Security Advisory Services Market Report Scope & Overview:

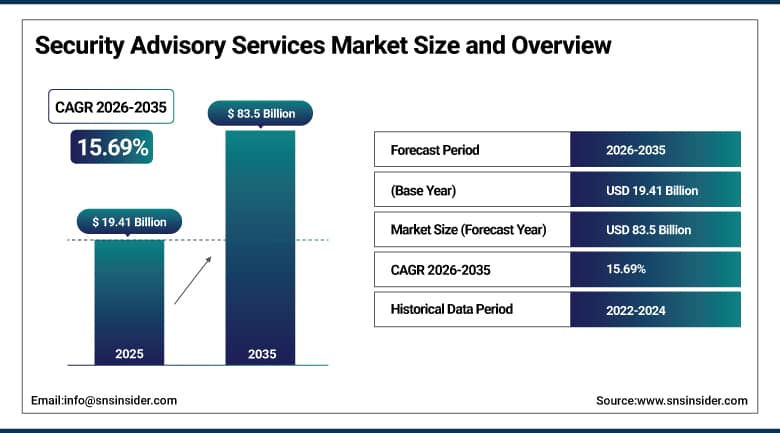

The Security Advisory Services Market was valued at USD 19.41 Billion in 2025 and is expected to reach USD 83.5 Billion by 2035, growing at a CAGR of 15.69% from 2026–2035.

Security advisory services provide organisations with the external expertise, strategic guidance, and technical assessment that most cannot develop or sustain internally. The market encompasses penetration testing that simulates attacker behaviour to identify exploitable vulnerabilities before they are exploited in reality, CISO advisory and support that delivers executive-level cybersecurity strategy to organisations. The market is growing because the threat environment is fundamentally worsening. Ransomware attacks targeting hospitals, municipalities, and manufacturers have caused billions of dollars in operational damage and ransom payments. Supply chain attacks through trusted software vendors have demonstrated that even organisations with mature security programmes are vulnerable through their technology dependencies. Nation-state threat actors with resources exceeding those of most enterprise security teams are actively targeting critical infrastructure. Against this threat backdrop, organisations that previously managed cybersecurity as an internal IT function are recognising that external advisory expertise provides a quality of threat intelligence, attacker perspective, and technical depth that in-house teams rarely achieve independently.

IBM's 2025 Cost of a Data Breach report confirmed the global average data breach cost reached USD 4.88 million per incident, the highest recorded figure in the report's two-decade history. This financial exposure, combined with regulatory penalties under GDPR and SEC disclosure requirements, creates the business case that drives organisations to invest in security advisory services before a breach rather than responding to one.

Market Size and Forecast

-

Market Size in 2026E: USD 22.46 Billion

-

Market Size by 2035: USD 83.5 Billion

-

CAGR: 15.69% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Security Advisory Services Market - Request Free Sample Report

Security Advisory Services Market Trends

-

AI-powered penetration testing tools are enabling advisory firms to conduct more comprehensive assessments faster, identifying attack paths that manual testing might miss while automating the reconnaissance and exploitation phases that previously consumed significant analyst time.

-

Regulatory compliance advisory is growing rapidly as the EU's DORA financial services resilience regulation, the SEC's cybersecurity disclosure rules, and expanding state-level privacy laws in the U.S. create new compliance requirements that organisations need external expertise to interpret and implement correctly.

-

Virtual CISO and fractional security leadership services are expanding the addressable market beyond large enterprises to mid-market and SME organisations that need executive-level security strategy but cannot justify or attract a full-time CISO at the compensation levels that experienced security leaders command.

-

Cloud security advisory is becoming the fastest-growing service specialisation as organisations struggle with the shared responsibility model of cloud computing, misconfigured cloud storage and access controls, and the security implications of multi-cloud architectures that their IT teams were not designed to manage.

-

Threat intelligence integration with advisory services is improving the commercial value proposition as advisory firms that access real-time threat actor intelligence can provide assessments and recommendations calibrated to the specific threats targeting a client's industry rather than generic security frameworks.

