow at the fastest CAGR of 14.51%.

Cardiovascular Diseases dominate with 34% market share, reflecting the high global burden of heart disease and maturity of remote cardiac monitoring tools.

The Chronic Disease Management Market was valued at USD 6.25 billion in 2025.

The Chronic Disease Management Market is expected to grow at a CAGR of 13.74% from 2026 to 2035.

Get in Touch