Seed Coating Market Report Scope & Overview:

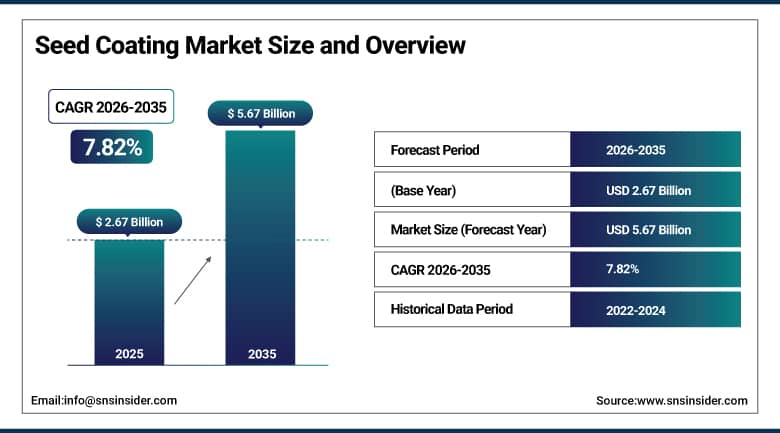

Seed Coating Market was valued at USD 2.67 billion in 2025 and is expected to reach USD 5.67 billion by 2035, growing at a CAGR of 7.82% from 2026–2035.

Market growth in the Seed Coatings industry has been steady owing to the increasing demands from farmers and seed producers worldwide, who are interested in providing better protection to seeds, improving their germination rate, and reducing the usage of chemicals during farming. The idea of seed coatings has come a long way from serving its basic purpose of acting as a coating layer. Seed coatings currently function as a means through which different active compounds like fungicides, insecticides, micronutrients, bio-fertilizers, and biological compounds are applied on seeds before plantation.

Government agricultural programs in major crop-producing economies are actively supporting the adoption of advanced seed treatment technologies. Initiatives in India, China, the United States, and across the European Union have directed funding toward research into improved seed coating formulations, provided incentives for farmers to adopt treated seeds, and established standards and certification pathways that are strengthening farmer confidence in coated seed products across multiple segments.

Seed Coating Market Size and Forecast

-

Market Size in 2025: USD 2.67 Billion

-

Market Size by 2035: USD 5.67 Billion

-

CAGR: 7.82% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Seed Coating Market - Request Free Sample Report

Seed Coating Market Trends

-

Rapid expansion of biological and bio-based seed coatings incorporating microbial inoculants, biostimulants, and natural polymers aligned with sustainable agriculture goals.

-

Growing adoption of precision agriculture practices increasing demand for treated seeds that deliver uniform germination, predictable plant populations, and reduced field variability.

-

Rising use of polymer-based film coatings enabling controlled and time-released delivery of active ingredients including fungicides, insecticides, and micronutrients to developing seedlings.

-

Increasing government programs and national seed initiatives in major agricultural economies supporting coated seed research, farmer adoption incentives, and quality certification frameworks.

-

Accelerating demand for fruits and vegetable seed coatings driven by global growth in commercial vegetable farming, organic production, and high-value horticultural crop output.

-

Technological advances in pelleting and encrusting processes improving automation compatibility and enabling precision planting of traditionally difficult-to-handle small or irregular seeds.

-

Growing integration of AI-driven formulation design and process monitoring tools by major coating manufacturers improving coating uniformity, active ingredient adhesion, and overall product consistency.

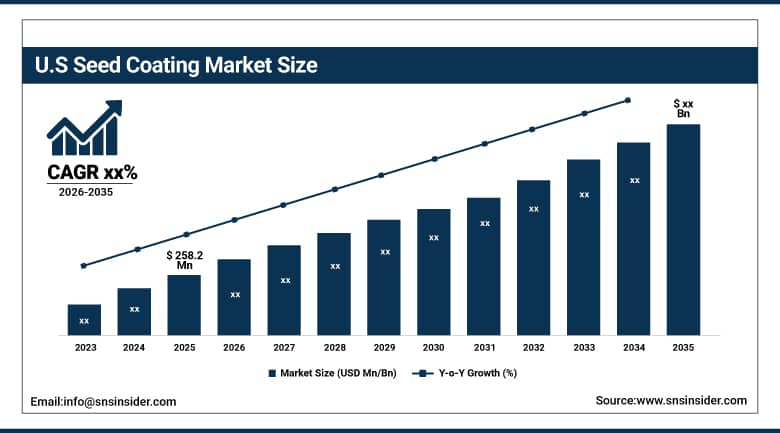

U.S. Seed Coating Market was valued at USD 258.2 million in 2025 and is expected to maintain strong growth through 2035, supported by advanced agricultural infrastructure, precision farming adoption, and the presence of leading global agrochemical and seed companies.