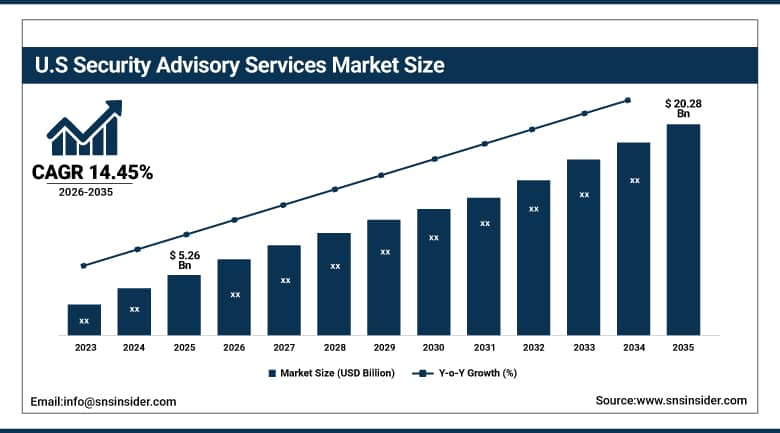

The U.S. Security Advisory Services Market Outlook

The U.S. security advisory services market was valued at approximately USD 5.26 Billion in 2025 and is expected to reach approximately USD 20.28 Billion by 2035, growing at a CAGR of 14.45%.

The United States is the world's largest security advisory services market. SEC cybersecurity disclosure rules effective from December 2023 require publicly traded companies to disclose material cybersecurity incidents within four business days, creating immediate advisory demand from boards. The U.S. healthcare organisations represent one of the fastest-growing security advisory client segments. The healthcare sector consistently ranks as the highest-cost industry for data breach incidents because of the lifetime value of health record data for identity theft and fraud. HIPAA compliance advisory, medical device security assessment, and operational technology security for hospital networks have all experienced significant demand growth. Government sector advisory demand is sustained by federal civilian agency security requirements, defence contractor CMMC compliance, and state and local government security improvement programmes funded through federal grants following significant ransomware incidents against municipalities and school districts.

The SEC's cybersecurity disclosure rules, effective December 2023, require public companies to report material cybersecurity incidents within four business days. This regulation has driven board-level cybersecurity investment and created structured demand for security advisory services from companies that previously managed cybersecurity as an operational IT concern rather than a board-level governance matter.

Security Advisory Services Market Segment Analysis

-

By Service Type, penetration testing led the market with approximately 32.40% share in 2025; CISO advisory and support is the fastest-growing service at a CAGR of 18.60%.

-

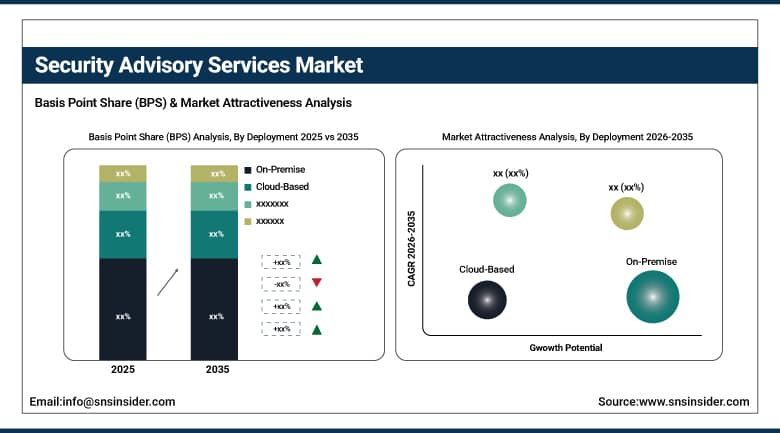

By Deployment, on-premise led the market with approximately 57.10% share in 2025; cloud-based is the fastest-growing at a CAGR of 17.30% through scalability, remote delivery capabilities, and cost efficiency.

-

By Organization Size, large enterprises led the market with approximately 64.20% share in 2025; SMEs are the fastest-growing at a CAGR of 16.10%.

-

By Industry Vertical, BFSI held the largest share in 2025 through high-value data assets, stringent financial sector cybersecurity regulations; Healthcare is the fastest-growing vertical.

By Deployment, on-premise dominates, cloud-based fastest By Deployment

The on-premise deployment segment dominated the Security Advisory Services Market with a 57.10% revenue share in 2025, driven by organizations requiring greater control over cybersecurity infrastructure, sensitive data, and regulatory compliance. Large enterprises, government agencies, BFSI institutions, and critical infrastructure operators continue to favor on-premise advisory services to strengthen internal security frameworks, mitigate cyber risks, and ensure adherence to stringent governance requirements. The segment's leadership is further supported by the need for customized security architectures, direct oversight of security operations, and protection of mission-critical systems from evolving cyber threats.

The cloud-based deployment segment is projected to register the fastest CAGR of 17.30% during the forecast period, fueled by increasing cloud adoption, digital transformation initiatives, and hybrid work environments. Organizations are leveraging cloud-based security advisory services for their scalability, flexibility, remote accessibility, and lower infrastructure costs. These solutions enable continuous monitoring, rapid threat detection, and streamlined compliance management across multi-cloud environments. Growing investments in cloud security, coupled with the rising demand for agile cybersecurity strategies and managed security services, are expected to accelerate segment growth significantly over the coming years.

