Rigid Foam Market Report Scope & Overview:

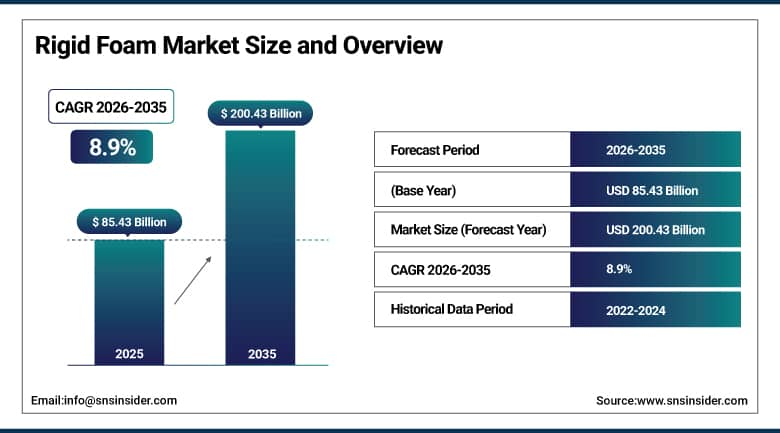

The Rigid Foam Market was valued at USD 85.43 Billion in 2025 and is expected to reach USD 200.43 Billion by 2035, growing at a CAGR of 8.9% from 2026–2035.

The global rigid foam market is growing at an exceptional and commercially broad-based pace. Rigid foam encompasses closed-cell polymer foam materials including polyurethane (PU) rigid foam, expanded polystyrene (EPS), extruded polystyrene (XPS), polyisocyanurate (PIR), and phenolic foam that provide thermal insulation, structural support, and buoyancy in building construction, refrigeration equipment, automotive panels, and packaging. The market growth is driven by increasing demand from construction and automotive industries, as well as the packaging sector, with rising demand for high-performance insulation materials propelling above-average commercial momentum.

In 2024, BASF launched its Neopor® BMB, a certified mass-balanced expanded polystyrene using bio-circular feedstocks for rigid insulation board production, offering building insulation material with reduced carbon footprint credentials that comply with green building certification requirements. The launch reflects the commercial response to construction sector sustainability mandates whose green building programme’s material carbon footprint assessment creates specification motivation for bio-circular content rigid foam insulation whose functional thermal performance matches conventional alternatives while delivering documented scope 3 emission reduction.

Market Size and Forecast:

-

Market Size in 2026E: USD 93.03 Billion

-

Market Size by 2035: USD 200.43 Billion

-

CAGR: 8.9% from 2026 to 2035

-

Fastest Growing Region: Europe

-

Largest Region: Asia Pacific

To Get More Information On Rigid Foam Market - Request Free Sample Report

Rigid Foam Market Trends:

-

Phase-out of high-GWP blowing agents is accelerating adoption of environmentally compliant rigid foam formulations using low-emission alternatives

-

Increasing implementation of net-zero building standards is driving demand for high-performance rigid foam insulation materials with superior thermal efficiency

-

Growing adoption of continuous insulation systems in commercial construction is supporting demand for rigid foam boards and insulated panel solutions

-

Phenolic foam is gaining traction in industrial and commercial applications due to its combination of excellent thermal insulation and fire-resistant properties

-

Expansion of cold chain infrastructure for food, pharmaceutical, and logistics sectors is increasing demand for rigid foam insulation in refrigerated storage and transportation systems

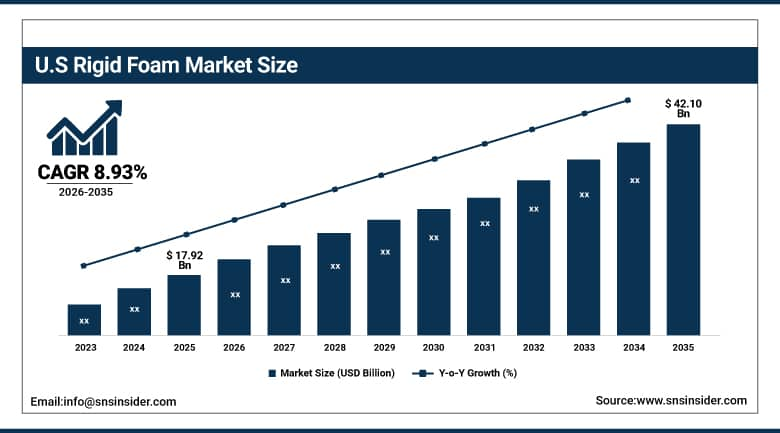

U.S. Rigid Foam Market Outlook:

