Semiconductor Gas Abatement Systems Market Size & Growth:

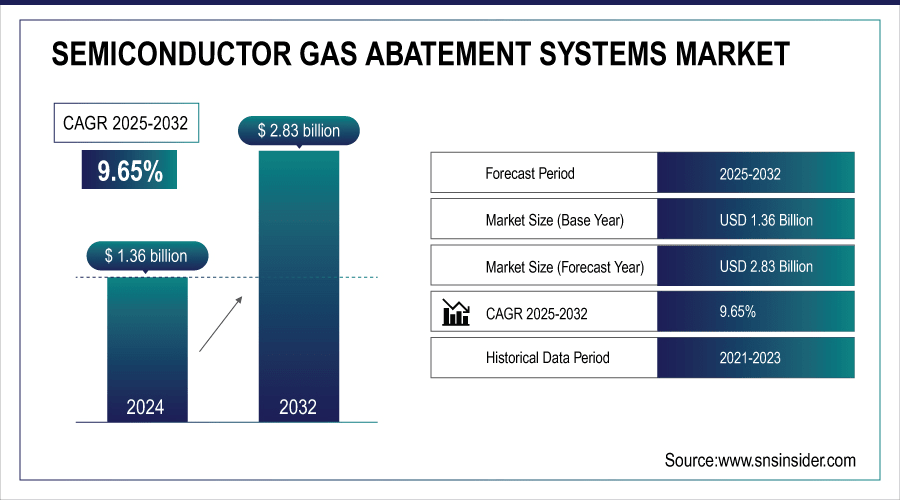

The Semiconductor Gas Abatement Systems Market Size was valued at USD 1.36 Billion in 2024 and is expected to reach USD 2.83 Billion by 2032 and grow at a CAGR of 9.65% over the forecast period 2025-2032.

The primary growth driver of the Semiconductor Gas Abatement Systems Market is the rapid expansion of semiconductor manufacturing facilities globally, particularly in Asia-Pacific, which is driving high demand for advanced gas abatement solutions. As semiconductor nodes shrink and production processes become more complex, the volume and variety of hazardous process gases, such as fluorinated and silane-based compounds have increased. Regulatory mandates for environmental compliance and worker safety are further compelling fabs to adopt efficient abatement systems, including combustion, scrubbers, and catalytic technologies, to minimize harmful emissions and meet strict local and international standards. According to study, TSMC aims to achieve a monthly production capacity of 45,000 to 50,000 wafers by the end of the year.

Semiconductor Gas Abatement Systems Market Size and Forecast:

-

Market Size in 2024 USD 1.36 Billion

-

Market Size by 2032 USD 2.83 Billion

-

CAGR of 9.65% From 2025 to 2032

-

Base Year 2024

-

Forecast Period 2025-2032

-

Historical Data 2021-2023

To Get More Information On Semiconductor Gas Abatement Systems Market - Request Free Sample Report

Semiconductor Gas Abatement Systems Market Trends

-

Rapid growth of semiconductor fabs is driving demand for advanced gas abatement systems.

-

Shrinking nodes and complex processes generate higher volumes of hazardous gases.

-

Regulatory mandates for emissions and worker safety are accelerating adoption.

-

High-efficiency systems for sub-7nm processes are increasingly required.

-

Energy-efficient and hybrid systems optimize treatment and reduce operational costs.

-

Focus on sustainability and green manufacturing is boosting investments.

-

R&D and pilot fabs adopting advanced processes are creating new opportunities.

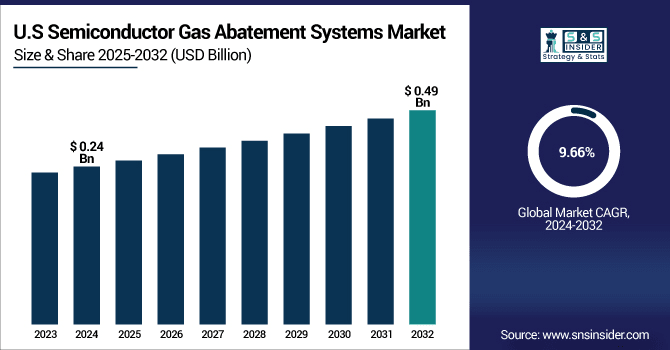

The U.S. Semiconductor Gas Abatement Systems Market size was USD 0.24 Billion in 2024 and is expected to reach USD 0.49 Billion by 2032, growing at a CAGR of 9.66% over the forecast period of 2025-2032. driven by increasing domestic semiconductor manufacturing and rising demand for advanced electronic devices. Stringent environmental regulations mandate the use of efficient abatement technologies to control hazardous emissions from fabs, while technological advancements such as IoT sensors and AI-driven diagnostics are improving system efficiency and performance.