By Service Type, penetration testing dominates, CISO advisory grows fastest

Penetration testing held approximately 32.40% of security advisory services market revenues in 2025. The commercial rationale is straightforward. Organisations that identify and fix vulnerabilities before attackers exploit them avoid the operational disruption, regulatory penalty, and reputational damage of an actual security incident. External penetration testers bring an adversarial mindset and independent perspective that internal security teams, who are operationally close to the systems they protect, cannot fully replicate. The most commercially significant penetration testing engagements combine network, application, and social engineering testing components that together simulate the realistic attack chains that sophisticated threat actors use. Red team exercises that simulate targeted attack campaigns against specific organisations provide the most realistic security posture assessment available and are growing as a premium service tier.

CISO advisory and support is the fastest-growing service type at a CAGR of 18.60% through 2035. The global shortage of experienced Chief Information Security Officers is more severe than the broader technology talent shortage. Companies that can attract a CISO with the strategic vision, executive communication skills, board relationship capability, and technical credibility required for the role typically pay compensation exceeding USD 300,000 to USD 500,000 annually in the U.S. Many mid-market organisations cannot justify this cost for a single hire or cannot attract a qualified candidate in competition with larger employers. Virtual CISO and fractional CISO advisory services provide the strategic security leadership, board reporting, programme development, and regulatory liaison functions at a fraction of the full-time employment cost.

By Organization Size, large enterprises dominate, SMEs grow fastest

Large enterprises held approximately 64.20% of security advisory services market revenues in 2025. Their commercial dominance reflects the scale of their cybersecurity investment, the complexity of their IT environments, and the regulatory obligations that require systematic security assessment and advisory engagement. A large financial institution might engage multiple advisory firms simultaneously for different purposes including offensive security testing for its core banking systems, regulatory compliance advisory for Basel III operational risk requirements, incident response retainer services for immediate post-breach support, and CISO advisory for strategic planning. The comprehensiveness of large enterprise security advisory requirements drives above-average per-client revenue that sustains large enterprise dominance despite their smaller number relative to SMEs.

SMEs are the fastest-growing client segment at a CAGR of 16.10% through 2035. The threat landscape has democratised in the worst sense: attackers are now systematically targeting small and medium businesses because their security controls are weaker, their backups are less robust, and their willingness to pay ransoms to restore operations is often higher relative to their financial capacity. Security advisory service providers have responded by developing packaged SME assessment and advisory products that provide structured security improvement programmes at price points accessible to businesses with security budgets of USD 50,000 to USD 500,000 annually rather than the millions that enterprise programmes command.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