The U.S. Rigid Foam Market was valued at approximately USD 17.92 Billion in 2025 and is expected to reach approximately USD 42.10 Billion by 2035, growing at a CAGR of approximately 8.93%.

The U.S. is a commercially significant rigid foam market within North America. BASF, Dow, Huntsman, Covestro, and Owens Corning’s U.S. operations collectively serve the domestic market across construction, refrigeration, packaging, and automotive applications. DOE’s building energy efficiency programmes, ASHRAE 90.1’s building envelope insulation requirements, and the IRA’s energy efficiency tax credit creating consumer motivation for insulation upgrade collectively sustain structured U.S. rigid foam procurement. The U.S. cold chain infrastructure’s expansion for pharmaceutical logistics and direct-to-consumer food delivery creates growing refrigeration insulation demand.

Dow launched its VORAFORCE™ composite spray polyurethane foam system in 2024 for roofing and building envelope applications, combining enhanced moisture resistance, improved adhesion to diverse substrates, and accelerated cure time that enables faster commercial roofing installation schedules. The system’s performance improvements create above-average adoption in the U.S. commercial re-roofing market whose energy efficiency upgrade motivation sustains structured procurement that compounds with the aging commercial building stock’s retrofit cycle.

Rigid Foam Market Segment Analysis:

-

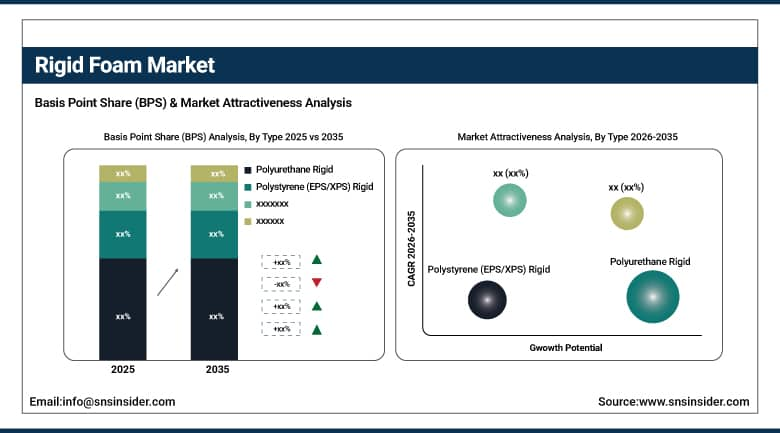

By Type, the Polyurethane Rigid Foam segment dominated the Rigid Foam Market with approximately 48% share in 2025, while the EPS/XPS Polystyrene segment is the fastest growing.

-

By Application, the Building & Construction Insulation segment dominated the Rigid Foam Market with approximately 52% share in 2025, while the Automotive segment is the fastest growing.

-

By End Use, the Building & Construction segment dominated the Rigid Foam Market with approximately 55% share in 2025, while the Refrigeration & Cold Chain segment is the fastest growing

By Type, polyurethane dominates, EPS/XPS grows fastest

Polyurethane rigid foam retained the dominant type position with approximately 48% of the rigid foam market in 2025. PU rigid foam’s commercial primacy reflects its superior thermal insulation performance whose lambda value of 0.022-0.028 W/m·K creates the highest R-value per unit thickness of any commercially available rigid insulation material, enabling thinner insulation specification that maximises usable interior space while meeting building energy code requirements. Spray PU foam’s ability to conform to irregular surfaces and eliminate air infiltration creates superior airtightness that board insulation alternatives cannot achieve equivalently. Continuous PU sandwich panel production whose integrated structural and insulation function creates commercial building envelope efficiency that sustains specification preference across industrial, commercial, and cold chain construction.