The US dominates the seed coatings market in North America and is one of the most technologically sophisticated commercial markets for seed treatments worldwide. The agriculture industry in the US is marked by massive commercial cultivation of crops such as corn, soybeans, wheat, and cotton on millions of hectares of farmland, where coated seeds play a critical role in protecting crops against soilborne diseases, insects, and erratic weather conditions during planting. The presence of a vibrant network of seed suppliers, agrochemical manufacturers, and coating technologies firms in the US has fueled healthy competition and innovation in the industry.

The U.S. Department of Agriculture and land-grant university extension programs continue to conduct and publish research on the agronomic benefits of seed coating technologies, providing the scientific validation that supports farmer adoption decisions.

Seed Coating Market Segment Insights

-

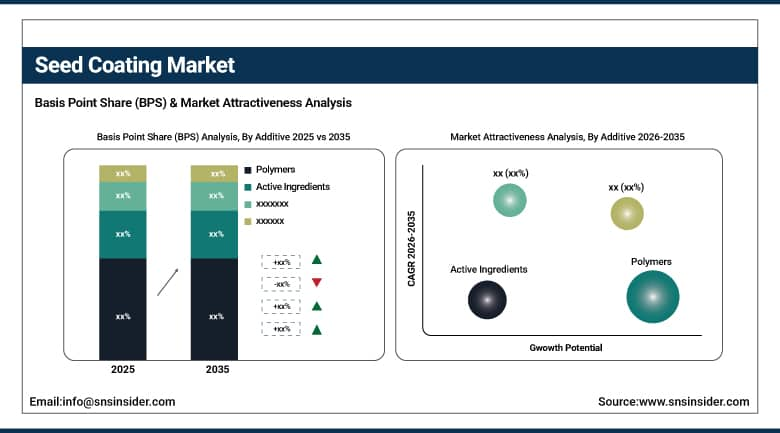

Based on Additive, Polymers accounted for the largest market share (~45.2%) in 2025; Active Ingredients expected to be the fastest-growing segment (CAGR).

-

Based on Crop Type, Cereals & Grains accounted for the largest market share (~40.5%) in 2025; Fruits & Vegetables expected to be the fastest-growing segment (CAGR).

-

Based on Form, Liquid accounted for the largest market share (~80.7%) in 2025; Dry segment growing steadily driven by specialty crop applications.

-

Based on Process, Film Coating accounted for the largest market share (~55.1%) in 2025; Pelleting expected to be the fastest-growing segment (CAGR).

Seed Coating Market Segment Analysis

By Additive, Polymers dominate the Seed Coating Market, Active Ingredients expected to grow fastest

Polymers accounted for the maximum market share in the seed coatings market, reaching a value of about 45.2% of the total additives revenue. Seed coatings based on polymers are highly valued because of their ability to provide uniform and effective film formation around the seeds without interfering with the germination capacity, size, or weight of the seeds, which would otherwise hinder their performance during rapid seed sowing by machines.

Active ingredients including fungicides, insecticides, micronutrients, and biological agents are expected to be the fastest-growing additive category during the forecast period. The shift toward multifunctional seed coatings that simultaneously protect against pathogens, supply nutritional inputs, and incorporate biological stimulants is driving increased investment in active ingredient development and formulation optimization.

By Crop Type, Cereals & Grains dominate the Seed Coating Market, Fruits & Vegetables expected to grow fastest

In 2025, the cereals and grains segment occupied the leading position in terms of market share, generating around 40.5% of the global revenue generated by different types of crops. Wheat, rice, corn, and barley are essential crops that require cultivation in huge hectares of land in each agricultural zone, and the production volume of these crops provides a stable volume market for seed coatings. The farmers engaged in growing such commodities are dependent on seeds' protection from soil pathogens, control of insects at the beginning of the growing season, and ensuring stand establishment for each hectare of land to achieve maximum yields.

The fruits and vegetables segment is expected to register the fastest growth rate during the forecast period of 2026 to 2035. These are high-value crops where seed costs are significant and where precise, uniform germination directly impacts crop quality and market returns. Farmers in commercial vegetable production and horticultural operations are willing to invest in premium seed coatings that deliver consistent germination, early disease protection, and enhanced seedling establishment. The rapid growth of organic vegetable farming globally, where biological seed coatings compatible with organic certification standards are in high demand, is adding further momentum to this segment.

