Fertilizers Market Report Scope and Overview:

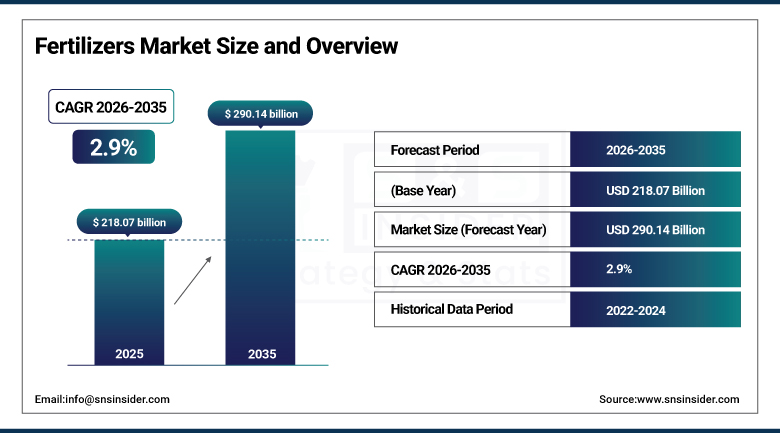

The Fertilizers Market was valued at USD 218.07 Billion in 2025 and is projected to reach USD 290.14 Billion by 2035, registering a CAGR of 2.9% from 2026 to 2035.

Fertilizers whether natural or synthetic in nature are added either to the soil or plant parts for supplying one or more than one nutrients that the plants need for their growth, and the fertilizers market can be considered as one of the cornerstones of the modern agricultural value chain, as it affects the productivity of crops, food security, and sustainability of farming systems around the globe. The growth is mainly being driven by factors like food demand, intensification of agriculture, and increased use of nutrient management systems around the globe, considering that the world's population which is expected to touch nine billion by 2050 as per United Nations.

The transition toward enhanced efficiency fertilizers, including slow-release, controlled-release, and inhibitor-based formulations, continues presenting substantial growth opportunities for manufacturers seeking to differentiate through value-added product portfolios, while the growing demand for specialty fertilizers tailored to specific crops and soil profiles, coupled with digital soil monitoring integrations, continues opening new avenues for technology-driven fertilizer companies throughout 2025.

Market Size and Forecast

- Market Size in 2026E: USD 224.32 Billion

- Market Size by 2035: USD 290.14 Billion

- CAGR: 2.9% from 2026 to 2035

- Fastest Growing Region: MEA

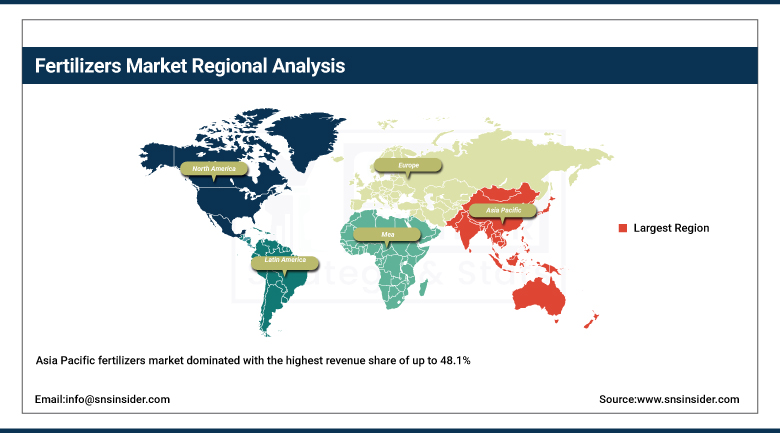

- Largest Region: Asia Pacific

To Get more information Fertilizer Market - Request Free Sample Report

Fertilizers Market Trends

- Increasing focus on soil health, crop quality, and precision farming continues accelerating demand for micronutrient fertilizers addressing specific nutrient deficiencies.

- Growers in regulated regions continue gradually shifting to enhanced-efficiency forms that meet environmental targets without sacrificing yield.

- Growing adoption of precision farming and modern nutrient management practices continues enhancing yield efficiency and fertilizer uptake across major producing regions.

- No-till farming and reduced tillage practices continue gaining traction, leading to increased demand for soil amendments and mycorrhizal fungi products.

- Organic fertilizers continue becoming increasingly widespread as farmers are encouraged to utilize fertilizers more effectively and safely.