71.2% |

|

Europe |

United Kingdom |

31.4% |

|

Asia Pacific |

India |

34.8% |

|

Middle East & Africa |

UAE |

28.7% |

|

Latin America |

Brazil |

42.4% |

North America Security Advisory Services Market Insights

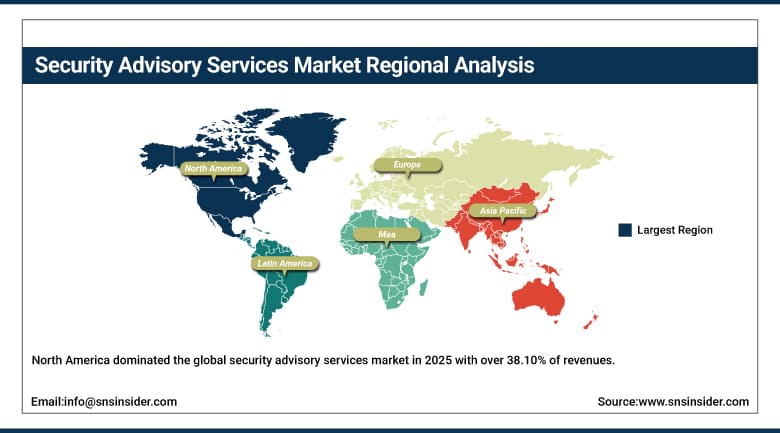

North America dominated the global security advisory services market in 2025 with over 38.10% of revenues. The United States accounts for approximately 71.2% of North American revenues as the market with the highest enterprise cybersecurity spending, the most demanding regulatory environment, and the greatest concentration of advisory service providers. The SEC cybersecurity disclosure rules, CISA critical infrastructure security requirements, state-level privacy law compliance obligations, and healthcare HIPAA enforcement together create a regulatory compliance advisory demand unique in its breadth and commercial scale. Major advisory practices at Deloitte, EY, KPMG, PwC, IBM Security, and Mandiant alongside specialist boutiques including CrowdStrike Services and Arctic Wolf provide the service capacity that corporate America's cybersecurity advisory demand requires. The Canadian Centre for Cyber Security provides threat intelligence that advisory firms use to calibrate their recommendations to the specific threat landscape facing Canadian organisations. Canadian federal regulatory requirements for financial institution cybersecurity and the Critical Infrastructure Protection programmes drive professional advisory engagement among the organisations within scope of these frameworks.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Security Advisory Services Market Insights

Europe is a large and regulation-driven security advisory services market. The United Kingdom accounts for approximately 31.4% of European revenues as the region's most mature cybersecurity advisory market with the highest concentration of specialist advisory firms and the deepest enterprise cybersecurity spending. GDPR enforcement by national data protection authorities across EU member states continues to drive compliance advisory demand from organisations responding to regulatory investigations, updating their data protection programmes, and assessing vendors for GDPR supply chain risk. DORA, the Digital Operational Resilience Act for EU financial services firms, came into force in January 2025 and has generated significant compliance advisory demand from banks, insurers, and investment firms across the EU. Germany, France, the Netherlands, and Scandinavia represent significant national security advisory markets. The EU's NIS2 Directive, which expanded the scope of mandatory cybersecurity requirements, created widespread new compliance advisory demand across manufacturing, food production, waste management, and other sectors that had not previously faced mandatory cybersecurity standards.

Asia Pacific Security Advisory Services Market Insights

Asia Pacific is the fastest-growing security advisory services market at a CAGR of 16.79% through 2035. India accounts for approximately 34.8% of Asia Pacific revenues as the region's largest and most commercially dynamic security advisory market. India's combination of a large IT services industry that provides substantial security advisory delivery capacity, rapid digital transformation creating new enterprise attack surface, and growing regulatory requirements for financial services and critical infrastructure cybersecurity collectively make it the most commercially significant market in the region. Japan, South Korea, Singapore, and Australia each maintain sophisticated security advisory markets characterised by above-average enterprise security spending and progressive regulatory frameworks for critical infrastructure protection.

MEA & Latin America Security Advisory Services Market Insights

The Middle East and Africa and Latin America are growing security advisory markets where increasing cyberattack incidents, expanding digital transformation, and developing regulatory frameworks are driving advisory demand. The UAE leads MEA revenues at approximately 28.7% of the regional share through its National Cybersecurity Strategy, the NESA regulatory authority's active enforcement programme, and the concentration of financial services, government, and energy sector organisations that represent the highest-value advisory clients in the region. Brazil leads Latin American revenues at approximately 42.4% through its large financial services sector operating under Banco Central do Brasil's cybersecurity resolution requirements and the LGPD data protection law's advisory demand.

Market Dynamics

Growth Drivers: Escalating cyberattack frequency and sophistication and expanding regulatory compliance requirements are the primary security advisory services market growth drivers.

The threat environment is worsening faster than most organisations' in-house security capabilities can keep pace. Ransomware-as-a-service has lowered the technical barrier for cybercriminal attacks, enabling less sophisticated actors to conduct financially devastating attacks on hospitals, municipalities, and manufacturers. Nation-state threat actors including groups attributed to Russia, China, North Korea, and Iran actively target Western government, defence, financial, and critical infrastructure organisations with capabilities that exceed most corporate security team counter-measure sophistication. Against this backdrop, organisations increasingly recognise that external advisory expertise provides a quality of threat perspective and technical assessment depth that in-house teams cannot independently match.

Regulatory complexity is a structural driver of security advisory demand. The security compliance landscape facing a mid-size U.S. company with international operations might include GDPR, CCPA, NYDFS cybersecurity regulation, CMMC if they supply the defence department, PCI-DSS if they process payment cards, and industry-specific requirements if they operate in healthcare or financial services. Navigating this regulatory matrix, implementing the required controls, and documenting compliance for auditors requires specialist advisory expertise that generalist IT teams and corporate legal departments cannot provide. Each new regulation adds incremental advisory demand across the entire organisation population within its scope.

Restraints: Shortage of experienced security advisors, advisory service standardisation challenges, and client budget constraints are restraining security advisory services market growth.