EPS and XPS are the fastest-growing types because the construction sector’s continuous insulation board adoption, below-grade waterproof insulation requirement, and insulated concrete form construction method collectively create above-average polystyrene rigid foam demand whose cost-competitive economics and moisture-resistant closed-cell XPS structure create specification advantages in ground-contact and moisture-exposed insulation applications. Each new commercial building that specifies continuous exterior insulation creates EPS/XPS board procurement whose aggregate across the extraordinary global construction investment pace creates commercial scale.

By Application, construction dominates, automotive grows fastest

Building and construction insulation retained the dominant application position with approximately 52% of the rigid foam market in 2025. Energy efficiency building codes’ progressive insulation requirement tightening, the net-zero building standard’s passive house performance prerequisite, and the commercial building sector’s LEED and BREEAM certification motivation create non-discretionary rigid foam insulation procurement whose compliance character sustains demand through construction cycle variation. Each new residential or commercial building constructed to current energy code creates rigid foam insulation procurement whose specification level grows with each successive code revision. The global residential construction volume, particularly Asia Pacific’s extraordinary apartment construction pace, creates aggregate rigid foam demand that substantially exceeds any single non-construction application category.

Automotive is the fastest-growing application because EV interior lightweighting, battery pack thermal management, and acoustic performance requirements are creating above-average per-vehicle rigid foam content growth that exceeds conventional ICE vehicle foam application. Each BEV platform that replaces heavy steel and acoustic felt with lightweight rigid foam composite structures creates procurement whose aggregate with the extraordinary EV production volume growth creates commercial scale. Battery thermal management’s polyurethane foam encapsulation and thermal interface requirements create new automotive application categories whose procurement compounds with EV market penetration.

By End Use, building & construction dominates, refrigeration grows fastest

Building and construction retained the dominant end-use position with approximately 55% of the rigid foam market in 2025. The non-discretionary compliance motivation of building energy codes creates consistent insulation procurement that sustains the construction end-use category’s market leadership independently of economic cycle variation in discretionary building improvement investment. Each new building whose energy performance compliance requires rigid foam insulation in roof, wall, floor, and foundation applications creates procurement whose value scales with building area and insulation specification level. Government stimulus programmes for energy-efficient building retrofit, including IRA’s weatherisation assistance and EU’s Renovation Wave, create above-average existing building insulation upgrade procurement that compounds with new construction volume.

Refrigeration and cold chain is the fastest-growing end use because the extraordinary expansion of pharmaceutical cold chain logistics for COVID-19 vaccine distribution, ongoing biologics therapy supply chain, and the direct-to-consumer fresh food delivery market’s cold chain investment are creating above-average refrigerated warehouse, cold store panel, and transport refrigeration rigid foam insulation procurement. Each new pharmaceutical cold store constructed and each new refrigerated trailer fleet expanded creates PU rigid foam panel procurement whose aggregate across the global cold chain investment creates commercial scale that compounds with pharmaceutical and food logistics growth.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

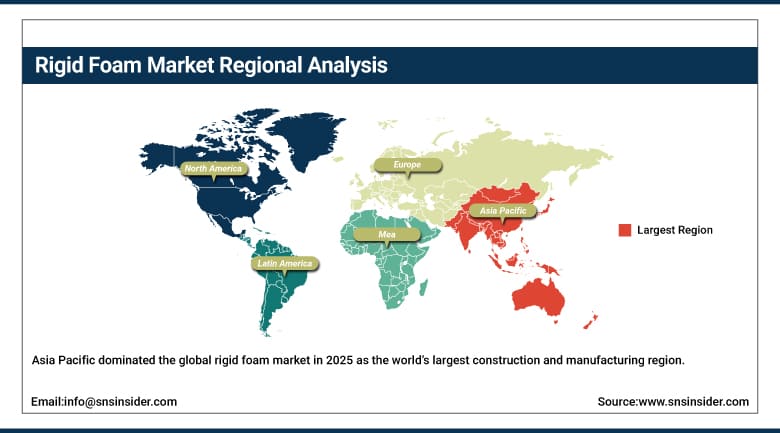

Asia Pacific Rigid Foam Market Insights

Asia Pacific dominated the global rigid foam market in 2025 as the world’s largest construction and manufacturing region. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary residential and commercial construction scale, the manufacturing sector’s insulation requirement, and the cold chain infrastructure investment creating refrigeration insulation procurement. The region’s rapid urbanisation, industrial development, and infrastructure investment create aggregate rigid foam demand that substantially exceeds any other regional market.