The US Fertilizers Market Outlook

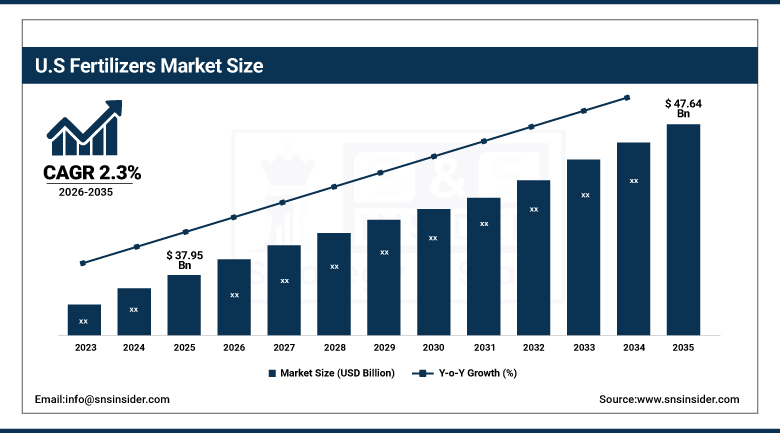

The US Fertilizers Market was valued at approximately USD 37.95 Billion in 2025 and is projected to reach approximately USD 47.64 Billion by 2035, registering a CAGR of approximately 2.3% from 2026 to 2035.

Domestic growth continued being supported by advanced precision farming, adoption of controlled-release fertilizers, and large-scale corn and soybean cultivation throughout the year. The country continued representing a significant share of global fertilizer demand, anchored by well-established agricultural infrastructure and continued investment in nutrient management technology. Rising regulatory pressure on fertilizer manufacturers to reduce their environmental footprint continued encouraging domestic innovation in enhanced efficiency formulations, while volatility of raw material prices continued adding complexity to the domestic market landscape even as underlying agricultural demand remained fundamentally stable.

Nutrien continued expanding its enhanced efficiency fertilizer production capability throughout 2025, targeting American row crop producers seeking slow-release and controlled-release formulations capable of improving nutrient use efficiency while meeting tightening environmental regulatory requirements across major corn and soybean growing regions.

Fertilizers Market Segment Analysis

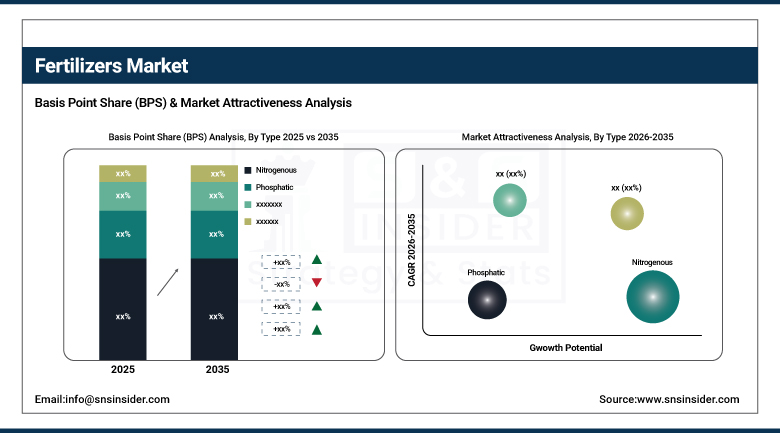

- By Type, nitrogenous led the market with an approximate 38% share in 2025, while micronutrients is the fastest-growing type, tracking a projected 6.6% CAGR.

- By Form, conventional led the market with an estimated 68.4% share in 2025, while specialty is the fastest-growing form, tracking a projected 6.3% CAGR.

- By Application Mode, soil application led the market with an estimated 72.0% share in 2025, while fertigation is the fastest-growing application mode, tracking a projected 6.0% CAGR.

- By Crop Type, cereals and grains led the market with an estimated 42.5% share in 2025, while horticultural crops is the fastest-growing crop type, tracking a projected 7.2% CAGR.

By Type, Nitrogenous led the market, Micronutrients grew fastest

Nitrogenous fertilizers dominated the global market with the highest revenue share of more than 38%. Rising global food demand and the need for high-yield crops continue driving strong consumption of nitrogen-based fertilizers, with their cost-effectiveness and critical role in enhancing staple crop productivity keeping this segment the largest contributor to the global market by a considerable margin.

Micronutrients are the fastest-growing segment with a projected CAGR of 6.6%. Increasing focus on soil health, crop quality, and precision farming continues accelerating demand for micronutrient fertilizers, as these high-value products address specific nutrient deficiencies, supporting premium yields and sustainable farming practices that keep this type category's growth rate climbing well ahead of the broader, still-dominant nitrogenous segment.

By Form, Conventional led the market, Specialty grew fastest

Conventional fertilizers are the largest form and account for up to 68.4% of the fertilizers market size, generally as uncoated granules or prills applied using broadcast spreaders or incorporated into the soil during tillage. That combination of established application methodology and broad agricultural compatibility kept conventional fertilizers the dominant form category by a considerable margin over specialty alternatives.