The global cybersecurity talent shortage extends directly into the security advisory services industry. Advisory firms compete with large enterprises, banks, and technology companies for the same pool of experienced security professionals. A senior penetration tester, threat intelligence analyst, or cloud security architect commands market compensation that limits advisory firm margins unless service delivery can be systematically scaled through automation, junior analyst leverage, and AI-assisted tooling. Staffing experienced teams for specialised advisory practices including industrial control system security, automotive cybersecurity, and healthcare medical device security is particularly challenging given the narrow intersection of security expertise and domain knowledge these require.

Advisory service pricing faces pressure from both budget-constrained clients and commoditised service competition. Basic penetration testing has become commoditised as automated scanning tools and offshore delivery teams enable low-cost providers to undercut premium advisory firms on simple assessments. Advisory firms must continuously invest in developing differentiating capability at the premium end, including sophisticated red team exercises, advanced threat actor simulation, and C-suite strategy advisory, while managing the cost pressures that commoditisation creates in their higher-volume assessment service lines.

Opportunities: AI-augmented security advisory capability and industrial OT security advisory as IT-OT convergence creates new attack surface represent the strongest growth opportunities.

AI-augmented security advisory is transforming both the quality and the commercial economics of advisory service delivery. AI tools can conduct automated asset discovery, vulnerability enumeration, and attack path analysis at a scale and speed that manual methods cannot match. Advisory teams equipped with AI-assisted tools can deliver more comprehensive assessments in less time, improving client value while sustaining advisor team economics. Generative AI tools for security report writing, compliance documentation, and risk communication are reducing the administrative burden on high-cost senior advisors who can redirect recaptured time toward higher-value analysis and client engagement.

Operational technology security advisory represents a rapidly growing and undersupplied specialisation. Manufacturing plants, power generation facilities, water treatment systems, and oil and gas infrastructure are implementing digital connectivity that creates cyberattack exposure in systems whose compromise could cause physical harm or environmental damage. The intersection of IT security knowledge and OT engineering understanding required for effective industrial cybersecurity advisory is uncommon, creating premium pricing opportunities for advisory practices that develop genuine expertise in ICS-SCADA security assessment and programme development.

Recent Developments:

-

2025: IBM Security expanded its X-Force threat intelligence integration into its security advisory service engagements, enabling advisory teams to calibrate assessments and recommendations based on real-time intelligence about threat actors actively targeting client industries.

-

2025: Mandiant (Google Cloud) reported continued strong demand for its incident response retainer services following high-profile ransomware incidents across healthcare and critical infrastructure sectors that demonstrated the financial consequences of inadequate security programme investment.

-

2025: Deloitte expanded its virtual CISO service offering to mid-market clients through a standardised programme that provides fractional security leadership, board reporting, regulatory advisory, and programme oversight at a fixed annual subscription price accessible to companies below the enterprise tier.

Security Advisory Services Market Key Players are:

-

IBM Security

-

Deloitte LLP

-

EY

-

KPMG International

-

PricewaterhouseCoopers

-

Accenture Security

-

Mandiant

-

CrowdStrike Inc.

-

Palo Alto Networks

-

Check Point Software Technologies

-

Rapid7 Inc.

-

Tenable Holdings Inc.

-

Bishop Fox

-

NCC Group

-

Trustwave

-

Arctic Wolf Networks

-

eSentire Inc.

-

SecurityScorecard

-

Coalfire Systems

-

Optiv Security

Security Advisory Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.41 Billion |

| Market Size by 2035 | USD 83.5 Billion |

| CAGR | CAGR of 15.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Penetration Testing, CISO Advisory & Support, Vulnerability Management, Incident Response, Compliance Management, Security Risk Management, Others) • By Deployment (On-Premise, Cloud-Based) • By Industry Vertical (BFSI, IT & Telecom, Healthcare, Government & Public Sector, Energy & Utilities, Manufacturing, Others) • By Organization Size (Large Enterprises, Small & Medium Enterprises) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Security, Deloitte LLP, EY, KPMG International, PricewaterhouseCoopers, Accenture Security, Mandiant, CrowdStrike Inc., Palo Alto Networks, Check Point Software Technologies, Rapid7 Inc., Tenable Holdings Inc., Bishop Fox, NCC Group, Trustwave, Arctic Wolf Networks, eSentire Inc., SecurityScorecard, Coalfire Systems, Optiv Security |

Frequently Asked Questions

North America dominated the market in 2025 with over 38.10% of global revenues.

Penetration testing dominated with approximately 32.40% of revenues in 2025.

Escalating cyberattack frequency and sophistication are the primary growth drivers.

The security advisory services market was valued at USD 19.41 Billion in 2025.

The security advisory services market is expected to grow at a CAGR of 15.69% from 2026 to 2035.

Get in Touch