India, South Korea, and Japan are significant secondary markets where construction sector growth, automotive manufacturing, and cold chain infrastructure investment create consistent rigid foam procurement that reinforces Asia Pacific’s regional dominance.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Rigid Foam Market Insights

Europe is the fastest-growing regional rigid foam market, driven by EU Energy Performance of Buildings Directive’s nearly-zero energy building standard, EU Renovation Wave’s retrofit insulation investment programme, and the European Green Deal’s building decarbonisation mandate creating the most structurally driven rigid foam demand growth of any region. Germany accounts for approximately 22.3% of European revenues through BASF’s and Covestro’s domestic commercial presence, the construction sector’s above-average insulation specification, and the industrial sector’s process insulation investment.

France, Poland, and the Netherlands are significant secondary markets where residential renovation insulation programmes, new construction energy code compliance, and cold chain logistics infrastructure create consistent rigid foam procurement.

North America Rigid Foam Market Insights

North America is a commercially significant rigid foam market whose IRA energy efficiency incentive, commercial building re-roofing cycle, and cold chain expansion create consistent procurement. The United States accounts for approximately 87.4% of North American revenues through BASF, Dow, Covestro, Huntsman, and Owens Corning’s commercial operations whose combined portfolio serves the domestic construction, industrial, and automotive rigid foam markets.

Canada contributes approximately 12.6% of North American revenues through its residential and commercial construction sector’s insulation procurement, the cold chain logistics investment, and the automotive manufacturing sector’s rigid foam component demand.

MEA & Latin America Rigid Foam Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its extraordinary construction investment for NEOM and Vision 2030’s infrastructure programme, the cold chain expansion for food and pharmaceutical logistics, and the industrial sector’s insulation procurement. Brazil leads Latin American revenues at approximately 44.2% through its construction sector’s insulation demand, the food cold chain infrastructure, and the automotive manufacturing sector’s rigid foam component procurement.

UAE’s commercial construction and cold chain investment and South Africa’s construction sector create significant MEA secondary markets whose rigid foam procurement reflects growing industrial and construction development investment.

Market Dynamics:

Growth Drivers: Energy efficiency building codes creating insulation demand and cold chain expansion driving refrigeration insulation

Energy efficiency building codes are the rigid foam market’s most commercially certain structural growth driver. The global progressive tightening of building thermal performance standards—EU EPBD’s NZEB requirement, U.S. IECC’s insulation value progression, and China’s building energy efficiency standard—creates systematic insulation specification upgrade whose rigid foam component grows with each code revision cycle. Each new building constructed to current energy code creates rigid foam insulation procurement whose specification level grows with progressive standard tightening. The Renovation Wave’s existing building retrofit programme creates additional incremental procurement that compounds with new construction volume.

Cold chain infrastructure expansion for pharmaceutical logistics and fresh food direct-to-consumer delivery creates the most commercially dynamic new rigid foam application growth. Each new pharmaceutical cold store, temperature-controlled food distribution centre, and refrigerated trailer fleet expansion creates polyurethane rigid foam panel procurement whose aggregate across the extraordinary global cold chain investment creates commercial scale that sustains above-average refrigeration application growth.

Restraints: HFC blowing agent phase-out creating reformulation investment and fire performance regulation creating product development cost

HFC and HCFC blowing agent phase-out under the Kigali Amendment’s progressive timeline creates reformulation investment whose cost and timeline create operational burden for rigid foam manufacturers. Each country’s accelerating phase-out deadline creates compliance capital expenditure whose aggregate across the global rigid foam industry creates substantial investment pressure. HFO blowing agents’ higher cost relative to HFC alternatives creates production cost increase whose downstream pricing impact creates adoption resistance in cost-sensitive construction applications.

Fire performance regulation tightening for rigid foam building insulation, following high-profile building fire incidents highlighting combustible cladding risk, creates product development investment in fire-retardant formulations whose performance compliance requires chemistry modification and accelerated testing investment that adds cost and timeline to product development programmes.