By Form, Liquid dominates the Seed Coating Market, Dry form growing in specialty applications

The liquid coating emerged as the leader among the various types of seed treatments available, generating about 80.7% of the entire form revenue in 2025. It is easier to use liquids in the commercial treatment of seeds because it can be evenly distributed on the surface of the seeds using the drum or continuous treater machines, it is relatively inexpensive both in terms of manufacturing and application, and is more flexible in terms of active ingredient formulation. The liquid coating creates an evenly distributed thin layer on the seeds that does not affect their weight and dimensions, thus making them compatible with precision planters.

Dry seed coating formulations, while representing a smaller market share, serve important specialized applications particularly in pelleting processes where a dry powder or clay-based matrix is built up around small or irregular seeds to create a more uniform spherical pellet. This is especially valuable for vegetable, flower, and specialty crop seeds where planting precision is critical and where seed shape variation would otherwise create challenges in automated planting systems. The dry form segment is expected to grow steadily as the commercial vegetable and ornamental seed industries expand globally.

By Process, Film Coating dominates the Seed Coating Market, Pelleting expected to grow fastest

The film coating process occupied the leading position with an estimated share of about 55.1% in the overall process market in 2025. In this process, a thin uniform coat of polymer is added to the surface of the seeds without significantly altering their size. As such, it is applicable in many different plant varieties while remaining compatible with most planting equipment. This is the most common method of seed processing employed by the major seed processors and commercial seed treatments due to its scalability, efficiency, and compatibility with most liquid active ingredients.

The pelleting segment is projected to grow at the fastest CAGR throughout the forecast period. Pelleting transforms small, irregularly shaped seeds into uniform, spherical units that can be handled and planted with precision automated equipment. This process is increasingly in demand as commercial vegetable and horticultural production scales up and as precision planting technology becomes more widely adopted. The growth of urban agriculture, vertical farming, and controlled-environment horticulture is also driving demand for pelleted seeds that perform consistently in automated seeding systems used in these high-tech growing environments.

Seed Coating Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

45% |

|

North America |

United States |

82% |

|

Europe |

Germany |

31% |

|

Latin America |

Brazil |

55% |

|

Middle East & Africa |

South Africa |

32% |

Asia Pacific Seed Coating Market Insights

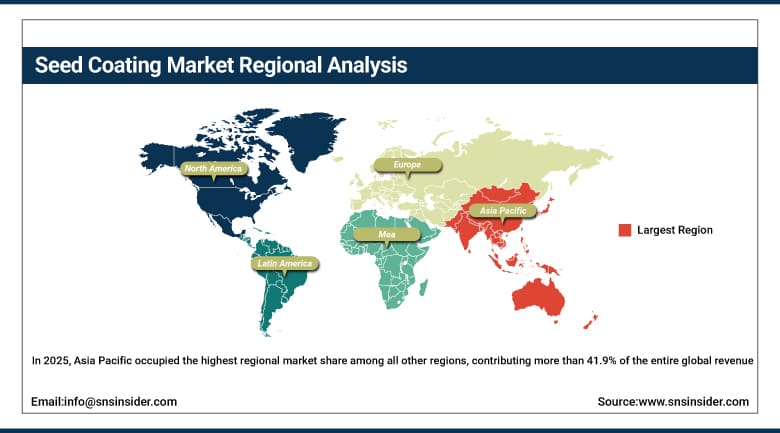

In 2025, Asia Pacific occupied the highest regional market share among all other regions, contributing more than 41.9% of the entire global revenue. The leadership of the region in this industry is largely explained by its massive agriculture system, since the two countries of the region, namely China and India, have some of the most extensive cropping systems in the world. Each of these countries is dealing with more than a hundred million hectares of farmland. The need for feeding the growing population along with the government-led initiatives aimed at developing high-quality seeds is driving a continuous demand for seed coatings from the institutional segment.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Seed Coating Market Insights

North America represents the second-largest market on a regional basis for coated seeds, in addition to being one of the regions with high technological advancement and innovations within this field. The United States is the leading country in the North American region due to a well-developed commercial agriculture industry, adoption of precision farming methods, and presence of key international players within the agrochemical and seed industries such as BASF, Bayer, Corteva, and Syngenta, who have established their formulation facilities in North America.

Europe Seed Coating Market Insights

The European region is characterized by the presence of a fully developed and technologically advanced seed coating industry owing to the presence of robust regulation regimes, strict environmental considerations, and adequate funding for agricultural research. The leading market in this region is Germany because the country is home to some of the biggest firms engaged in coating technologies and scientific advances in the area of biodegradable polymer-based coatings and biological seed coating technologies. Restrictions set up by the regulators of several countries in Europe regarding the usage of neonicotinoids in seed treatments have promoted innovation and adoption of biological-based coatings in Europe.