Specialty fertilizers are anticipated to grow at the fastest CAGR of 6.3% between 2026 and 2035, as growers in regulated regions gradually shift to enhanced-efficiency forms that meet environmental targets without sacrificing yield. That regulatory-driven transition keeps this form category's growth rate climbing well ahead of the broader, still-dominant conventional segment even as conventional forms retain the overwhelming majority of total market volume.

By Application Mode, Soil Application led the market, Fertigation grew fastest

Soil application accounted for the largest share of the fertilizers market, representing up to 72.0% of total revenue. That combination of established agricultural practice and broad crop compatibility kept soil application the dominant application-mode category across the broadest range of farming operations this market serves.

Fertigation is forecast to register the highest growth rate, with a CAGR of 6.0% from 2026 to 2035. As precision irrigation systems continue expanding globally, farmers increasingly adopt fertigation for its ability to deliver nutrients with genuinely greater precision and efficiency than traditional broadcast soil application, keeping this application-mode category's growth rate climbing well ahead of the broader, still-dominant soil application segment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|

Asia Pacific |

China |

39.85% |

|

North America |

United States |

80.40% |

|

Europe |

Germany |

23.75% |

|

Africa |

Nigeria |

22.60% |

|

Latin America |

Brazil |

44.30% |

North America Fertilizers Market Insights

North America held a substantial share of global revenue, with the region representing approximately 17.41% of global demand and supported by advanced precision farming, adoption of controlled-release fertilizers, and large-scale corn and soybean cultivation across the continent. That combination of established agricultural infrastructure and continued technology adoption kept North America a genuinely significant contributor to global fertilizer demand throughout the year.

The United States accounted for roughly 80.40% of regional revenue, anchored by large-scale corn and soybean cultivation and advanced precision farming technology adoption. Canada added further regional demand through its own substantial grain production sector, and that combined strength kept North America among the largest addressable regional markets for fertilizer vendors through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Fertilizers Market Insights

Europe held a meaningful share of global revenue, supported by increasing regulatory pressure on fertilizer manufacturers to reduce their environmental footprint and continued adoption of enhanced efficiency formulations across the region's major agricultural economies. Growing emphasis on sustainable farming practices kept reinforcing steady European demand for specialty and low-impact fertilizer products throughout the year.

Germany led demand at roughly 23.75% of European revenue, supported by its substantial agricultural production base. France and other major European agricultural producers contributed substantial additional demand, and continued European regulatory emphasis on environmental compliance should keep shaping regional demand patterns through the forecast period.

Asia Pacific Fertilizers Market Insights

Asia Pacific fertilizers market dominated with the highest revenue share of up to 48.1%, driven by rising population, expanding commercial agriculture, and high crop intensity in major markets like India and China. Growing adoption of precision farming and modern nutrient management practices continues enhancing yield efficiency and fertilizer uptake, keeping the region firmly positioned as the market's clear leader by a considerable margin.

China continues to lead global fertilizer consumption due to its intensive cereal cultivation and population-driven food demand, with government initiatives focused on food security continuing to reinforce sustained domestic fertilizer investment. India and Southeast Asian economies contributed meaningful additional demand, with rice production concentration and rapid agricultural intensification continuing to reinforce Asia Pacific's structural leadership in both production and consumption.

MEA Fertilizers Market Insights

Africa is projected to be the fastest-growing regional market, advancing at a meaningful pace as expanding commercial agriculture, growing food security initiatives, and rising fertilizer adoption across historically underserved farming regions continue driving regional growth well ahead of every other region tracked in this report. Latin America continued showing steady, substantial growth over the same period, anchored by large-scale commercial agriculture.

Nigeria led African demand, supported by growing government food security initiatives and expanding commercial agriculture investment. Other major African agricultural economies contributed further demand through their own agricultural modernization programs. In Latin America, Brazil accounted for the largest share of regional revenue, with its position as a leading global soybean and grain exporter continuing to anchor substantial regional demand for fertilizers.

Market Dynamics

Growth Drivers: Global Population Growth and Food Security Imperatives

Growth continues being primarily attributed to rising food demand, agricultural intensification, and increasing adoption of advanced nutrient management practices worldwide. Increased agricultural output and growing demand for improved soil nutrients continue further raising fertilizer demand, as the world's population, projected to top nine billion by 2050, continues driving sustained need for high-yield agricultural production.

Government initiatives focused on food security continue reinforcing this driver across major agricultural economies, as nations increasingly prioritize domestic food production capacity amid growing global population and changing dietary patterns. That combination of genuine demographic necessity and expanding government policy support is exactly what keeps demand climbing steadily across virtually every major agricultural region this market serves.