Opportunities: Net-zero building renovation programmes and EV battery thermal management foam

Net-zero building renovation programmes represent the most commercially certain near-term volume growth opportunity. EU Renovation Wave’s EUR 275 billion annual investment target, U.S. IRA’s building energy efficiency incentive, and equivalent national retrofit programmes collectively create the most commercially certain large-scale rigid foam insulation procurement pipeline of any application category. Each residential building retrofitted with rigid foam continuous insulation creates procurement whose aggregate across hundreds of millions of European and North American buildings’ upgrade programme sustains above-average demand growth.

EV battery thermal management foam represents an emerging premium application whose polyurethane thermal interface foam’s ability to fill battery cell-to-module gaps while providing controlled thermal conductivity creates a new automotive rigid foam application category whose per-vehicle content grows with EV market penetration. Each new EV battery pack design that specifies thermal management foam creates procurement whose aggregate across the extraordinary global EV production volume growth creates commercial scale.

Recent Developments:

-

2024: BASF launched Neopor® BMB, a certified mass-balanced EPS insulation with bio-circular feedstock credentials in 2024, targeting building insulation manufacturers seeking to meet green building certification’s material carbon footprint requirements while maintaining conventional EPS thermal performance.

-

2024: Dow launched its VORAFORCE™ composite spray polyurethane foam system in 2024 for roofing and building envelope applications with enhanced moisture resistance, improved substrate adhesion, and accelerated cure time for faster commercial roofing installation.

-

2024: Covestro expanded its Desmodur blowing agent-free polyurethane rigid foam formulations in 2024 targeting next-generation HFO-blown continuous insulation panel production, enabling manufacturers to achieve EU F-Gas Regulation compliance while maintaining panel thermal performance specifications.

Rigid Foam Market Key Players:

-

BASF SE

-

Dow Inc.

-

Covestro AG

-

Huntsman Corporation

-

Recticel NV

-

Owens Corning

-

Saint-Gobain S.A.

-

Kingspan Group plc

-

Armacell International S.A.

-

Knauf Insulation GmbH

-

Tosoh Corporation

-

Bayer MaterialScience (Covestro)

-

Asahi Kasei Corporation

-

SABIC (Saudi Basic Industries)

-

Nitto Denko Corporation

-

Rogers Corporation

-

Sekisui Chemical Co., Ltd.

-

Puren GmbH

-

Synthos Group

-

Versalis S.p.A. (Eni)

Rigid Foam Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 85.43 Billion |

| Market Size by 2035 | USD 200.43 Billion |

| CAGR | CAGR of 8.9% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Polyurethane Rigid Foam, Polystyrene/EPS/XPS Rigid Foam, Polyisocyanurate/PIR Foam, Phenolic Foam, Others) • by Application (Building & Construction Insulation, Industrial & Commercial Refrigeration, Automotive, Packaging, Marine & Aerospace, Others) • by End Use (Building & Construction, Refrigeration & Cold Chain, Automotive & Transportation, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | BASF SE, Dow Inc., Covestro AG, Huntsman Corporation, Recticel NV, Owens Corning, Saint-Gobain S.A., Kingspan Group plc, Armacell International S.A., Knauf Insulation GmbH, Tosoh Corporation, Bayer MaterialScience (Covestro), Asahi Kasei Corporation, SABIC (Saudi Basic Industries), Nitto Denko Corporation, Rogers Corporation, Sekisui Chemical Co., Ltd., Puren GmbH, Synthos Group, Versalis S.p.A. (Eni) |

Frequently Asked Questions

The Rigid Foam Market is expected to grow at a CAGR of 8.9% from 2026 to 2035.

The Rigid Foam Market was valued at USD 85.43 Billion in 2025.

Increasing demand from construction and automotive industries for high-performance insulation materials.

Polyurethane Rigid Foam dominated the Rigid Foam Market with approximately 48% share in 2025, while EPS/XPS Polystyrene is the fastest growing segment.

Europe is the fastest-growing region in the Rigid Foam Market, driven by energy efficiency building regulations, while Asia Pacific holds the largest market share in 2025.

Get in Touch