Semiconductor Gas Abatement Systems Market Growth Drivers:

-

Rapid Expansion of Semiconductor Manufacturing Facilities

The primary driver for the market is the rapid growth of fueled by increasing demand for advanced electronic devices and next-generation semiconductors. With semiconductor nodes shrinking, and processes getting more complicated, huge amounts of hazardous process gases are vented by a fab including fluorinated and silane-based compounds. These gases are among the most hazardous and need strict environmental management. The need for worker safety and emission limits is spurring fabs to implement superior abatement solution, including combustion systems, wet scrubbers, and catalytic units, driven by regulatory mandates from governments. Furthermore, the demand for advanced semiconductor manufacturing for mobile, AI and high-performance computing sectors continues to drive the need for densely configured, high-efficiency abatement systems designed to manage smaller process footprints at lower energy consumption levels.

Advanced nodes (sub-7nm) produce 2–3 times higher volumes of hazardous gases per wafer compared to older nodes,

Semiconductor Gas Abatement Systems Market Restraints:

-

High Initial Capital and Operational Costs

The high installation and maintenance cost of gas abatement systems, which has been a key constraint. Semiconductor abatement systems are ambitious technologies, including thermal oxidation, plasma abatement, dry scrubbing that require significant capital investment and high OPEX, including energy, spare parts, consumables (like filters), and sodas (in the case of dry scrubbing). Adoption rates can be slowed down due to cost as small and medium-sized fabs (and R&D facilities) may struggle to pencil out the budget to obtain these systems. Furthermore, older fabs may be unable to integrate modern abatement without expensive retrofitting of existing production lines which would also lead to costs and possible downtime of the fab, both of which restricts the penetration of the market in cost-sensitive regions.

Semiconductor Gas Abatement Systems Market Opportunities:

-

Adoption of Energy-Efficient and Hybrid Abatement Systems

The market has a significant opportunity in the adoption of energy-efficient, modular, and hybrid abatement solutions. Hybrid systems combine centralized and point-of-use (POU) functionalities, enabling fabs to optimize gas treatment, reduce footprint, and save energy costs. The increasing emphasis on sustainability and green manufacturing is pushing semiconductor companies to invest in abatement systems that lower environmental impact while meeting regulatory standards. Additionally, with the rise of R&D facilities and pilot fabs exploring advanced processes like ALD and next-generation CVD, there is a growing demand for flexible and scalable abatement solutions, creating new avenues for market growth.

Semiconductor fabs implementing green manufacturing practices have reported up to 25% reduction in hazardous gas emissions when adopting modular or hybrid abatement solutions.

Semiconductor Gas Abatement Systems Market Segment Analysis

-

By Type, Combustion Type accounted for around 38.10% of the market in 2024, while Dry Scrubber Type emerged as the fastest-growing segment with a CAGR of 11.40%.

-

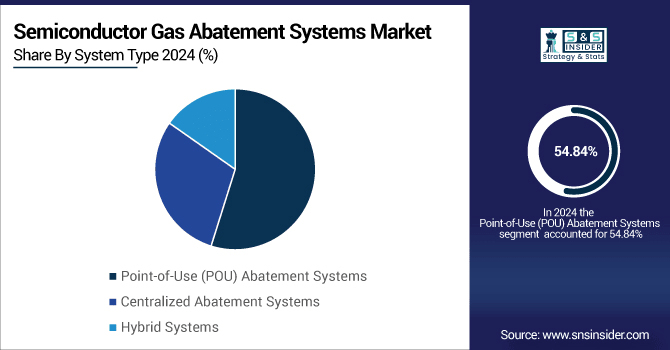

By System Type, Point-of-Use (POU) Abatement Systems solutions dominated with about 54.84% share in 2024, whereas Hybrid Systems is witnessing the fastest growth at a CAGR of 11.00%.