Restraints: Raw Material Price Volatility and Environmental Regulatory Pressure

The volatility of raw material prices continues adding genuine complexity to the market landscape, as fertilizer production costs remain directly exposed to broader energy and mineral commodity market fluctuations that manufacturers can't always pass through to farmers without demand destruction risk. That price sensitivity keeps long-term supply and pricing agreements genuinely complicated to negotiate.

Increasing regulatory pressure on fertilizer manufacturers to reduce their environmental footprint continues posing a further restraint, as tightening emissions and runoff standards require genuine investment in enhanced efficiency formulation technology that traditional conventional fertilizer production simply wasn't designed to meet. That compliance burden keeps operational costs elevated for producers transitioning toward increasingly stringent environmental standards.

Opportunities: Enhanced Efficiency Formulation Development and Precision Agriculture Integration

The transition toward enhanced efficiency fertilizers, including slow-release, controlled-release, and inhibitor-based formulations, represents a genuinely significant opportunity for manufacturers seeking to differentiate through value-added product portfolios. Vendors offering genuinely proven, environmentally compliant enhanced efficiency technology stand to capture meaningful share as regulatory pressure and grower sustainability commitments continue expanding this category's addressable market.

Growing demand for specialty fertilizers tailored to specific crops and soil profiles, coupled with digital soil monitoring integrations, offers a second substantial opportunity, as precision agriculture technology continues enabling increasingly targeted, efficient nutrient application. Vendors that can deliver genuinely integrated, technology-driven fertilizer solutions stand to capture meaningful share as farmers increasingly prioritize precision over traditional broad-application approaches.

Recent Developments:

- 2025: Yara International continued expanding its precision nutrient management and digital farming platform, targeting large-scale grain producers seeking data-driven fertilizer application optimization capability.

- 2025: The Mosaic Company continued advancing its enhanced efficiency phosphate and potash fertilizer product line, targeting row crop producers seeking improved nutrient use efficiency and reduced environmental runoff.

- 2024: CF Industries continued expanding its low-carbon nitrogen fertilizer production capability, targeting customers seeking sustainably produced ammonia-based fertilizers with reduced greenhouse gas emissions.

Fertilizers Market key players are:

- Nutrien Ltd.

- Yara International ASA

- The Mosaic Company

- CF Industries Holdings, Inc.

- EuroChem Group AG

- ICL Group Ltd.

- OCI N.V.

- K+S Aktiengesellschaft

- PhosAgro PJSC

- Uralkali PJSC

- Sociedad Química y Minera de Chile S.A.

- Coromandel International Limited

- Indian Farmers Fertiliser Cooperative Limited

- Sinofert Holdings Limited

- Compass Minerals International, Inc.

- Haifa Group

- ArrMaz Products, Inc.

- Yunnan Yuntianhua Co., Ltd.

- Wengfu Group Co., Ltd.

- Kingenta Ecological Engineering Group Co., Ltd.

Fertilizers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 218.07 Billion |

| Market Size by 2035 | USD 290.14 Billion |

| CAGR | CAGR of 2.9% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Nitrogenous, Phosphatic, Potassic, Micronutrients) • By Form (Conventional, Specialty) • By Application Mode (Soil Application, Foliar, Fertigation) • By Crop Type (Cereals and Grains, Oilseeds and Pulses, Horticultural Crops) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nutrien Ltd., Yara International ASA, The Mosaic Company, CF Industries Holdings, Inc., EuroChem Group AG, ICL Group Ltd., OCI N.V., K+S Aktiengesellschaft, PhosAgro PJSC, Uralkali PJSC, Sociedad Química y Minera de Chile S.A., Coromandel International Limited, Indian Farmers Fertiliser Cooperative Limited, Sinofert Holdings Limited, Compass Minerals International, Inc., Haifa Group, ArrMaz Products, Inc., Yunnan Yuntianhua Co., Ltd., Wengfu Group Co., Ltd., and Kingenta Ecological Engineering Group Co., Ltd. |

Frequently Asked Questions

The Fertilizers Market is expected to grow at a CAGR of approximately 2.9% from 2026 to 2035, based on triangulated secondary research estimates.

The Fertilizers Market was valued at approximately USD 218.07 Billion in 2025, based on triangulation across multiple independent research sources.

The major growth factor is rising food demand, agricultural intensification, and increasing adoption of advanced nutrient management practices worldwide.

The Nitrogenous segment dominated the Fertilizers Market by type, representing an estimated 38% of revenue in 2025.

Asia Pacific dominated the Fertilizers Market in 2025, holding an estimated 50% share of total global market revenue.

Get in Touch