Latin America and Middle East & Africa Seed Coating Market Insights

The Latin American region can be considered an increasingly significant market for seed coating products, with Brazil being its major market. This is because Brazil is among the countries in the world that boasts one of the biggest and most commercially advanced soybean and corn cultivation industries. Brazilian consumers are aware of the importance of seed treatments and are also big buyers of polymer-based coatings, fungicide treatments, and biological inoculations in the form of seed coatings. The second significant Latin American market is Argentina.

Seed Coating Market Growth Drivers:

-

Rising global demand for higher agricultural productivity and precision farming adoption driving seed treatment investment

The primary motivation behind seed coating is the unceasing quest to grow more food with fewer inputs and resources on a limited amount of farmland. This has been made possible through seed coatings by means of improving the efficiency of germination and providing early protection to the crops, along with delivery of necessary nutrients right to the seeds where required. By doing so, there will be no wastage or runoff of resources like fertilizer or pesticides in large agricultural fields, and instead, they will provide nutrients directly to where they are required.

Government agricultural policies and public research programs are actively reinforcing farmer awareness of the measurable productivity benefits provided by seed coating treatments. Extension services and agricultural universities across North America, Europe, and Asia Pacific are conducting and publishing field trials demonstrating germination improvements, stand establishment benefits, and yield outcomes associated with various coating formulations. This growing body of publicly available agronomic evidence is accelerating adoption among farmers who might otherwise have been hesitant to invest in treated seeds without independent scientific validation.

Seed Coating Market Restraints

-

Regulatory restrictions on chemical active ingredients and stringent approval processes limiting formulation options

The most significant barrier to the growth of the market for seed coatings is the increasing stringent regulatory environment surrounding specific chemicals that traditionally have been widely used in seed treatments. The banning of neonicotinoid insecticides when used as a coating on seeds in the EU has resulted in the need for alternative technologies and solutions, thus posing a challenge for innovation but also impacting demand temporarily in those segments that were affected by such regulations. Approval of any new active substances takes time and resources, delaying innovative seed coatings from reaching the market.

Seed Coating Market Opportunities

-

Expansion of biological and biopolymer-based coatings creating new sustainable product categories aligned with organic farming growth

One of the major growth prospects for the global seed coating industry over the coming years will be the accelerated introduction and adoption of biological and bio-based coating formulations, which comply with the norms and criteria associated with organic farming. Given that the global market for organic foods is expected to see significant growth in the coming years and as farmers are facing increasing pressure to minimize their reliance on chemical products, there will be a huge surge in demand for seed coatings based on natural substances that provide effective protection against pests and weeds.

Recent Developments:

- June 25, 2025 – BASF SE introduced InVigor Gold, an advanced canola seed innovation featuring improved heat tolerance, pod shatter resistance, and enhanced disease resistance for North American farmers.

- 2024 (January): Lucent BioSciences launched NutriGrow, a plant-based, biodegradable seed coating product specifically designed to improve early crop growth and seedling establishment while reducing chemical runoff and overall environmental footprint, targeting the growing market for sustainable seed treatment solutions.

Seed Coating Market Key Players

Some of the Seed Coating Market Companies

-

BASF SE

-

Bayer AG

-

Syngenta Group

-

Corteva Agriscience

-

Germains Seed Technology

-

Precision Laboratories LLC

-

BrettYoung Seeds Limited

-

Centor Oceania

-

Universal Coating Systems

-

Chromatech Incorporated

-

Seed Dynamics, Inc.

-

Summit Seed Coatings

-

Smith Seed Services

-

Seedpoly Biocoatings Pvt. Ltd.

-

Lucent BioSciences

Seed Coating Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.67 Billion |

| Market Size by 2035 | USD 5.67 Billion |

| CAGR | CAGR of 7.82% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Additive (Polymers, Colorants, Pellets & Binders, Active Ingredients) • By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Flowers & Ornamentals, Other Crop Types) • By Form (Liquid, Dry) • By Process (Film Coating, Encrusting, Pelleting) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Bayer AG, Syngenta Group, Corteva Agriscience, Germains Seed Technology, Precision Laboratories LLC, BrettYoung Seeds Limited, Centor Oceania, Universal Coating Systems, Chromatech Incorporated, Seed Dynamics, Inc., Summit Seed Coatings, Smith Seed Services, Seedpoly Biocoatings Pvt. Ltd., Lucent BioSciences |

Get in Touch