-

By Application, Chemical Vapor Deposition (CVD) led the market with nearly 45.08% share in 2024, while Atomic Layer Deposition (ALD) are projected to grow fastest with a CAGR of 11.00%.

-

By End-User, the Semiconductor Manufacturing Plants sector held the largest share at 70.05% in 2024, with Research and Development Facilities expected to be the fastest-growing vertical at a CAGR of 10.49%.

By System Type, Point-of-Use (POU) Abatement Systems Leads Market While Hybrid Systems Fastest Growth

Point-of-Use (POU) abatement systems continue to dominate the market, as these systems are often implemented in fabs to address the need for on-site, near-tool treatment of hazardous process gases. The clear choice in this type of system is especially dominant in areas with an established semiconductor manufacturing base where regulatory compliance and safety protocols demand very specific, local area abatement response. Region wise, the fastest growth globally for hybrid systems. Hybrid solutions bring together centralized and POU features, providing flexibility and energy efficiency and making them a good fit for both new fabs and R&D environments. In general, global market dynamics are starting to move toward more energy-efficient, flexible, and sustainable abatement technologies, as hybrid systems are positioned to capture a significant share of market growth across a range of applications.

By Type, Combustion Type Leads Market While Dry Scrubber Type Platforms Fastest Growth

Due to their efficiency in high gas flow rates and ability to meet stringent emission regulation, combustion type systems lead the market in this region. In contrast, North America and Europe enjoy consistent demand, fueled by regulatory mandates, innovation, and sustainability initiatives in their respective legacy semiconductor hubs. In terms of growth trends, dry scrubber type platforms are likely to grow the fastest in thousands in the emerging fabs and R&D centers. With such advantages like lower operating costs, modularity of deployment and incompatibility with next generation semiconductor processes, these systems are becoming ever more interesting for larger or even POU centralized applications. The global transition towards energy-efficient and hybrid abatement systems spans all the regions, demonstrating an industry-wide pursuit of sustainability, operational efficiency and meeting more stringent regulations.

By Application, Chemical Vapor Deposition (CVD) Market While Atomic Layer Deposition (ALD) Fastest Growth

The Chemical Vapor Deposition (CVD) segment dominates the market worldwide as it is widely used in high volume semiconductor production as well as the large quantity of toxic process gases produced during its process. CVD processes are key to thin film deposition for the new semiconductor nodes thus requiring high performance gas abatement systems to comply with regulatory limits and ensure safety from exposer to humans. Most of the CVD demand enabled by established fabs with ongoing investment, next-gen semiconductor tech. growth and tight environmental regulation Global ALD is expected to grow at the fastest CAGR as compared to its counterparts. Atomic Layer Deposition (ALD) is widely used in all the advanced R&D facilities and pilot fabs for accurate thin-film deposition in the sub-7nm technology nodes for the semiconductors. In general, the trend is to support vapour abatement systems that are scalable and sustainable in nature, suitable for high-volume production and higher (R&D) applications.

By End-User, Semiconductor Manufacturing Plants Leads Market While Research and Development Facilities Fastest Growth

Semiconductor Manufacturing Plants segment dominates the market in all the regions, being the high-volume production segment which produces significant amounts of hazardous process gases. To begin with, large fabs have stringent regulatory requirements to meet, especially for worker and environmental safety, and could be made compliant through advanced abatement systems, namely combustion, scrubbers, catalytic solutions, and the like. In contrast, the R&D Facilities is poised to record the highest growth worldwide. Novel fabs, pilot plants, and R&D centers need flexible, modular, and energy-saving gas abatement systems to ensure they can manage experimental processes, such as ALD and advanced CVD. The adaptability of ensuring R&D from the collaboration of localized resources is propelling this segment to witness faster growth in emerging regions such as around the newer parts of Latin America and the Middle East. This trend focuses on scalable, agile, and green abatement that can help enable production in semiconductor fabrication while concurrently allowing an environment for innovation.

North America Semiconductor Gas Abatement Systems Market Insights:

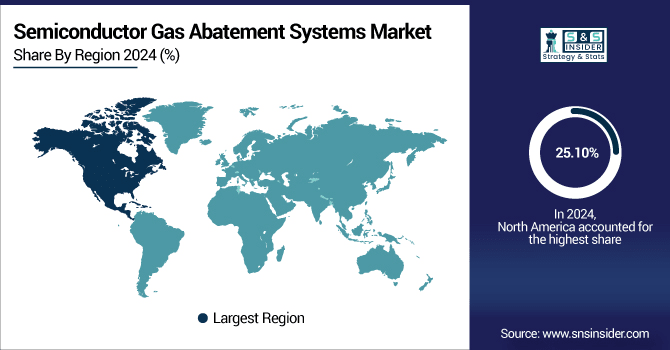

In 2024, North America is expected to lead over other regions by contributing a major share 25.10%, Semiconductor Gas Abatement Systems Market, due to presence of established semiconductor manufacturing centers, stringent regulatory standards, and advanced technology. Advanced semiconductor processes such as ALD & CVD, as well as sub-7nm nodes, produce hazardous gases and the region's fabs are focused on energy-efficient solutions that are also modular and hybrid to deliver effective abatement.

Get Customized Report as Per Your Business Requirement - Enquiry Now

U.S. Leads Semiconductor Gas Abatement Systems Market with Policy Support and Technological Adoption:

The U.S. leads the region due to strong government initiatives, such as the CHIPS and Science Act, which boost domestic semiconductor manufacturing. Point-of-use (POU) and hybrid abatement systems are increasingly being deployed by larger fabs and R&D facilities, with the addition of IoT sensors and AI-driven diagnostics to efficiently treat gas streams, maintain compliance, and drive operational improvements. Key sectors target high-throughput semiconductor volume manufacturing, pilot fabs and specialty materials.

Asia-Pacific Semiconductor Gas Abatement Systems Market Insights:

In 2024, Asia-Pacific will continue to lead the world market share 10.02%, bolstered by strong semiconductor fab growth, high-volume production and advancing next-generation semiconductor processes. The industry sectors leading the way in the front end are China, South Korea, Taiwan, Japan, Singapore, and Malaysia as they require the large-scale combustion, scrubber, and catalytic abatement systems to handle the hazardous gas effluents.

China, South Korea, and Taiwan Drive Rapid Growth in Semiconductor Gas Abatement Systems Market:

China countries is fueled by high-volume semiconductor production, technological advancement, and adoption of hybrid and energy-efficient abatement solutions. Demand for the expansion of R&D facilities and pilot fabs and sustainability and regulatory compliance will also help project the market forward. The growing adoption of flexible and scalable gas abatement systems, is also driven by emerging hubs like India and Malaysia.

Europe Semiconductor Gas Abatement Systems Market Insights

In 2024, Europe accounted for a healthy share of the Semiconductor Gas Abatement Systems Market over 12.08, owing to presence of established semiconductor hubs, sound environmental regulations supporting operational efficiency and sustainability. Specifically, Germany, France, and the Netherlands dominated in the uptake of energy-efficient modular and hybrid gas abatement systems to handle harmful gases produced during advanced semiconductor processes such as at ALD, CVD, and the sub-7nm nodes.

Germany Leads Europe in Semiconductor Gas Abatement Systems Market Growth

Germany and the Netherlands and France are at the forefront of the regional market growth high adoption of point-of-use (POU) and hybrid abatement systems, deployment of IoT sensors, and AI-based diagnostics that can optimize gas treatment, minimize operational footprint, and maintain compliance standards. Developed and technologically advanced market with maturity expansion of R&D centers and pilot fabs further stimulates the need for flexible and scalable abatement solutions reinforcing Europe as mature market.

Latin America and Middle East & Africa Semiconductor Gas Abatement Systems Market Insights

In 2024, Latin America and the Middle East & Africa represent emerging markets for Semiconductor Gas Abatement Systems, driven by the development of semiconductor manufacturing facilities, R&D centers, and specialty material production. Key countries such as Brazil, Mexico, Argentina, the United Arab Emirates, Saudi Arabia, and South Africa are increasingly investing in modular, hybrid, and point-of-use (POU) abatement systems to efficiently manage hazardous gases while optimizing energy consumption. Market growth in these regions is supported by government initiatives promoting technological infrastructure, environmental compliance, and sustainable manufacturing practices, as well as the rising adoption of flexible and scalable solutions for pilot fabs and smaller production lines.

Semiconductor Gas Abatement Systems Market Competitive Landscape

Ebara Corporation introduced its LPCMN-type combustion-based exhaust gas abatement system, designed to detoxify process gases in semiconductor manufacturing. The system offers high destruction efficiency for hard-to-decompose gases and minimizes NOx and COx emissions, supporting environmental compliance in semiconductor fabs.

-

In December 2024, Ebara announced the launch of the LPCMN-type combustion-type exhaust gas abatement system, with sales starting in January 2025.

Baker Hughes delivered an integrated gas recovery and hydrogen sulfide (H₂S) removal system at SOCAR’s Baku Oil Refinery. The system recovers flare gas equivalent to 7 million Nm³ of methane annually and reduces CO₂ emissions by up to 11,000 tons, enhancing refinery efficiency and sustainability.

-

In November 2024, Baker Hughes implemented the integrated gas recovery and H₂S removal system to reduce routine flaring and improve environmental performance at SOCAR’s refinery.

Cefla S.C. continued providing semiconductor gas abatement equipment and services to support sustainable manufacturing practices. Its ongoing solutions help semiconductor manufacturers maintain environmental compliance and energy efficiency.

-

In July 2024, Cefla S.C. expanded its offerings in gas abatement systems, reinforcing its role in sustainable semiconductor production.

Semiconductor Gas Abatement Systems Companies are:

-

Edwards Vacuum (Atlas Copco Group)

-

Ebara Corporation

-

Shin Nippon Air Technologies (SNK)

-

Kanken Techno Co., Ltd.

-

Centrotherm Clean Solutions GmbH & Co. KG

-

Praxair Technology, Inc. (Linde plc)

-

Baker Hughes Company

-

Applied Materials, Inc.

-

Lam Research Corporation

-

Tokyo Electron Limited (TEL)

-

Hitachi High-Tech Corporation

-

Global Standard Technology (GST)

-

UNISEM Co., Ltd.

-

CS Clean Solutions AG

-

EcoSys Corp.

-

Mott Corporation

-

Ares Corporation

-

Mathews International Corporation

-

Cefla S.C.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.36 Billion |

| Market Size by 2032 | USD 2.83 Billion |

| CAGR | CAGR of 9.65% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Combustion Type, Wet Scrubber Types, Dry Scrubber Type, Catalytic Type) • By System Type (Point-of-Use (POU) Abatement Systems, Centralized Abatement Systems, Hybrid Systems) • By Application (Chemical Vapor Deposition (CVD), Atomic Layer Deposition (ALD), Etching, Diffusion) • By End-User (Semiconductor Manufacturing Plants, Research and Development Facilities, Specialty Material Producers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Edwards Vacuum (Atlas Copco Group), Ebara Corporation, Shin Nippon Air Technologies (SNK), Kanken Techno Co., Ltd., Centrotherm Clean Solutions GmbH & Co. KG, Praxair Technology, Inc. (Linde plc), Air Liquide S.A., Baker Hughes Company, Applied Materials, Inc., Lam Research Corporation, Tokyo Electron Limited (TEL), Hitachi High-Tech Corporation, Global Standard Technology (GST), UNISEM Co., Ltd., CS Clean Solutions AG, EcoSys Corp., Mott Corporation, Ares Corporation, Mathews International Corporation, Cefla S.C., and Others. |

Frequently Asked Questions

Asia Pacific dominated the Semiconductor Gas Abatement Systems Market in 2024.

The Combustion Type segment dominated the Semiconductor Gas Abatement Systems Market.

The major growth factor of the Semiconductor Gas Abatement Systems Market is the rapid expansion and technological advancement of semiconductor manufacturing facilities, which generate increasing volumes of hazardous process gases.

The Semiconductor Gas Abatement Systems Market size was USD 1.36 billion in 2024 and is expected to reach USD 2.83 billion by 2032.

The Semiconductor Gas Abatement Systems Market is expected to grow at a CAGR of 9.65% during 2025-2032.

Get in Touch